Alongside the financial and REIT sectors, small cap stocks are falling victim to the banking crisis. The logic is that many small companies tend to rely heavily on debt financing. As financial lending standards tighten and credit spreads widen, small cap companies must pay higher interest rates on their debt. Further, those may be the lucky companies. Some companies with poor financials may find it too costly to borrow and dilute their shareholders via issuing equity. Over 20% of the Russell Small Cap Index is estimated to be comprised of zombie companies. These are companies that have interest coverages of less than one. As a result, they must borrow to meet their debt obligations.

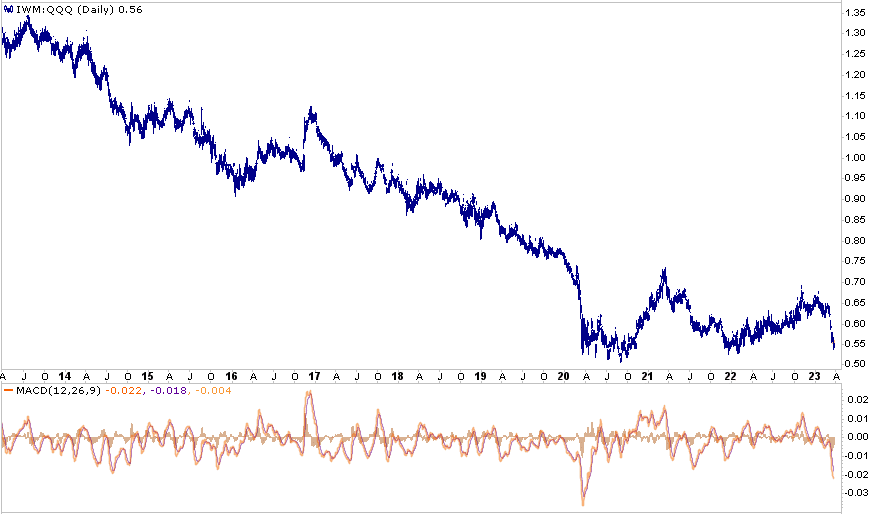

Large tech companies, on the other hand, are flourishing in the current environment. Not only does the dip in interest rates help their valuations, but many of these companies are not burdened with debt, nor will they have similar problems borrowing. The graph below shows the ratio of small cap stocks (IWM) to the NASDAQ (QQQ) erased thirteen months of small cap outperformance in only a few weeks. Below the graph, note that the MACD is very oversold, meaning it might bounce in the coming days or weeks. We offer caution, if lending conditions tighten appreciably and corporate bond spreads widen, any bounce may be a chance to reduce or eliminate small cap stocks that are overly reliant on debt.

What To Watch Today

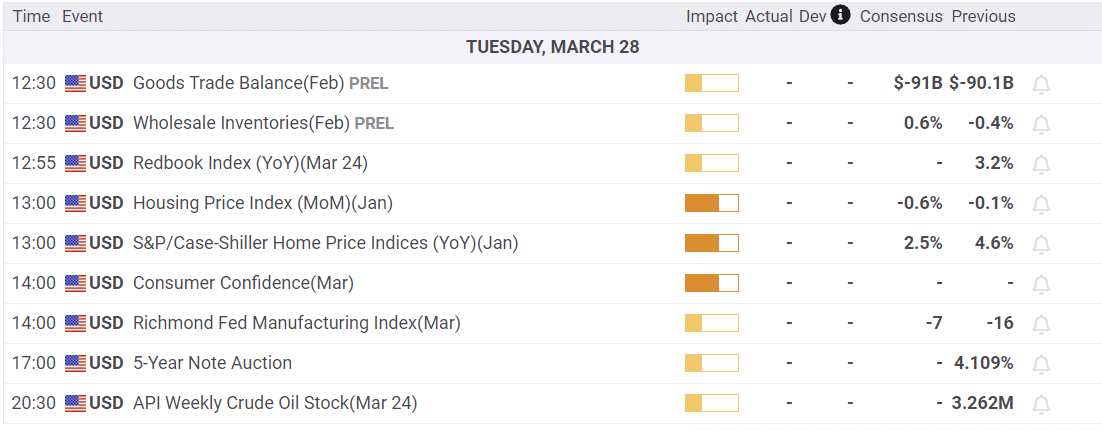

Economy

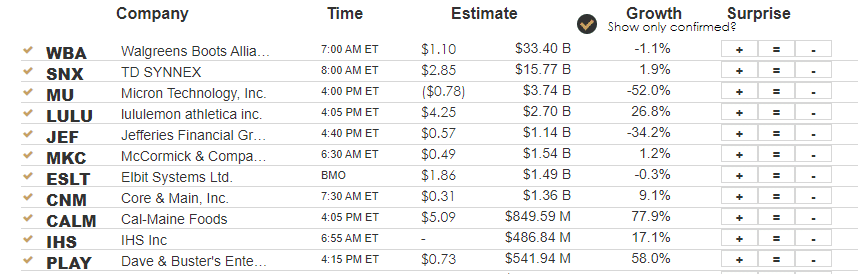

Earnings

Market Trading Update

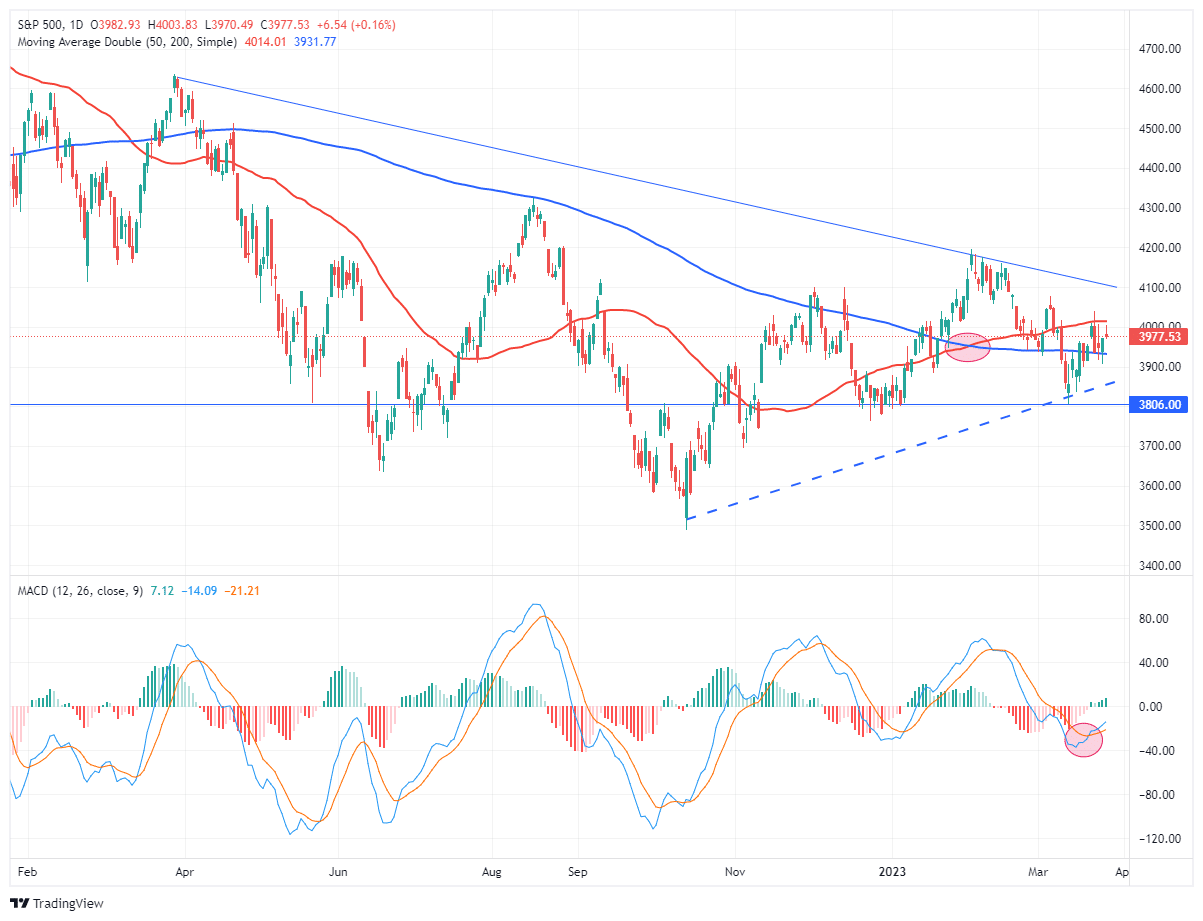

The market struggled a bit yesterday, trading in positive territory but volatile. Currently, traders are torn between concerns over the recent banking crisis and hope that the Fed is now finished hiking rates. Despite all of the headline risk, the market continues to trade bullishly and above support at the 200-DMA. With buy signals triggered, we did add a small trading position in the S&P 500 yesterday to increase exposure for now. When this trade is over or the market breaks the 200-DMA, we will reduce equity risk accordingly.

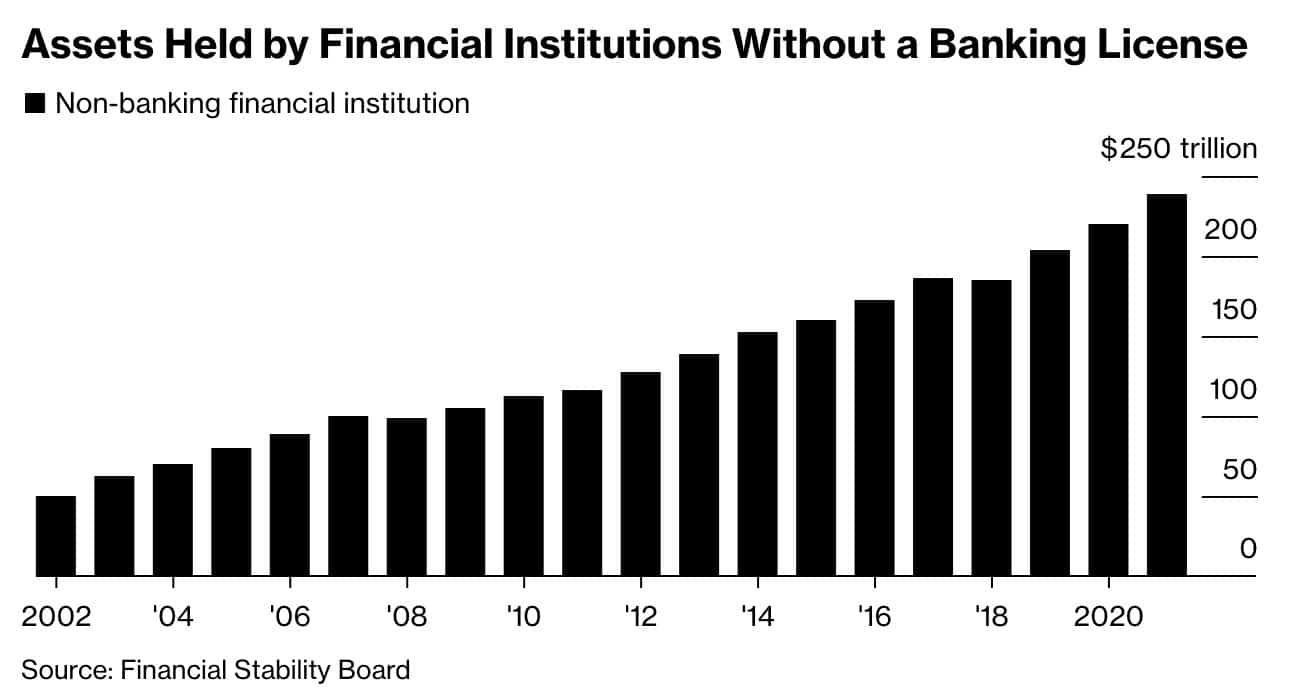

Shadow Banking

Recently, financial stability issues in the banking sector are coming to light. However, some issues affecting banks equally affect the shadow banking sector. The graph below shows assets held by non-bank financial institutions (shadow banks) have risen 2.5x since 2008. The graph, courtesy of Bloomberg, was accompanied by the following quote:

The recent turmoil will likely lead to deeper probes into shadow lending globally, which includes credit provided by private equity firms, insurers and retirement funds. That means identifying where the risk ended up after it moved off bank balance sheets

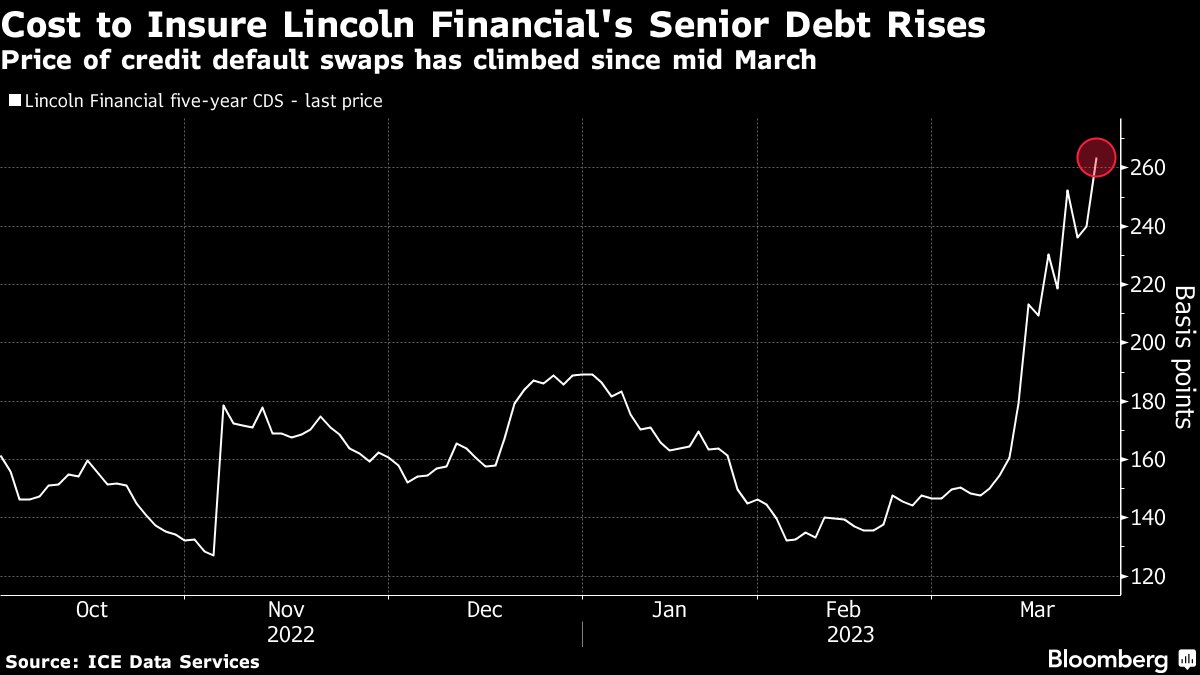

Along these lines, Lincoln Financial and other large insurers are seeing attention turned to their risks. In particular, investors are concerned about their extensive commercial real estate holdings. The chart below, also from Bloomberg, shows the price of credit default swaps on Lincoln Financial has doubled over the last few weeks.

Digging Into The Tech Rally

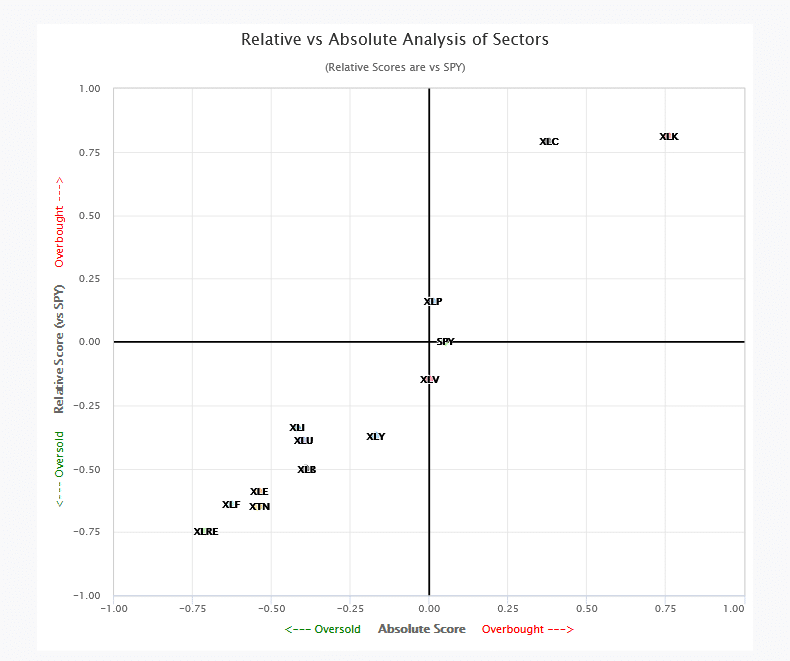

Since March 1, the tech sector (XLK) is up over 7%, while the broader S&P 500 is barely eking out a gain. To better appreciate what is driving technology, we share proprietary analysis from a few SimpleVisor graphs.

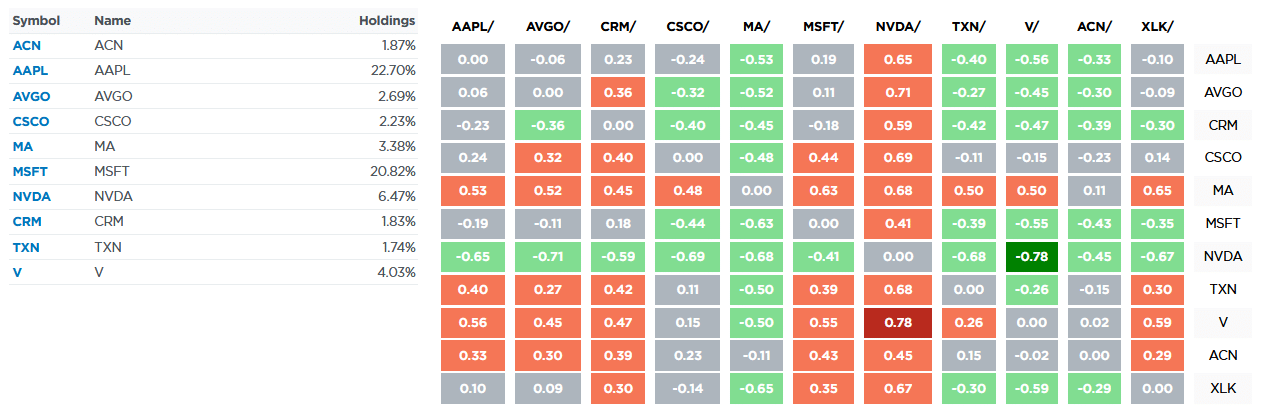

SimpleVisor uses our relative and absolute analysis to help gauge which sectors are hot and which are not. The value of analyzing sectors and stocks with relative and absolute methods is that sectors tend to rotate. As such, hot sectors stop outperforming, and at the same time, underperforming sectors take the lead. The graph below shows that technology (XLK) has very overbought scores on the relative and absolute axes. Every other sector, except communications and staples, is at fair value or oversold. The table below the scatter plot helps determine which technology stocks lead the way within the sector. Looking at the bottom row, comparing each stock to the sector ETF, we find that NVDA, MSFT, and CRM are the most overbought. Not surprisingly, the two most oversold are V and MA. It is very debatable whether they are technology or financial stocks.

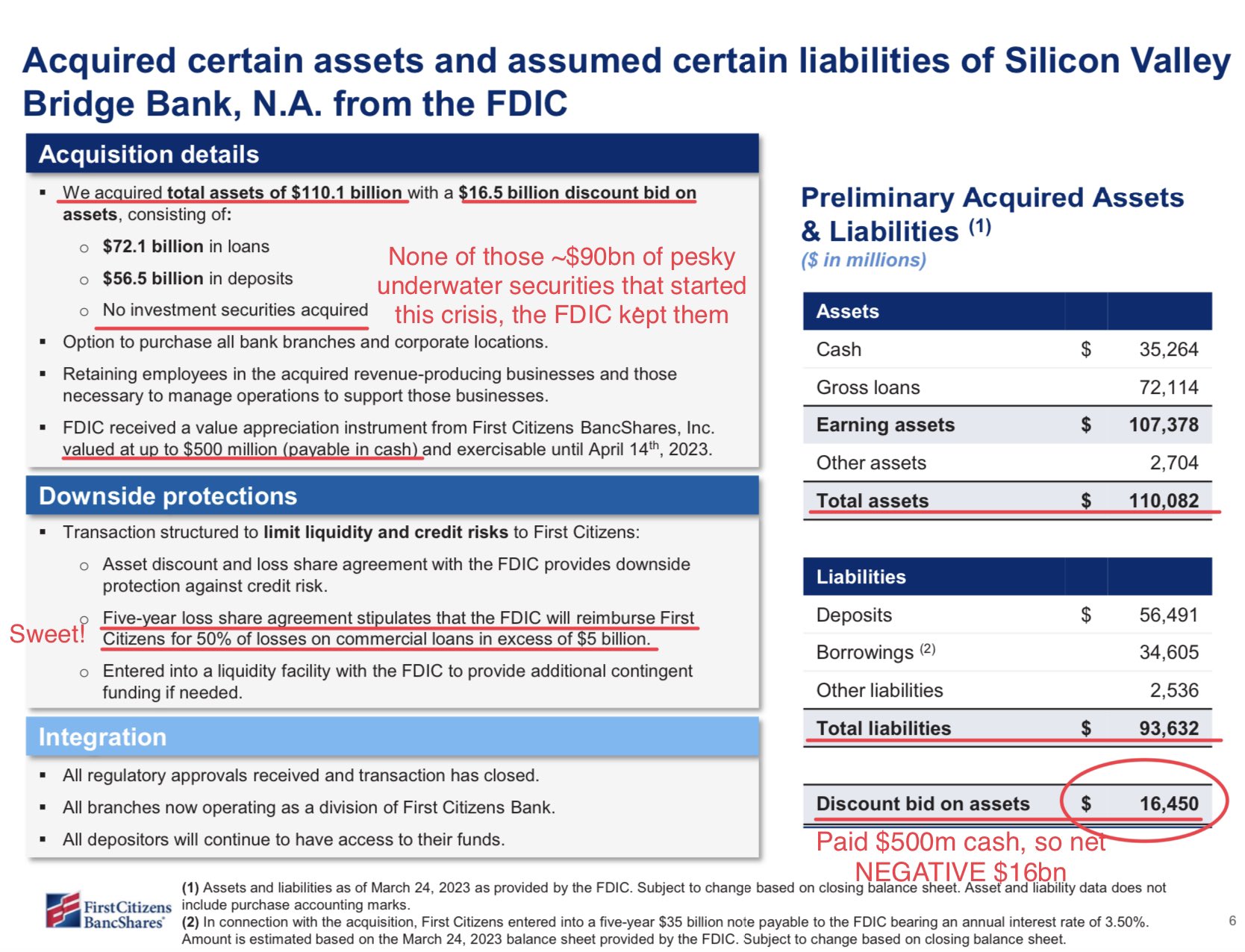

First Citizens Buys SVB

First Citizens is buying Silicon Valley Bank for $500 million. A year ago, SVB was worth nearly $40 billion and at the same time, First Citizens was half its size. The graphic below shows the terms of the buyout. Per First Citizens, they “paid” negative $16bn in equity for SVB. In other words, they think they are buying SVB’s assets at a 15% discount. They avoided buying about $90bn of troubled assets. Also, prompting First Citizens to purchase SVB, the FDIC will cover 50% of commercial loan losses if they exceed $5 billion. The FDIC will bear any losses on SVB’s loan book outside of what First Citizen assumes. They currently estimate that number to be about $20 billion. The second graph below shows that First Citizens (FCNCA) shares rose nearly 50% on Monday. Investors seem to think First Citizens got quite a deal.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.