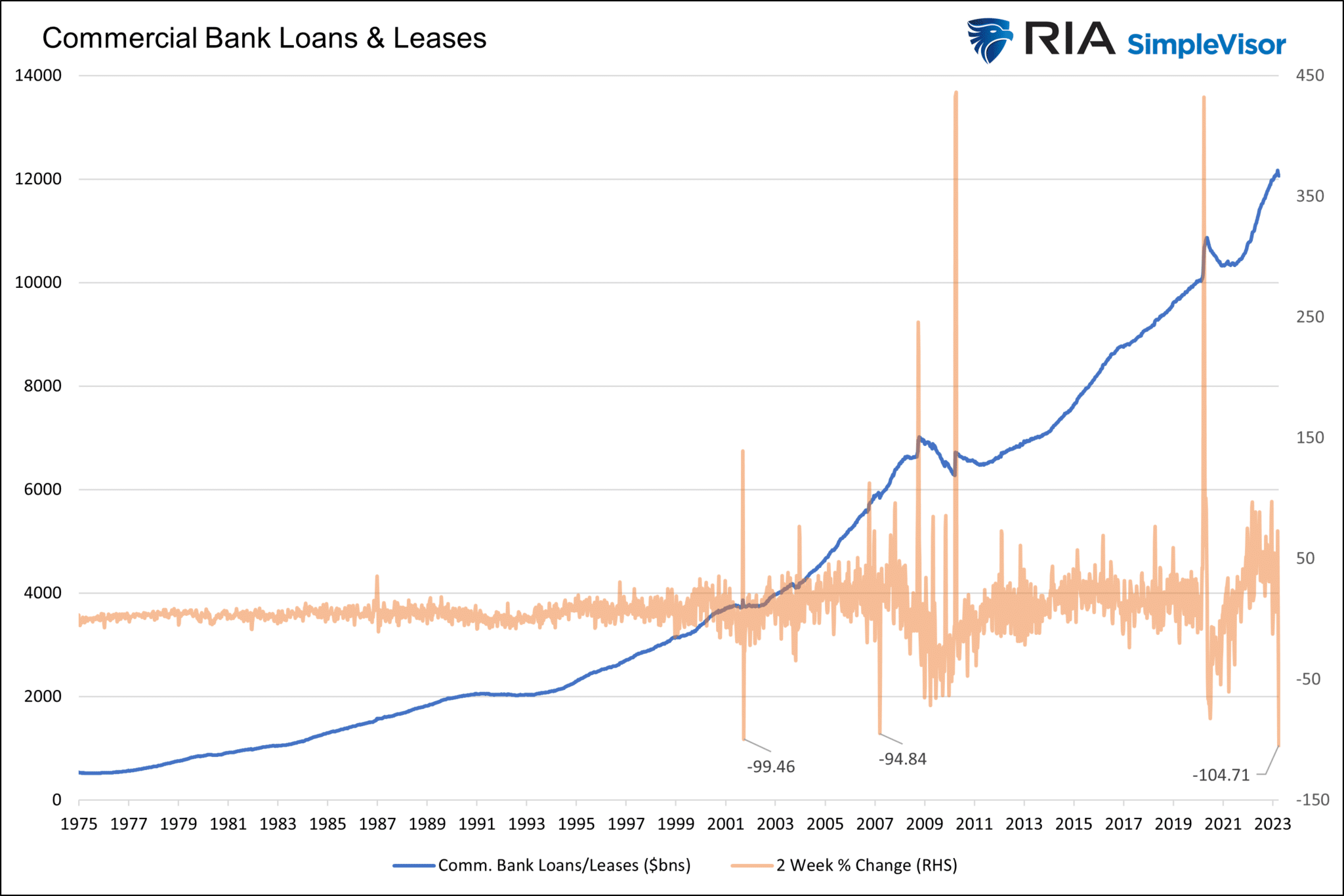

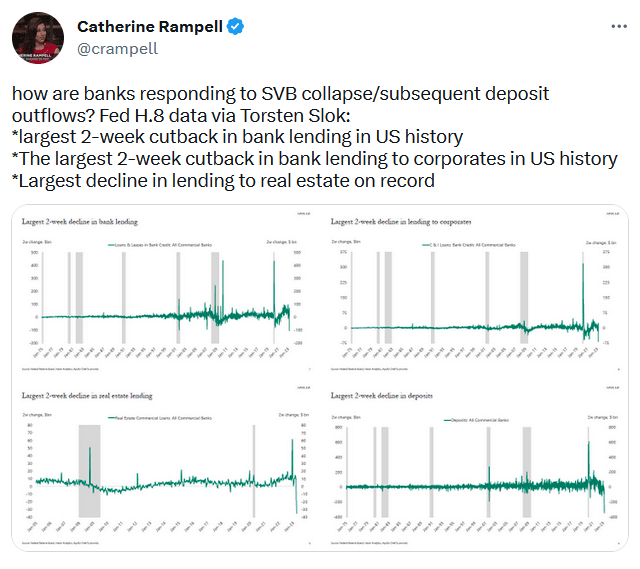

CPI, Retail Sales, and Employment are often the three most important economic data releases in a typical month. It turns out that last Friday’s employment report was not even the most important report on that day. On Friday, the Federal Reserve reported that U.S. Commercial Bank Loans fell by $104.7 billion in the last two weeks of March. This was the largest 2-week drop on record. However, as the chart shows, the decline is minimal thus far, compared to the last two recessions in which loans fell over an extended period. Today’s Tweet Of The Day highlights that loan declines are hitting the corporate and real estate sectors hard. To zoom in on the pictures, click HERE.

The Federal Reserve’s H.8 report chronicles bank balance sheets, including loans and assets. Investors will likely follow it closely in the coming months as economic activity often correlates strongly with debt growth. As we shared in prior Commentaries, tighter bank lending standards can take up to a year to be felt economically. But, when the actual amount of bank loans shrinks, the drag on the economy is almost immediate. While the two-week change is the largest since 1975, the total decline is tame compared to 2008 and 2020. However, if the trend lower continues, a recession later this year becomes much more probable.

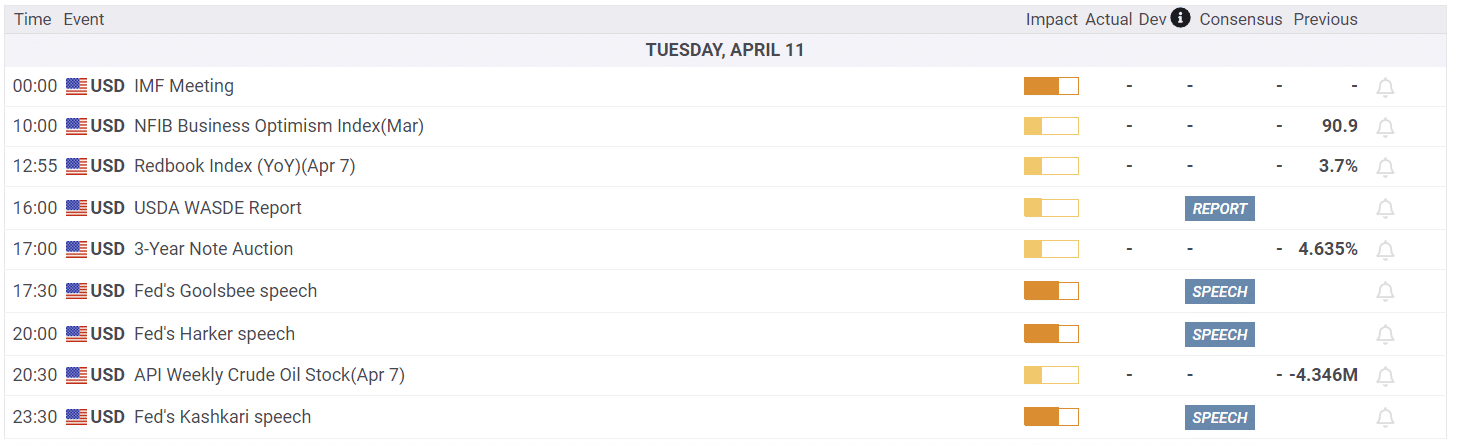

What To Watch Today

Economy

Earnings

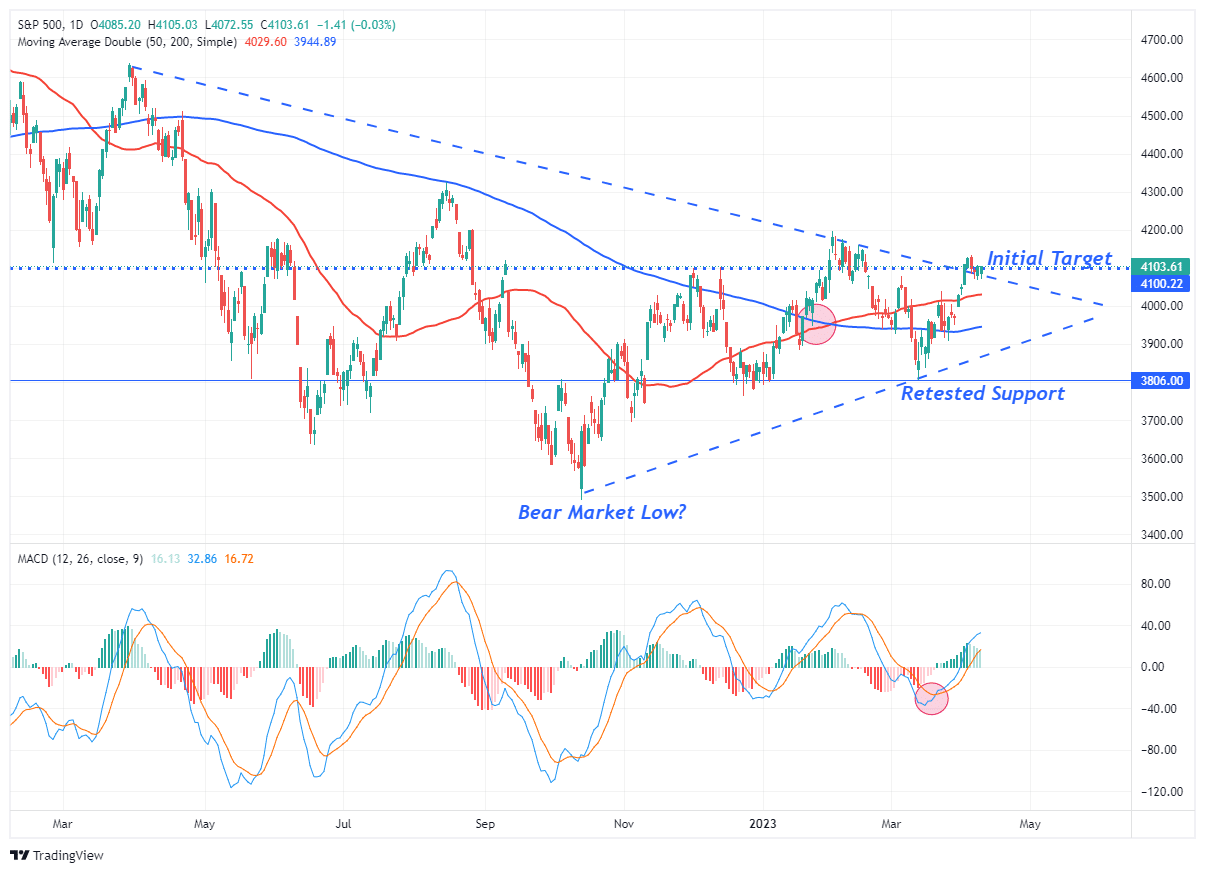

Market Trading Update

As I noted in this weekend’s newsletter, we are seeing some rotation from the Technology sector into more defensive sectors. Such was expected given the large outperformance by the Technology sector since the beginning of the year. With this rotation starting, we reduced our technology holdings yesterday and will look for weaknesses to add to our core large-capitalization technology holdings.

Overall, the market continues to hold up, challenging short-term resistance. Yesterday, the market opened weakly but rallied into the close, reversing all the early losses. That is a very bullish indicator that suggests buyers are showing up to remove sellers from the market. With the buy signal still intact, there is no reason to get overly defensive. Maintain equity exposure now and look for opportunities to add exposure if needed. We will recommend reducing that exposure when the next sell signals are triggered.

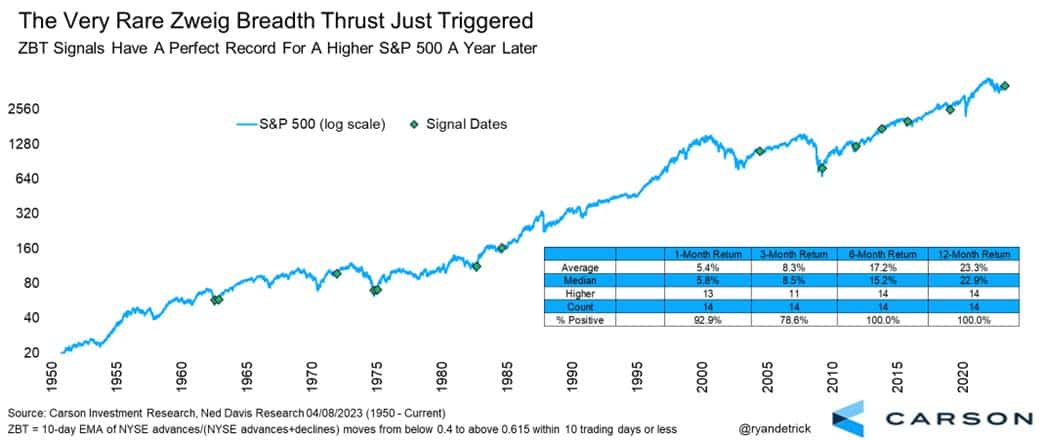

Bullish Zweig Breadth Thrust

The graph below, courtesy of Ryan Detrick, shows the S&P 500 just triggered a Zweig Breadth Thrust. Since 1950, only 14 such episodes have occurred. On average, one-year returns are +23% after the indicator occurs. To calculate the indicator, divide the number of daily advancing stocks by the total number of advancing and declining stocks. The indicator triggers when the 10-day moving average of that calculation increases from below 40% to above 61.5%.

Probability Neglect – Behavioral Traits Part V

In Yesterday’s Commentary, we discussed the Prospect Theory. The gist is that investors don’t view risk and return equally. Probability neglect falls along a similar theme.

Regarding “risk-taking,” there are two ways to assess a potential outcome. There are “possibilities” and “probabilities.” As individuals, we tend to lean toward what is possible such as playing the “lottery.” The statistical probabilities of winning the lottery are astronomical. However, this infinitesimal “possibility” of being fabulously rich makes it popular. Las Vegas profits for one reason; almost all gamblers favor possibility over probability.

Investors tend to neglect the “probabilities,” specifically the statistical measure of “risk” undertaken with any given investment. Our bias is to “chase” stocks that have already shown the biggest increase in price as it is “possible” they could continue higher. However, the “probability” is that when the masses discover the opportunity, most gains have likely already been garnered.

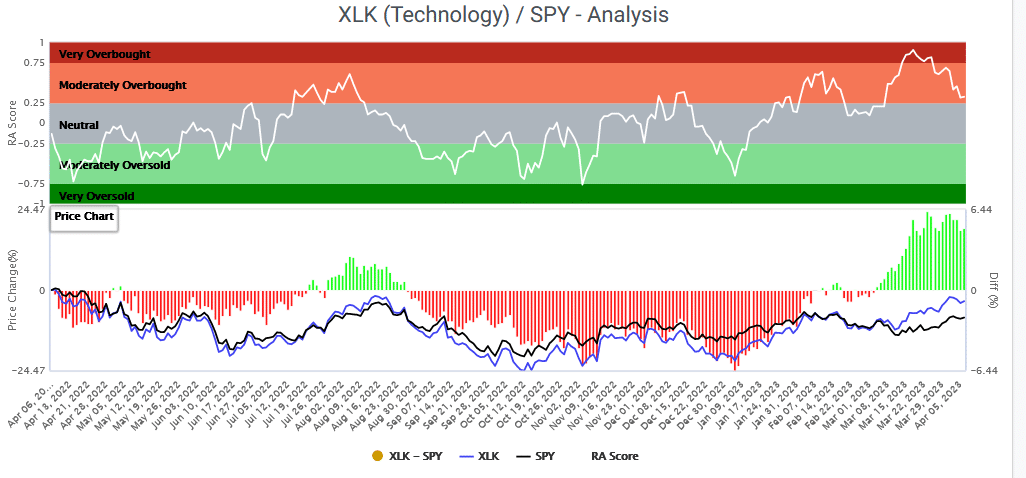

Recently, we have seen emotional rallies and drawdowns. The key to managing wealth during these manic episodes is relying on technical indicators, not emotions. For example, the Tech sector has been on fire over the last few months. However, in the process, the sector became extremely overbought. While the rally and outperformance of the sector may continue, mathematical probabilities argue it will likely underperform for a little while. The graphs below from SimpleVisor’s proprietary relative sector analysis show that XLK was extremely overbought in mid-March. Since then, it has trended toward fair value and underperformed the S&P 500. It was hard to avoid the sector in mid-March, but realizing the probability it would “need a rest” was the correct analysis.

Cyclical/Defensive Equities, ISM, and Liquidity

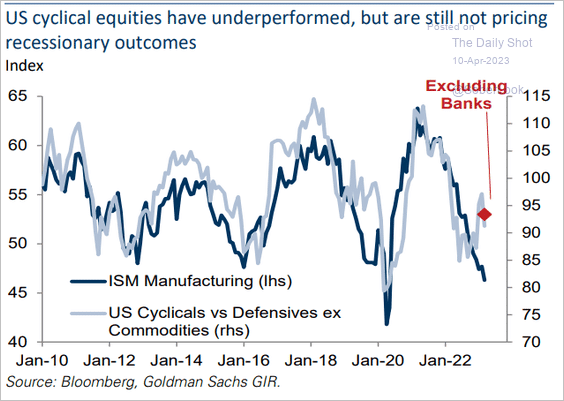

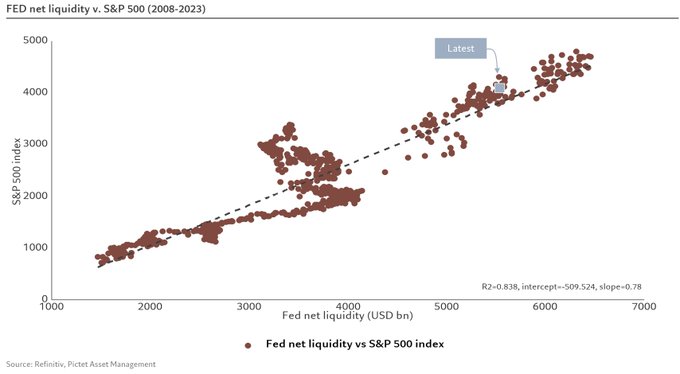

The graph below, courtesy of the Daily Shot, shows the typically tight relationship between the ISM manufacturing index and the relative performance of U.S. cyclical versus defensive stocks. Recently, the correlation has diverged. Despite ISM at levels that often accompany recessions, many investors continue to believe that a soft landing, not a recession is in the cards. The second graph below may provide an explanation for the divergence. Steve Donze at Pictet Asset Management shows that the correlation between Fed net liquidity and changes in the S&P 500 has been robust recently. Currently, the S&P 500 is about 8% above where it should be given the relationship.

With the banking crisis liquidity injections slowly unwinding and the Treasury likely to add to its Fed balances once the debt cap limit is resolved, the trend lower in Fed assets (QT) will also reduce liquidity. Such may also cause the relationship between ISM and cyclical/defensive stocks to normalize.

For more on Fed liquidity, please see our article entitled S&P 3500 by Year End. Per the article:

The size of the Fed’s assets less the sum of the TGA and RRP equals the amount of Fed-generated liquidity in the system. Recent changes in net liquidity shed light on how the S&P 500 trends.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.