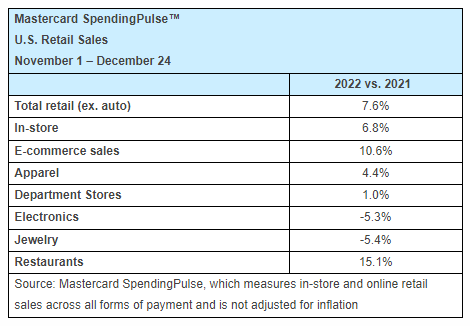

Mastercard’s SpendingPulse report provides valuable information on credit card spending through the holiday buying season. The SpendingPulse report below shows that spending via Mastercard credit cards rose 7.6% from November 1st to Christmas Eve. The data exclude auto sales. Mastercard’s data aligns with estimates from other credit card companies, retailers, and trade associations. While holiday sales growth seems robust, there are two factors worth considering. First, inflation for the non-durable products shown below was higher than 7.6% in most cases. Ergo, real growth was around zero percent. Second, credit card debt outstanding is up over 10% from the 2021 holiday season.

Excluding inflation and unsustainable credit card balances, it appears holiday spending may not have been as strong as Mastercard and others are making it out to be.

What To Watch Today

Economy

- 8:30 a.m. ET: Initial Jobless Claims, week ended Dec. 24 (225,000 expected, 216,000 prior)

- 8:30 a.m. ET: Continuing Claims, week ended Dec. 17 (1.706 million expected, 1.672 million prior)

Earnings

- No notable earnings releases today

Market Trading Update

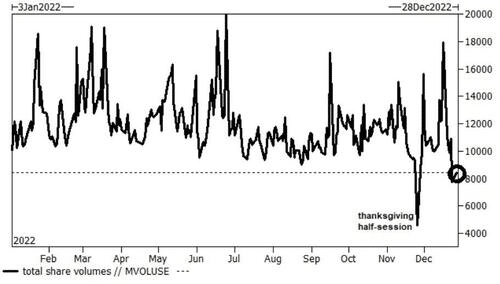

“Ba-Humbug” was the best way to sum up yesterday’s market action which with only two trading days left in the year, we can safely assume that “Santa” took a vacation and left Wall Street with the proverbial “lump of coal.”

The Nasdaq printed a fresh 2022 low amid the second lowest trading volume day of the year. Such is an important note. While the performance of the last few days have been dismal, we suspect much of this is due to both light trading volume and managers dumping stocks heading into year-end reporting. (Who wants to have $TSLA on their books.)

Such is why we have recommended not taking the year-end action too seriously as the “inmates run the asylum.” We will find out the true tenor of the market when traders return from their Christmas breaks in the New Year. There is a substantial risk of getting whipsawed in individual equities right now.

Nonetheless, market action remains dismal. The MACD “sell signal” remains firmly intact and the market is now short-term VERY oversold. If you are wanting to sell, I would look for a bounce to sell into at this point. There is a lot of overhead resistance that will continue to challenge markets into the New Year.

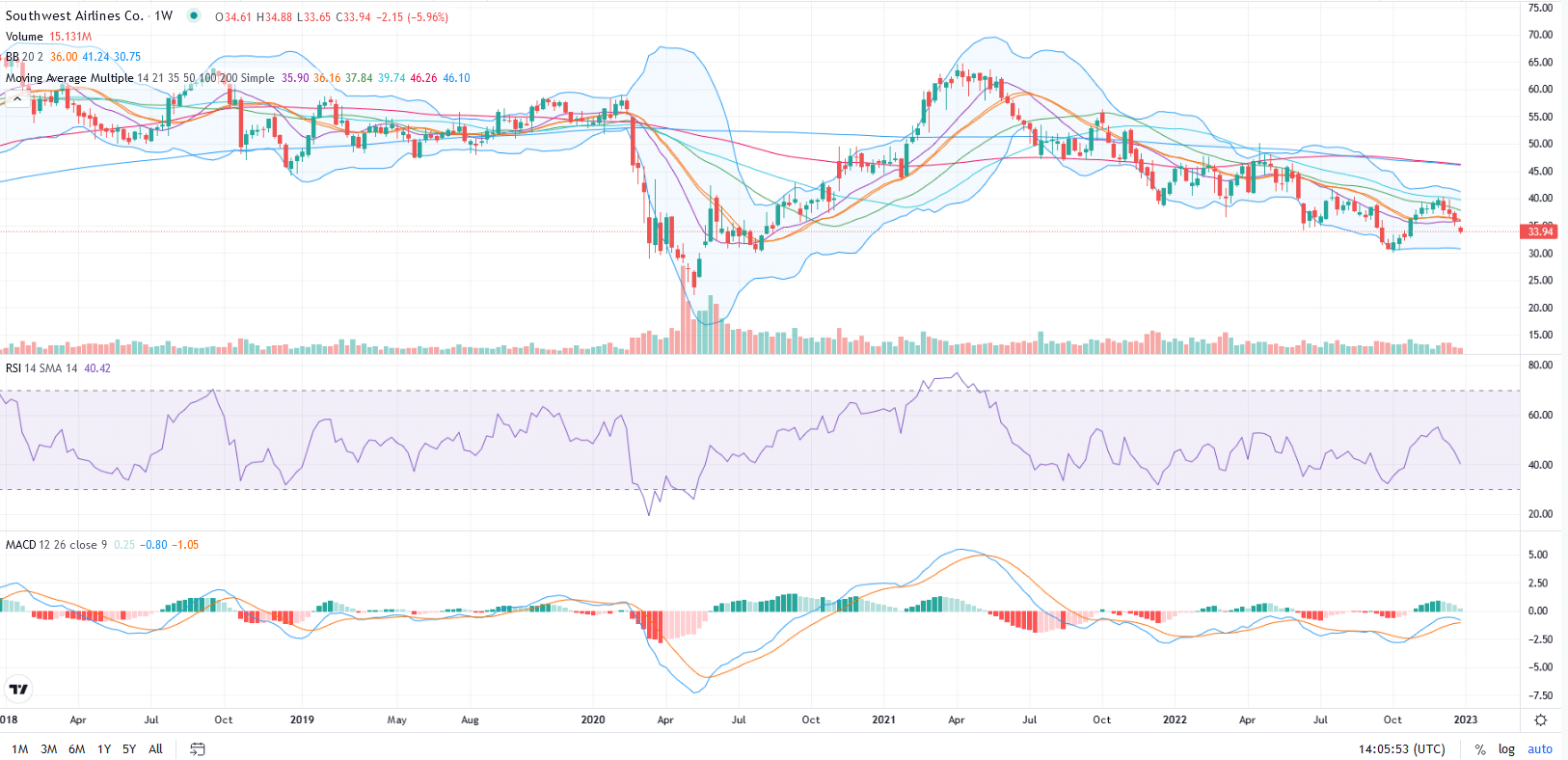

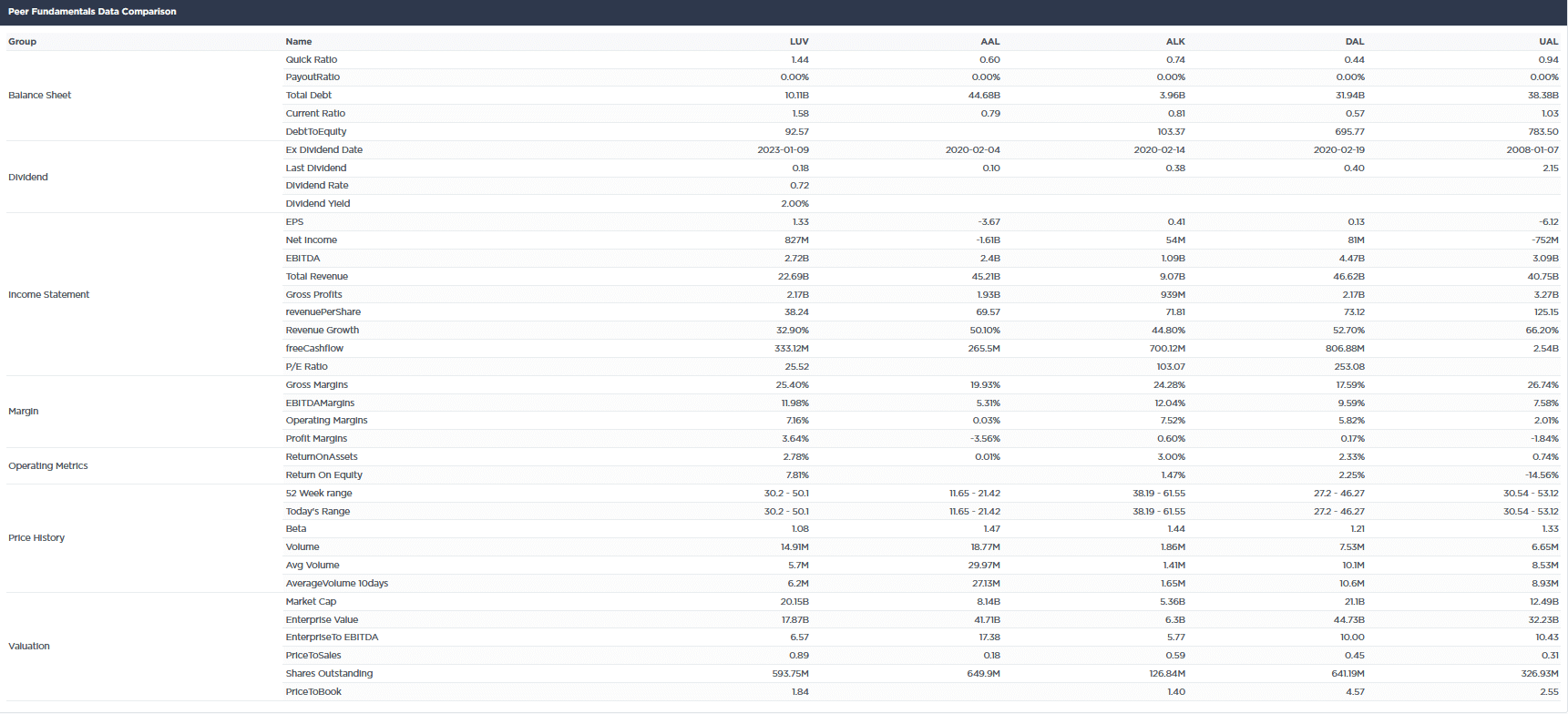

Is Southwest Airlines a Buy?

Wednesday’s Commentary opened with Southwest Airlines and its weather-related struggles over the last week. Southwest (LUV) shares peaked in early April 2021 at $63 and are now trading at nearly half of that value. Let’s do some fundamental analysis in SimpleVisor and see if buying LUV makes sense.

The first graph shows that LUV is not far from its April 2020 pandemic lows. At that time, air travel was virtually shut down, and there was little hope it would normalize anytime soon. Bankruptcy was a possibility at that time. The price rose sharply once the government bailed out the airline industry, and air travel started to pick up. In one year, the stock rose above its pre-pandemic level. Since peaking, it has trended lower. The Bollinger Bands suggest the price can fall to around $30. The RSI and MACD also suggest its price has room to fall.

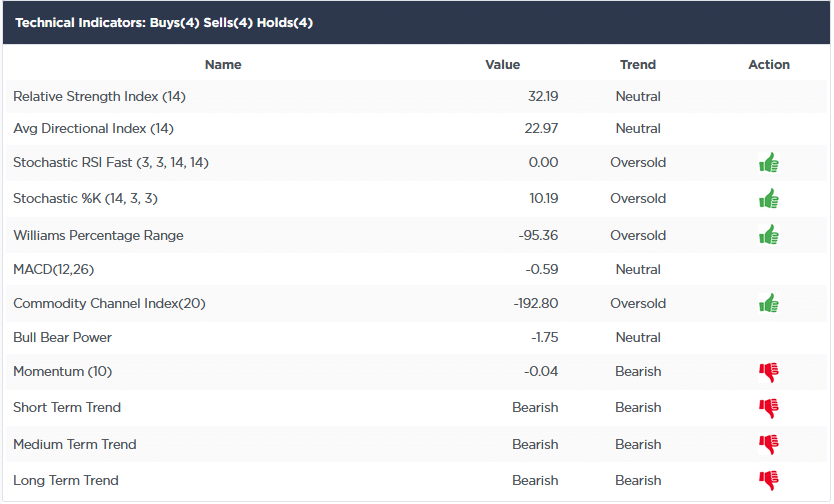

The second table summarizes technical studies. The recent trend is poor, but some shorter-term technical indicators are starting to signal the stock is in oversold territory.

Southwest Airlines Fundamentals

Our fair value model in the SimpleVisor Screener tool points to a fair value of 39.69, about 15% above its current price. The first table below shows LUV has a forward P/E of 10.48 and price to book value of 1.84. As a comparison, the S&P 500 has a forward P/E of 18.81 and a price-to-book value of 2.95. From that perspective, it is cheap versus the market, but, as shown in the second table, its valuations are similar to its competitors.

LUV is undoubtedly cheaper than it has been. Further, it is trading at levels when investors were panicked, and LUV’s future was in jeopardy. That said, a case can be made that it was too expensive heading into the pandemic, and its valuations can get cheaper. With high recession odds and the likelihood of less air travel, the stock can undoubtedly fall further. However, at lower prices and a cheaper valuation, it may be worth tracking in 2023.

200+ Years of Bonds

The graph below charts 10-year U.S. Treasury yields going back to 1790. The chart gives perspective to the recent surge in yields. Compared to the post-WW2 and 1970s inflation era in which bond yields rose from 1.7% to 15.8%, the recent experience seems exceptionally mild. However, note that the recent increase is notable compared to other short-term yield increases. Importantly, many sharp increases occurring over short periods led to financial crises.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.