Inside This Week’s Bull Bear Report

- Full-Time Employment As A Recession Indicator

- How We Are Trading It

- Research Report –Household Allocations Suggest Caution

- Youtube – Before The Bell

- Market Statistics

- Stock Screens

- Portfolio Trades This Week

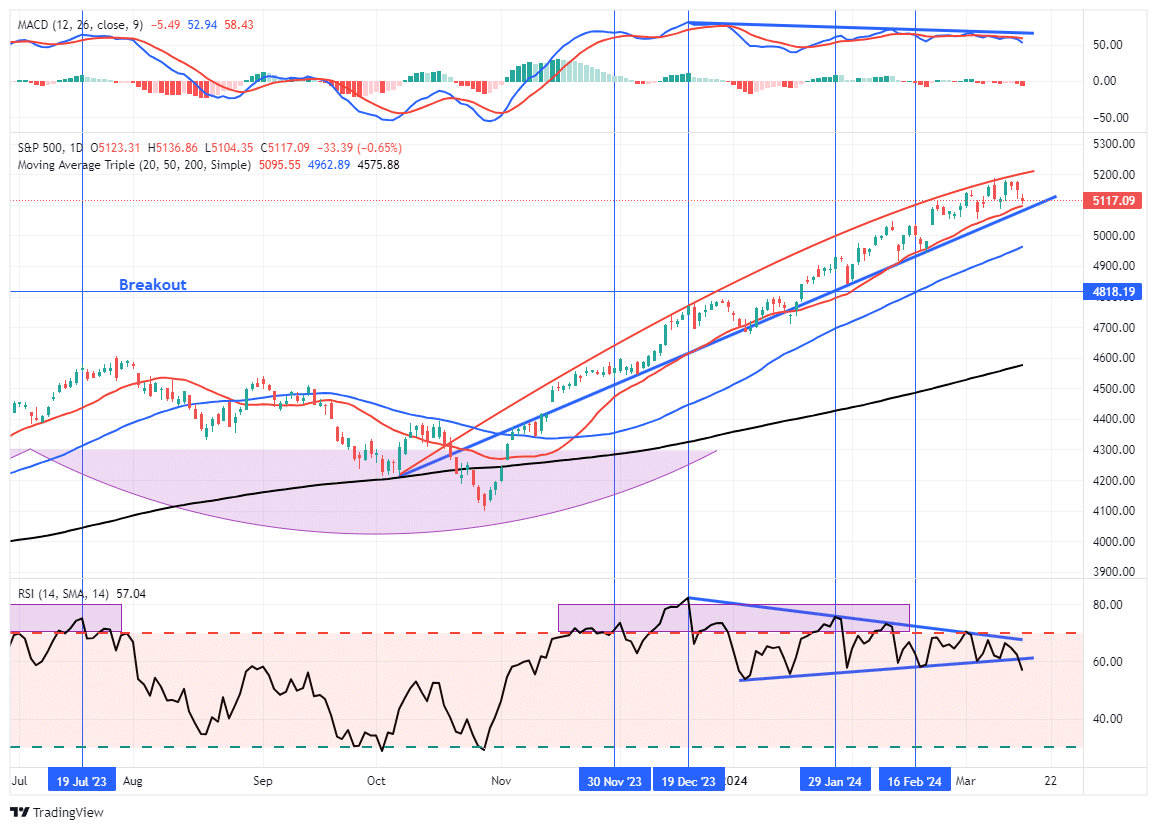

Bull Trend Of Market Shows Some Cracks

Last week, we discussed whether this is a short-term market top or a bubble. In that discussion, we noted that the ongoing bullish trend remains intact, with the market trading from the top of the trendline to the 20-DMA. After a rally to all-time highs, the market again traded lower on Thursday and Friday to finish at the 20-DMA.

However, some differences this week suggest we may see a further correction next week. The market was trading in a very defined bullish trend channel. Over the last two weeks, the advance has begun to taper off, and a more rounded top may be forming. While the 20-DMA continues to act as support, a violation of that level could well trigger additional selling. Momentum and relative strength have also shown continued weakness, and both registered “sell signals” on Friday.

As we stated last week:

“While we have become increasingly cautious over the last few weeks, as the market continues to rise, we have suggested taking profits and rebalancing portfolio risks. If you have not done so, such remains a recommended course of action. However, this does not mean to reduce equity allocations aggressively.”

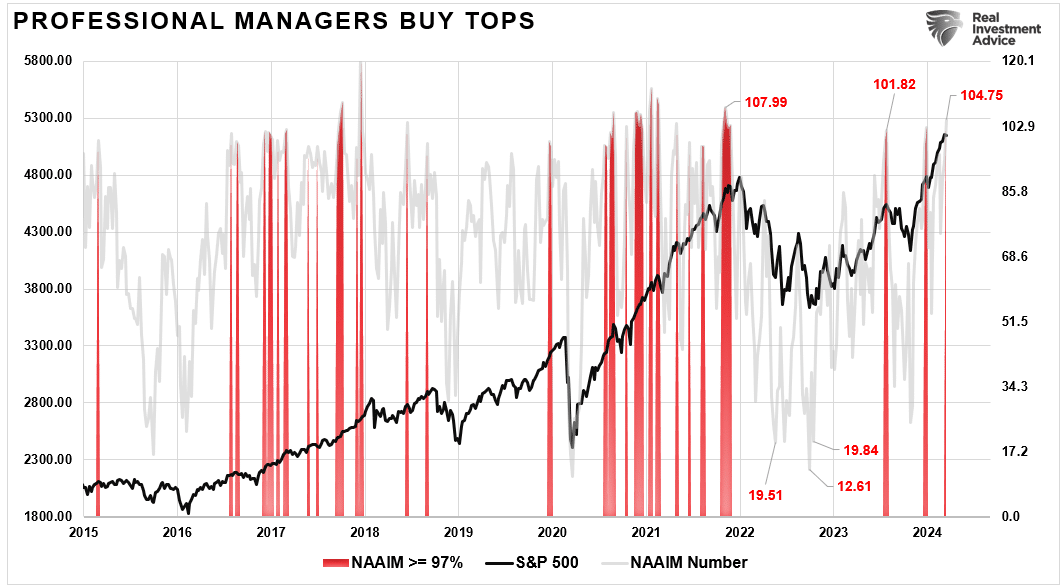

That recommendation remains again this week. While we have done some “trimming” to portfolios over recent weeks, we have not aggressively reduced risk. However, if the market does show evidence of a corrective phase, we will become more attentive to risk management. While we are never sure about the timing of market corrections, that is a part of the normal market cycle. With bullish exuberance getting a bit extreme, something will likely catalyze a reversal of sentiment. As shown, professional managers are notorious for buying the tops of markets. The red highlights are when professional manager’s allocations exceed 97%.

There is mounting evidence that the economy is slowing faster than many economists think. One of those data points is full-time employment, which is the subject of our analysis this week.

Need Help With Your Investing Strategy?

Are you looking for complete financial, insurance, and estate planning? Need a risk-managed portfolio management strategy to grow and protect your savings? Whatever your needs are, we are here to help.

A Brief Review

The current consensus is that the U.S. economy will avoid a recession following the aggressive rate-hiking campaign in history. While it certainly seems that such will be the case given the relatively strong economic growth rates over the last few quarters, important indicators still suggest recession risks remain.

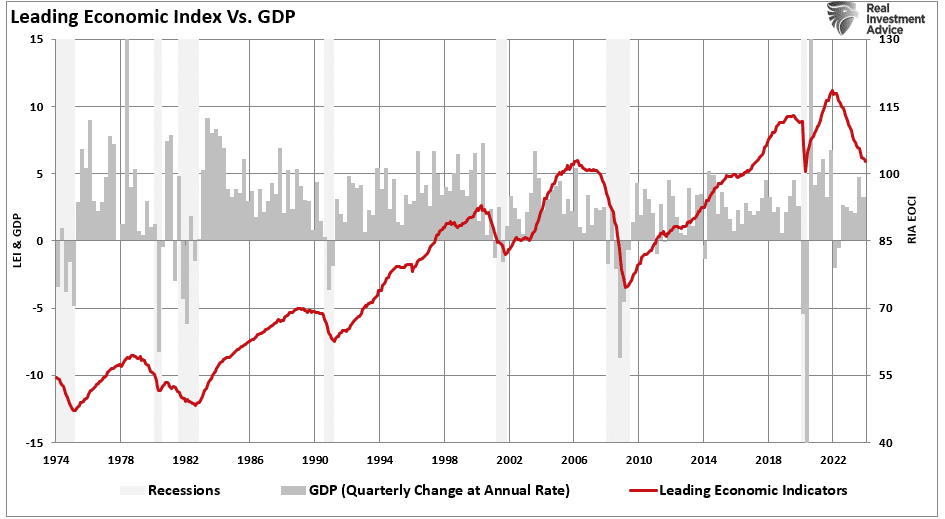

As discussed in “Conference Board Scraps Its Recession Call,” the Leading Economic Index (LEI) has a long history of accurately predicting recession outcomes. As we showed, each previous decline in the raw LEI from the Conference Board versus GDP has aligned with a recession.

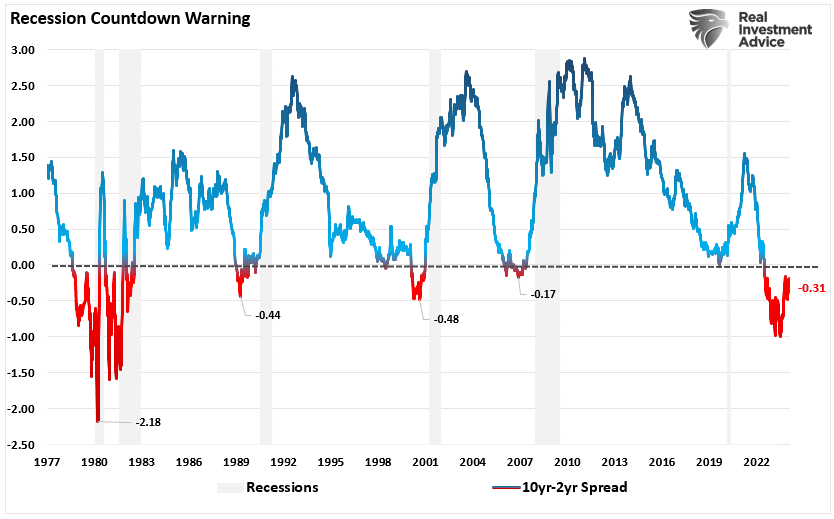

We also discussed the inverted yield curve, which suggests that recession risks remain. To wit:

“While the Conference Board has abandoned its recession call, the bond market has not. The yield spread between the 10-year and 2-year Treasury Bonds remains deeply inverted. Notably, the inversion is NOT the recessionary warning. It is when that yield-curve UN-inverts that signals the onset of a recession. Such has historically occurred in response to Federal Reserve rate cuts to try and offset a rapidly slowing economy.”

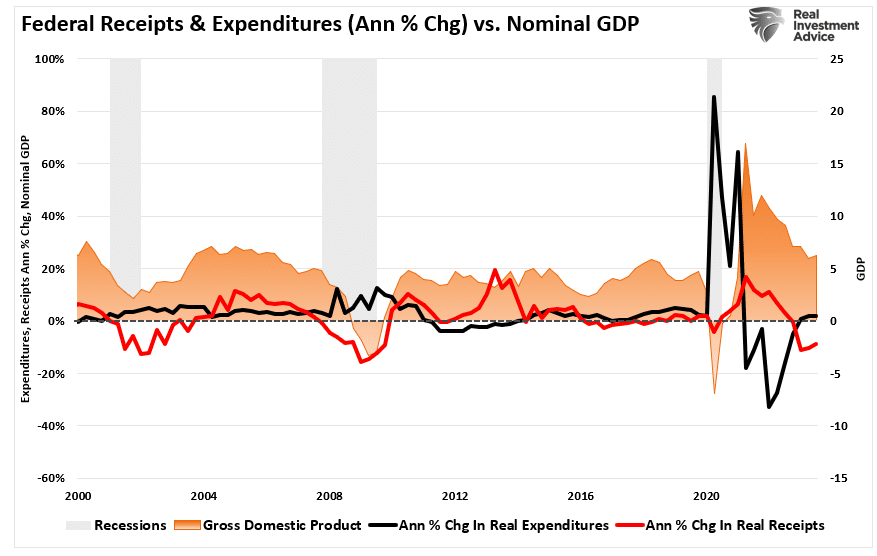

However, the conundrum remains as economic growth rates defy the numerous leading recessionary indicators. Of course, we understand that economic strength remains a function of the financial stimulus from the Inflation Reduction Act and the CHIPS Act, as well as a surge in deficit spending.

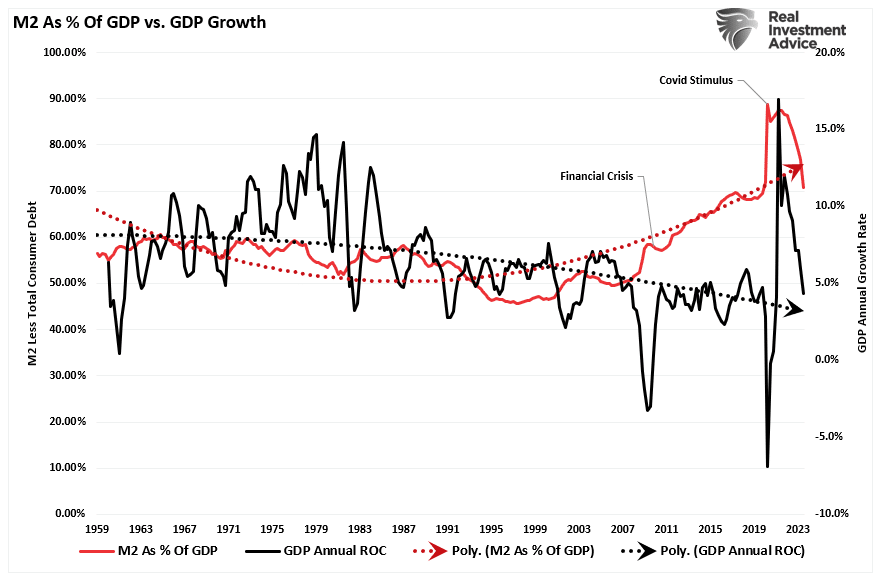

We see that same support to economic activity in the monetary supply (M2) as a percentage of the economy. While those monetary and fiscal supports caused economic growth to surge following the “pandemic-related” spending spree, both are reversing.

However, as the monetary stimulus reverses, the risk of a recession remains. One of the most important indicators is full-time employment.

Full-Time Employment As A Recession Indicator

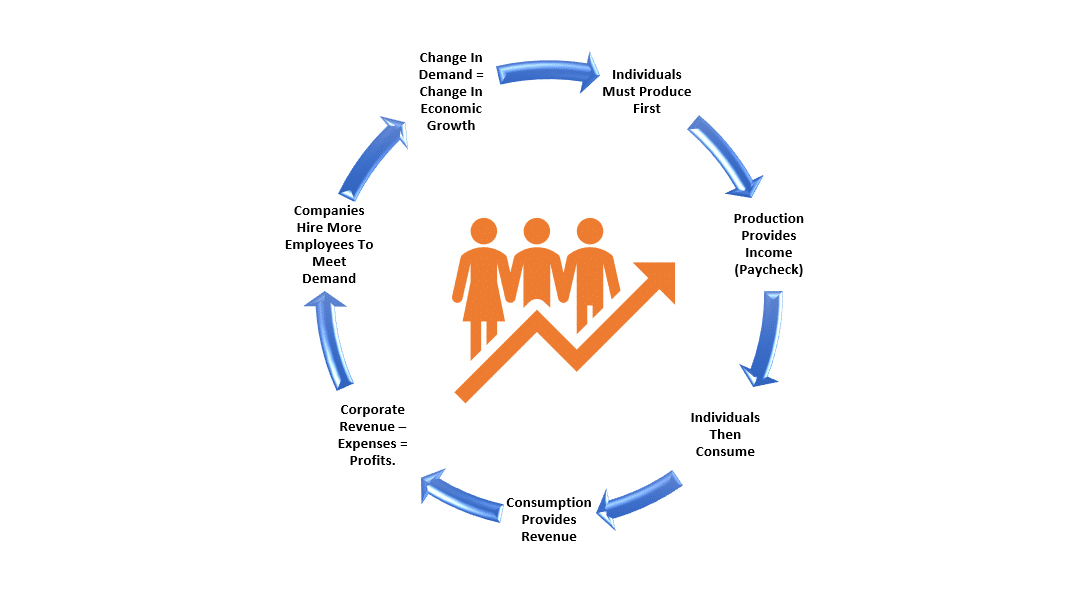

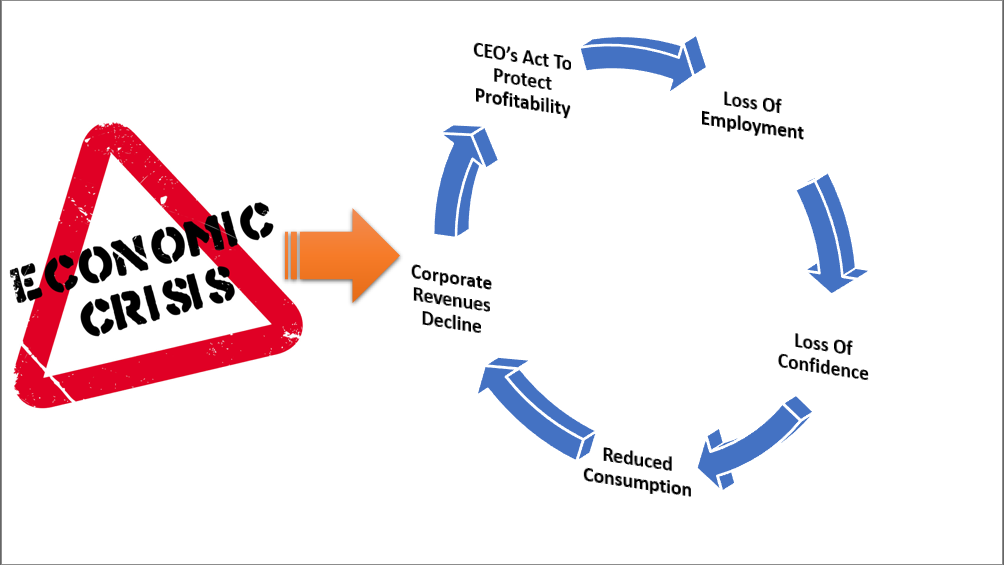

The U.S. is a consumption-based economy. However, consumers can not consume without producing something first. Production must come first to generate the income needed for that consumption. The cycle is displayed below.

Of course, if you bypass the production phase of the cycle by sending checks directly to households, you will get a strong surge in economic growth. As shown in the M2 to GDP chart above, the massive spike in economic growth in the second quarter of 2021 directly resulted from those fiscal policies.

However, once individuals spent that stimulus, the economic activity subsided as the production side of the equation was still lagging. Here is the crucial point about full-time jobs.

“For a household to consume at an economically sustainable rate, such requires full-time employment. These jobs provide higher wages, benefits, and health insurance to support a family. Part-time jobs do not.”

While the media touts the ‘strong employment reports,’ such is mostly the recovery of jobs lost during the economic shutdown. However, the reality is that the full-time employment rate is falling sharply. Historically, when the rate of change in full-time employment dropped below zero, the economy entered a recession.

Notably, given the surge in immigration into the U.S. over the last few years, the all-important ratio of those employed full-time relative to the population has dropped sharply. As noted, given that full-time employment provides the resources for excess consumption, that ratio should increase for the economy to continue growing strongly. However, full-time employment has decreased since the turn of the century as automation, technology, and offshoring have risen. While President Biden recently touted strong employment growth in his SOTU address, full-time employment as a percentage of the working-age population failed to recover to pre-pandemic levels.

Notably, sharp downturns in full-time employment have been coincident with recessionary onsets.

No Job = No Income

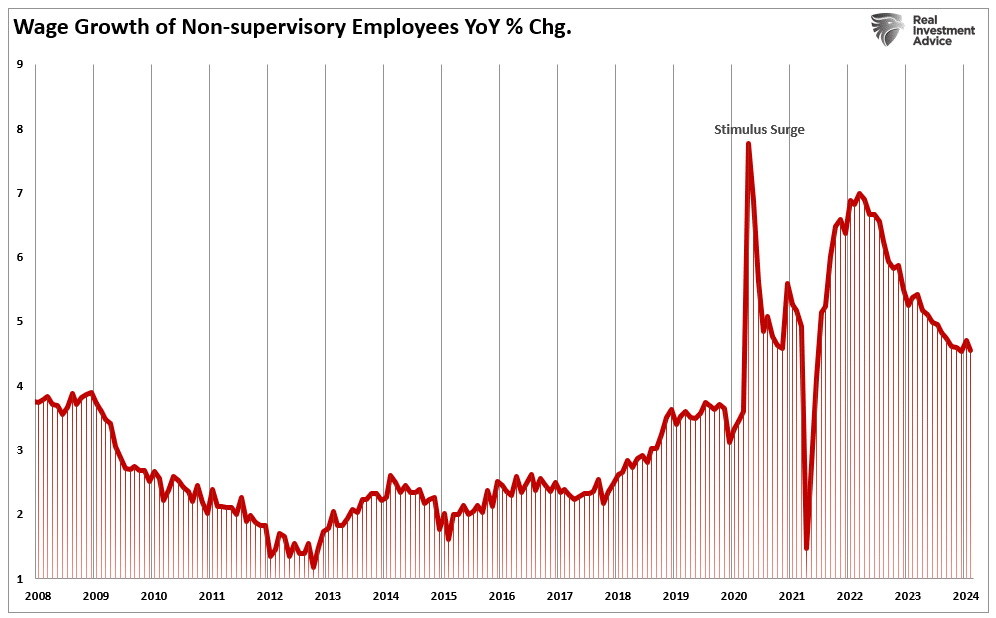

The problem with declines in full-time employment is that, as noted, it negatively impacts economic consumption. While the current administration has been able to offset that decline with a massive increase in deficit spending, the latter is not sustainable. Combine that with the decline in wage growth, and the potential stress on the economy becomes more apparent.

As is always the case, as the economy slows down, employers begin to change the most costly aspect of any business – employment. Cutting full-time jobs is the most efficient way to protect earnings and profitability. While employers tend to hang on to employees as long as possible, employees eventually get sacrificed when protecting profits. As such, a reasonably predictable cycle continues until exhaustion is reached.

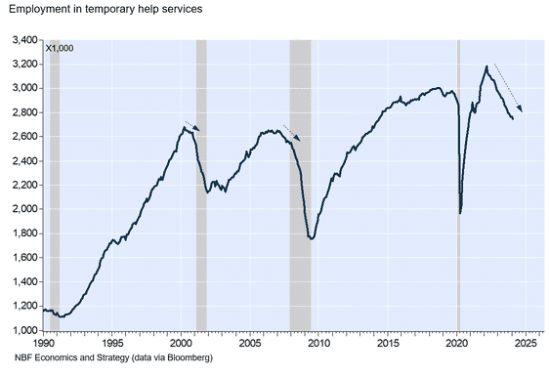

While we are seeing declines in full-time employment as the economy slows, we are now also seeing cuts in temporary help. As noted by the Daily Shot this past week, employment in temporary help services has decreased monthly for the last 23 months.

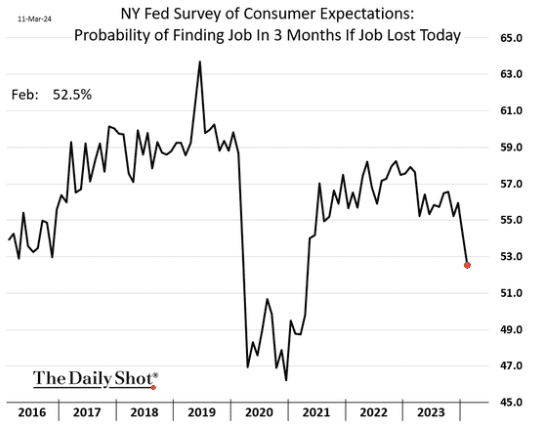

At the same time, consumers across income categories are growing more concerned about their ability to secure new employment should they lose their current job.

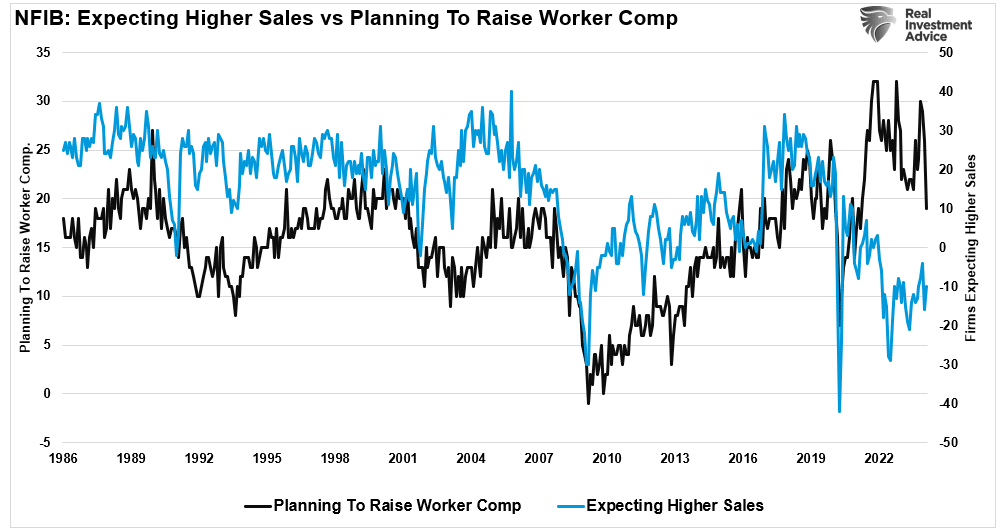

The decline in wages and jobs should be unsurprising. Small businesses comprise 50% of the employment makeup and have failed to see the surge in sales growth touted by the mainstream media. While they initially raised wages to attract talent following the shutdown, that is beginning to reverse sharply as sales fail to materialize.

While there may not be any indication of a recession in the next 12 months, according to mainstream economists, it is likely worth paying attention to what is happening in employment since nearly 70% of economic growth is derived from consumption. Without a job, consumption becomes drastically more challenging for most Americans. Furthermore, temporary jobs won’t fill the gap.

While the recent downturn in full-time jobs is very early, it is a data point worth paying close attention to. Regardless of whatever else is happening in the world, a recession will ensue if full-time jobs continue to decline.

Sure, this “time could be different.” The problem is that, historically, such has not been the case. Therefore, while we must weigh the possibility that analysts are correct in their more optimistic predictions of a “soft landing,” the probabilities still lie with the indicators.

Full-time jobs are an indicator that is worth paying very close attention to.

How We Are Trading It

We remain in the camp that a 5-10% is coming over the next few months. Therefore, we remain cautious about deploying new capital and taking on excess risk in portfolios at current valuations.

With the earnings season behind us, the focus will return to the economic data and the Federal Reserve. As discussed previously, we have yet to see a meaningful rotation into value from growth, leaving this market confined to a tight trading range. We suspect that will change at some point, and our portfolio seems well positioned with some value balanced against growth for such a rotation.

Given we suspect a further correction is forthcoming, we suggest reverting to basic portfolio management rules to reduce portfolio risks for now.

- Trim Winning Positions back to their original portfolio weightings. (ie. Take profits)

- Sell Those Positions That Aren’t Working. If they don’t rally with the market during a bounce, they will decline when it sells off again.

- Move Trailing Stop Losses Up to new levels.

- Review Your Portfolio Allocation Relative To Your Risk Tolerance. If you have an aggressive allocation to equities, consider raising cash levels and increasing fixed income accordingly to reduce relative market exposure.

The market remains quite bullish, but that is also when the risk of a reversal is the greatest.

Have a great week.

Research Report

Subscribe To “Before The Bell” For Daily Trading Updates

We have set up a separate channel JUST for our short daily market updates. Please subscribe to THIS CHANNEL to receive daily notifications before the market opens.

Click Here And Then Click The SUBSCRIBE Button

Subscribe To Our YouTube Channel To Get Notified Of All Our Videos

Bull Bear Report Market Statistics & Screens

SimpleVisor Top & Bottom Performers By Sector

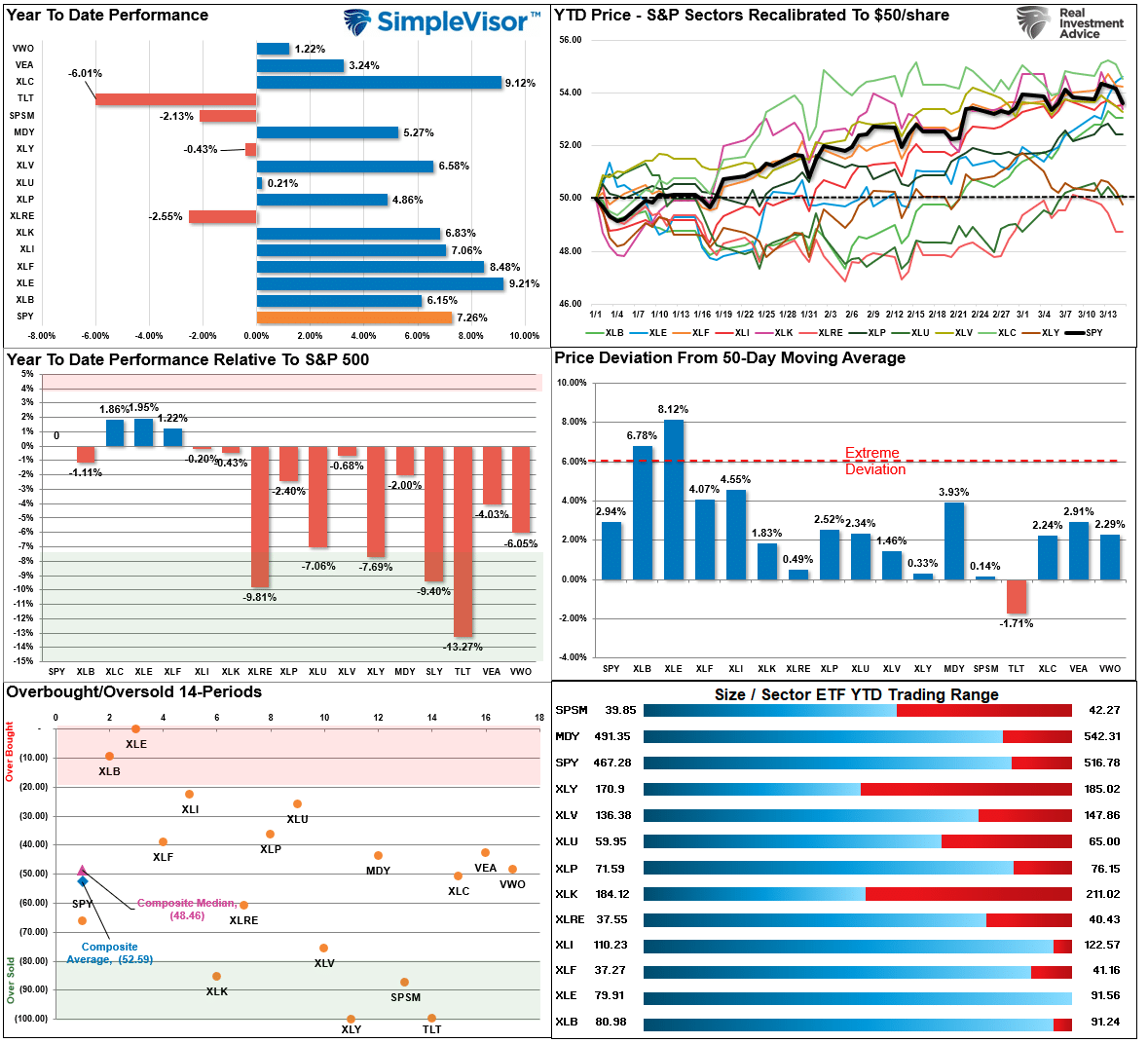

S&P 500 Weekly Tear Sheet

Relative Performance Analysis

As noted last week:

“The push higher put most sectors and markets back to extreme short-term overbought conditions, which will likely limit further upside over the next week as the market continues trading in a tight range since the November lows.”

This past week, the market sold off into Friday, reducing some of that short-term overbought condition. Some cracks are showing in the bullish momentum, so the market may have more work to do before the next leg of the bull market can resume. As shown in the relative performance of the index, this is a market driven by a handful of stocks. If we see further corrective action, there may be a rotation to some of the laggard and more defensive sectors.

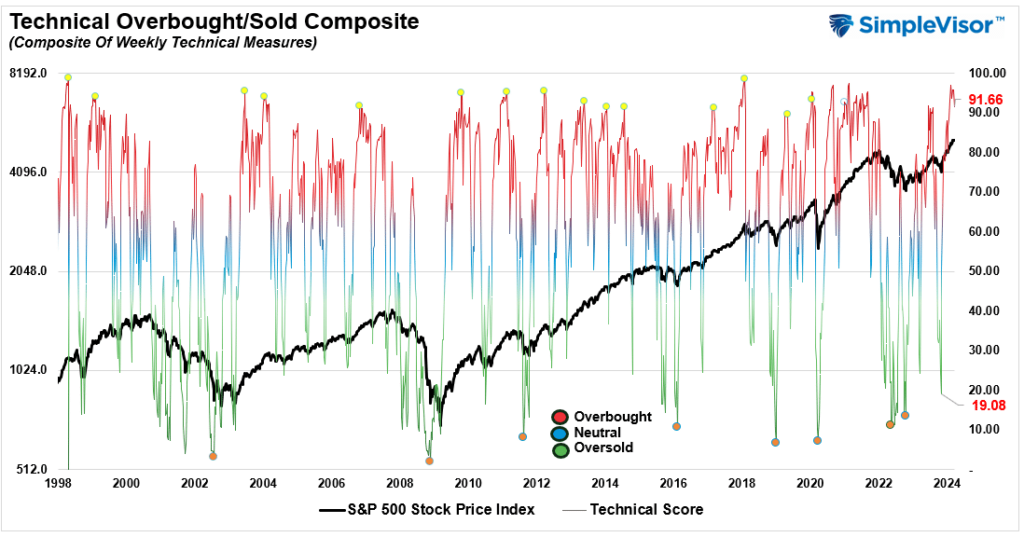

Technical Composite

The technical overbought/sold gauge comprises several price indicators (R.S.I., Williams %R, etc.), measured using “weekly” closing price data. Readings above “80” are considered overbought, and below “20” are oversold. The market peaks when those readings are 80 or above, suggesting prudent profit-taking and risk management. The best buying opportunities exist when those readings are 20 or below.

The current reading is 91.66 out of a possible 100.

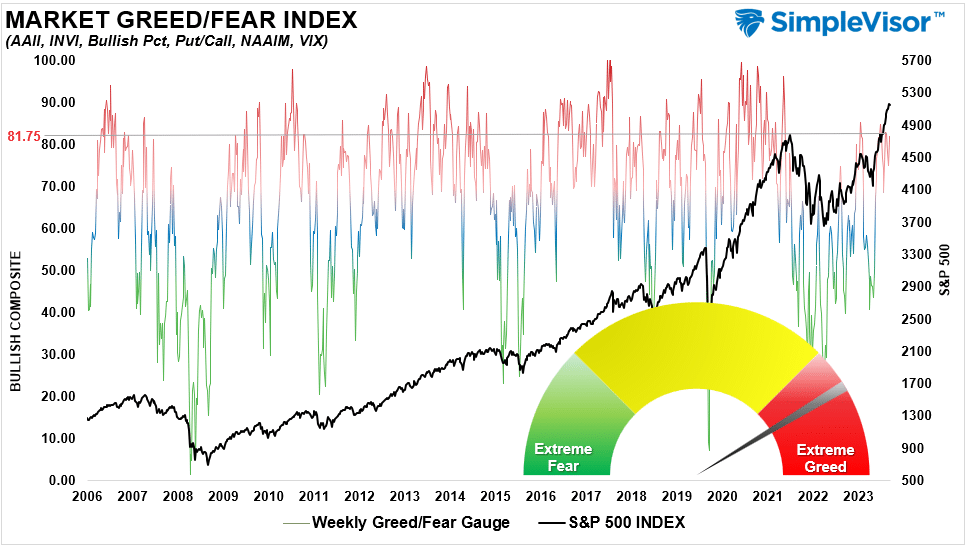

Portfolio Positioning “Fear / Greed” Gauge

The “Fear/Greed” gauge is how individual and professional investors are “positioning” themselves in the market based on their equity exposure. From a contrarian position, the higher the allocation to equities, the more likely the market is closer to a correction than not. The gauge uses weekly closing data.

NOTE: The Fear/Greed Index measures risk from 0 to 100. It is a rarity that it reaches levels above 90. The current reading is 81.75 out of a possible 100.

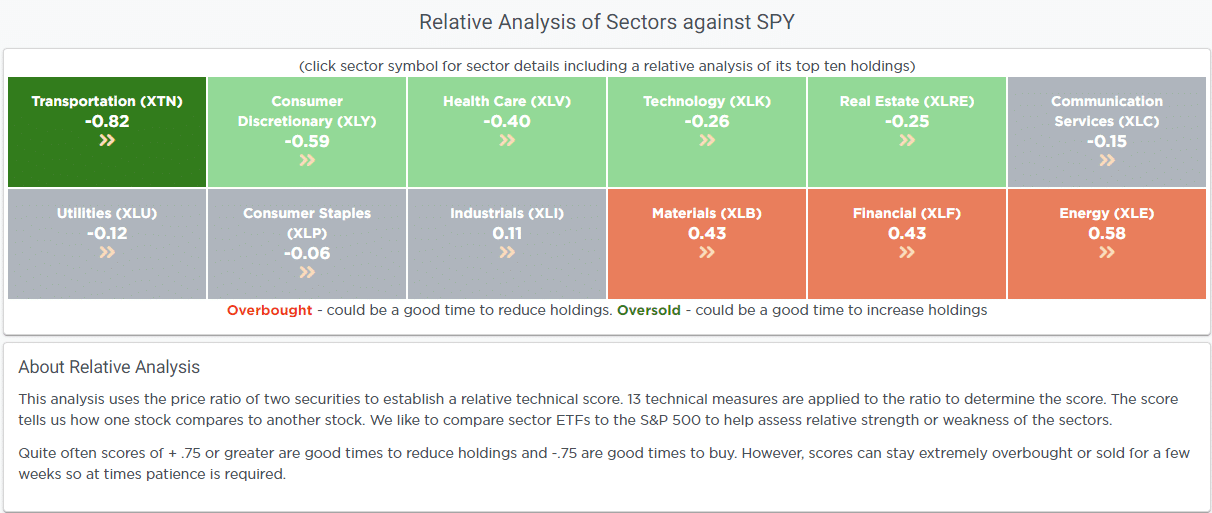

Relative Sector Analysis

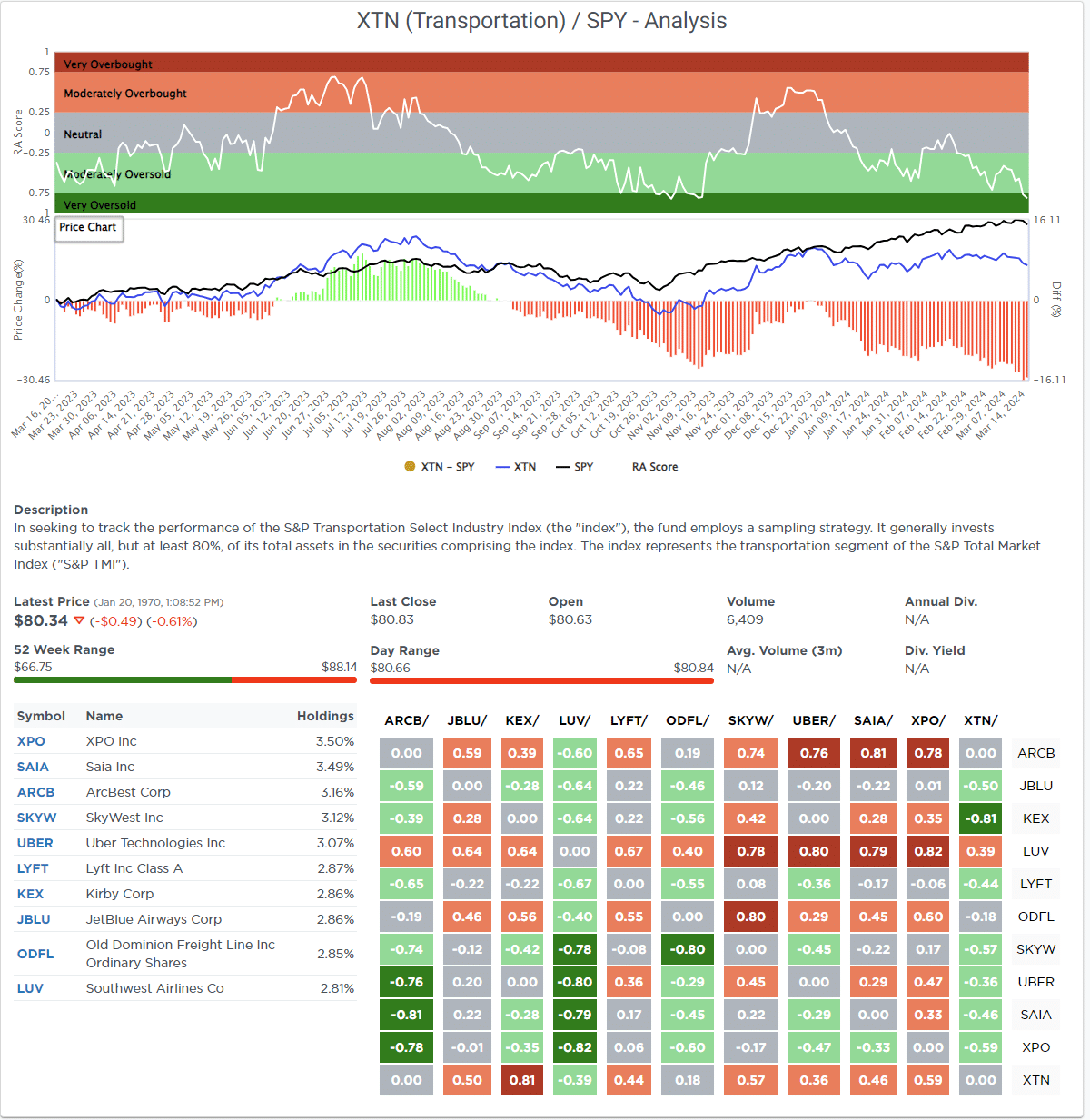

Most Oversold Sector Analysis

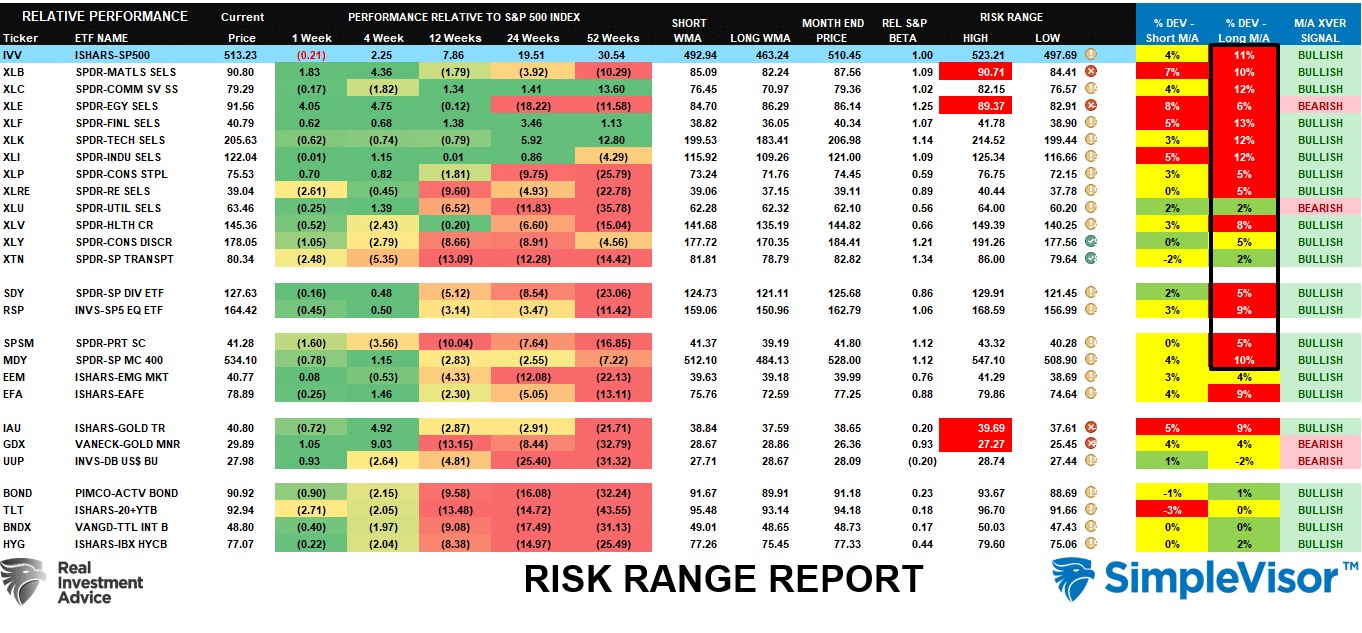

Sector Model Analysis & Risk Ranges

How To Read This Table

- The table compares the relative performance of each sector and market to the S&P 500 index.

- “MA XVER” (Moving Average Crossover) is determined by the short-term weekly moving average crossing positively or negatively with the long-term weekly moving average.

- The risk range is a function of the month-end closing price and the “beta” of the sector or market. (Ranges reset on the 1st of each month)

- The table shows the price deviation above and below the weekly moving averages.

Deviations for many market sectors from their longer-term moving averages are extreme. Gold, Gold Miners, Energy, and Materials are well outside their normal risk ranges as well, suggesting profit-taking should be implemented. The bullish backdrop of the market remains, but last week may have started a period of correction or consolidation.

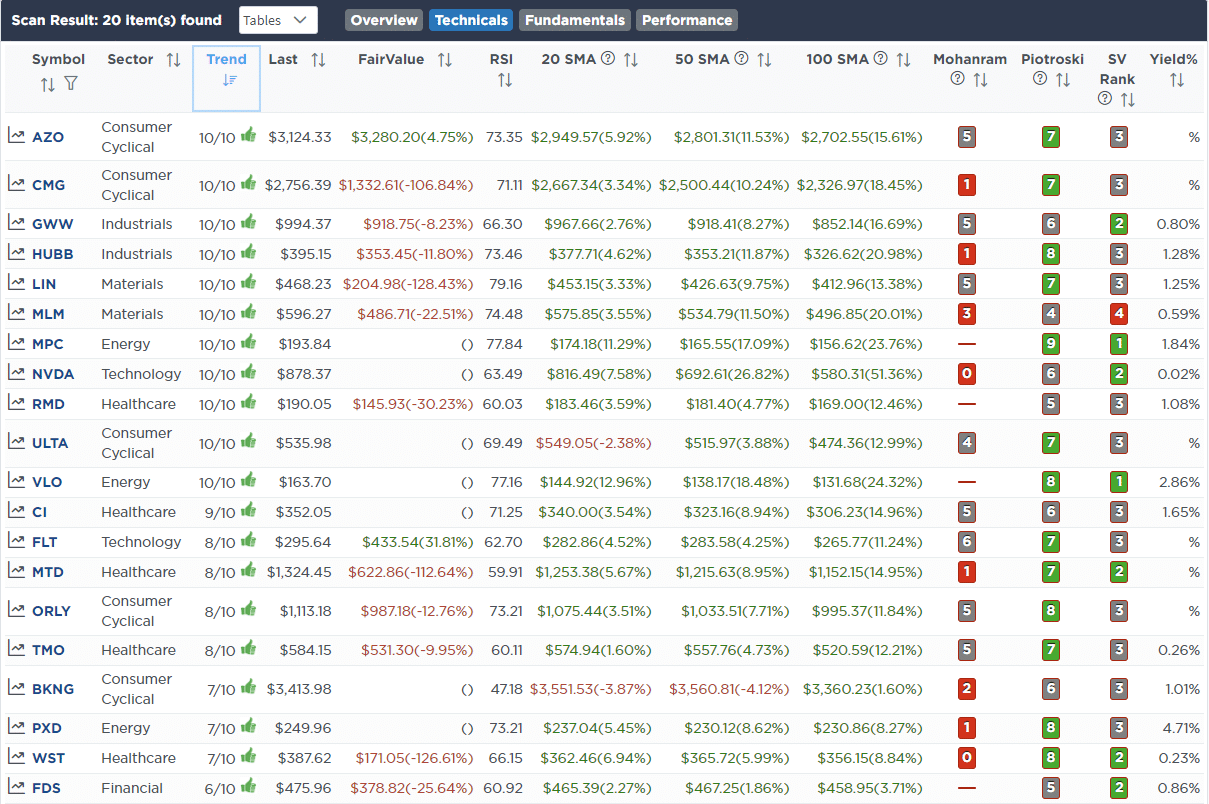

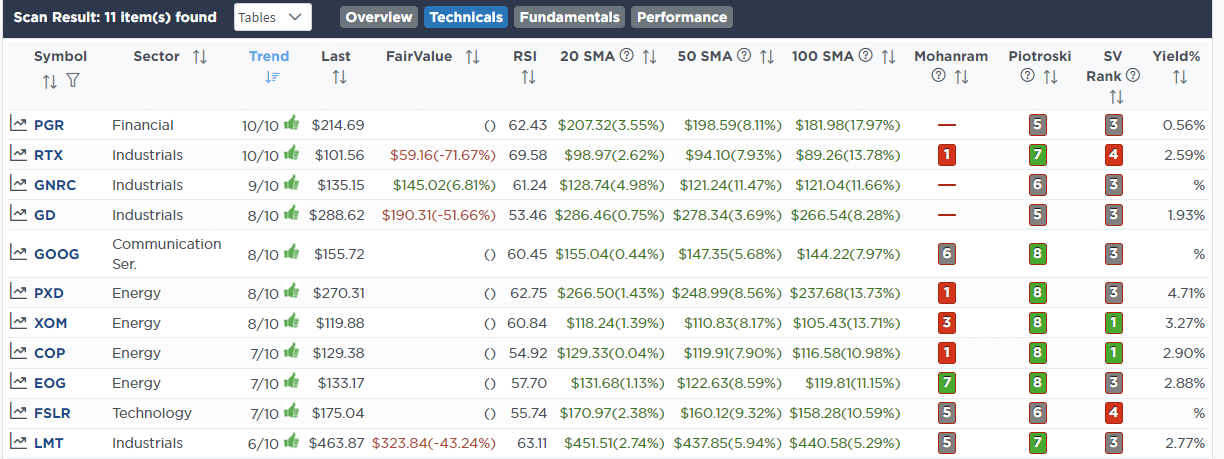

Weekly SimpleVisor Stock Screens

We provide three stock screens each week from SimpleVisor.

This week, we are searching for the Top 20:

- Relative Strength Stocks

- Momentum Stocks

- Fundamental & Technical Strength W/ Dividends

(Click Images To Enlarge)

R.S.I. Screen

Momentum Screen

Fundamental & Technical Strength

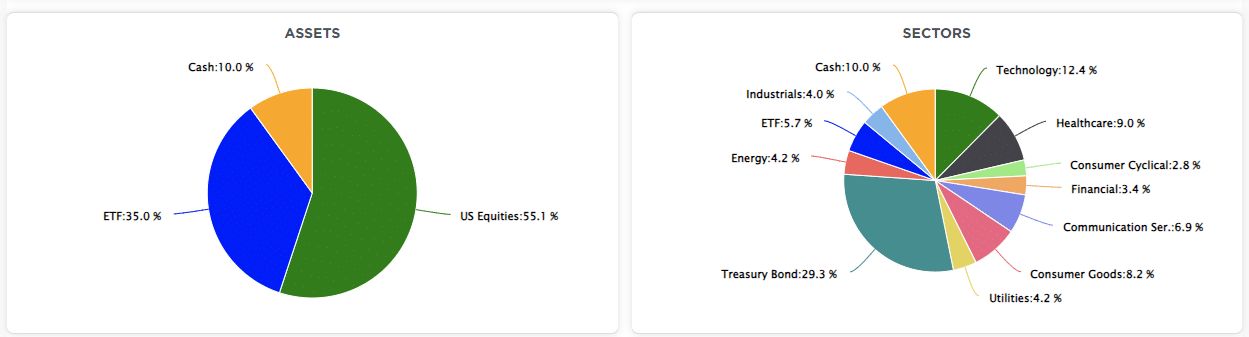

SimpleVisor Portfolio Changes

We post all of our portfolio changes as they occur at SimpleVisor:

No Trades This Week

Lance Roberts, C.I.O.

Have a great week!