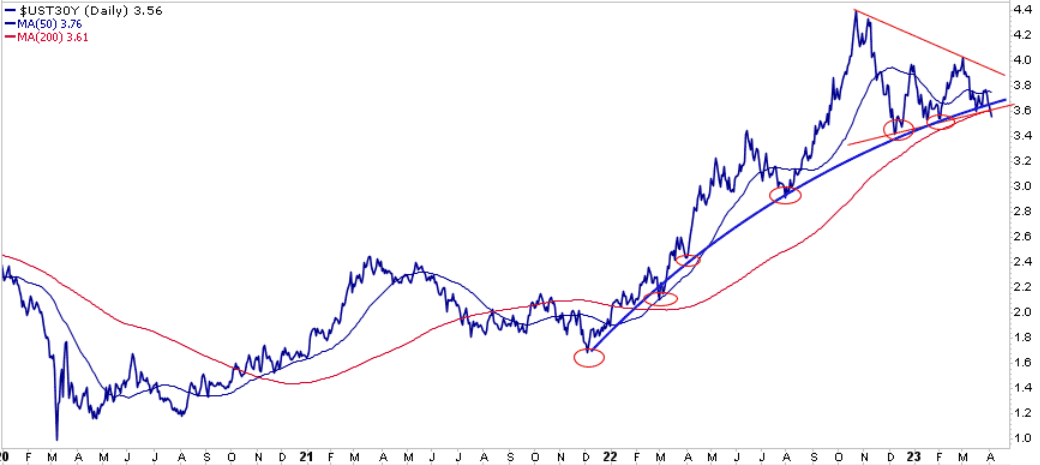

We added to our 30 year UST bond exposure on Wednesday via the ETF TLT. The recent rally in bond prices and the corresponding decline in 30 year yields shows promise it will continue. The graph below charts the steep increase in 30 year yields since late 2021. Throughout 2022, 30 year bond yields were making higher highs and higher lows. After peaking in October, 30 year yields broke the cycle of higher highs in March. More encouraging, the recent low yield is the first lower low in over a year. The prior series of higher lows are circled. Further, 30 years yields broke lower out of a wedge pattern (red lines). If the trend continues, the 50dma will cross below the 200dma forming a bearish death cross. In this case, bearish refers to lower yields which are bullish for bondholders.

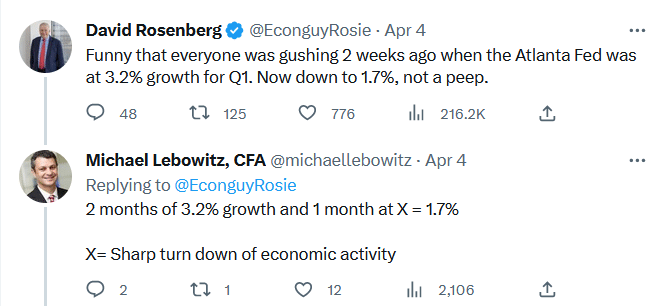

Economic data over the last few weeks has fallen off rather sharply. The ISM manufacturing and service sector surveys were weaker than expected. ADP, JOLTs, and Jobless Claims are finally showing signs the labor markets are weakening. More concerning, as we share in the Tweet of the Day below, the Atlanta Fed’s GDPNow has fallen quickly. GDPNow is not a forecast but a running GDP. Unlike predictions, GDPNow only uses released economic data. Therefore, with two months of data in hand, the recent decline points to a sharp drop-off in March’s economic activity. Might bond traders be sniffing this out?

What To Watch Today

Economy

Earnings

- No notable earnings releases

Market Trading Update

The markets took a bit of a breather this week, as we suggested would be the case.

“After last week’s bullish push higher, every major sector and market is now highly overbought short-term. Look for a bit of correction next week, which will provide an opportunity to increase exposure for the next couple of weeks. April tends to be one of the more robust performance months of the year, and while markets are short-term overbought, they remain on solid bullish buy signals for now.”

This past week, the market did correct a bit but did not resolve the short-term overbought conditions, which can remain overbought during a rally. The good news is that the upside breakout of the downtrend line from the April highs was tested and held. This is the first attempt at turning that previous resistance line into support. I would not be surprised to see more weakness next week, particularly given Friday’s employment report, which showed a slowing in the pace of hiring and suggests economic weakness is becoming more widespread.

As we have discussed over the last several weeks, the market continues to defy the recession calls despite weakening economic data. However, the actual test for the market will start next week as the first quarter earnings season gets underway. Estimates were lowered substantially going into Q1, so expect a high “beat rate” for companies. While the beating estimates will get headlines, it will be the “forward guidance” driving their prices. CEO confidence remains very low. Therefore, weak guidance could knock some of the exuberance out of the markets.

Notably, the first companies to announce earnings will be the major banks. All eyes will be focused on their reports to determine if the banking crisis is behind us.

The Week Ahead

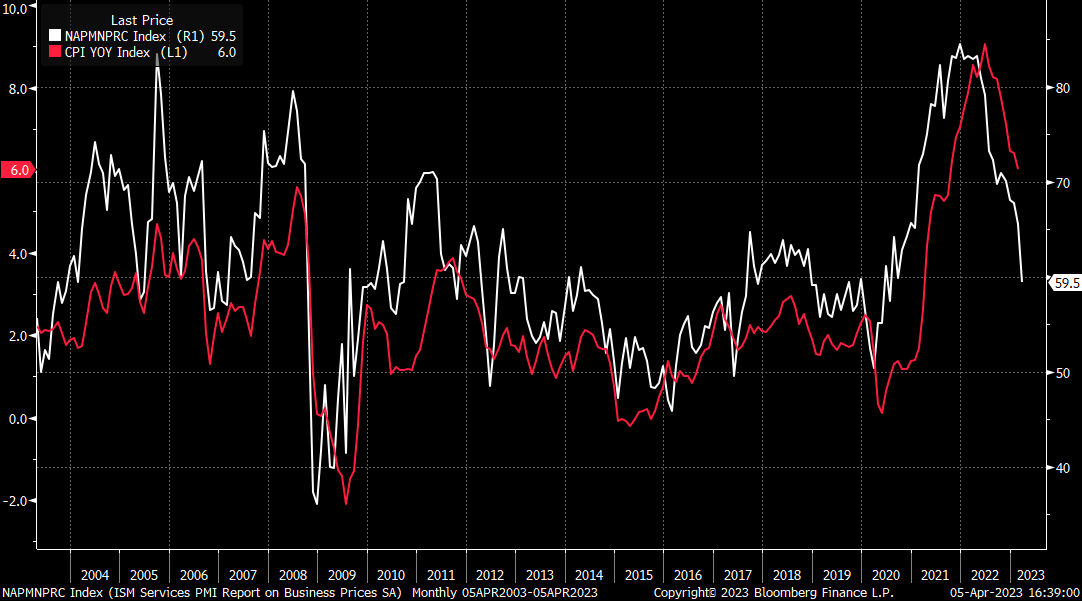

CPI on Wednesday, PPI Thursday, and Retail Sales Friday will provide investors with pertinent information. CPI is expected to be a tenth lower than last month but remaining sticky. The graph below shows that ISM Services prices and CPI are well correlated. Consequently, based on last week’s ISM data, CPI could fall more than expected. PPI, driven by higher used car and energy prices, is expected to uptick slightly. The Fed wants inflation to fall quicker than forecasts. Retail sales for March will help assess if, in fact, consumption is slowing. Recent credit card data has shown a decline in personal consumption. Economists expect monthly retail sales to decline by 0.9% following a 0.4% decline last month.

The FOMC minutes for the March meeting will come out on Wednesday afternoon. The Fed has been relatively quiet the last few weeks. They have also been sticking to the “higher for longer” expectation. We doubt the minutes will provide new news for investors. Expect the Fed to walk the tightrope between inflation and financial stability.

This week, the first quarter earnings season kicks off with the banks and airlines. The large banks, including JP Morgan, Citi, and Wells Fargo, release their earnings on Friday. Smaller regional banks will release throughout the week and the following week. Much attention will be paid to large and small banks to gain insight into how the recent crisis affects profitability. From a macro perspective, it will be interesting to see how much large banks increase their loan loss reserves. Large increases are a sign they worry about the economy.

ETF Investment Flows

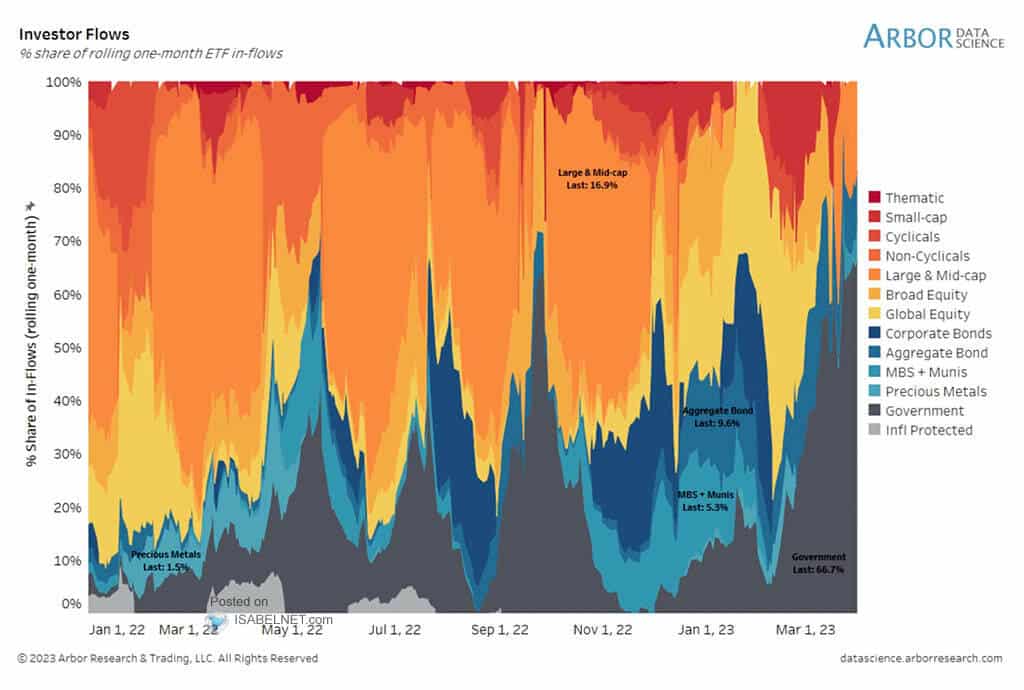

The graph below from Arbor Data Science shows that ETF investors have gradually preferred bonds over stocks in the last year. Bonds in the blues and grays account for about 80% of recent investor flows. At the start of 2022, they accounted for less than 20% of flows. As shown, allocations between stocks and bonds can be volatile.

The Prospect Theory – Behavioral Traits Part IV

The prospect theory, also known as loss aversion, suggests that investors do not view risk and return equally. For example, researchers have shown that most people will not play a game of Heads or Tails where they can win $100 but risk losing $50. From a risk/return perspective, you should take the bet all day. The following example is courtesy of Investopedia:

Consider an investor who is given two pitches for the same mutual fund. The first advisor presents the fund to Sam, highlighting that it has an average return of 10% for the last three years. Meanwhile, a second advisor tells the investor that the fund has had above-average returns over the last decade, but has been in decline for the last three years.

Prospect theory says that although the investor has been pitched the exact same mutual fund, they are likely to buy from the first advisor. That is, the investor is more likely to buy the fund from the advisor that expresses the fund’s rate of return in terms of only gains, while the second advisor presented the fund as having high returns, but also losses.

As we have seen, it is important to keep a level head in volatile markets. Often in down markets, the Prospect Theory causes investors to panic and sell. Trends, up and down, contain lots of counter-trend movements. Understanding the broader trend and the factors that determine the trend will help you avoid letting emotions do your trading.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.