Do the headlines below sound familiar? They should because the same fears and political rhetoric as 2011 are surfacing as the nation faces yet another debt crisis stalemate. Congress has raised the debt cap 78 times since 1960, but many political and media pundits are concerned that this time is different.

- US Malaise, Debt Stalemate Shake Allies Globally

- Obama tells nation debt stalemate requires compromise now

- U.S. debt stalemate sinks stocks

- How worried should we be if the debt ceiling isn’t lifted?

- A Stock Market Plunge Will Resolve the Debt-Ceiling

It’s worth looking back at 2011 to assess how the major asset classes traded before, during, and after the debt crisis stalemate. The table below shows that stocks were the worst-performing asset class both leading up to the debt crisis stalemate and in the week following resolution. Ten-year U.S. Treasury yields fell before and after the crisis. Gold was also a big winner. Surprisingly, despite fiscal turmoil, the dollar also did well before and after raising the debt cap.

This time the reaction is quite different. The S&P 500 is up 2% over the last month, while ten-year yields have risen by about 0.25%, and gold is off by 1.50%. Like in 2011, the dollar is rising before the potential crisis. We caveat the data below as there are a lot of macroeconomic, monetary, and fiscal policy differences between 2011. Further, the political dissension in the country is worse, and the fiscal imbalances are much larger.

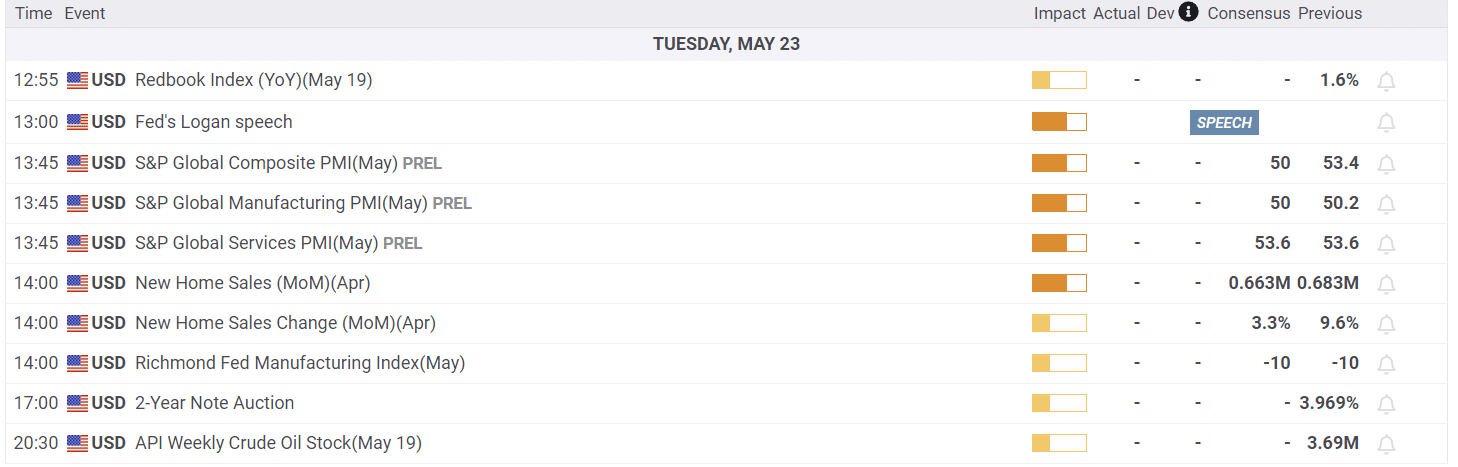

What To Watch Today

Economy

Earnings

Has Tech Been The Debt Ceiling Debacle Hedge?

Over the last few weeks, the F.O.M.O. chase in Technology stocks has baffled the more bearish prognosticators. However, an overlooked reason for investors piling into Technology stocks may be the “debt ceiling” crisis. Technology stocks, by their very nature, are long-duration assets. As such, a disinflationary environment, which will precede lower interest rates, benefits cyclical growth stocks. While technology stocks were performing well earlier in the year, it has been interesting to see the ramp in the big technology-driven stocks in the market as the debt-ceiling rhetoric of a “potential default” heated up.

As the mainstream headlines noted, the risk of failing to raise the “debt ceiling” would potentially be a technical default of interest payments. Such an event would theoretically be disinflationary, triggering an economic recession and leading to lower rates. Such would explain why the defensive and economically-sensitive stocks have been performing so poorly while only a handful of highly liquid stocks that would benefit from such an environment have risen.

While this is likely an oversimplified explanation if technology stocks have been a hedge against a debt-ceiling crisis, a resolution that leads to a debt-limit increase should lead to a reversal of that hedge. Such is because when the debt ceiling is lifted, the Treasury will need to issue a lot of debt to refund current borrowings, leading to a short-term spike in interest rates and setting the backdrop for a reversal from disinflationary to inflationary assets short-term.

It’s just a thought.

Kashkari Warns that 6% Fed Funds May Be Needed

The following headline welcomed traders early Monday morning:

FED’S KASHKARI: IT MAY BE THAT WE HAVE TO GO NORTH OF 6%, BUT IT’S NOT CLEAR.

Might he be taking advice from our article, Speak Loudly Because You Carry A Small Stick? We summarize the article as follows:

Given the lag effect of prior rate hikes and the massive leverage embedded in the economy, we advise Jerome Powell to speak very loudly but take limited further action regarding rate hikes.

Minneapolis Fed President Neel Kashkari is one of the more hawkish Fed members. The recent FOMO-like Nasdaq environment is likely pushing him to use rhetoric to scare markets. The Fed has long believed that the stock market plays an important role in consumer confidence, which drives consumption and economic activity. Given that the Fed is trying to slow the economy, Kashkari may be using fear and speaking loudly to help accomplish its task.

The Bull-Bear Market Tug of War

On Monday, we published Monetary Support Suggests Bear Market is Possibly Over. The article starts by highlighting the growing debt-to-GDP ratio and the recent sharp increase in interest rates. It then helps answer the following quote from @MichaelAArouet :

“What are the odds that the fastest tightening cycle combined with highest debt/GDP level will end up in a soft landing?”

Yes, concerns for a recession are high, especially given the sharp increase in interest rates and the debt imbalance. But, as the article notes, “Federal spending ramps up” and “Monetary support is still high.” Might the decline in 2022 have already priced in weaker economic growth, and “it is possible the recent rally in stocks, a leading indicator, combined with the ongoing monetary supports, suggests we may start to see some improvement in the economic data.”

The article ends as follows:

I am not suggesting the markets, and the economy, won’t potentially struggle in the months ahead. However, we could avoid a deep economic due to the still massive amounts of monetary support in the system.

These competing forces will make investing more difficult until those monetary excesses reverse.

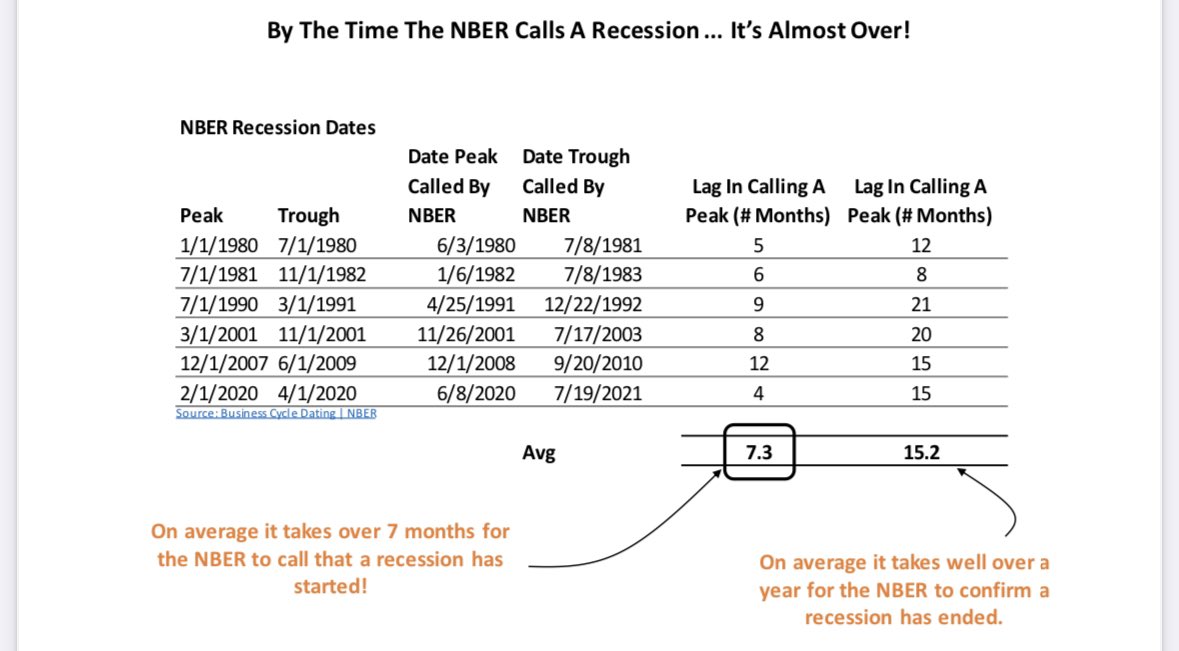

Don’t Wait on NBER to Call a Recession

The NBER is the official arbiter of recessions. The problem, as the Piper Sandler table below shows, is that they are, on average, about seven months too late in determining when a recession starts and over a year late in determining when a recession ends. While it can be problematic for investors relying on the NBER, they should be aware the NBER waits for revised economic data. Further, they heavily rely on a higher unemployment rate as a key recession determinant. The labor markets tend to be lagging economic indicators as layoffs do not typically occur until a recession is underway.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.