What can breakeven inflation rates tell us about oil prices, energy stocks, and market direction? It turns out it’s a lot more than you think.

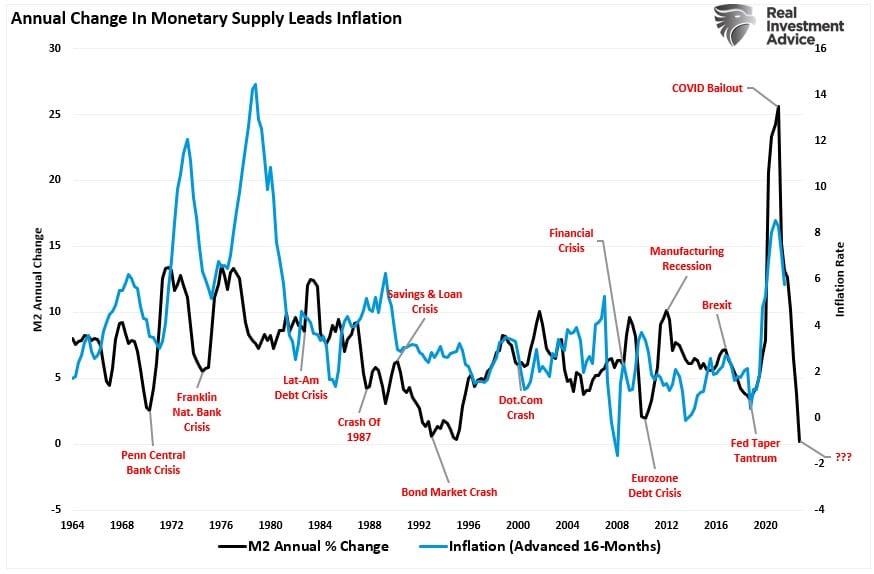

Since 2021, as the impact of an economic shutdown collided with $5 Trillion in artificial, stimulus-driven demand, inflation has consumed everything from headlines to financial markets and the Fed’s monetary policy. With employment back to pre-pandemic levels, the monetary impulse has reversed, the supply-demand imbalance has normalized, and inflation is falling. Changes to the money supply precede changes in inflation by about 16 months.

As discussed previously, the impact of higher interest rates on a debt-laden economy leads to the destruction of economic demand. That economic and inflationary decline is witnessed in numerous indicators. The Leading Economic Index (LEI) and our Economic Composite Index are good examples.

However, in many cases, the data comprising these economic indicators are lagging and subject to substantial changes. Therefore, the bond market provides a more real-time view of expectations for inflation and economic growth.

As such, we will focus on “breakeven inflation rates.”

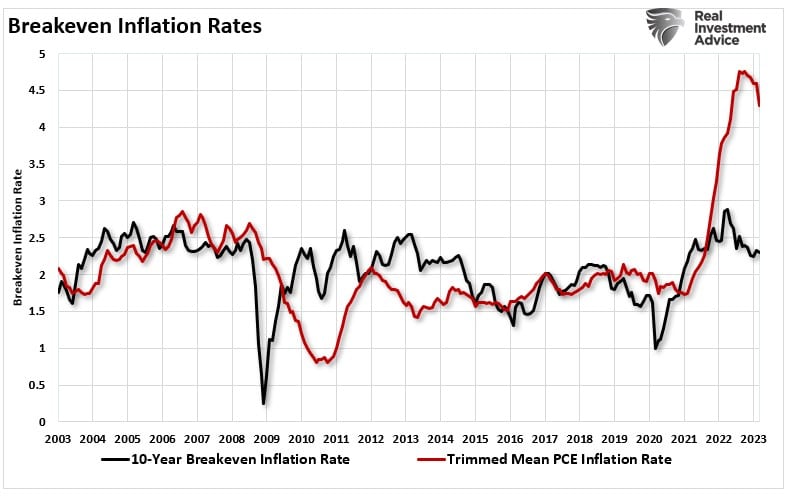

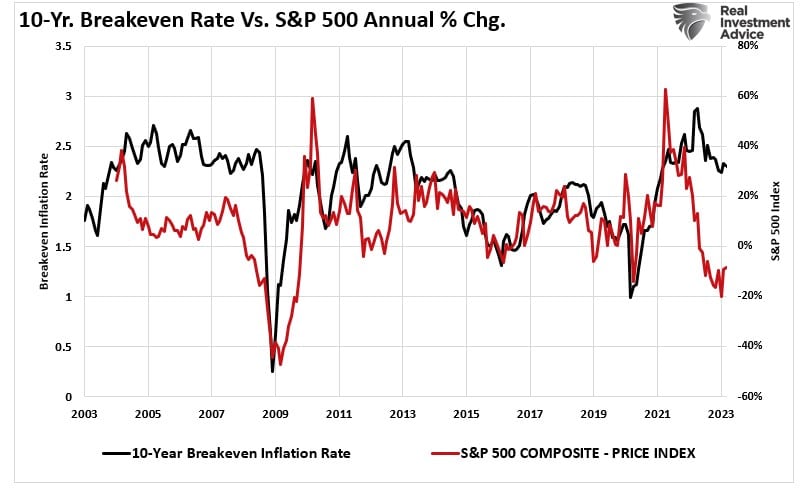

That rate is the difference between the nominal and real yield on fixed-rate investments with similar maturity and credit quality. The 10-year breakeven rate peaked well before the Fed’s preferred measure of inflation, the trimmed-mean Personal Consumption Expenditure (PCE) rate.

You will notice the significant gap between inflation and the 10-year breakeven rate. The bond market is betting on a substantial decline in inflation over the next 12 months. That differential in what the market expects and lagging economic data is not “bullish” for the economy.

The Economy & Profits

An old saying says the “best cure for high prices is high prices.”

Simply, higher prices will reduce demand, leading to a decline in prices. Of course, high prices, with higher borrowing costs due to the Fed’s actions, slow demand even more.

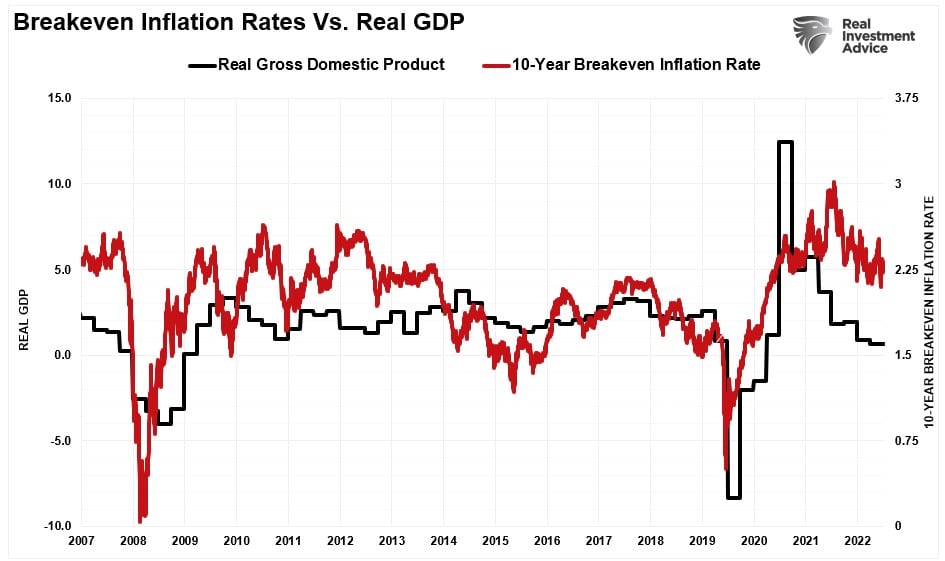

If the bond market is pricing in weaker inflation, weaker economic growth will follow. Such is due to the inherent “demand destruction” of consumption. You can understand the correlation in an economy comprised of nearly 70% personal consumption expenditures. As such, if inflation is declining, that is representative of weaker, not stronger, economic activity.

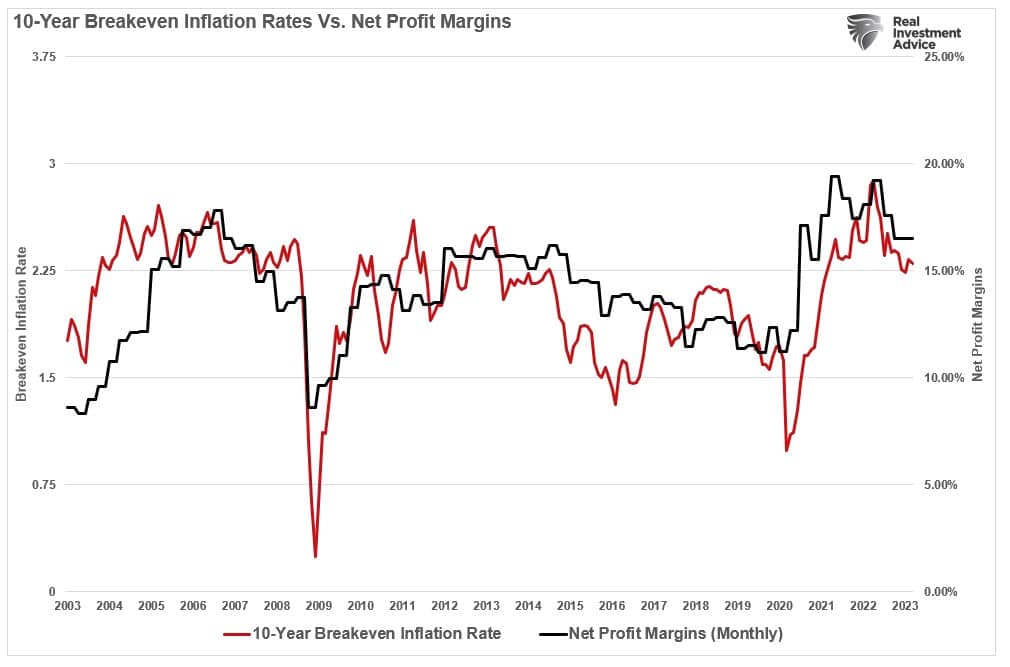

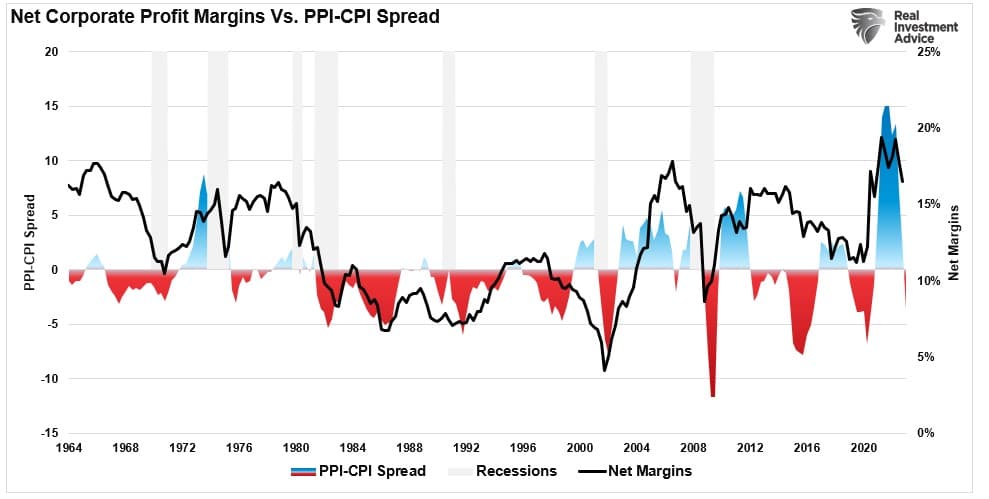

Naturally, as economic demand and inflation decline, so do the prices companies charge consumers. Unsurprisingly, there is a high correlation between breakeven inflation rates and corporate profit margins.

Furthermore, given that earnings are also the result of economic activity, as inflation falls due to slowing economic demand, so do earnings.

Given that the surge in earnings and corporate profits resulted from massive fiscal interventions, investors should be asking what the next growth driver will be. If the sharp decline in M2, and falling breakeven rates, tell us anything, it is likely that without further monetary accommodations, earnings growth, and ultimately profitability, may be challenging.

Oil Prices And Energy Stocks

Another economically sensitive area to examine are oil prices. As with the economy, oil prices are ultimately a function of supply and demand. When demand outpaces current supplies, prices rise, and vice versa. While there are near-term anomalies that can move prices in the short term, such as an oil production cut, in the long term, it is basic economics.

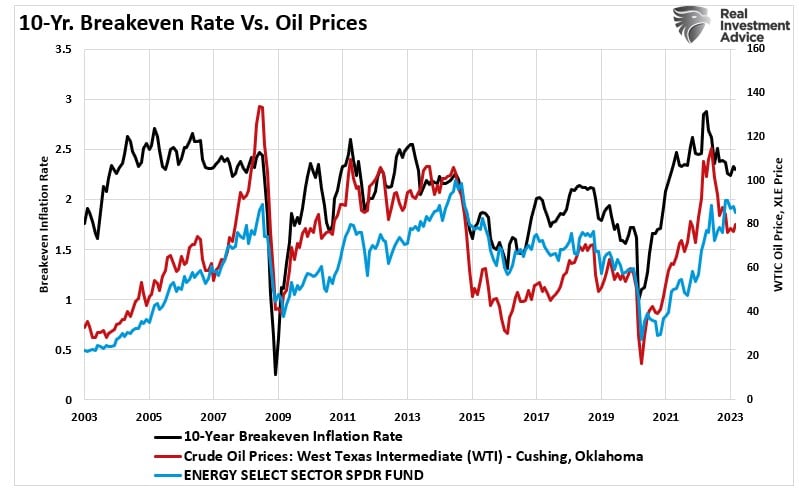

Not surprisingly, the rise and fall of oil prices are highly correlated to breakeven inflation rates. Again, such makes sense, given the economic sensitivity of oil to the economy. Energy companies, dependent on oil prices for their revenue, are also highly correlated to the economy, oil prices, and breakeven inflation rates.

As the Fed continues to hike interest rates to combat high inflation levels, the risk of further decline in breakeven rates is elevated. Such is particularly true if the Fed’s monetary actions result in an economic recession.

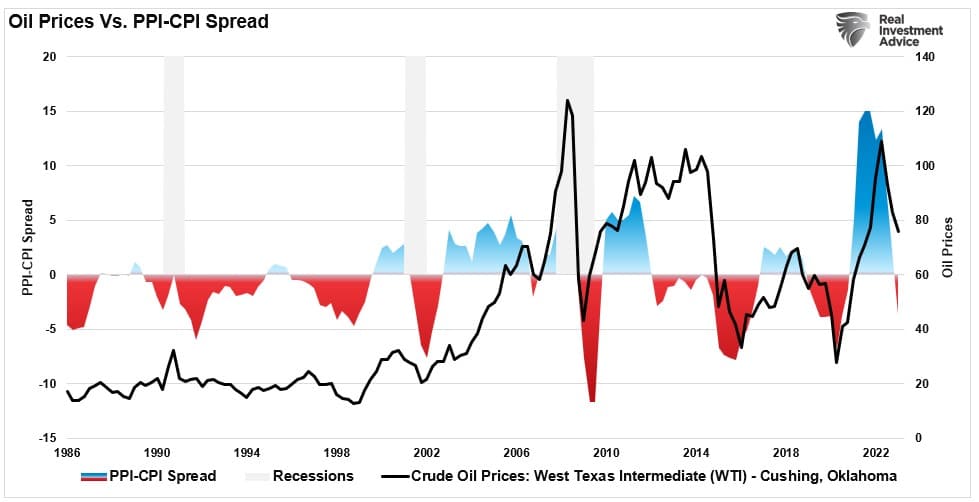

Another confirmation of the impact of disinflation on economic activity and, ultimately, corporate profits and commodity prices is the spread between the inflation rate of consumers versus the producers. As the economic activity slows and inflation falls, so do the costs the producers can pass along to consumers through higher prices. When producers cannot pass higher costs to consumers, the company must absorb them, reflected by profit margin contractions.

The exact correlation exists, unsurprisingly, with oil prices. As demand slows, the input costs of higher energy prices decline as “demand destruction” in the economy increases.

While the Fed intends to push higher rates to ensure an inflationary decline, the economic consequences are not optimistic.

The Market May Not Like Getting Its Wish

Since the beginning of the year, the market has risen in hopes that a “Fed pivot” and a return to monetary accommodation would be bullish for investing outcomes. However, the breakeven inflation rates and the spread between producer and consumer inflation have significant consequences.

Falling inflation is not a function of a growing economy, so the Fed has reiterated its call for a “mild recession.”

“The staff’s projection at the time of the March meeting included a mild recession starting later this year, with a recovery over the subsequent two years.” – March FOMC Minutes

It is crucial to understand that the Federal Reserve has never previously verbalized the word “recession” in its speeches. Even before the 2008 financial and the 2000 “dot.com” crisis, the Fed regularly discussed a “soft landing” or “Goldilocks” economy. If the Federal Reserve says, “Get prepared, a recession is coming,” its words would cause actions within the economy that would advance, and potentially worsen, that outcome.

Therefore, the Fed must always be cautious in making statements to the financial markets, as its words cause actions. My concern is that if the Fed’s previous discussions of “soft landings” and “Goldilocks” scenarios resulted in fairly deep recessions, what does a “mild recession” portend?

More importantly, until a recession of any magnitude or further banking stress materializes, we do not expect the Fed to start cutting rates. However, when the Fed does begin to cut rates, it will be due to the recognition that a “recession” is underway. The yield curve will steepen dramatically, lowering yields as inflation eases with slowing economic activity.

None of that is “bullish” for corporate earnings, profits, or market prices.

Which is probably what “breakeven rates” are telling us.

Investors just aren’t listening.

Yet.