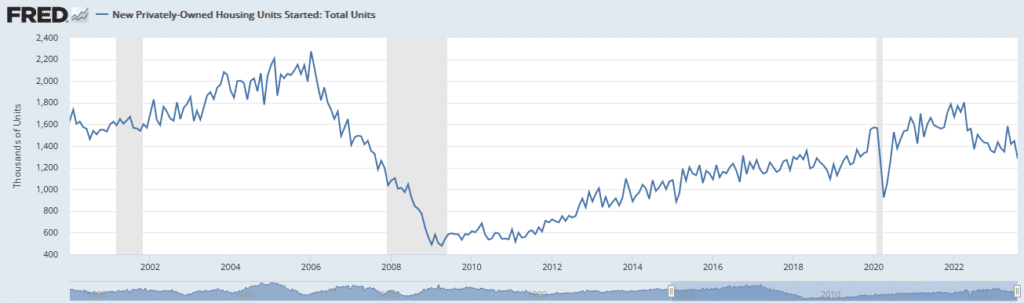

Higher mortgage rates are resulting in a shortage of inventory of used homes and a surge in new homebuilding. Recent data shows a third of all homes for sale are new homes. That is almost three times the average ratio. While homebuilders have been taking advantage of the low inventory situation by offering home buyers reduced mortgage rates and other discounts, it appears they are starting to have concerns. The most recent NAHB builder confidence survey fell to 45. A reading below 50 means there are more homebuilders with negative sentiment than positive sentiment. Further, housing starts fell to their lowest level since June 2020, when the pandemic wreaked havoc on the economy. August annualized housing starts were 1.283 million on a seasonally adjusted basis. That is -11.3% below the downwardly revised 1.45 million from the previous month and expectations for 1.43 million.

The recent decline in homebuilder confidence and reduction in housing starts bodes poorly for the industry. From a macroeconomic perspective, housing is an excellent leading indicator of economic activity. As we outlined in Janet Yellen Should Focus On HOPE, “HOPE is an acronym describing the lags and the sequence in which economic activity typically weakens before a recession.” The “H” or leading indicator is housing. If existing home sales, housing starts, and homebuilder confidence continue to weaken while mortgage rates preclude buyers and sellers from transacting, the housing sector may suffer. Until mortgage rates decline, the problems are likely to continue.

What To Watch Today

Economics

Earnings

Market Trading Update

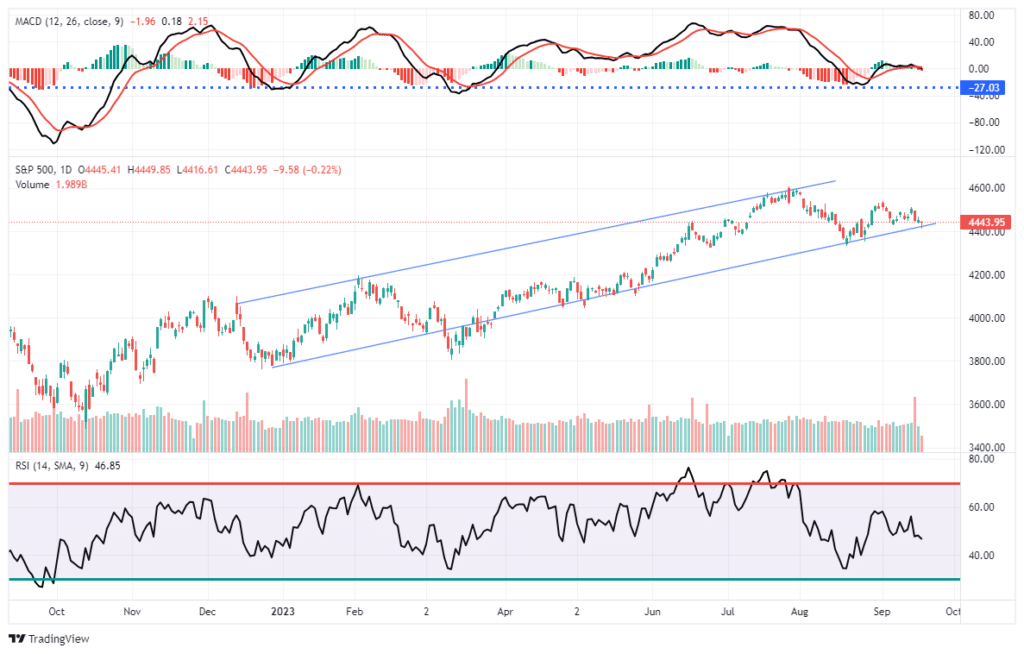

Yesterday’s market action was diametrically opposed to Monday’s as the market sold off early in the day only to stage a comeback rally by the end. Traders remain unwilling to take on any big bets ahead of the Federal Reserve’s interest rate decision this afternoon. The sloppy action continues for now, and while the market did trigger a short-term sell-signal, that signal is occurring from lower levels, suggesting downside risk is likely limited. Such continues to look like a market treading water until the Q3 earnings season begins in October. For now, continue to monitor risk and use current market weakness as an opportunity to rebalance portfolios as needed.

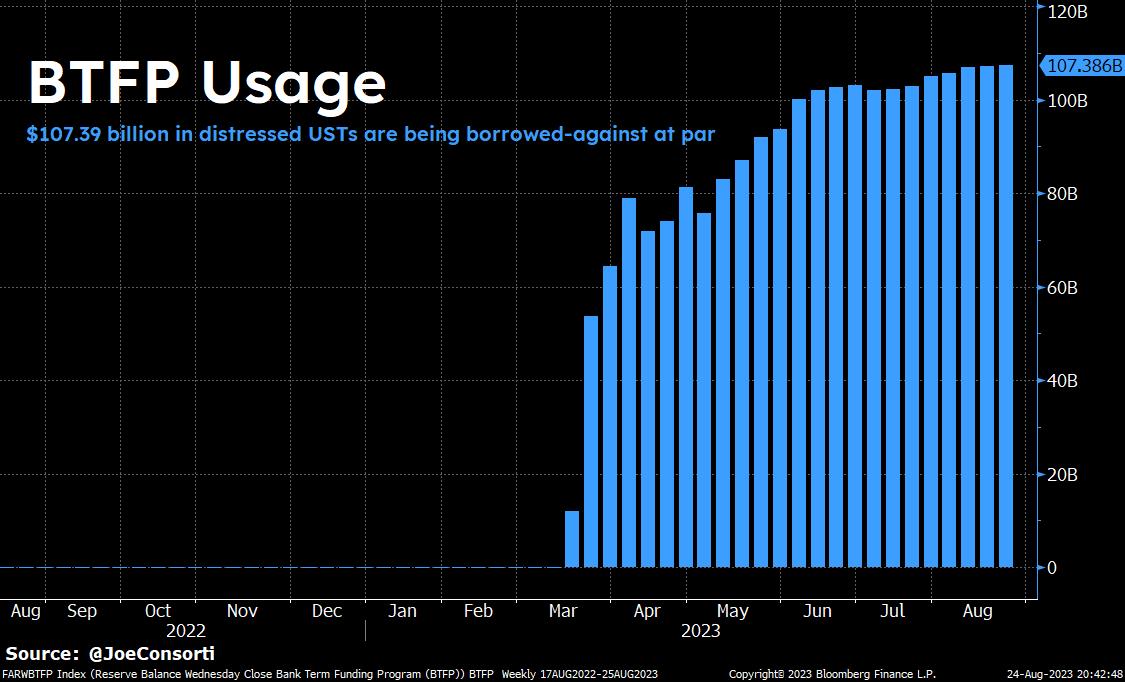

Bank Bailout- Six Months In and Six Months To Go

In March, the Fed was dealing with a banking crisis of its own making. The surge in interest rates caught many banks off guard. With deposits fleeing the banks for higher yields, banks were forced to sell assets. Most banking assets, be they loans or securities, were trading at discounts to their purchase prices. As a result, banks like Silvergate and Silicon Valley had to take bankruptcy-inducing losses to offset lost deposits.

Seeing the potential trouble of underwater bank assets, the Fed created the Bank Term Funding Program (BTFP). The facility allows banks to pledge Treasury bonds trading at discounts to par as collateral for loans based on the par value of the collateral. Three months into the program, the balances continue to grow, albeit slowly. The program ends in March. As such, we suspect the Fed will start to discuss their options. They can extend the program and roll over existing loans or terminate it. The program is a form of QE, so the Fed may perceive rolling over existing loans as inflation-inducing. However, terminating the program could lead to more bankruptcies.

Housing Update

Redfin puts out great commentary and statistics on the housing markets to help us navigate how high mortgage rates affect the sale and rental markets. As we have noted, 40% of CPI is tied to rents and rental prices imputed from home prices. As such, we thought it would be helpful to share a handful of charts and commentary from Redfin’s website.

Home prices are slightly higher year over year despite a substantial 14.5% drop in the number of homes sold. Home sales are seasonal. Therefore, comparing the recent peak in June to the prior June peaks is essential.

In regards to the supply of houses, Redfin says the following:

In August 2023, there were 1,514,235 homes for sale in the United States, down 18.6% year over year. The number of newly listed homes was 536,703 and down 13.3% year over year.The median days on the market was 30 days, up 4 year over year. The average months of supply is 2 months, down year over year.

Essentially, the housing market is at a standstill. Existing homeowners are finding it tough to sell houses despite high prices because they do not want to give up their very low mortgage rates. On the flip side, home buyers are finding homeownership expensive due to high prices, limited supply, and high mortgage rates.

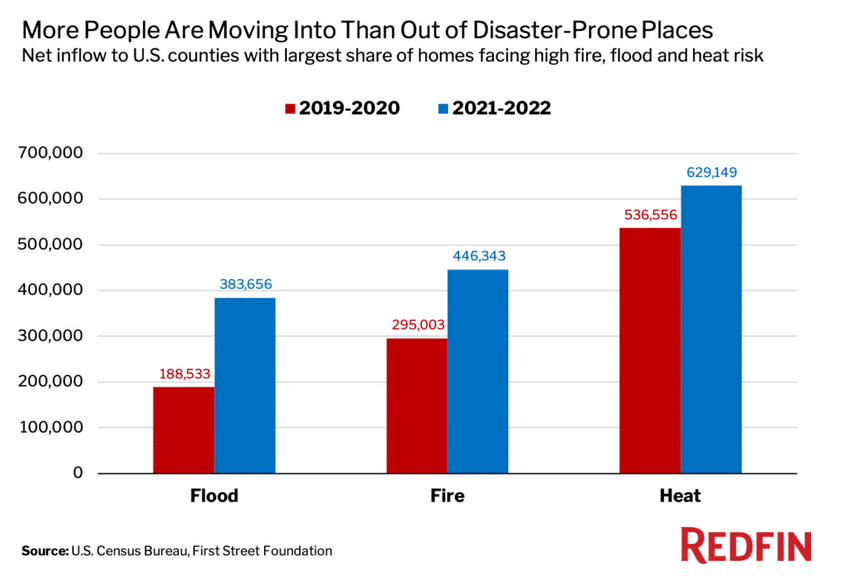

In regards to the recent migration trends, we continue to see movement from the northeast, California, and upper midwest to the south. The data is from the last three months but replicates recent longer-term trends.

Politics, taxes, cost of living, and weather are leading factors in the migrations. However, some that have moved may be trading those issues for new ones, as we share below.

The final graph shows rental prices. The good news is that rents are flat year over year. As such, the contribution to annual CPI inflation is zero. However, recently, rents have been increasing and remain significantly elevated from pre-pandemic levels. The CPI data on rents lags significantly from the graph. Therefore, the next four to six CPI reports will show rental prices declining despite the evidence below that they are rising again.

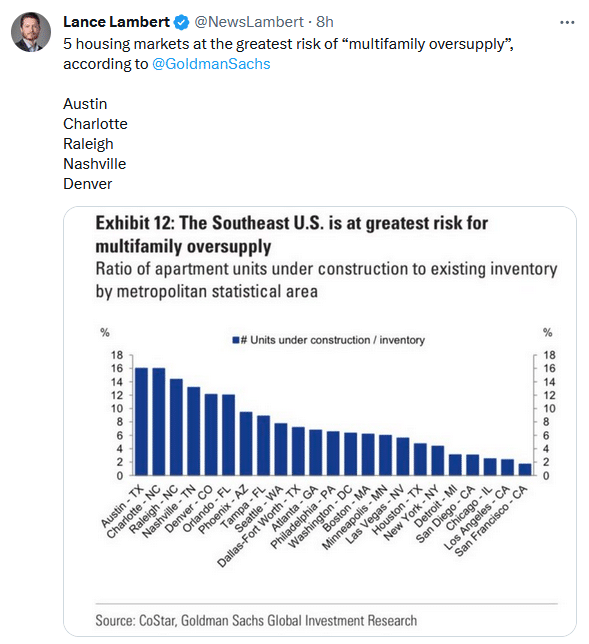

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.