A Dose of Reality About the Labor Market

The language used to describe recent employment data is confusing. The Bureau of Labor Services (BLS) reported that the U.S. regained 9.3 million jobs since May. In reporting on those results, the business media characterizes the jobs market as “better than expected.” Given that no one expected 22 million jobs to be lost, why should we use expectations as a meaningful gauge?

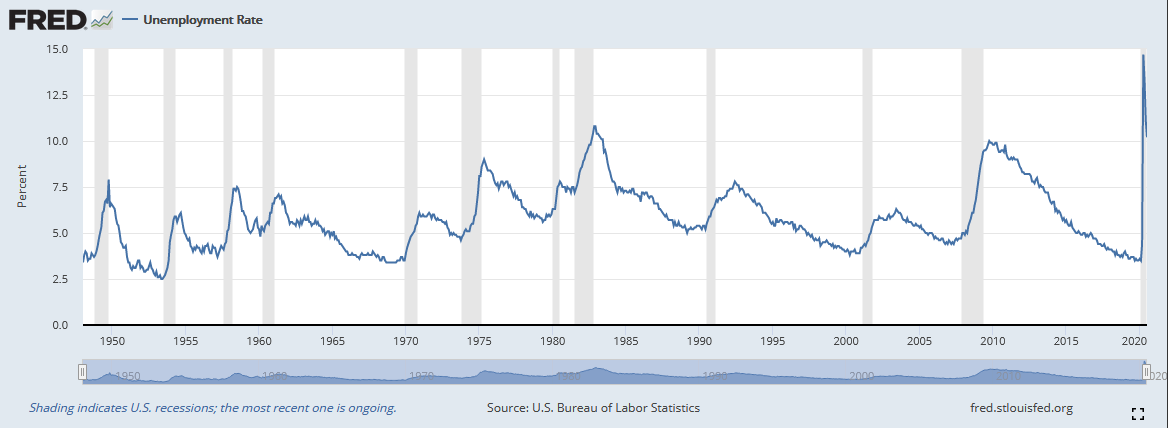

Although it is encouraging to see improvement in employment amid the COVID-19 pandemic, investors would be wise to avoid rose-colored lenses just yet. Despite the job gains, the U.S. still has about 12 million fewer people employed today as compared with February before the pandemic shutdowns hit the economy. Additionally, though down from over 15%, the unemployment rate remains extremely high.

Correctly Assessing Labor Markets

Having written in the past about the importance of linguistic precision, reports on the labor market should be rephrased. Technically, recent data is better than economists’ expectations, but the situation is better characterized as “ugly but improving.”

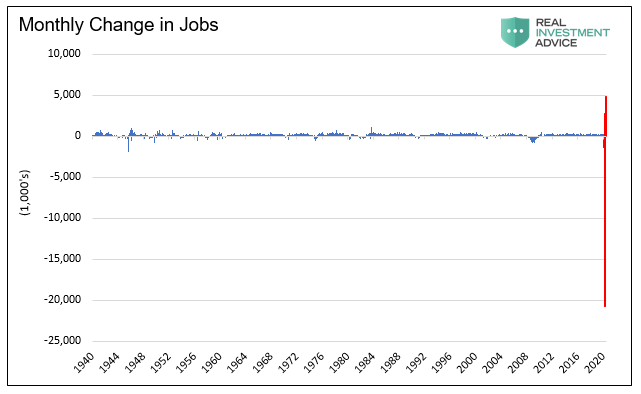

Job gains of the past three months are filling a vast unemployment crater formed by the COVID virus meteor. As the chart below highlights, U.S. job gains of the past three months have only just gotten back to the worst levels of the past 70 years. Bear in mind, various adjustments make today’s data look better than it is.

For example, according to BLS, the formation of over 881,000 new jobs occurred over the last three months due to net new business formations. The likelihood of that being true seems quite remote given the circumstances we are facing.

Narrative-Driven Journalism

As is evident from the labor market facts and the media’s characterizations, the reasoning seems to be going backward from some desired conclusion to the preferred “V-shaped” recovery story. A term we recently heard that fits is “narrative-driven journalism” which is just a euphemism for propaganda. It is the opposite of investigative journalism. This is a symptomatic issue and one that resurfaces time and again in the evaluation of the economy’s “recovery” from the virus shutdowns.

If we look at job losses as opposed to the unemployment rate, one gets another perspective on the enormity of the situation, as illustrated below. Never before have we seen anything resembling the labor market devastation seen in April.

One standard deviation of the monthly change in jobs between 1939 and 2019 is 223,000. As a percentage of the workforce, the 1.3 million jobs lost in March was a 2.7 standard deviation event. The negative 21 million job report in April counts as a 35.7 standard deviation event. That number is even more incomprehensible than the image on the chart above. Devastating job losses during the 2008 financial crisis are barely perceptible.

Employment in July rose by an impressive 1.8 million and, as mentioned, the economy has recovered over 9 million jobs since April. While encouraging, of those that lost their job in March and April, a majority remain out of work. Not only that, but a large percentage of those can also expect to once again be out of a job. Another 2.8 million people have left the workforce altogether. The BLS does not count them as members of the workforce.

Looking Ahead

Results from a recent study conducted by Cornell’s Daniel Alpert, the U.S. Job Quality Index (JQI), and RIWI, indicate maintaining improvement in the labor market is unlikely. Furthermore, their work suggests that a sizeable percentage of job gains are temporary.

The results of their survey illustrate the problems and complexities associated with interpreting the job gains since May. Developed to test the vulnerability of U.S. employees to business failures once government support diminishes, their data reveals that concern is well-founded. Although not yet showing up in economic data, another round of layoffs is indeed occurring. The study suggests that the problems in the labor market are “much more significant and systemic” and not isolated to those states that experienced another COVID-19 surge.

The Trend Is Not Labor’s Friend

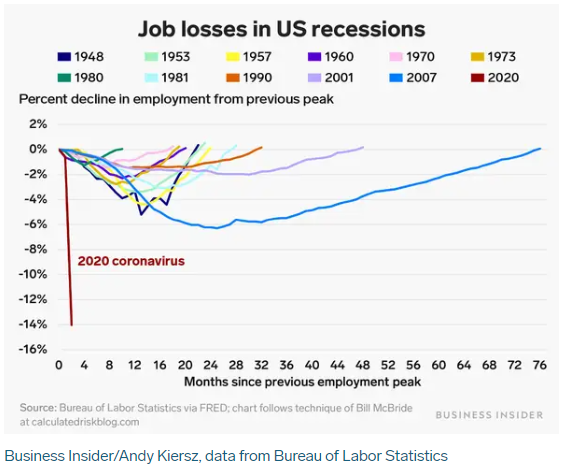

Looking back at prior recoveries, as shown in the chart below, employment rebounds are progressively more anemic. With that trend as evidence, the outlook for displaced workers, and therefore the economy, is troubling.

For the moment, the various forms of record stimulus are trying to prop up a very sick economy. Massive stimulus obscures a reasonable assessment of economic fundamentals. Being a prudent steward of wealth demands that we attempt to draw sensible conclusions about the current environment and, more importantly, the economic outlook. That task, as discussed in Why the Recovery Will Fall Short of Forecasts, has never been more challenging.

Political Considerations

Meanwhile, the cities hardest hit by the virus are in peril. For the nation’s largest cities like Chicago, Los Angeles, and New York, most of the things that make those cities exciting and dynamic remain shut down. As discussed by @boriquagato in a recent thread on Twitter, restaurants, clubs, live music, sporting events, and theater will have difficulty rebounding from a 5 or 6-month pause. They do not hold enough capital to survive such a pause.

Permanent changes to behavioral patterns will alter much even after cities fully reopen. The respective mayors and governors mostly failed to understand the trade-off between shutdowns and economic destruction until now. The irony is that re-opening at this point will reveal the extent of the economic damage. For the politicians of those states hardest hit, that is a significant problem.

As former President of the European Commission Jean-Claude Juncker once said, “We all know what needs to be done, we just don’t know how to get re-elected after doing it.”

Summary

Personal consumption represents 70% of GDP. Therefore, no single piece of economic data is more important than the employment picture. It is not a matter of unjustified pessimism to urge a proper characterization of economic fundamentals, it is prudence. Although temporarily encouraging, assuming the post-pandemic recovery will be robust or “V-shaped” is disingenuous. Not only that, it encourages behavior and decision-making that is detrimental to the prospect of recovery. Given the profoundly uncertain outlook, we should prepare for the worst and hope for the best.

Put another way, failing to prepare is preparing to fail.