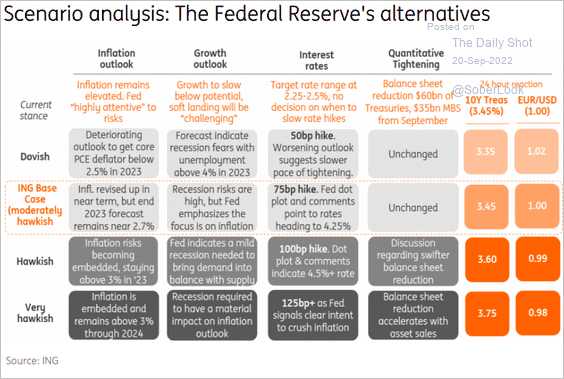

At 2 pm ET, the Fed’s FOMC will update monetary policy. Given the Fed’s role in managing liquidity, investors should be very interested in how the FOMC talks about inflation, growth, interest rates, and QT, as well as any adjustments they make to monetary policy. The table below from ING provides interesting guidance on what we might expect. While we agree on the range of possible outcomes, we disagree on ING’s hawkish-dovish characterizations. ING believes the base case is moderately hawkish. Using their table, we think it’s hawkish. Many FOMC members, including Jerome Powell, want to keep policy rates at 4% or higher and keep them there through next year. We also disagree with them on interest rates. As we discussed yesterday, markets imply a .75bps rate hike, which we believe is hawkish, not moderately hawkish. A 100bps rate increase would be very hawkish.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended August 12 (0.2% prior)

- 10:00 a.m. ET: Existing Home Sales, August (4.70 million expected, 4.81 million prior)

- 10:00 a.m. ET: Existing Home Sales, month-over-month, August (-2.3% expected, -5.9% prior)

- 2:00 p.m. ET: FOMC Rate Decision (Lower Bound), September 21 (3.00% expected, 2.25% prior)

- 2:00 p.m. ET: FOMC Rate Decision (Upper Bound), September 21 (3.25% expected, 2.50% prior)

- 2:30 p.m. ET: FOMC Press Conference

Earnings

Market Trading Update

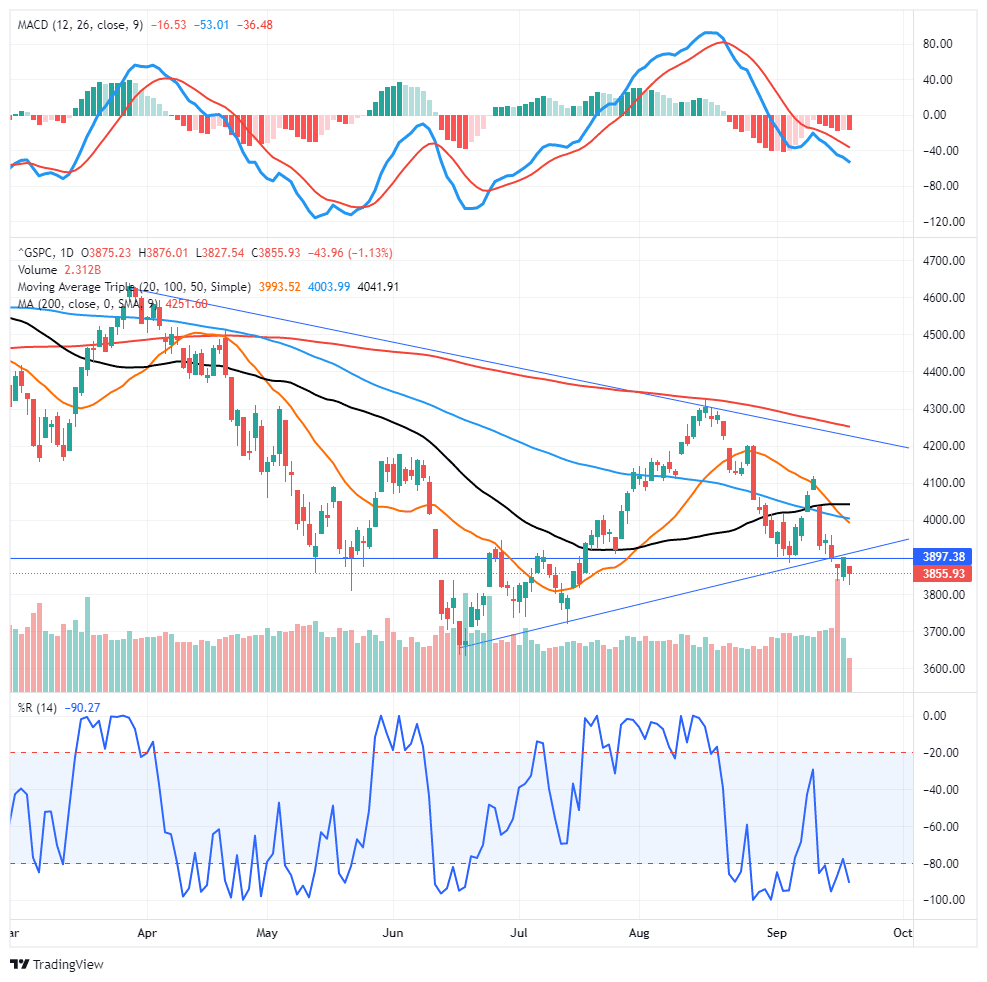

After a small rally yesterday, the market sold off ahead of today’s FOMC meeting announcement. After the surprise comments by Jerome Powell at Jackson Hole, the markets were unwilling to take on risk ahead of the meeting announcement. We expect a 75bps hike today with no real change to the messaging, which could provide a bit of a relief rally to the markets. As shown, the support level did give way yesterday, which will be critical for the market to recover by the week’s end. Otherwise, we will likely see a test of the July lows.

As noted, the markets are oversold, but the “sell signal” remains intact, keeping downward pressure on stocks. We suggest using any rallies toward the 50-dma as an opportunity to reduce risk and raise cash levels as needed.

Are 4% One-Year T-Bills A Good Investment?

The graph below shows the long-term history of one-year T-bill yields and compares the recent surge in yields versus prior periods. While many investors focus on the 4% yield and the fact that it is now at its highest point in almost 15 years, the bigger story is the recent surge in yields. In just one year, the one-year yield has risen 4%. The last time yields rose that much in one year was about 40 years ago.

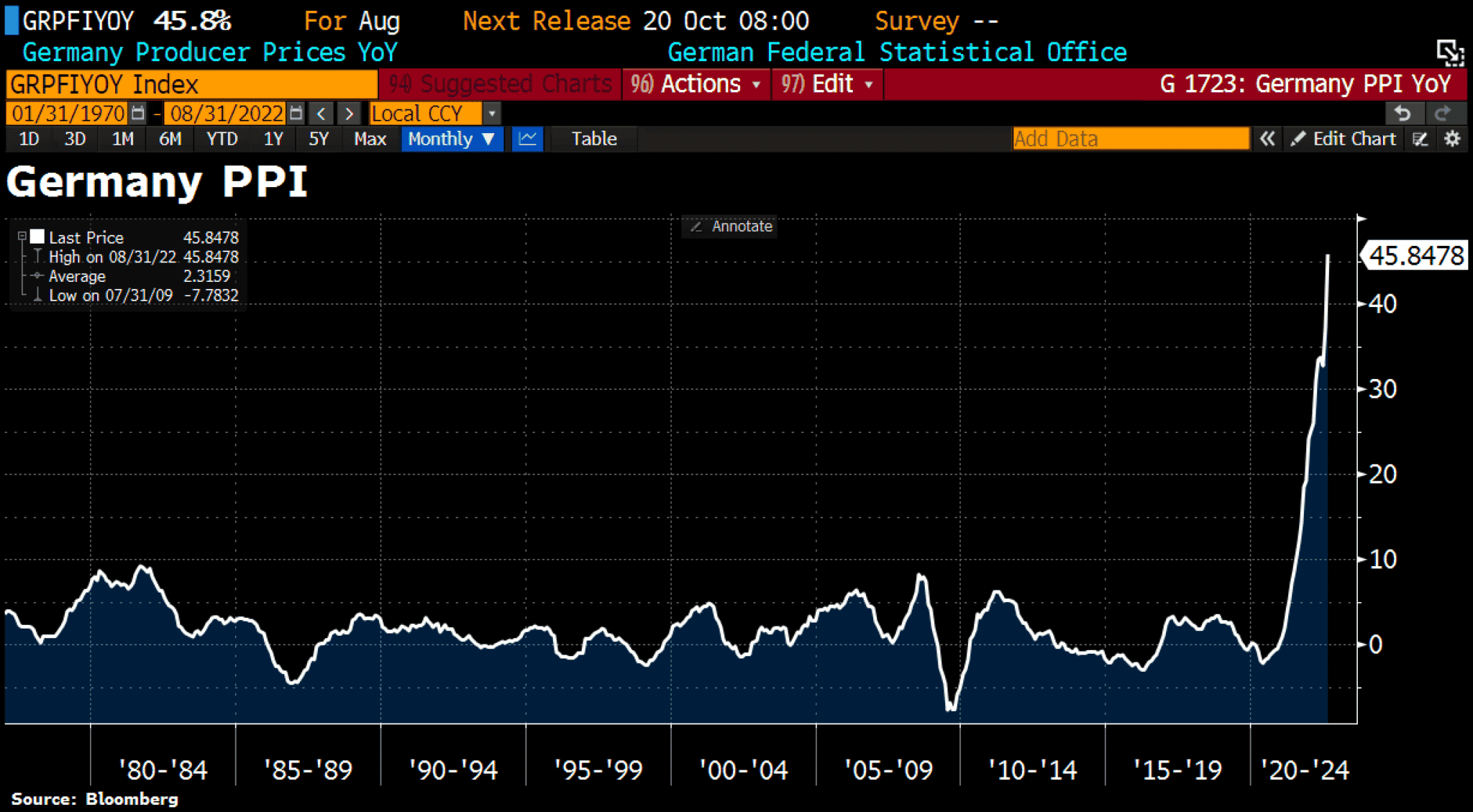

German Inflation Off The Charts

Germany’s year-over-year PPI accelerated to 45.8% in August from 37.2% in July. As shown below, that is the largest annual price increase since at least 1949. The monthly figure jumped by 7.9% in August, also the highest monthly increase since 1949. Germany is a major industrial power. There is little doubt that its manufacturers and chemical producers will pass on these rising costs to its customers, many of which are U.S. companies. German PPI will keep pressure on U.S. PPI and CPI.

Fiscal Tightening is Underway

It’s not just the FOMC and monetary policy that is slowing economic activity. The graph below from the Tax Foundation shows that Federal tax collections as a percentage of GDP are 3% above the average of the last 70 years and even more so versus the last 20 years. Further, they are at their highest point as a percentage of GDP since WWII. Larger tax collections mean less consumption and will negatively impact economic growth. We will have to watch this closely to see if the recent high will likely stay at current levels or is just a temporary reaction to the massive fiscal response during the pandemic.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.