What To Watch Today

Earnings Economy

Economy

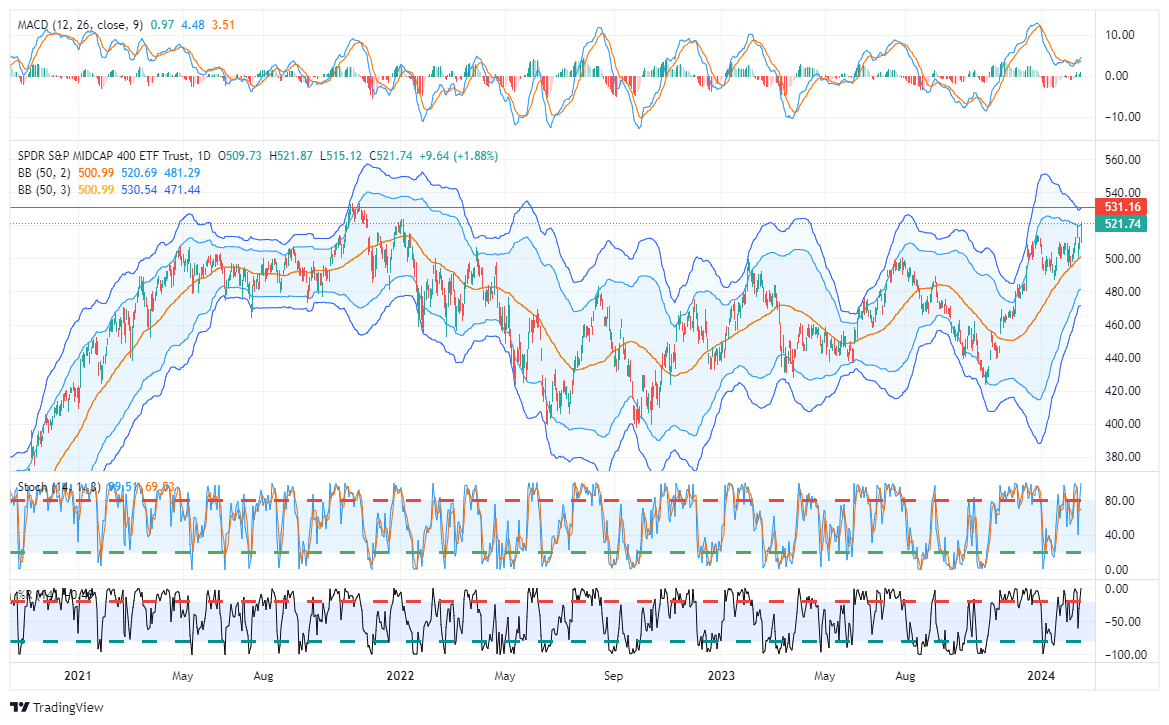

Market Trading Update

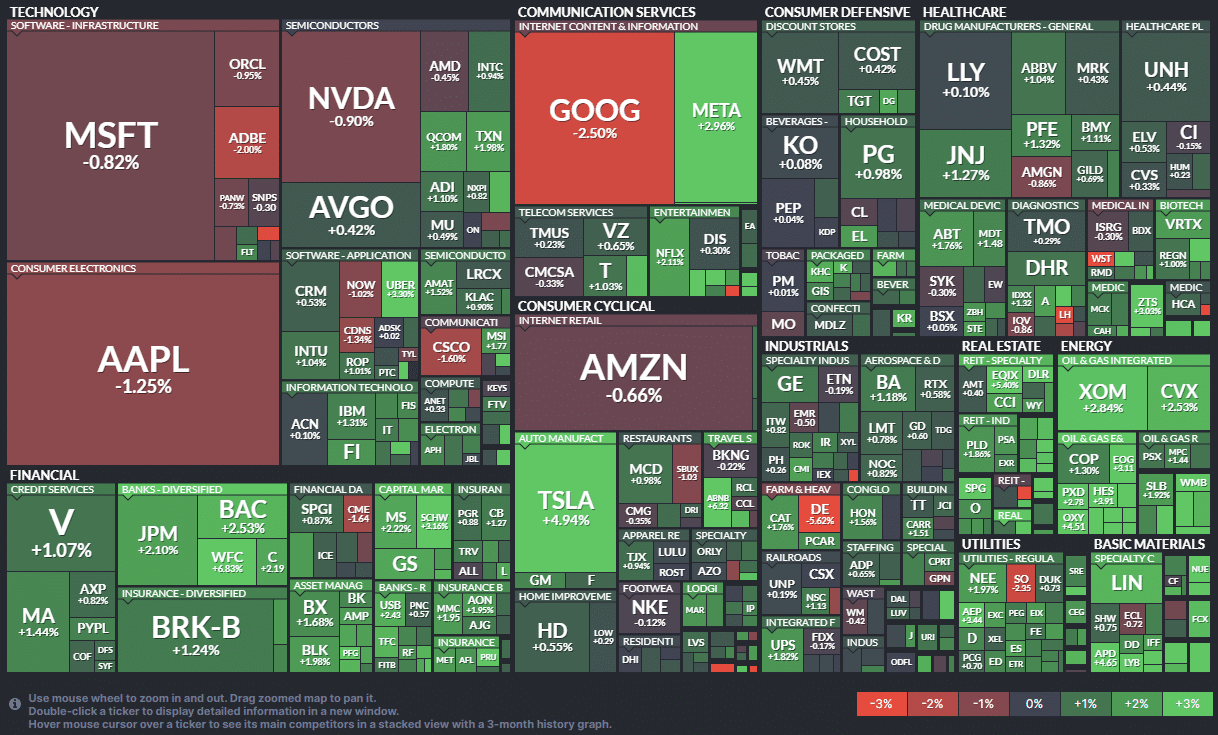

Yesterday’s commentary noted that the bullish trend remains intact, with the market holding near-term support. To wit:“The market rebounded off the 20-DMA average yesterday, keeping the bull trend intact for now. The market bounced off the 20-DMA and slightly reduced the overbought condition. Such keeps the current trend positive, keeping equity allocations near full weight. However, the internals continue to weaken, and the market is close to registering a sell signal from an elevated level. Furthermore, the deviation from the 200-DMA remains quite large, likely limiting further upside until a more significant correction occurs to reduce the extension.”Such remained the case yesterday, with the rally challenging recent highs. What was notable in that rally was that the “Magnificent 7” were NOT in charge. Instead, as shown in the heat map below, Financials, Energy, Healthcare, and Utilities were rising decently.

While this was not enough to reverse recent breadth issues, seeing some rotation in the markets was encouraging. This is a healthy change. As we have discussed recently, two ways exist to correct some of the more egregious overbought conditions in the market. The first is a correction that reverses the price. The second is a consolidation, where a rotation from leaders to laggards works off some of the overbought issues. It is too early to tell if a rotational consolidation is in process; yesterday’s action was encouraging.

Notably, mid-cap stocks, which got slaughtered on Tuesday, reversed all those losses and set a new high for the week. We are watching mid-caps closely, which are currently extremely overbought but are lagging performance relative to the S&P. Mid-caps are close to potentially setting a new all-time high to join their large-cap brethren. If such is the case, we will look to increase our exposure to some of those names.

While this was not enough to reverse recent breadth issues, seeing some rotation in the markets was encouraging. This is a healthy change. As we have discussed recently, two ways exist to correct some of the more egregious overbought conditions in the market. The first is a correction that reverses the price. The second is a consolidation, where a rotation from leaders to laggards works off some of the overbought issues. It is too early to tell if a rotational consolidation is in process; yesterday’s action was encouraging.

Notably, mid-cap stocks, which got slaughtered on Tuesday, reversed all those losses and set a new high for the week. We are watching mid-caps closely, which are currently extremely overbought but are lagging performance relative to the S&P. Mid-caps are close to potentially setting a new all-time high to join their large-cap brethren. If such is the case, we will look to increase our exposure to some of those names.

Retail Sales

January retail sales fell 0.8%, worse than the consensus estimate of a 0.1% decline. Last month’s red hot gain of +0.8% was revised lower to +0.4%. Retail Sales, excluding automobile sales, were -0.6% versus estimates of an increase of +0.3%. The control number, which feeds GDP, was -0.4%. The following summary is courtesy of Pantheon Macro:This report is remarkably downbeat, with an unexpectedly sharp plunge in total sales, significant downward revisions .. and only a few signs of light in the details. .. Are consumers starting to tire?”While drawing assumptions from the report is easy, we offer caution. December and January data are skewed due to the holidays and the seasonal adjustments made to the data. We want to see a few more months of weak consumer activity before declaring consumers are starting to tire.

Answering A Reader Question On Rent Inflation

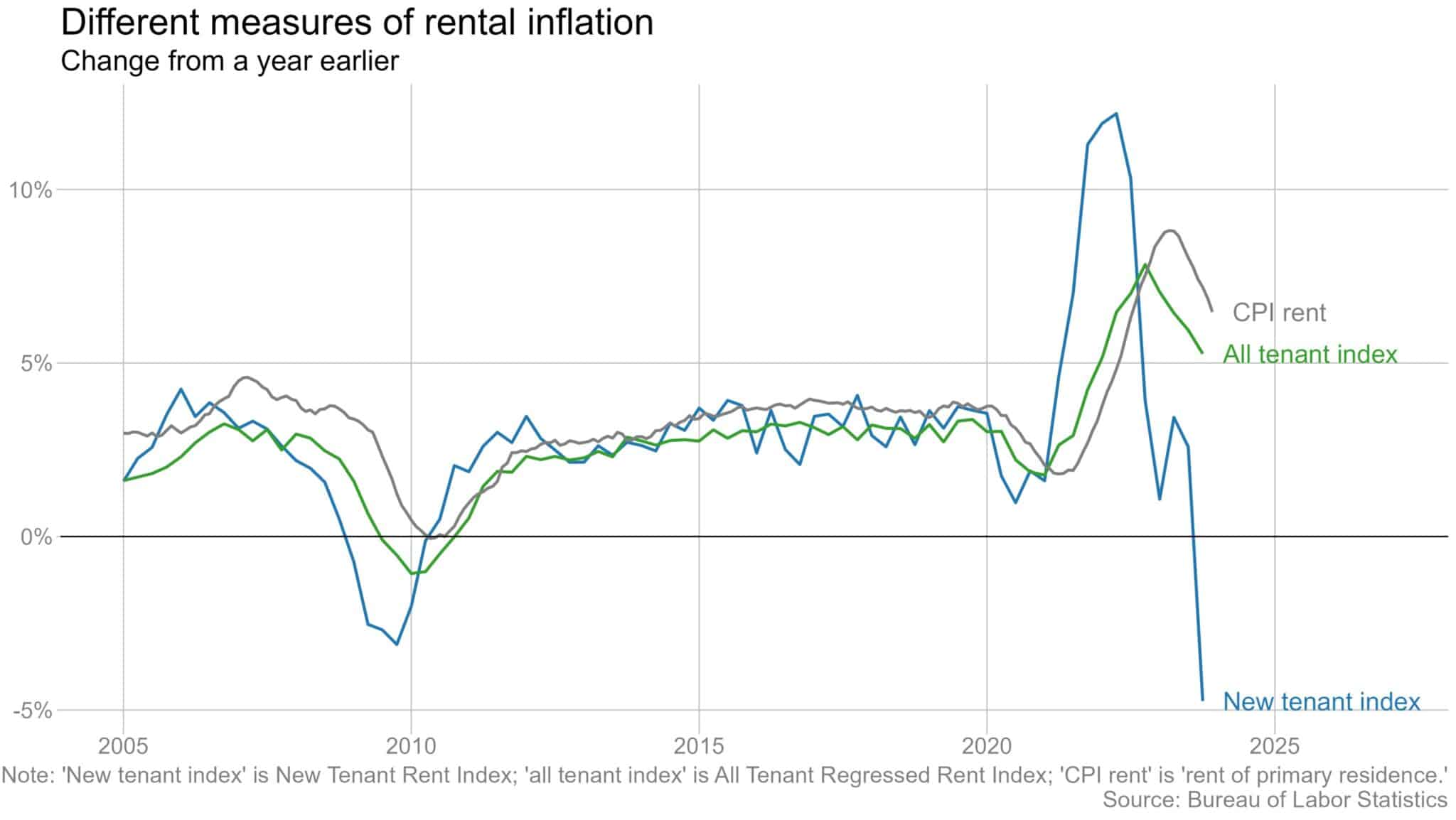

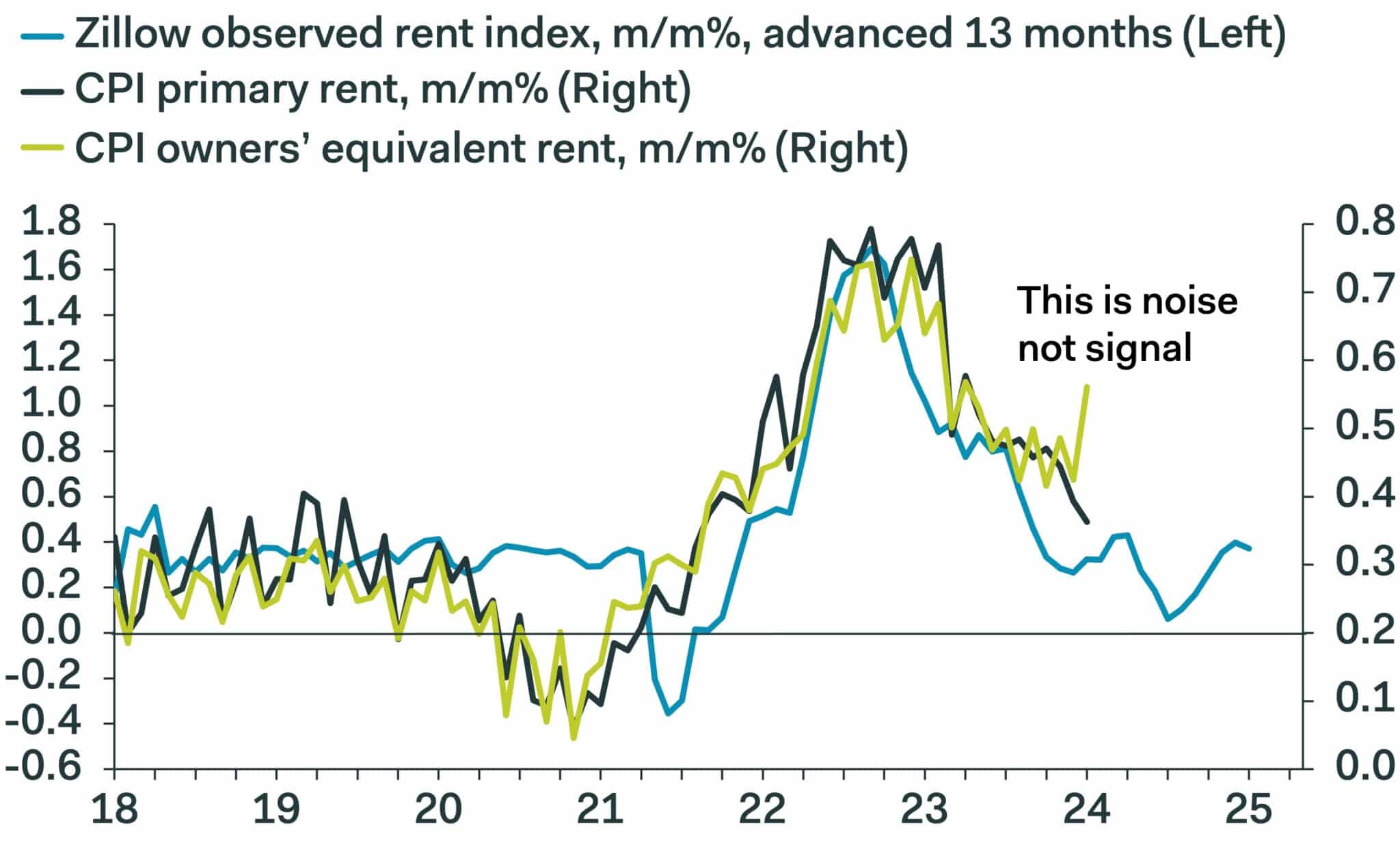

A reader asked if we could further detail why CPI rent prices are flawed and why that is an important reason that we (RIA) are not worrying about Tuesday’s CPI data. Shelter costs (OER and actual Rent) are the most crucial variable in the CPI’s largest category. Therefore it is the most significant driver of inflation. CPI shelter prices are well above market prices. The reason is the lag embedded in the BLS calculations. Further, the BLS imputes rents in its owner’s equivalent rent (OER), which can be faulty due to seasonal effects. CPI Rent lags market rents because it doesn’t fully factor in today’s actual rents for new lease signings. Instead, it measures the change in rent among all renters. Given most rents expire annually, over 90% of renters in any month are un-expiring leases. Accordingly, their rent doesn’t change. Also consider the CPI surveys the same renters once every six months. Therefore, if your rent changes a month after the last survey, the new rent is not captured for five months. The first graph below shows the BLS measurement of new tenant rental inflation, which is down over 4% from a year ago. Unfortunately, the BLS only publishes this data every six months. The next report will be in April. The second graph shows the downward trend in the CPI’s measure of rent inflation. The third graph is from Ian Shepherdson. Clearly, OER (imputed rent) is askew from actual rental prices and the BLS rent measure. The bottom line is that we think the lag effect and the odd OER data account for the increase. When they correct, CPI will fall accordingly.

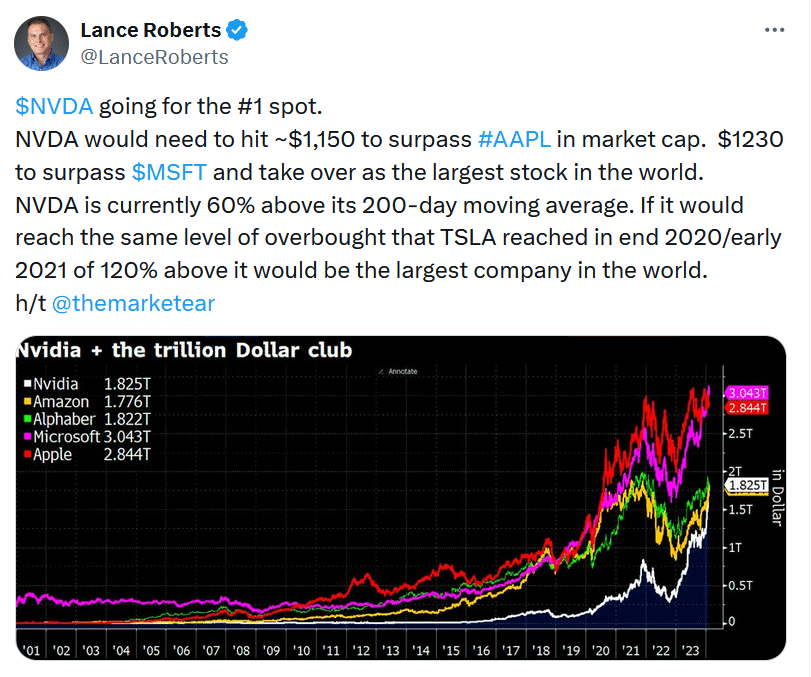

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.