Financial friction burns wealth in 5-insidious manners.

What is financial friction?

Financial friction burns wealth when money is lost.

Financial friction burns wealth when there’s resistance – the heat of conflict, clash of opinion. When money lies between two opposing forces, friction can destroy wealth.

What are the elements of financial friction that burn wealth? What are financial gaps that require attention?

Friction #1: The Gap Between an Estate Plan and Family.

Priorities have changed as we spend more time at home. A strong focus on family. Attorneys across the country now witness renewed interest in estate plans. Young and old contemplate what happens when they’re gone.

Formal estate planning is essential – Proper wills, powers of attorney, advance directives in case of incapacitation. However, do not forget the words. No – not the legal, cold verbiage placed in a fancy ‘pleather’ binder read and executed upon death. I mean the warm words of love and reason. The thoughts behind estate intentions should be communicated clearly by grantors while they’re alive and healthy enough to do so.

Open communication eliminates the friction family members may succumb to after a loved one passes. I witness this kind of friction create irreparable separation. Siblings who no longer communicate. Children who won’t talk to parents again. All because the legal estate plans do the talking with no personal explanation behind the motives.

Now that we’re quarantined, it’s an opportune time for open communication with loved ones, especially parents. In my family, elders were not questioned about financial matters or money decisions. However, I didn’t have a pandemic to motivate me to ask questions. The discussion of finances with family especially parents, can be difficult and awkward.

One of the organizations I support – Aging with Dignity, has created a COVID-19 conversation guide. Five Wishes is unique among all other living will and health agent forms because it speaks to all of a person’s needs: medical, personal, emotional and spiritual. Five Wishes also helps to guide and structure discussions with your family and physician. Try it and see it it helps jump start conversations!

Financial friction burns wealth through poor or non-existent estate planning.

Friction #2: The Gap Between Financial Services and Retirement Account Withdrawals.

The financial services industry perceives every market downturn as an opportunity to purchase stocks. This advice can be detrimental to pre-retirees or those five years or less from retirement. The priority for this group should be to limit downside risk so retirement plans are not postponed. Naturally, losses are inevitable. It’s the price investors pay for stock risk. However, those who plan to retire in five years or less or been in retirement less than ten, should focus primarily on the risk of portfolio losses vs. the potential for gains.

Professor of retirement income at The American College Wade Pfau weighed in on the topic of portfolio withdrawals during the COVID-19 crisis recently in an interview for ThinkAdvisor.

The financial industry touts an annual fixed 4% withdrawal rate as a rule of thumb. During a bear cycle or headwind for stock market returns as we’re in now, the 4% Rule is perilous. Wade Pfau, one of the leading academics in the financial field believes the same.

He says in the interview with Jane Wolman Rusoff dated April 14, 2020:

I did some updates in mid-March; and for an investor taking a moderate amount of risk, I put out 2.4% as my equivalent of the 4% rule. That’s still about the same today.

Think about it: The ‘sacred’ 4% Withdrawal Rule is now cut in half. Investors who blindly followed this tenet or were convinced to do so by their financial partners, need to re-think their lifestyle spending next year.

Financial friction burns wealth by adherence to stale rules of thumb.

Friction #3: The Gap Between You and Your Broker.

Most likely, your financial plan portfolio return estimates continue to be too optimistic. To a broker, flat or bear market cycles don’t exist. The dogma is detrimental to your financial health. Fall for it and risk spending an investment life making up for losses or breaking even.

Most financial planning software creates outcomes based on “Monte Carlo” simulation. It’s as close as planners get to represent the variability of market returns over time. Monte Carlo generates randomness to a portfolio and simulates, perhaps thousands of times, around an average rate of return. Unfortunately, asset-class returns most Monte Carlo tools incorporate tend to be optimistic. In addition, even though Monte Carlo simulates volatility of returns, it does a very poor job representing sequence of returns which I think of as a tethered rope of poor or rich returns.

Per friend and mentor Jim Otar, a financial planner, speaker and writer in Canada:

“Markets are random in the short term, cyclical in the medium term, and trending in the long term. They are neither random, nor average, nor trending in all time frames. Secular trends can last as long as 20 years (up down or sideways). The randomness of the markets are piggybacked onto these secular trends. Assuming an average growth and adding randomness to it does not provide a good model for the market behavior over the long term and it makes the model to “forget” the black swan events.”

It’s why at RIA as a backstop, we employ various planning methodologies which take into account the nature of market cycles and where your goals fall within them.

Granted, a financial plan won’t be the popular talk at your next ZOOM cocktail party. However, a plan provides peace of mind. The only person who succumbs to hidden dangers in poorly executed financial plans is you. The friction derived from your broker’s lack of knowledge about market cycles must be a catalyst for change. Or at the least, awareness.

Financial friction burns wealth through lack of awareness of real market dynamics.

Friction #4: The Gap Between Valuations and Your Portfolio Outcomes.

Our financial planning team is prepared for a future of anemic portfolio returns. Due to our foresight, clients’ plans have not been disrupted. We are thankful for this outcome.

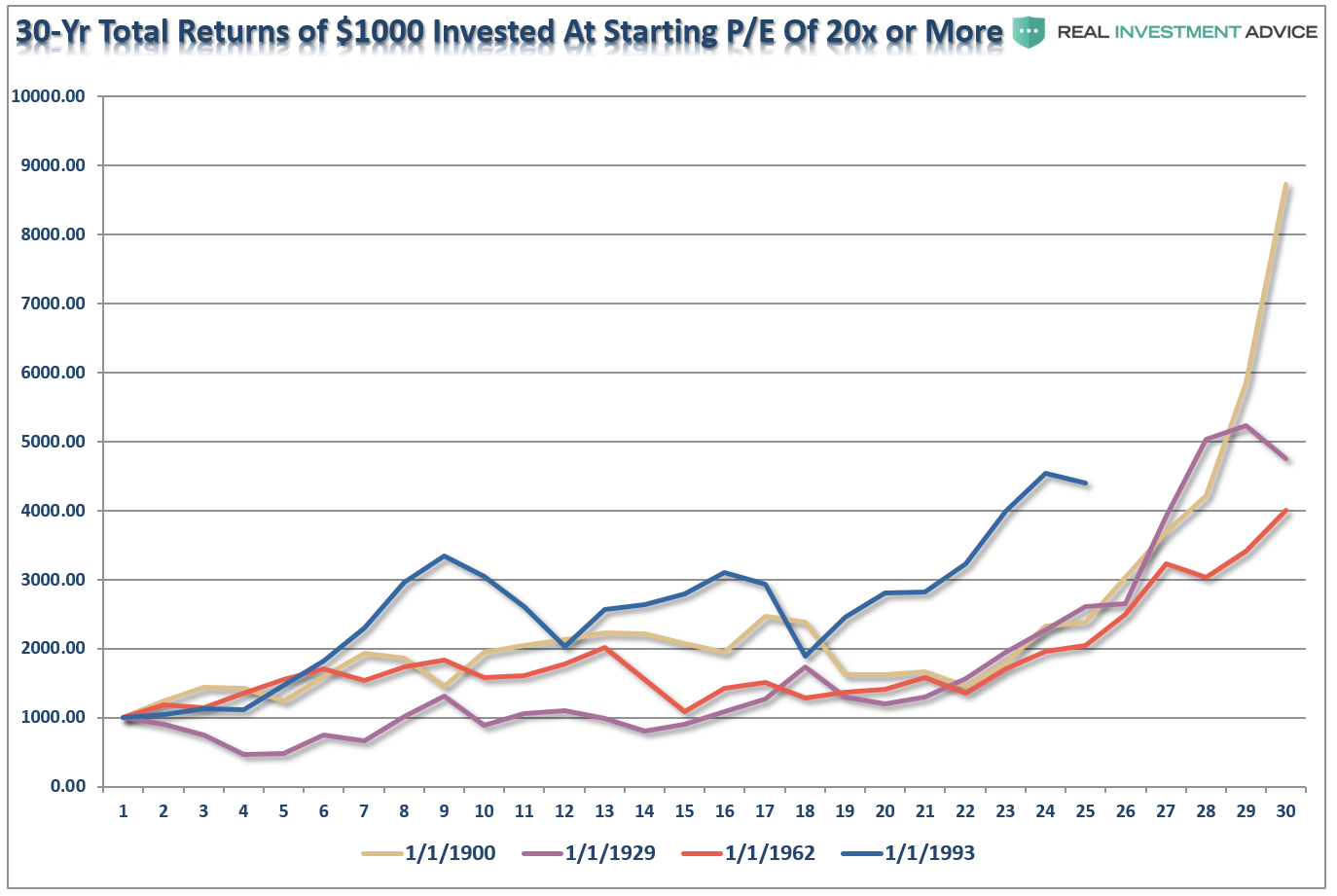

Despite the unprecedented stock market volatility so far this year, the Shiller P/E remains extended at 26.56X. Therefore as a firm, we are not altering our view: Investors are going to face a long-term headwind to portfolio returns.

The Shiller P/E is a poor predictor of short-term market performance. However, over long periods, lofty valuations lead to lower future returns. Displayed below is our analysis of the growth of $1,000 over 30 years when the Shiller PE is at 20X or higher. Based on our research, retirees should prepare for a minimum of one decade of sub-par investment returns and adjust expectations accordingly.

Until valuations are at or below 20X, expect greater risk and lower returns. In fact, all additional risk will do is add risk. Mind this gap or the danger of burning through money before life expectancy is a real possibility.

Financial friction burns wealth by ignoring lofty stock valuations.

Friction #5: The Gap Between Your Retirement Income and Social Security.

Due to lower projected returns and the long-term economic after-effects of the pandemic, the maximization of guaranteed retirement income from Social Security and the purchase of income annuities should be given higher priority. Prospective retirees will need to fill the gaps of poor returns on variable assets with guaranteed income vehicles. Even more so now. I’ll explain.

Cost of living adjustments for Social Security will likely be close to zero over the next five years. At the same time, recipients will absolutely witness increases for Medicare Part B premiums and deductibles which will eat into Social Security retirement benefits. Preliminary information outlines how the pandemic will have profound effects on the cost of healthcare delivery to older Americans.

Currently, we face a deflationary tailwind due to demand destruction and the downward spiral in oil prices. However, I believe there’s a looming inflationary crisis. I didn’t believe inflation would be an issue post-financial crisis. Today, I envision renewed focus on nationalism vs. globalism whereby prices on goods will increase as manufacturing is pulled from China and selectively brought home. In addition, wage growth may stagnate for years as companies attempt to rebuild profit margins. These changes have the potential to inhibit consumer demand, place pressure on corporate earnings and strain household spending budgets.

There’s another issue that concerns me:

Per a working paper by Andrew G. Biggs titled ‘How the Coronavirus Could Permanently Cut Near-Retirees’ Social Security Benefits,’ for the Wharton Pension Research Council, based on the sharp economic downturn, some groups of near-retirees are likely to suffer substantial permanent reductions to their Social Security Retirement benefits.

Those born in 1960 or later could see annual benefits in retirement reduced by around 13% with losses over their retirement period by close to $70,000. This is based on the assumption of a 15% decline in the Social Security Administrations measure of economy-wide average wages in 2020.

The Social Security benefits formula not only examines an individual’s highest 35-years of earnings, but also the national Average Wage Index (AWI) to calculate a worker’s PIA or Primary Insurance Amount. ‘Bend points’ in the formula are usually increased along with average wages in the economy. For the 1960 birth cohort, the bend point values used to calculate benefits will be equal to the values in 2020, adjusted by the growth of the Average Wage Index between 2018-2020. For 2018, the most recent year for data available, the AWI was $52,146. The projection for 2020 in the Social Security Trustees’ Report was to be $56,396 – 8% higher!

A significant decrease in the 2020 projection would reduce Social Security benefits for future recipients age 60 or younger. Those age 62 or older and current benefit recipients are not affected by changes to the AWI. Personally, I believe the author is too conservative when it comes to the negative long-term affects of the pandemic on the Average Wage Index. I foresee a challenge with wage growth over the next five years which means the AWI estimates may decrease again in the future. The possibility of this event requires close monitoring for financial planning purposes.

In addition, planners need to remain aware of the overall state of Social Security which is funded primarily by payroll taxes. Payroll taxes may be cut for a period by Congress and the Executive Branch or simply by less of the population working and paying in over an extended period. Per Alicia H. Munnell, Director at the Center for Retirement Research at Boston College, the sudden collapse in payroll taxes due to COVID-19 may accelerate the depletion of the trust fund by two years – 2033 – which means benefits could be reduced by 25% at that time.

It’s crucial for financial professionals to keep abreast of the economic aftermath of the pandemic and to determine whether financial plans maintain an adequate level of guaranteed income to compensate for future changes.

At RIA, based on negative outcomes from the current crisis, we believe that no less than 65% of mandatory fixed expenses in retirement, should be covered by guaranteed income vehicles such as Social Security and other types of annuities that provide lifetime income.

Naturally, everybody’s situation differs. There are people who live frugally and maintain modest retirement expectations. Therefore, Social Security will be the only guaranteed income needed to complement withdrawals from variable asset portfolios. However, headwinds to Social Security may change otherwise successful outcomes.

Your financial planner should isolate how much of your future retirement income is to be generated by variable assets like stocks and bonds vs. guaranteed income vehicles such as Social Security. From there, personal recommendations can be made to fill the gap or friction caused by the current crisis we now face.

Financial friction burns wealth through the avoidance of guaranteed income options.

Friction within household finances isn’t a good thing.

Now is the time to do what you can to minimize the heat.