The on and off again Russian invasion of Ukraine is heating back up, and with it, Gold prices eclipsed $1900 per ounce, and bond yields fell sharply. To wit is the following headline: WE’RE IN A TIMEFRAME WHERE A RUSSIAN ATTACK MIGHT HAPPEN AT ANY TIME– Source: White House. Gold and bonds are safe-haven assets and typically trade well when potentially destabilizing geopolitical events occur. Caution is warranted, however, as trading gold and bonds is difficult as their prices are closely tied to news/rumors which create significant volatility.

[dmc]

What To Watch Today

Economy

- 10:00 a.m. ET: Existing Home Sales, January (6.10 million expected, 6.18 million in December)

- 10:00 a.m. ET: Existing Home Sales, month-over-month, January (-1.3% expected, -4.6% in December)

- 10:00 a.m. ET: Leading Index, January (0.2% expected, 0.8% in December)

Earnings

- 6:45 a.m. ET: Deere (DE) to report adjusted earnings of $2.26 on revenue of $8.2 billion

- 7:00 a.m. ET: DraftKings (DKNG) to report adjusted losses of 74 cents on revenue of $444.4 million

- 7:00 a.m. ET: Bloomin’ Brands (BLMN) to report adjusted earnings of 53 cents on revenue of $1.04 billion

Market Update

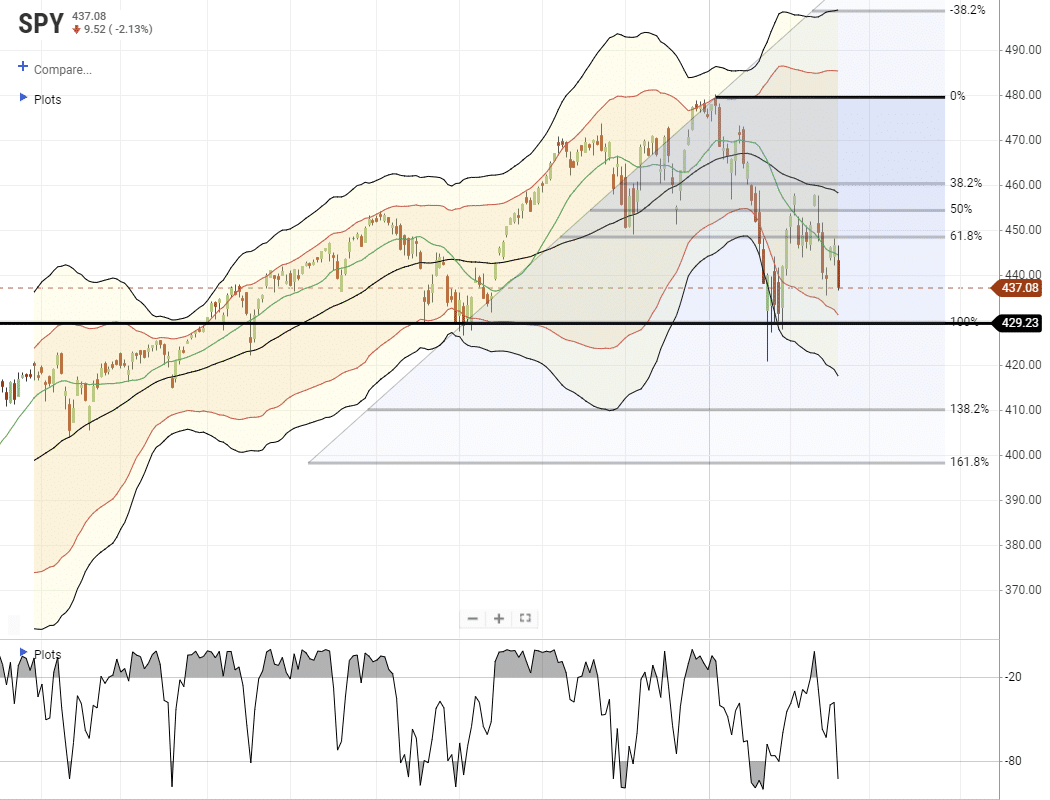

Stocks came under pressure yesterday, as “fear” of geopolitical events pushed stocks lower and gold and bonds higher. It was a classic “risk-off” trade. Nonetheless, while the selloff was harsh, it remains nothing more, at this juncture, than a retest of the January lows. IF this market is going to maintain its bullish bias, it must hold those January lows otherwise we are looking at a potentially deeper correction. The good news, if you want to call it that, is the market has now reversed its previous overbought condition.

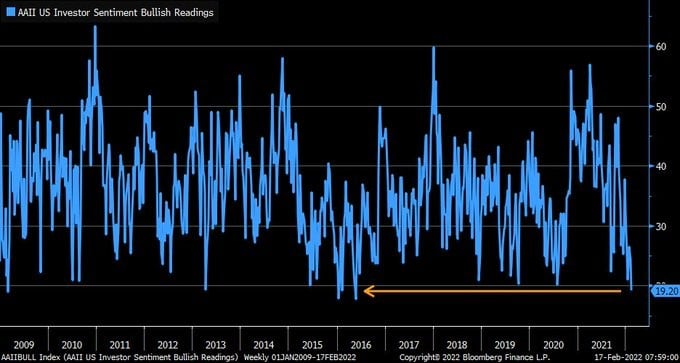

Sentiment Is Really Bearish – Which Could Be Bullish

Bulls are at the lowest level since early 2016 when we all thought the world would end over Brexit.

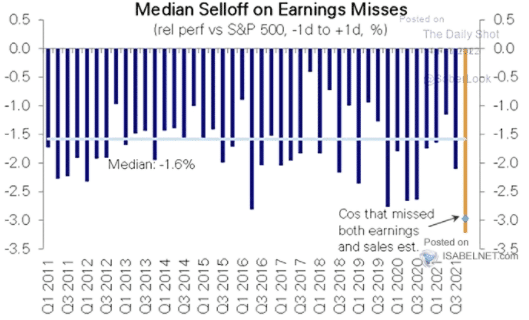

It Has Been Tough On Stocks That Disappointed

It’s been a tough quarter on stocks that either missed earnings or just guided down forward estimates. The penalties on stocks like Netflix, Viacom, Facebook, and many others have been 20% or more in some cases. As shown, the quarter has been the most punishing of any quarter going back to 2011. This speaks much to the underlying lack of liquidity in markets as buyers exist but at much lower levels than sellers would like.

Zoltan Speaks

Zoltan Pozsar, a highly regarded Fed watcher from Credit Suisse, wrote an interesting research piece on Wednesday. The core of his argument is the Fed may try to lower asset prices. They might do this to temper inflation and satisfy “political imperatives.” We link the full report HERE.

Maybe the path to slower services inflation – OER and all other services – is through lower asset prices. We recognize that what we are saying is extreme, but we think the Fed will soon incorporate some version of this thought process. It wasn’t tried before, but what was tried before, the Fed cannot do anymore due to the political imperatives of inclusive low unemployment and redistribution. Hence the need for a Volcker moment.

Volatility is the best policeman of risk appetite and risk assets. To improve labor supply, the Fed might try to put volatility in its service to engineer a correction in house prices and risk assets – equities, credit, and Bitcoin too…

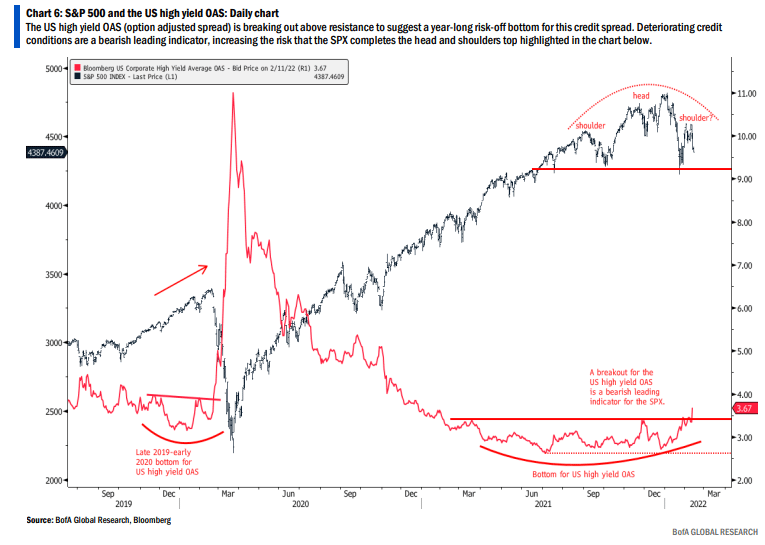

A Bearish Turn of Events

The chart below from BofA Research shows the strong negative correlation between the S&P 500 and Junk-rated credit yield spreads. Junk bond spreads are forming a bearish rounded bottom pattern while stocks appear to be creating a head and shoulders topping pattern. Junk spreads remain historically low. However, the uptick bears watching as the Fed considers credit spreads a key barometer of financial stability.

The Northeast Economy Is Slowing

Following the New York Fed’s Empire State Manufacturing Survey earlier this week, the Philly Fed Manufacturing survey also disappointed. It came in below expectations for February at 16, down from 23.2 in January. Both reports indicate manufacturing activity is expanding, but they point to a slowdown in manufacturing in New York and Philadelphia. Those are the two largest cities in the Northeast U.S.

The graph below, courtesy of BofA, shows that delivery times are down sharply and at the lowest levels since 2008. This measure serves as a good indication that shortages and supply line problems are easing quickly. It may also prove promising in the fight against inflation.

Which Industries Face A High Risk of Wage Inflation?

The Roosevelt Institute put out an excellent research piece on the labor market. It discusses how the combination of the quits and discharge rates provides a good gauge of employee leverage. Per the article: “The current higher LLR is reflective of both a record-high quit rate and a record-low discharge rate. And with quits rising faster than discharges, the increasingly credible possibility that workers will quit is further increasing their bargaining power and lifting the LLR.”

The graph below helps us focus on which industries are most at risk for rising wages. Note that almost all classifications below are at near their highest levels in 20 years.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.