The FDIC graph shows that banks are sitting on over $500 billion of losses on their investment securities. This doesn’t include bank loans and other assets with significant unrealized losses. The graph may look scary, but thanks to a rule passed during the financial crisis, it may not be. In 2008, banks were taking tremendous losses as their loan and security prices plummeted. Banks were failing in large numbers. To halt the crisis, FASB changed accounting rules to shelter banks from taking losses unless they sell the assets. Before the new rule, banks had to report the fair value, aka mark to market, of all assets. Now, they can elect to classify assets such that they mark them at par instead of current prices. With some long-term bank assets trading at 50-60 cents on the dollar, the 2008 rule is saving many banks from reporting large losses and potentially bankruptcy.

We can debate the rule change, but what’s important to grasp is the bank losses shown below, while not realized are real and there are situations in which the losses might be realized in the futre. Since the Fed started raising rates, bank depositors began withdrawing money from banks and moving it to higher-yielding options. Deposits are a bank’s primary source of funding for its assets. When a deposit leaves the bank, the bank can either replace the funding or sell assets. Selling an asset turns an unrealized loss into a realized loss. Such actions played a primary role in bankrupting Silicon Valley Bank, Silvergate, and others. The graph below represents the possibility for the future realization of losses and possibly more bankruptcies. Therefore, as we consider Fed policy going forward, a big challenge the Fed faces with its “higher for longer” campaign is the possibility banks must realize losses.

What To Watch Today

Economics

- No notable economic releases

Earnings

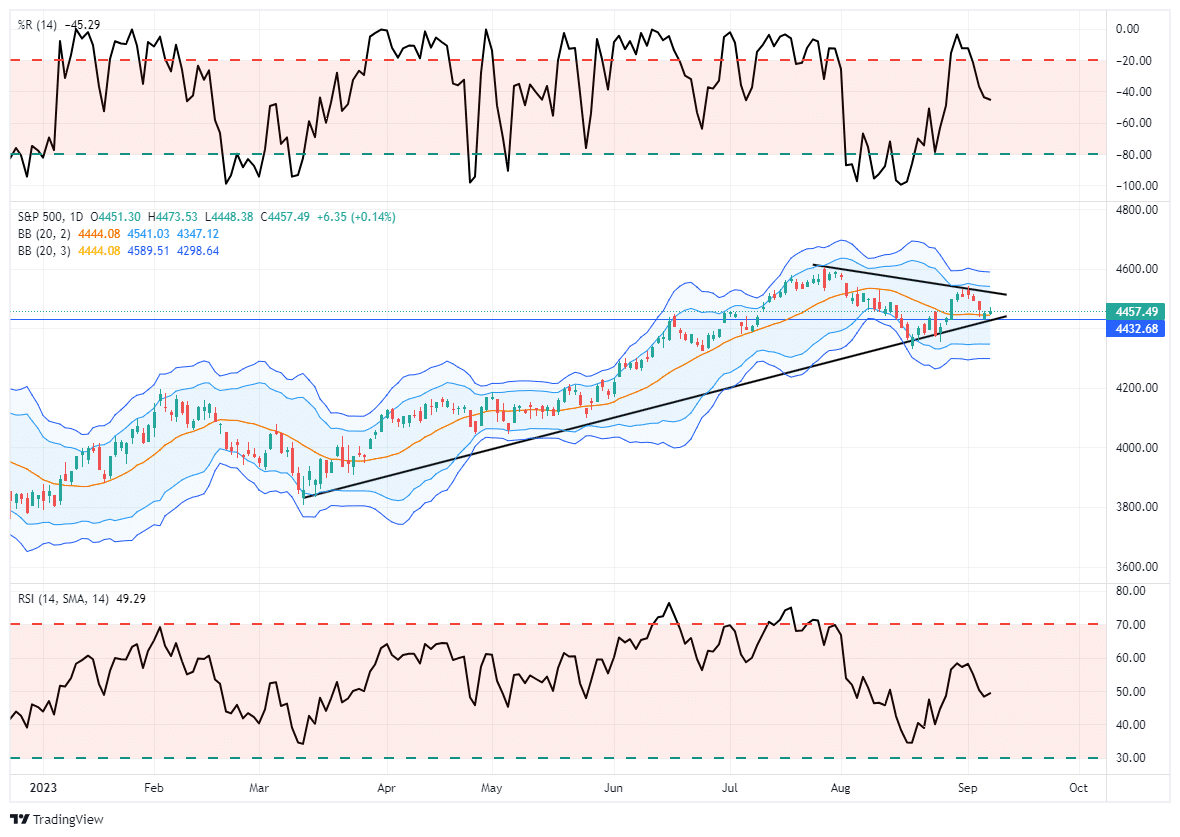

Market Trading Update

The market sold off decently over the last week, retesting the rising trend line and holding the 50-DMA. The more extreme overbought condition is about halfway through a corrective cycle, suggesting we could see some further “sloppy” trading next week. With the market holding within a consolidation range, a breakout to the upside should confirm the start of the seasonal strong trading period into year-end.

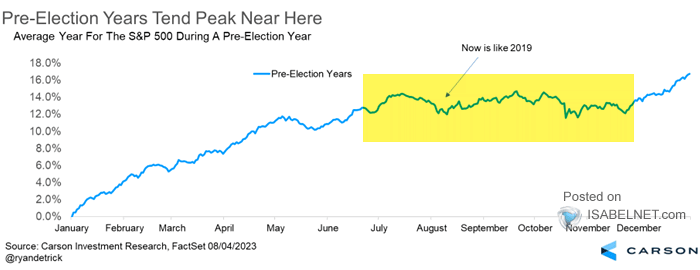

As shown, the July through October periods tend to trade sideways in pre-election years with a stronger year-end push as portfolio managers window-dress portfolios into year-end. This year, the market has tracked fairly closely to the historical norms and should continue into year-end, given no major financial or economic upheaval.

We continue to suggest remaining allocated to the equity market for now. However, we also suggest using short-term rallies to rebalance equity risks and overall allocations accordingly. While there is no evidence of a more severe market correction on the near-term horizon, such does not mean that it can’t happen. As we get into 2024, the odds of a more meaningful contraction rise as the risk of economic grows. Continue to manage risk accordingly.

The Week Ahead

After a sleepy economic data week, this will week be more lively and help us better assess what the Fed may do at next week’s FOMC meeting. CPI is expected to increase by 0.4%, 0.2% more than last month. However, the core rate is only expected to rise by 0.2%. monthly and fall from 4.7% to 4.5% annually. PPI and Retail Sales follow on Thursday.

The Fed will enter their pre-meeting media blackout period this week. Consequently, we have likely already heard the last thinking of the Fed members. The table below shows that Fed Funds market assigns a 94% chance they keep rates the same on September 20 and a 40.6% chance they hike rates by .25% at the November 1 meeting.

The Treasury will auction 10 year notes on Tuesday and 30 year bonds on Wednesday. The combination of important inflation data and the auctions will likely create a good amount of volatility in the bond markets.

The Fed Is Buying Bonds, Not Selling Them

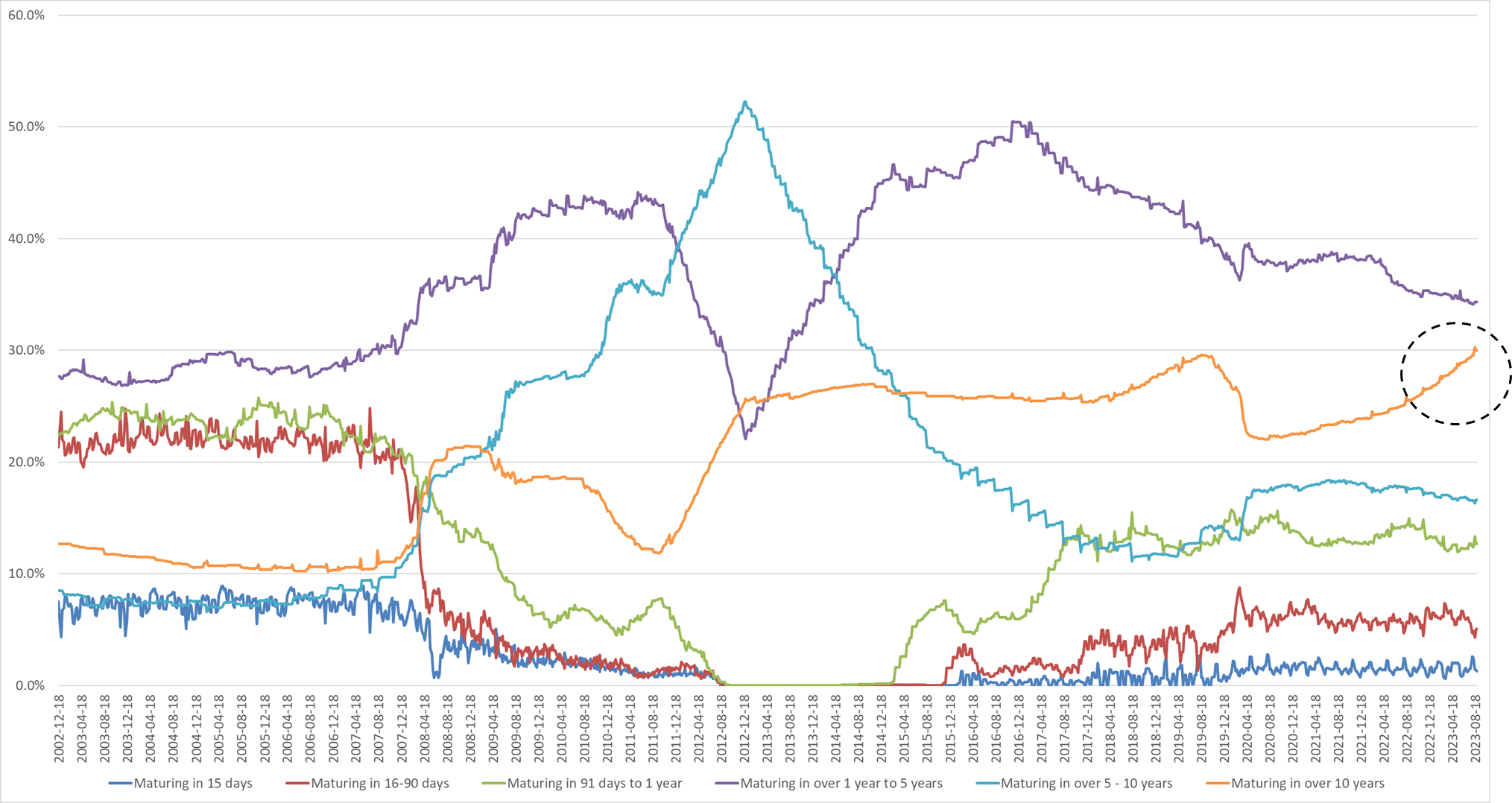

The first graph below from Jim Bianco shows the Fed has reduced its balance sheet by about $1 trillion since QT started in April 2022. However, the graph, because it’s a stacked area graph, does a poor job of showing which maturity ranges and security types have been most affected. A client of ours did some great work producing the second chart to better clarify how QT effects the Fed’s holdings by maturity ranges. The orange line represents securities ten years and longer. As the graph shows, these longer assets have been steadily rising since the Fed enacted QE in 2019. As he highlights, they continue to increase despite the Fed’s policy reversal to QT in 2022. QT aims to remove $95 billion of assets a month from its balance sheet.

We bring this up because we have heard incorrect statements claiming that QT adds to the supply of long term bonds in the market. The fact is the Fed conducts QT by allowing bonds to mature. By default, the maturing bonds are all very short-term. Importantly, when the monthly amount of maturing bonds exceeds the Fed’s $95 billion target, they need to buy bonds. Again, despite QT, the Fed has been buying long-term bonds as there have been more bonds maturing than their stated monthly objective.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.