The price of cattle futures has been bullish since troughing during the early days of the pandemic. As we share below, Live Cattle futures are up 10% this year and about 125% since early 2020. The price of live cattle just briefly eclipsed the late 2014 peak. One of the reasons for the bullish trading in cattle futures is that supplies are lean. Per the USDA, the inventory of cattle and calves has fallen to 89.3 million. Such is the lowest level since those at the prior peak and down about 10% from pre-pandemic inventories. Also helping cattle prices, the average weight of cows declined due to last winter’s harsh weather conditions. Lastly, exports of U.S. beef have grown substantially since 2015. For more details, please click the following LINK from the Progressive Farmer.

We raise this topic to teach an essential lesson about commodity ETFs. While bullish cattle futures was a great trade, many investors cannot buy futures contracts. Most bullish investors on cattle or any commodity must find an ETF that can replicate the commodity. Such is often tricky. As we share below, the ETF that best mimics a position in cattle futures, COW, is flat on the year, while futures are up over 10%. Some ETFs, like GLD, which holds physical gold, track gold prices well. Most others that cannot store the physical commodity find it challenging to replicate the performance of a futures contract.

What To Watch Today

Earnings

- No notable earnings releases

Economy

Market Trading Update

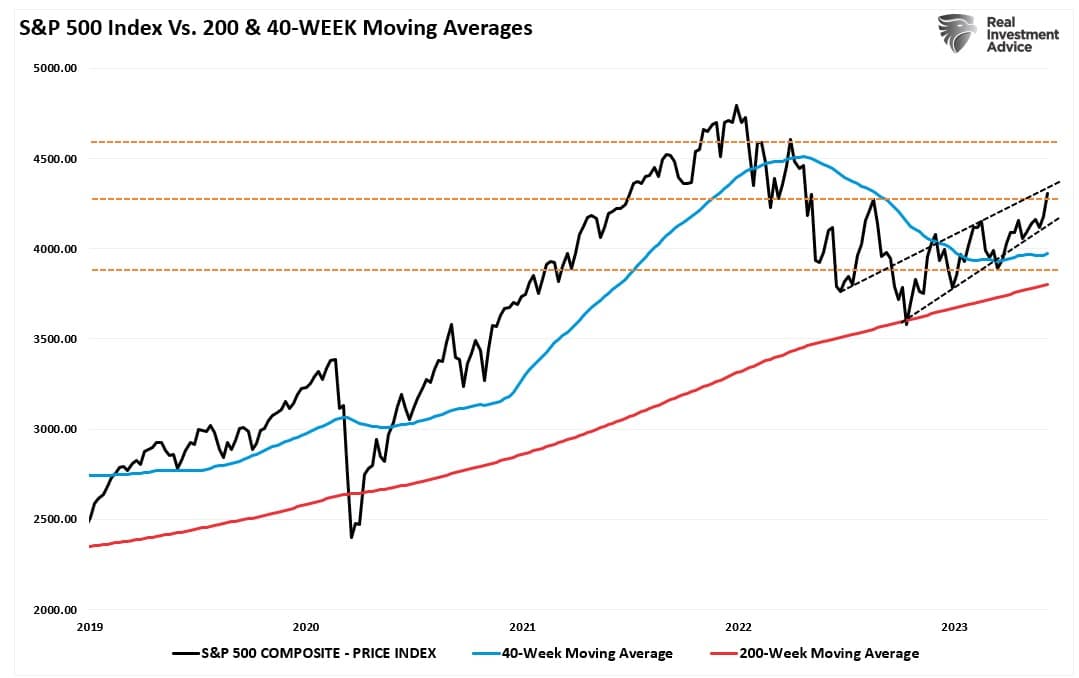

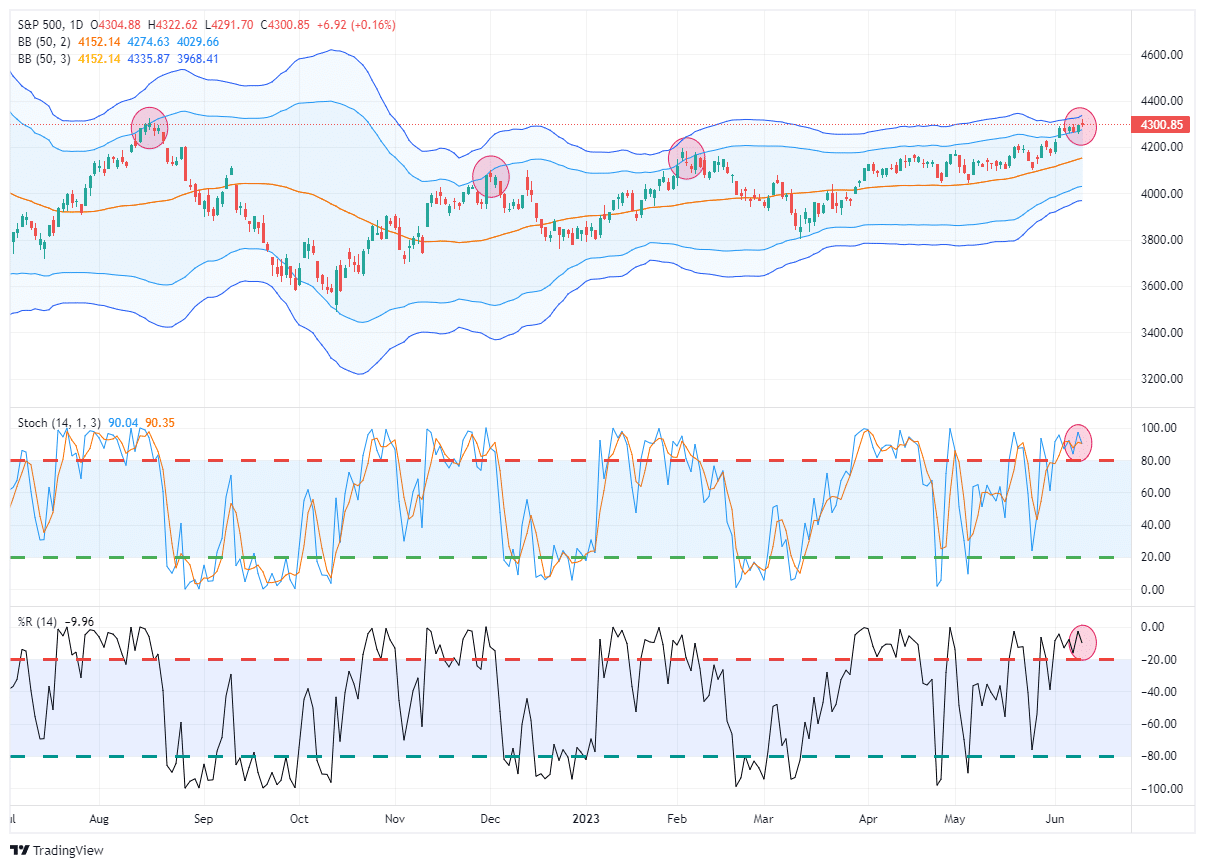

Last week, we touched on the current bifurcation of this rather lopsided market and suggested sector rotations are likely. The chase for anything “artificial intelligence” related has heated up recently, and deviations from moving averages are now more extreme. Nonetheless, the market approached our target for this rally that we discussed previously:

“The S&P 500 has scored seven weekly closes above its 40-week moving average, which is a positive sign. In addition, the market has cleared the 40-week DMA downtrend line from January and December 2022, suggesting a potential bullish turn in the trend. Assuming supports hold, the next major resistance beyond the post-FOMC peak at 4195 is the August 2022 peak at 4325 (orange dashed line).” – March 7th

Here is the updated version through Friday’s close.

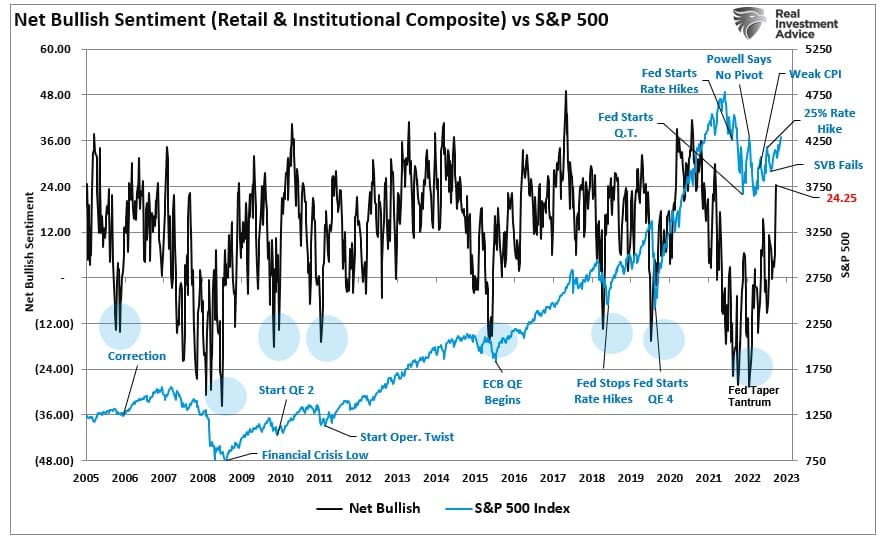

With the market pushing into that resistance at 4300 and the top of the rising trend channel from the October lows, a pause in the advance would be unsurprising. However, the rally has finally convinced the bears to come off the sidelines, with professional and retail investors getting substantially more “bullish” over the last two weeks.

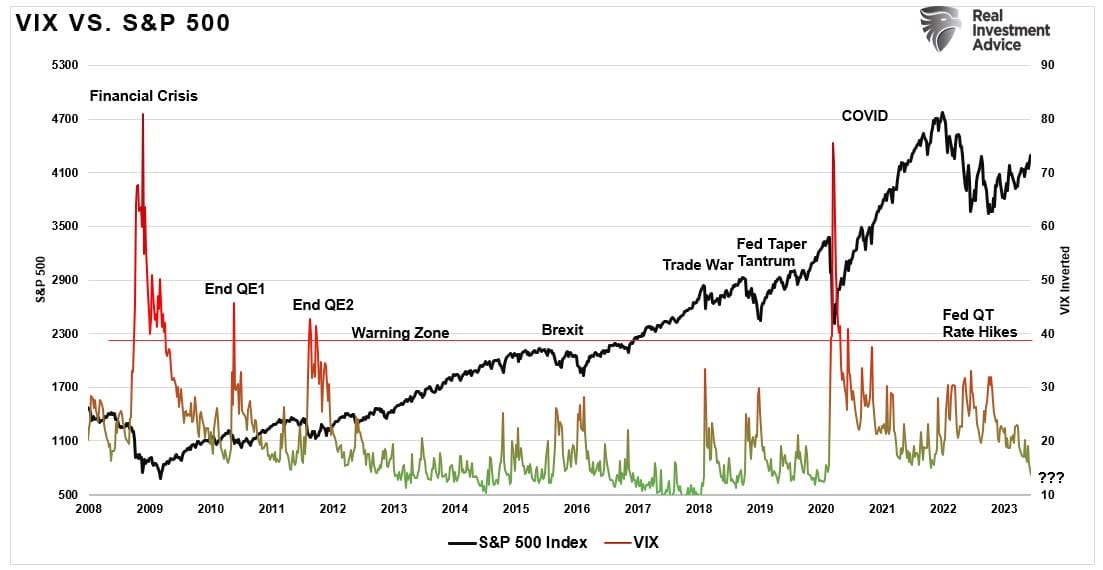

Such a jump in sentiment is unsurprising, given the sharp decline in volatility over the same period.

The consequence, of course, is a market that is pushing more extreme overbought levels than we have witnessed in quite some time. While it is possible for these extremes to last longer than logic would predict, it does suggest that without a correction to “reset” the markets, the upside will likely be limited near term.

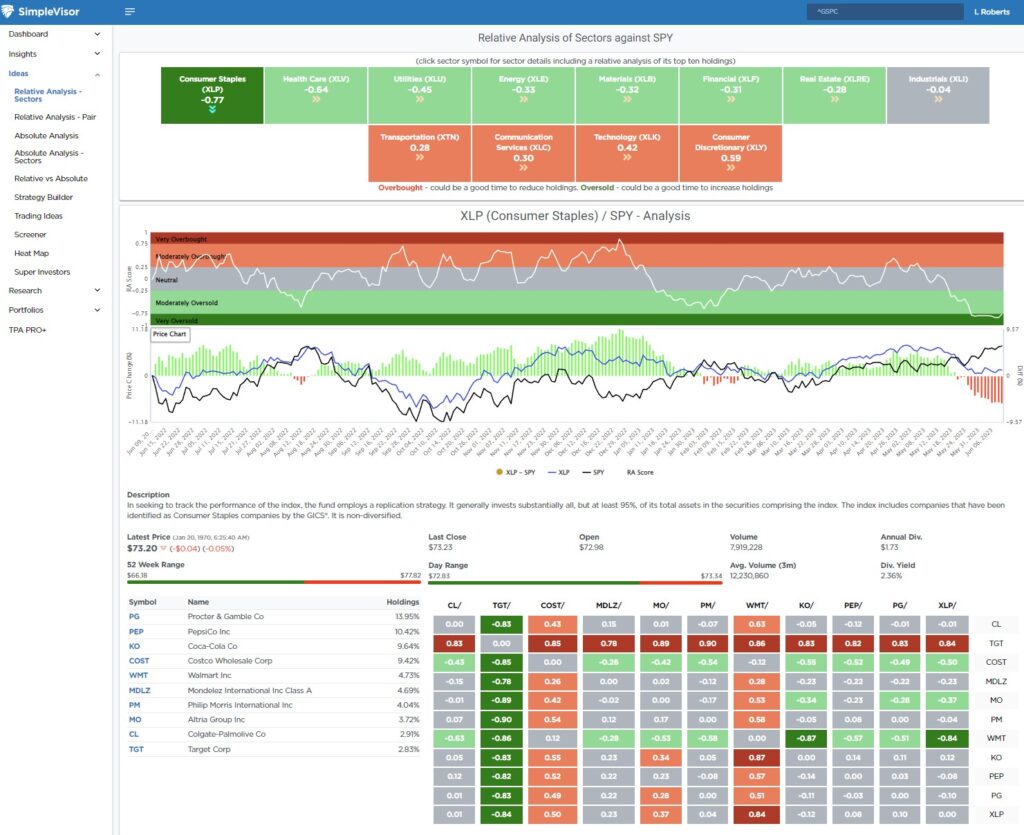

This need for corrective action will likely be the basis for market sector rotations we have discussed over the last few weeks. Look to take profits in grossly oversold conditions and look for opportunities in out-of-favor markets. For ideas, go to SimpleVisor.com and check out the Sector Rotation Analysis we provide under the IDEAS tab.

The Week Ahead

The Fed highlights this week as they conclude their FOMC policy meeting on Wednesday. Therefore, we will get updated on its policy stance via the meeting statement, its quarterly economic projections, and Powell’s press conference. As we highlight below, the market implies a 22% chance they hike rates by 25bps but a roughly 50/50 chance the Fed will hike rates at the July or September meetings. The market is finally taking the higher-for-longer Fed narrative more seriously. However, they expect about 2.00% in rate cuts in 2024. If that comes to fruition, will it have been due to weaker economic activity or recession, or might it be because inflation is firmly back near the Fed’s 2% target? That will be the million-dollar question later this year and next.

To help answer that question, the Fed will get CPI data on Tuesday and PPI on Wednesday. The monthly CPI rate is expected to be +0.3%, equating to 3.6% annualized inflation. The year-over-year rate is expected to fall from 5.5% to 5.4%. The market will focus more on the year-over-year rate, which is still too high for the Fed’s liking, despite more recent data pointing to lower annualized inflation rates. PPI is much tamer than CPI, with expectations for a year-over-year rate of 2.1%. Following the Fed meeting, the Census Bureau will release retail sales on Thursday. The market expects a 0.5% increase. Following last week’s jump in jobless claims, we will closely monitor Thursday’s claims report.

The Treasury will continue to issue large amounts of debt. Highlighting the week will be the $32 billion 10-year note auction on Monday and the $18 billion 30-year bond auction on Tuesday.

Did Baron’s Just Jinx the Bull Market

The latest cover of Baron’s magazine tells us not to fear the bull market and offers its readers reasons to be bullish. Despite no statistical evidence, bears often argue that covers like the Baron’s one shown below are warnings that a market top is near. Only history, not bullish or bearish pundits, will tell if Baron’s is correct or if they jinxed the market.

Hedge Funds are Bearish the Economy

The graph below from Morgan Stanley shows hedge funds hold less cyclical stocks (excluding energy stocks) as a percentage of their collective portfolios since at least 2010. Cyclical stock prices tend to correlate well with the health of the economy. Cyclical stocks are companies with products in demand when the economy is strong but often see weaker sales when consumers and corporations spend less. Based on their positioning, hedge funds must be worried about a recession or slower economic growth in the future.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.