The top graph below charts stock prices and bond yields. The smaller graph below shows the rolling ten-day correlation of stocks (SPY) and bond yields (10-yr UST). The higher the correlation, the stronger the relationship between stock prices and bond yields. Conversely, the weaker the correlation, the more stocks and bond yields move in opposite directions. As we highlight in blue, it is common for the relationship to be negative. But, as we highlight in yellow, there are periods where stocks and bonds have a positive correlation. For instance, the S&P 500 was up nearly 10% from May through July, while the ten-year yield rose by 0.70%. Such a strong correlation with already high and rising bond yields is not sustainable. Higher interest rates raise borrowing costs and impede on economic growth. Both negatively affect earnings.

Recently, the stock bond correlation has shifted back to its more normal negative relationship. The spurt in bond yields approaching the 2022 peak is weighing on the stock market. Our take is that the stock market doesn’t care about bond yields until they do. Stock gains going forward will become increasingly more difficult unless bond yields start to fall. Given this likelihood, stocks will probably become more sensitive to economic and inflation data, as well as Fed speak and monetary policy actions. If so, the stock market mantra going forward will likely be to sell stocks on good economic news and buy on bad economic news.

What To Watch Today

Economics

Earnings

Market Trading Update

Despite the selloff in the market over the last couple of trading days, market volatility remains extremely compressed. While declining volatility is bullish for equities in the short-term, as there is a lack of fear about a correction, such is also a concern. Going back 20 years, whenever volatility was as suppressed as it is currently, such has previously led to short-term corrections in risk assets or worse. Given the deep oversold condition of the index, investors should expect a reversal sooner rather than later. Historically, the unwinding of compressed volatility tends to be a rather sudden event with a sharp negative move in asset prices. I would eventually expect the same this time.

Avoiding The Volatility Tax

Buy and hold is a very popular strategy, but is it the most effective for compounding wealth? The upside to buy and hold is it’s incredibly simple and can be easily accomplished by DIY investors. But, while paying management fees or putting your own time and effort into portfolio management may be avoided, the volatility tax on buy and hold is a notable cost. The graph below, courtesy of Hi Mount, shows that avoiding both the best and worst performance days leads to higher returns and a lower risk profile. We put the data from the graph into the table below it. It shows the Sharpe ratio. The ratio measures the ratio of returns versus the risk taken. It allows for an easy comparison of different strategies. Not surprisingly, avoiding more of the highest volatility best and worst days, improves the Sharpe ratio.

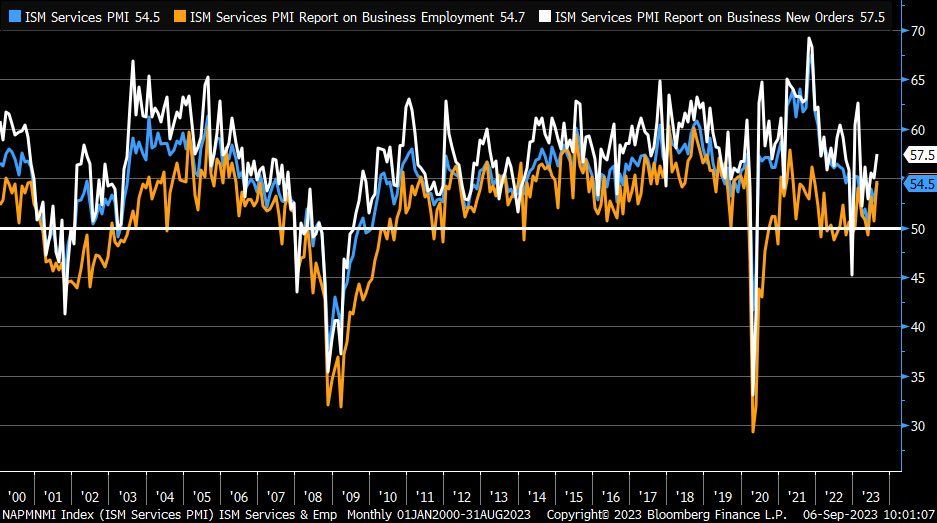

Service Sector is Heating Up

The service sector continues to drive economic growth. Additionally, Jerome Powell has mentioned the strength in the sector is feeding his inflation concerns.

As we share in the graph below, the ISM services survey has recently flirted with an economic contraction reading (sub 50) but remains resilient above 50. In yesterday’s latest release, new orders, employment, and prices rose. The only blemish on the survey is that inventories are rising and order backlogs are falling. The report will do nothing to ease Powell’s worries. However, the PMI services survey, a lesser-followed gauge of the service sector, fell from 52.3 to 50.5. The PMI report shared the following insight.

Although only fractional, the fall in new orders was the first in six months and signalled a marked turnaround from the sharp upturn seen in the second quarter of 2023. Muted demand conditions reportedly stemmed from the impact of higher interest rates and inflation on customer spending.

The odds of a Fed hike at the September 20 meeting remain below 10%, but implied Fed Funds futures saw a slight uptick to nearly a 50% chance of a hike at the November meeting. Next week’s CPI and Retail Sales will play a large role in helping the Fed decide what they will do at the two upcoming meetings.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.