Despite the weekend’s positive news on China trade negotiations and the associated jump in most stock prices, the healthcare sector was hit hard. The culprit is an executive order aimed at reducing U.S. prescription drug prices. Donald Trump plans to implement a “Most Favored Nation” (MFN) policy. The policy would tie Medicare drug prices to the lowest prices paid by other countries. Consequently, drug prices in the US could fall an estimated 30% to 80%. Or, they could rise substantially abroad.

While daunting for the healthcare industry at first glance, the executive order faces significant challenges. The industry has long argued that such a policy stifles innovation and reduces R&D. Moreover, the courts could present a significant roadblock. Courts blocked a similar proposal by Trump in 2020. Also worth noting is that the order’s specifics, such as which drugs and insurance programs it will cover, remain unclear. Additionally, its implementation may require congressional action.

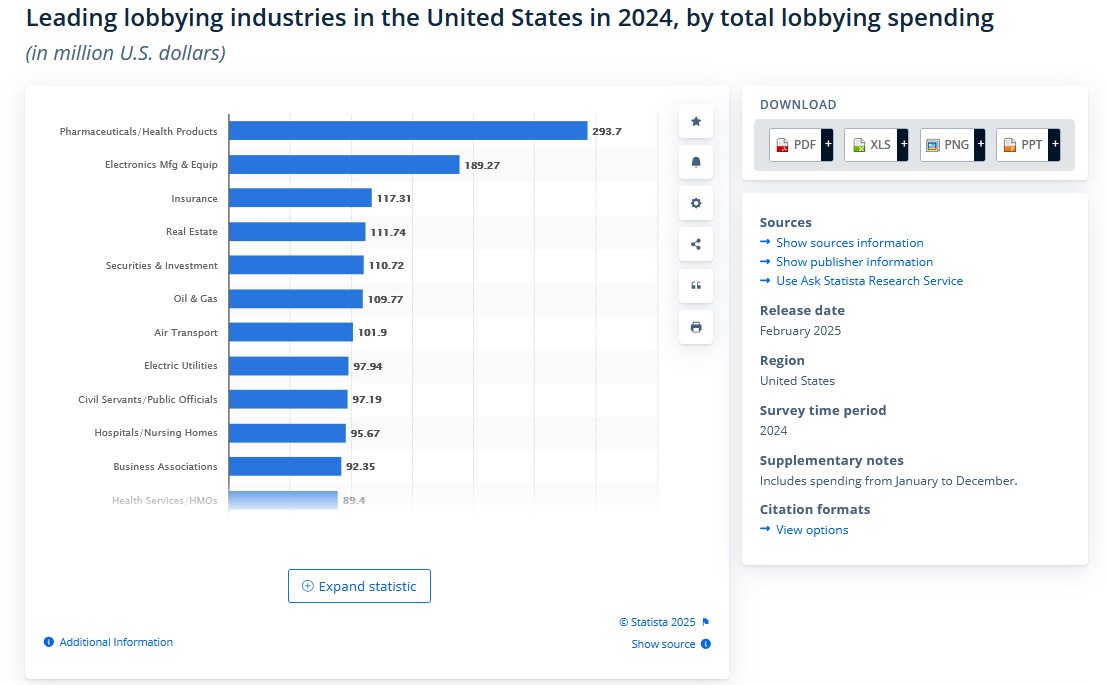

The pharmaceutical lobby is strong. As we share below, courtesy of Statista, pharmaceutical and health product companies spend significantly more on lobbying than other industries. They will put undue pressure on Congress and likely minimize the executive order’s impact.

What To Watch Today

Earnings

- No notable earnings releases today

Economy

Market Trading Update

Yesterday, the market rallied sharply following news that a trade negotiation had been struck with China, reducing tariffs to just 30% over the next 90 days. Technically, we continue to track the initial decline and rally in 2022. As I stated previously, I don’t like analogs as “this time is always different,” however, it is worth noting that bear market rallies look like the end of corrections and a return of a bull market, until it isn’t.

From a technical perspective, the market also continues to trace the reversal of extremely oversold conditions to more optimistic ones.

As noted in Monday’s Trading Update, this could still be a “bear market rally,” as we saw in 2022. Such is entirely possible. But with the markets breaking above both resistance levels at the 100 and 200 DMA, there is a rising probability that the correction process is over. With the MACD pushing more elevated levels and the RSI index approaching overbought, we are at levels where we should expect a “pause” in the rally before making the next push higher. If the market can consolidate a bit, without breaking back below those previous resistance levels, we will remove hedges and reduce our cash holdings.

However, this week we will have the next batch of economic data, including CPI, which will likely determine the market’s next move. We remain somewhat cautious with our allocations, but the market reversal is healthy. We are watching our weekly indicators closely, and if they turn back to the positive, we will look to overweight equities and reduce cash holdings completely. However, that will likely be several weeks before seeing those signals turn.

Trade accordingly.

Industrials And Healthcare Move In Opposite Directions

As shown below, courtesy of SimpleVisor, the impact of potential tariffs plays a significant role in stock sector selection. With news of tariff agreements, the industrial and technology sectors, both among the most negatively impacted by tariffs, are now the most overbought on a relative basis. Healthcare, which has traded poorly on rumors of executive actions calling for lower drug prices, weighs on healthcare stocks. The sector will be pushed further into oversold status over the coming days as Trump’s prescription pricing plan was announced on Sunday.

The graph to the right of the sector scores shows that both healthcare and industrials were orbiting around in the upper left box, denoting decent relative scores versus the market but oversold on an absolute basis. Over the last two weeks, industrials moved to the upper right and healthcare to the lower left. The second graphic shows that aerospace companies are leading the industrials sector.

A Bear Market Rally, Or Just A Correction?

Assessing a bear market rally proves challenging when you experience it firsthand. It is only in hindsight that the complete picture reveals itself to investors. Of course, after a bear market rally, investors tend to review their investments and speculate on what they should have done differently.

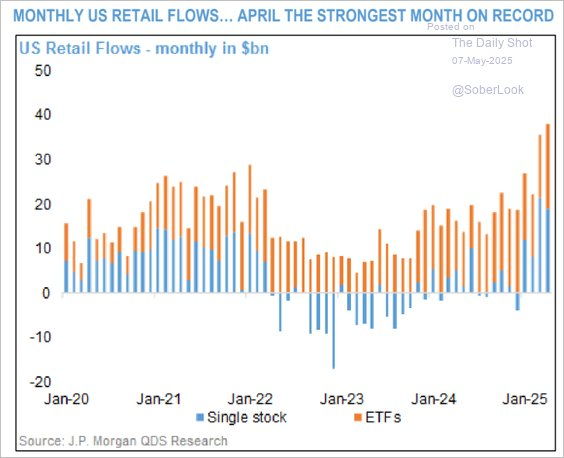

Retail investors seem to view the recent sharp correction as possibly finished. As I noted last week on X, despite the near 20% correction in the markets, retail investors piled into US equities at a record pace. Of course, historically, retail investors were considered a contrarian indicator, but in recent years, particularly post-pandemic, they have been aggressive buyers of any dip in the market. Of course, after 15 years of monetary and fiscal interventions to stave off deeper bear markets, their “buy the dip” mentality is unsurprising.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.