The S&P 500 capped off last week on a positive note with a strong rally to close above both its 50- and 200-day moving averages. The last time the index closed above both key moving averages was back in January. With the S&P 500 starting to push into overbought territory, we will look to take profits and reduce our risk this week. In addition, on a pullback, we will be watching to see if the index can establish support at the top of its downtrend line.

[dmc]

What To Watch Today

Economy

- 8:30 a.m. ET: Chicago Fed National Activity Index, February (0.50 expected, 0.69 in January)

Earnings

- Nike (NKE) to report adjusted earnings of 72 cents on revenue of $10.61 billion

Weekly Market Recap With Adam Taggart

Market Trading Update

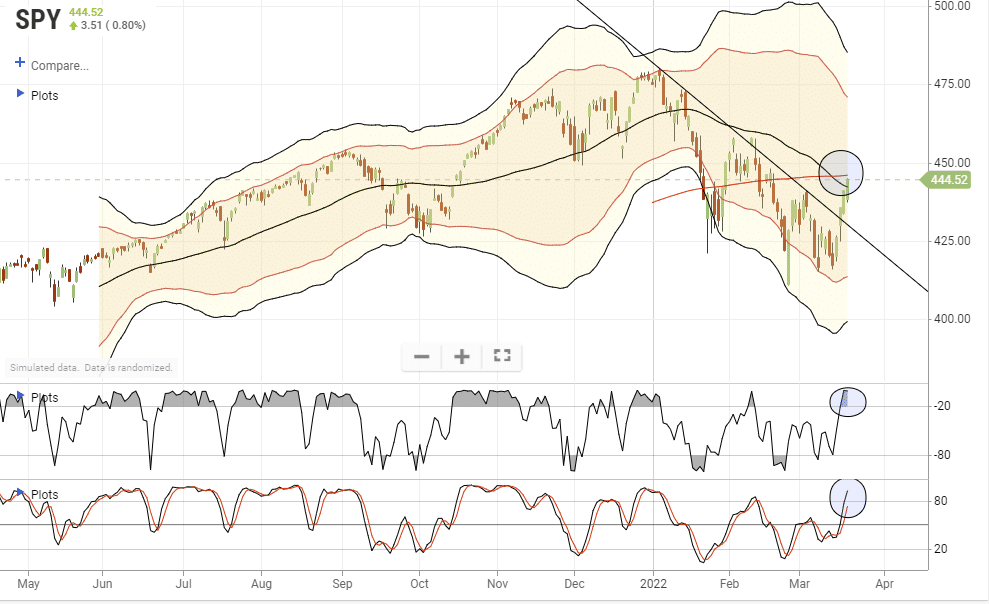

We previously stated that any rally above the downtrend would test the 50- and 200-dma averages. That test occurred on Friday, with the index clearing the 50- and sitting just below the 200-dma. With markets back to short-term overbought, it may be challenging for markets to clear resistance next week.

On a positive note, investor sentiment and positioning remain negative. While the rally did reverse some negativity, it still provides “fuel” for a rally through the end of the month.

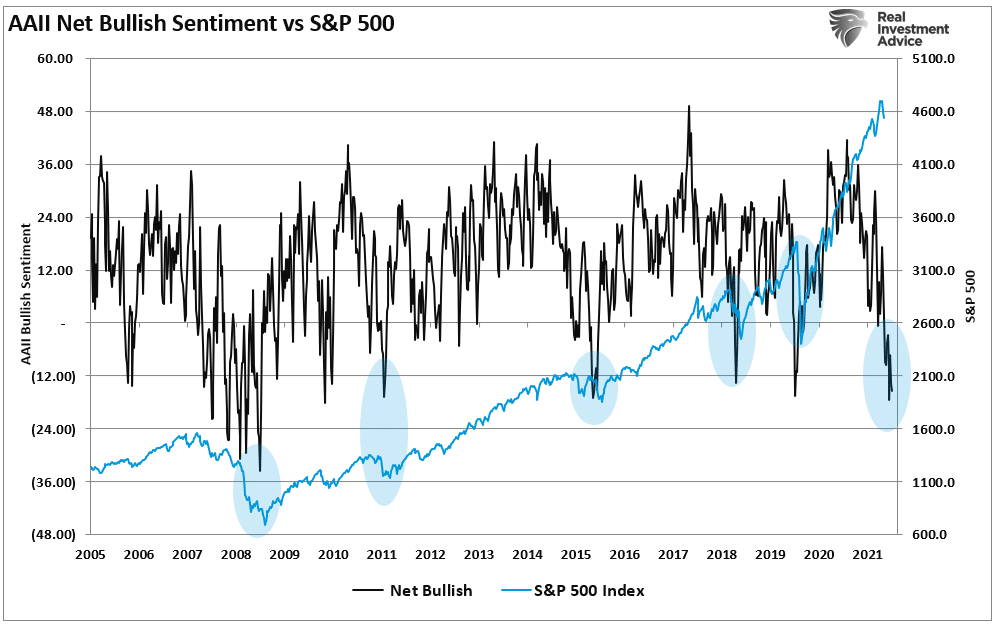

Several things currently suggest a follow-through rally is possible, encouraging the “bulls” to declare the “bottom is in.”

- Extremely negative investor sentiment.

- High cash levels

- Low equity positioning by fund managers.

- Equity fund flows are strong.

- Stock buybacks remain strong

But other issues suggest this rally may be limited to the upside, keeping this a more tradeable rally.

- Liquidity that drove the rally from the 2020 lows is reversing.

- The Fed is hiking interest rates

- Inflation is hot

- Earnings will slow along with economic growth.

- There are a lot of “trapped longs” that need an exit.

TPA Research – Top 10 Stocks To Buy And Sell

Click on RIAPro+ today to add TPA Research to your subscription for just $20/month.

Mortgage Rates Cut into February Existing Home Sales

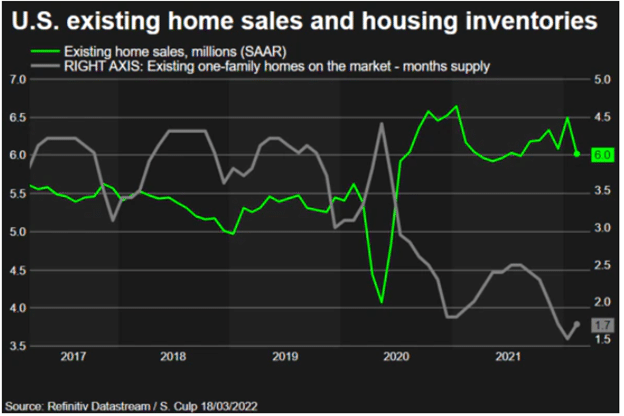

Existing home sales in the U.S. fell 7.2% MoM in February, completely wiping out the spike in January. It was the largest sequential decrease since February 2021, and sales fell 2.4% YoY. As we noted on Friday, rising mortgage rates are beginning to harm affordability in the housing market. In concert with the short supply, higher rates will continue dragging on sales in the coming months. The chart below, courtesy of Reuters, shows the market had 1.7 months of supply in February- just off record lows from January. On a positive note, the higher mortgage rates’ impact on affordability should help moderate the rate of home price appreciation.

The Week Ahead

This week will start light on economic data then pick up as the week goes on. Today kicks off with the Chicago Fed National Activity Index report for February. Expectations are for an increase to 0.75. On Wednesday, we will get new home sales data for February with expectations for a rise to 0.813M (SAAR). Thursday will hold updates on Durable Goods Orders for February, jobless claims data, and the Markit PMI for March. Friday, we cap off the week with a final reading of the University of Michigan Consumer Sentiment Index for March and February Pending Home Sales data.

Fed speakers will be out in droves this week following last Wednesday’s FOMC meeting. We will hear from Bostic and Chair Powell today, followed by Williams, Daly, and Mester tomorrow. Powell and Daly will speak again on Wednesday. Then on Thursday, Waller, Evans, and Bostic are scheduled to speak. Friday will hold speeches from Williams, Barkin, and Waller.

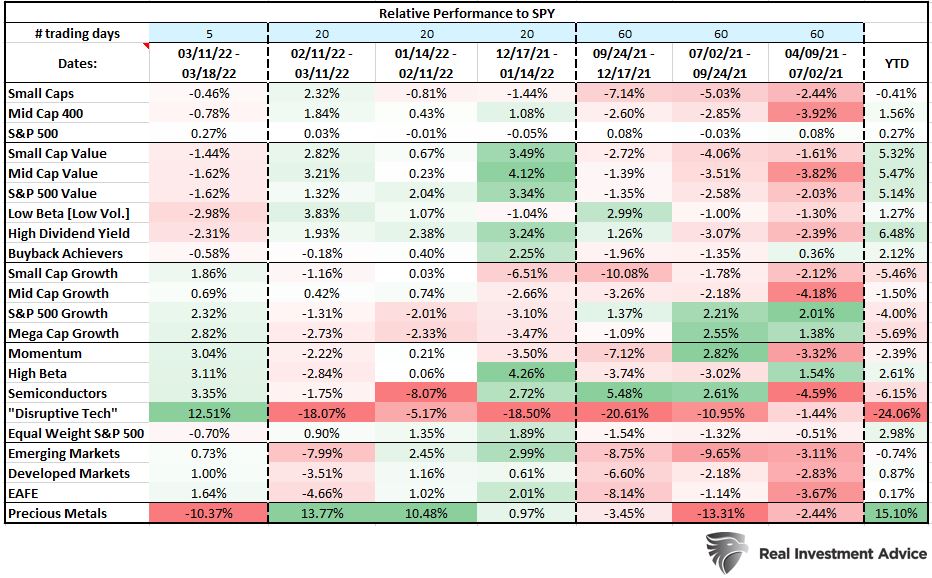

The Growth Trade Gets a Bid

The S&P 500 has fallen 6.1% YTD as investors grapple with the Fed, inflation, and geopolitical factors. Conventional wisdom says defensive positioning is the place to be in a down market, which has held up so far this year.

The chart below illustrates how factor performance trends have evolved over the last 245 trading days. The value/dividend trade is substantially outperforming the growth/momentum trade YTD. However, last week’s post-FOMC rally put a spark back in the tech- and discretionary-heavy growth/momentum trade. Although, with the S&P 500 getting into overbought territory, that move may be coming to an end. On a positive note, a pullback would give the index a chance to establish support at its downtrend line and confirm a breakout.

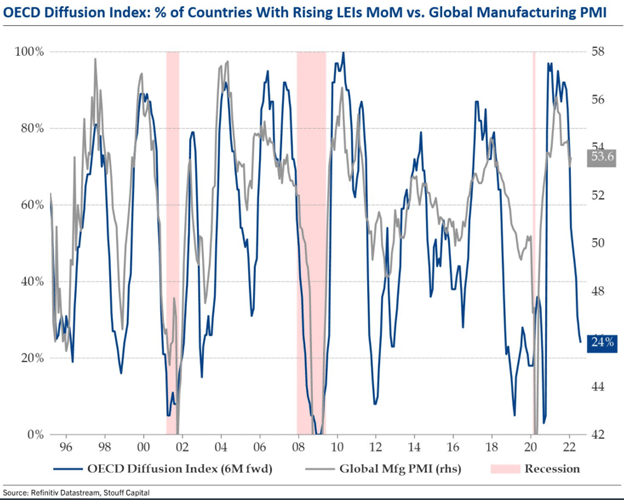

Global Manufacturing Activity Could See More Downside

The chart below from Julien Bittel makes a good case for further downside in the Global Manufacturing PMI. The OECD diffusion index tends to lead Global Manufacturing PMI by about six months, give or take, and displays a solid relationship over time. Interestingly, it appears that the relationship was stronger pre-GFC than it has been in the days since the GFC.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.