There are many media-driven narratives about the impact of tariffs on the economy and the markets. Most of them are incredibly bearish, predicting the absolute worst possible outcomes. For fun, I asked ChatGPT what the expected impact of Trump’s tariffs will likely be. Here is the answer:

“One of the immediate consequences of increased tariffs is higher consumer prices. Tariffs function as an import tax, and companies that rely on foreign goods often pass these costs onto consumers. This could lead to higher inflation, particularly in electronics, automobiles, and household goods, where China plays a dominant role in supply chains.

Over the longer term, Trump’s tariffs could contribute to stagflation—lower economic growth combined with persistent inflation—if businesses struggle to adjust. While the intended goal is to bring jobs and manufacturing back to the U.S., the broader economic risks suggest that tariffs could ultimately slow growth and raise costs for American consumers and businesses.”

To see if ChatGPT is correct in its assessment, we need a proper definition of “stagflation.”

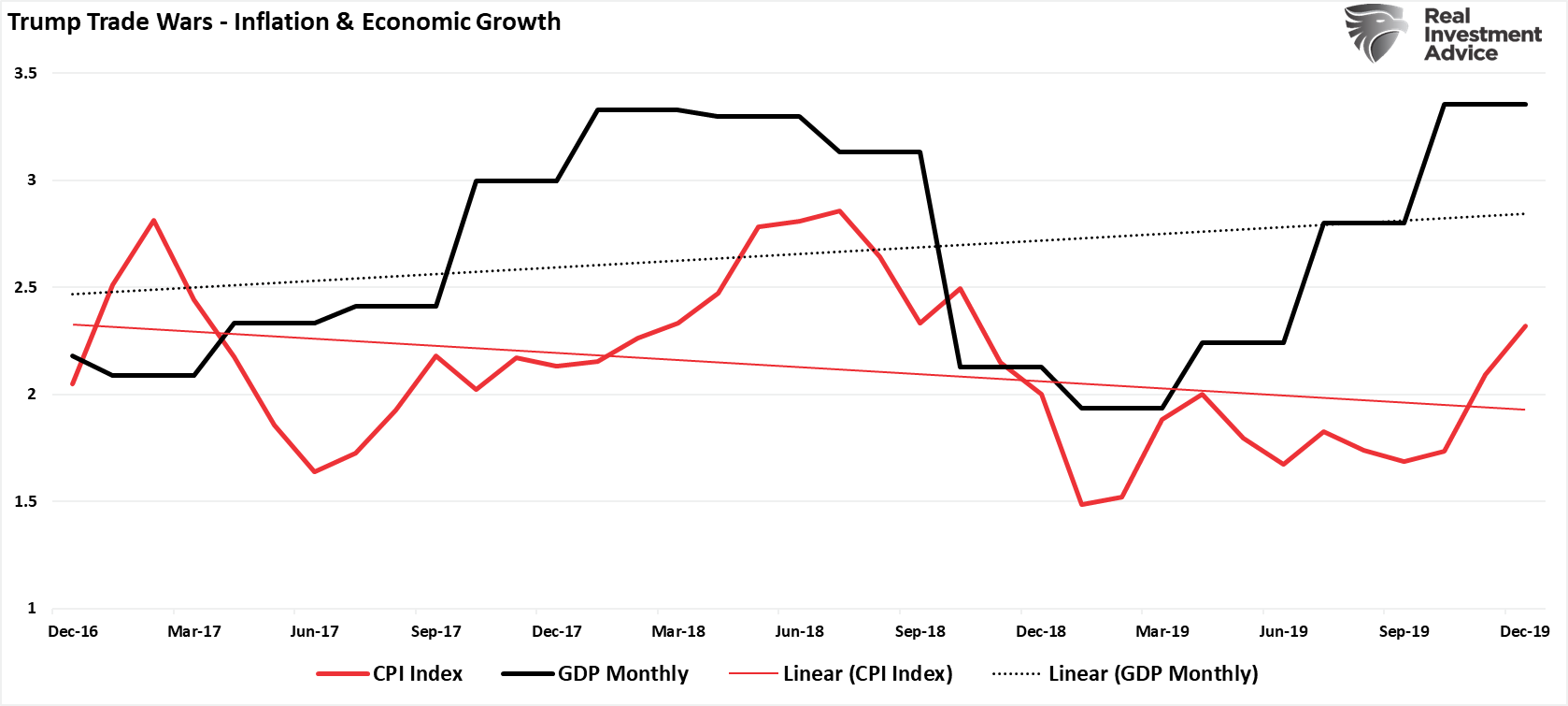

Notably, most analyses of “stagflation,” from which ChatGPT drew its answer, exclude the third component of the definition – unemployment. While individuals trying to sell gold or use “stagflation” headlines to get clicks, they conveniently leave out the most crucial ingredient of the definition. As shown, during Trump’s first administration, the impact of tariffs on inflation was not what the media suggested would happen. Inflation averaged close to the Fed’s 2% target during that previous term. However, as should be expected, inflation did rise in response to more robust economic growth rates and vice versa.

However, contrary to the “stagflation-istas,” the impact of tariffs did not lead to surging unemployment. During that period, the unemployment rate fell to one of the lowest levels on record. At the same time, the economy continued to expand.

Despite recent market concerns over the impact of tariffs, our previous experience suggests that “stagflation” is not likely to be the case. The reason, as explained previously in “Trumpflation,” is that:

“…a closer examination reveals that inflation may not rise as dramatically as feared. The normalization of supply chains, stabilizing energy prices, evolving consumer spending habits, and the backdrop of slowing global economic growth all point toward continued downward pressure on inflation. Moreover, historical evidence shows that high debt and deficits are more likely to contribute to deflation than inflation.”

But what about the impact of tariffs on the stock market?

Tariffs And The Stock Market Reaction

While ChatGPT answered with the latest narrative and failed to review the economic outcomes during Trump’s previous “trade war,” what about the impact of tariffs on the stock market and volatility? Here is ChatGPT’s outlook

“Initially, the stock market is likely to react negatively to new tariffs, particularly in sectors heavily reliant on international trade. Higher import costs and the threat of retaliatory tariffs could weigh on investor sentiment, increasing uncertainty. The last major tariff escalation under Trump in 2018 resulted in sharp market corrections, as investors priced in the risk of slower global growth and corporate margin compression. If history repeats, a similar market reaction could occur, with cyclical sectors like industrials, technology, and consumer goods facing the most pressure.

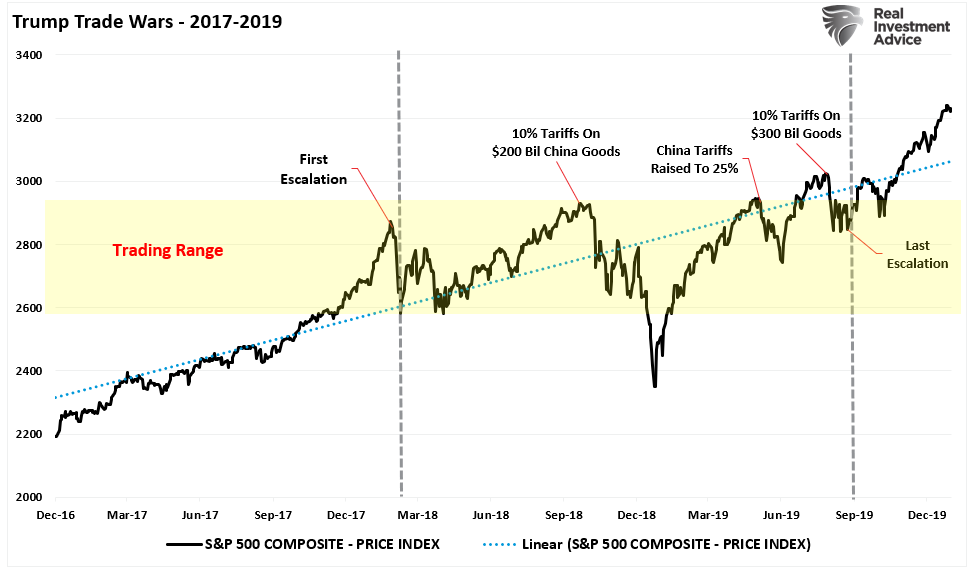

Last week, we discussed the “Tariff Turmoil” that rocked the markets. Many headlines suggest that Trump’s tariffs will cause the next major market crash. Maybe that is the case. There is always a possibility of “something breaking.” However, as ChatGPT suggests, a look at Trump’s first term in office shows how the markets reacted as the China “trade war” developed.

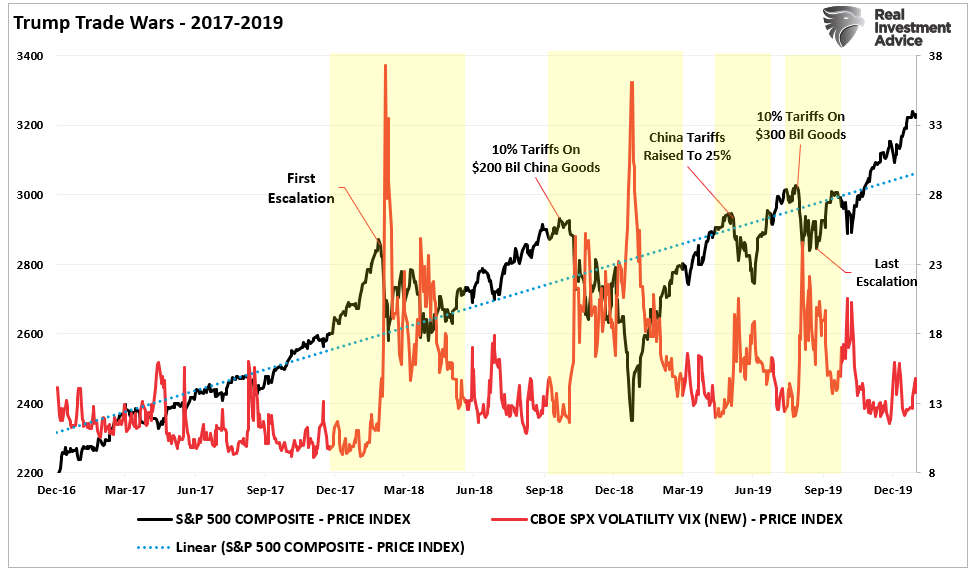

Following the passage of the “Tax Cuts and Jobs Act,” the market surged to all-time highs. Valuations were elevated, and the Fed was beginning a rate-hiking campaign. At the same time, Trump launched the first escalation of the trade war with China. Over the next 18 months, the market traded in a very wide trading range but remained in a steady linear growth trend that was higher.

As noted in “Curb Your Enthusiasm,” this year may be very similar to what we saw during the first trade war with bouts of volatility. As shown, as different facets of the trade war developed, the impact of tariffs caused short-term volatility spikes as investors digested the actions and their potential ramifications on the market. However, those spikes in volatility were short-lived as the impact of tariffs was quickly absorbed.

Despite the barrage of negative headlines, concerns about inflationary impacts, and economic outcomes, the market ultimately weathered the trade war. As is often the case with more dire predictions, the worse potential outcomes failed to appear. There is no denying that the “trade war” did induce a significant amount of volatility, which made it difficult for investors to “stay the course.” However, in hindsight, we can now see that those spikes in volatility provided repeated buying opportunities for investors to pick up stocks at lower prices.

Will this time be the same? Maybe. However, one facet that could be very important to consider is corporate earnings.

Impact Of Tariffs On Corporate Earnings

The risk of “stagflation” is likely way overblown, given the ongoing strength of employment reports and low unemployment rates. Furthermore, while the impact of tariffs will likely increase volatility, the market will likely withstand that impact. However, the risk that is different this time is the combined risk of overvaluation and high corporate earnings growth expectations.

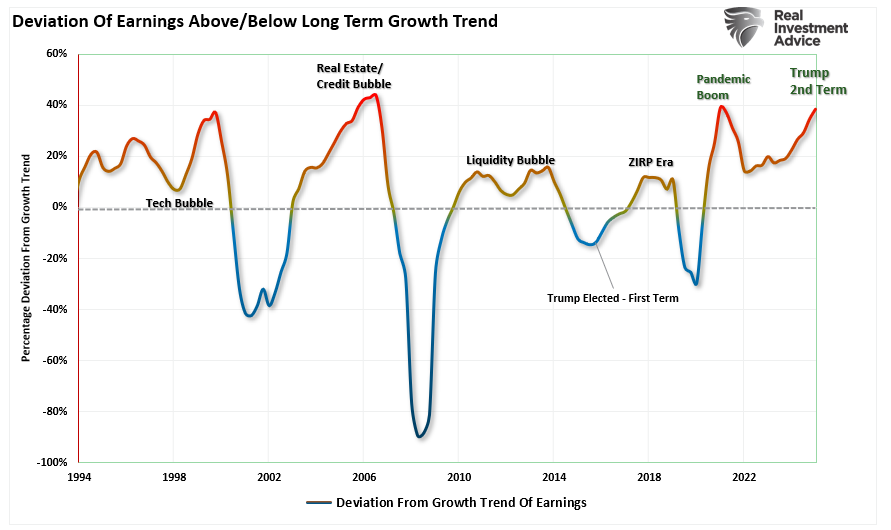

Currently, expectations for earnings growth in 2024 are highly optimistic and have deviated from the long-term growth trend of earnings. (Read “Are Return Expectations Too High” for a more thorough discussion on the relationship between earnings and economic growth.)

When Trump took office during his first term, earnings expectations were below the long-term exponential growth trend. That is not the case today, leaving the market vulnerable to more significant disappointment.

The same is true for both trailing and forward earnings valuations. On the most optimistic basis, using forward operating earnings, Trump entered his first term with the valuation at just 18x forward earnings. Today, the most optimistic form of valuation measures stands at 24.5x, one of the highest levels since 1985.

This background is crucial to our discussion of market risk from the impact of tariffs in the future.

The most immediate impact of tariffs will be on corporate earnings, as companies that rely on imports will face rising costs. Do not take that statement lightly. Currently, 41% of corporate revenue is derived from exporting goods and services. However, as noted above, the ability to pass those tariffs onto consumers is likely limited. As noted above, consumer inflation was not present to a great degree during our first experience with tariffs. However, there is a risk that tariffs could weaken consumer demand in a high-interest-rate and inflation-sensitive environment, which is undoubtedly different than Trump’s first term. Therefore, if companies cannot fully offset tariff-related costs, this could result in downward earnings revisions.

During Trump’s first term, the 3-month rate of change in earnings suggests there is a risk that companies fail to pass on tariffs to consumers. Again, this is why inflation fell, undermining the more bearish outlooks.

With valuations and earnings expectations very elevated, the impact of tariffs could lead to more significant disappointment in outlooks. As we saw previously, while tariffs did not lead to inflation or “stagflation,” they did induce more serious bouts of volatility and reduced market returns.

The risk of the same this time certainly seems plausible.

Conclusion

We don’t have much history regarding tariffs and the stock market. However, avoiding media-driven narratives and focusing on managing your portfolio is likely best. As we warned previously, media headlines are often wrong.

“That does not mean that things won’t change in the future. However, using media headlines to make portfolio decisions has repeatedly turned out poorly. If the recent market volatility is weighing on you, and you “feel” you must “do something,” take very small steps.”

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against significant market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

“As we saw on Monday, taking small steps to reduce portfolio risk now can help you weather sharp market events. Remembering that portfolio management is not an “all or none” process is crucial. It is about positioning yourself to minimize emotional decisions so you can find the “opportunity that exists in crisis.”

For now, the risk of “stagflation” is likely close to zero, and the risk of a major surge in inflation is likely similar.

However, the risk of a more volatile market as earnings expectations and valuations are repriced for reality is likely a high probability event this year.

Trade accordingly.