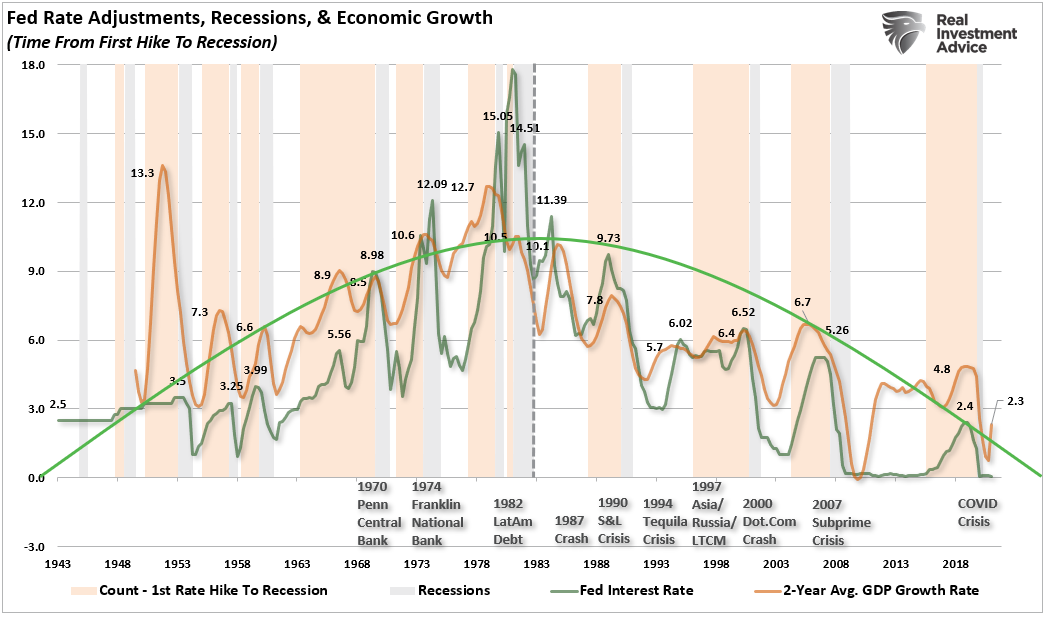

An honest review of history shows the Fed is consistently a “day late and a dollar short” regarding monetary policy. With the market trading at historical extremes, it is clear the Fed is about to make another policy mistake.

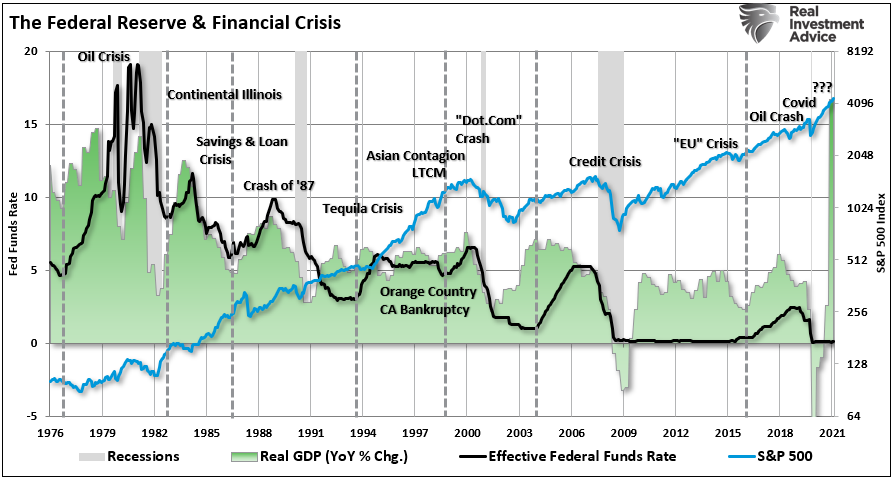

The history of “financial accidents” due to the Fed’s monetary intervention schemes is evident. Not just over the last decade, but since the Fed became “active” in 1980.

What should be evident is that before the Fed became active, economic growth was accelerating. There were few crisis events and economic prosperity was broad. However, post-1980, the trend of economic growth declined. There are many reasons leading up to each event, However, the common denominator is the Fed tightening monetary policy.

Notably, Fed rate hiking campaigns also correlate with poor financial market outcomes, as higher rates impacted the credit and leverage markets.

Once again, the Fed is discussing tightening monetary policy. The first step would be reducing their $120 billion monthly bond purchases, then potentially hiking rates. While they believe they can achieve this reduction without disrupting the equity markets or causing an economic contraction, history suggests otherwise.

Right Idea. Wrong Implementation.

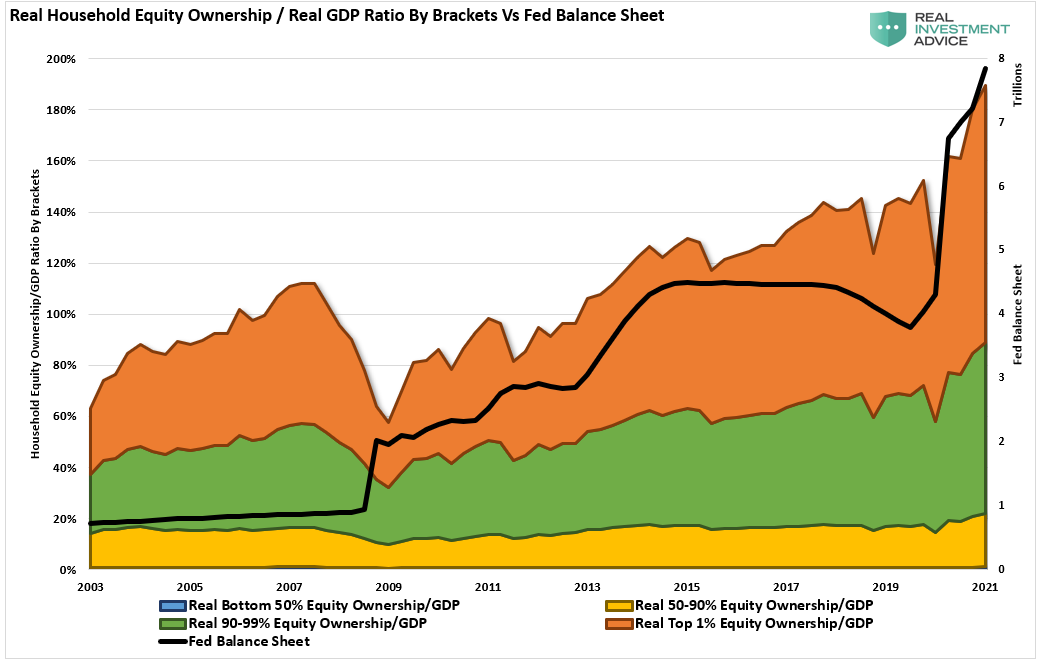

The Fed’s assumption is that by providing excess reserves to the banking system, the banks would lend those funds, thereby expanding economic activity. Furthermore, as discussed previously, the Federal Reserve’s entire premise of inflating asset prices was the subsequent boost to economic activity from an increased “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

However, after more than a decade of “monetary policy,” little evidence supports that claim. Instead, there is sufficient evidence “monetary policy” leads to other problems. Such include greater wealth inequality, speculative investment activity, and slower economic growth.

Current monetary policy has its roots in Keynesian economic theory. To wit:

“A general glut would occur when aggregate demand for goods was insufficient, leading to an economic downturn resulting in losses of potential output due to unnecessarily high unemployment, which results from the defensive (or reactive) decisions of the producers.”

In such a situation, Keynesian economics states that fiscal policies could increase aggregate demand, thus expanding economic activity and reducing unemployment.

The only problem is that it didn’t work as planned because “monetary policy” is NOT expansionary.

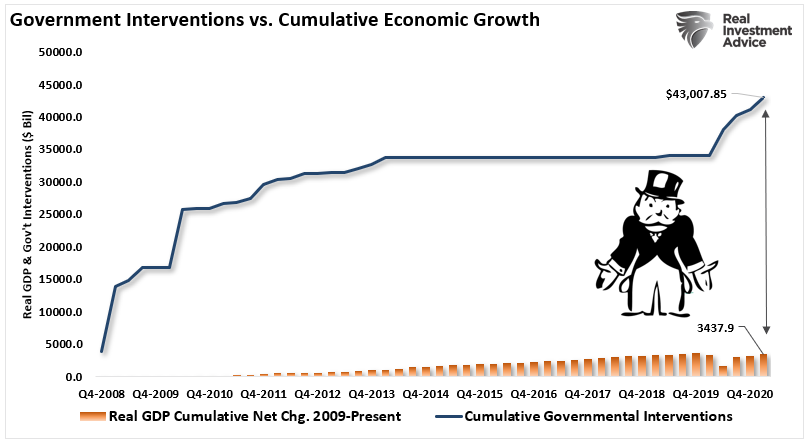

“Since 2008, the total cumulative growth of the economy is just $3.5 trillion. In other words, for each dollar of economic growth since 2008, it required $12 of monetary stimulus. Such sounds okay until you realize it came solely from debt issuance.“

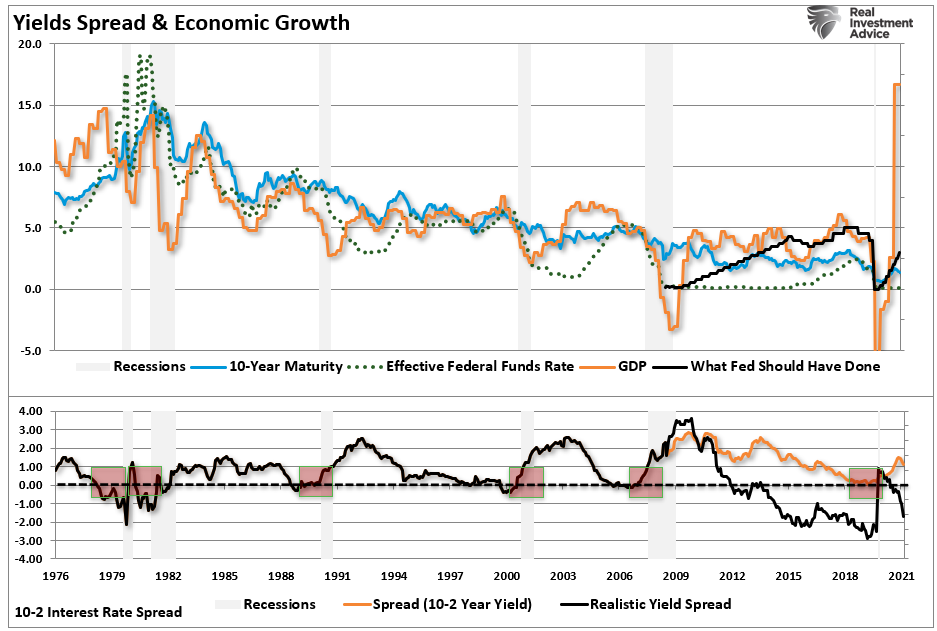

Fed Should Have Already Hiked Rates

The problem for the Fed is they are always a “day late and a dollar short.” Where the Fed repeats its mistake is keeping monetary policy accommodative for too long.

Instead, the Fed should use Government interventions to hike rates from zero while the excess liquidity supports economic growth.

For example, during the “Financial Crisis,” the Fed should have hiked rates as the spike in economic growth occurred in 2010-2011. At that point, both the Fed and Government had flooded the economy with liquidity. Yes, hiking rates would have slowed the advance in the financial markets. However, the excess liquidity would have offset the impact of tighter monetary policy.

If they had hiked rates sooner, interest rates on the short-end would have risen. Such would have given the Fed a policy tool to combat economic weakness in the future. But, of course, such assumes a historically normal response to economic recoveries. In that case, the yield curve would steepen sharply, providing higher yields to lenders.

Higher yields would slow speculative investment activity in the financial markets, housing, and other leveraged market investments. Such would reduce the financial risks to markets and potentially the need to continually “bailout” bad actors.

Such was a point made by Don Kohn, the Fed’s former vice chair for financial supervision.

“Dealing with risks to the financial stability is urgent. The current situation is replete with unusually large risks of the unexpected, which, if they come to pass, could result in the financial system amplifying shocks, putting the economy at risk.”

Policy Mistake In The Making

Don Kohn explicitly noted the Fed’s mention of “notable” vulnerabilities in the financial system. With asset values at historical highs, and record levels of financial debt, the concerns are valid.

The problem for the Fed is that interest rates are already at zero, the Government is running a massive deficit, not to mention $120 billion in QE monthly. Such puts the Fed in a poor position to respond to an economic downturn resulting from the bursting of an asset bubble or a debt crisis.

Our view aligns with GMO co-founder Jeremy Grantham. He argued:

“The Fed should act to deflate all asset prices carefully, knowing that an earlier decline, however painful, would be smaller and less dangerous than waiting.”

Yes, if the Fed had acted earlier to start hiking rates in which QE was in full swing, the market indeed would not have doubled in a year. However, the Fed would be in a much better position to minimize the damage from the next recessionary spat.

“Right now, systemic risk is not something the Fed is required to take into account as they carry out their missions. They should be required to broaden their perspective to consider the systemic implications of their actions and of the activities and firms they oversee and be held accountable for doing this.” – Kohn

Maybe, if such were the case, the Fed would not have to “bailout” the financial institutions every time the market declines.

In the end, the Fed will be a “day late and a dollar short” once again.