While the world’s central banker’s aggressively hiked interest rates and curtailed QE to fight inflation, the Bank of Japan maintained a stimulative monetary policy. In a shock to markets, it appears they are finally reversing course. On Tuesday, they raised the cap on ten-year Treasury yields from 0.25% to 0.50%. This action follows twenty years of zero to negative overnight borrowing rates and, more recently, yield curve control (rate caps) to keep monetary policy as stimulative as possible. The Bank of Japan will continue to cap interest rates via QE. Further, they are not yet increasing short-term borrowing rates. The move is not a traditional hike per se, but it will raise borrowing costs and alert investors to a change toward a more restrictive policy. It also warns that the Bank will not tolerate further yen weakness.

The Bank of Japan has been concerned about rising inflation and a weakening yen for the last few months. However, recent bouts of fixed-income market illiquidity, including the UK pension crisis, kept them from taking action. Assuming liquidity remains acceptable, as it has been recently, we suspect the bank will take further steps, including increasing short-term borrowing rates. Below we share our thoughts on how this major monetary policy regime change introduces a new set of risks for global markets.

What To Watch Today

Economy

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Dec. 16 (3.2% prior)

- 8:30 a.m. ET: Current Account Balance, Q3 (-$222.0 billion expected, -$251.1 billion prior)

- 10:00 a.m. ET: Existing Home Sales, November (4.20 million expected, 4.43 million prior)

- 10:00 a.m. ET: Existing Home Sales, month-over-month, November (-5.2% expected, -5.9% prior)

- 10:00 a.m. ET: Conference Board Consumer Confidence, December (101.0 expected, 100.2 prior)

- 10:00 a.m. ET: Conference Board Present Situation, November (137.4 prior)

- 10:00 a.m. ET: Conference Board Expectations, November (75.4 prior)

Earnings

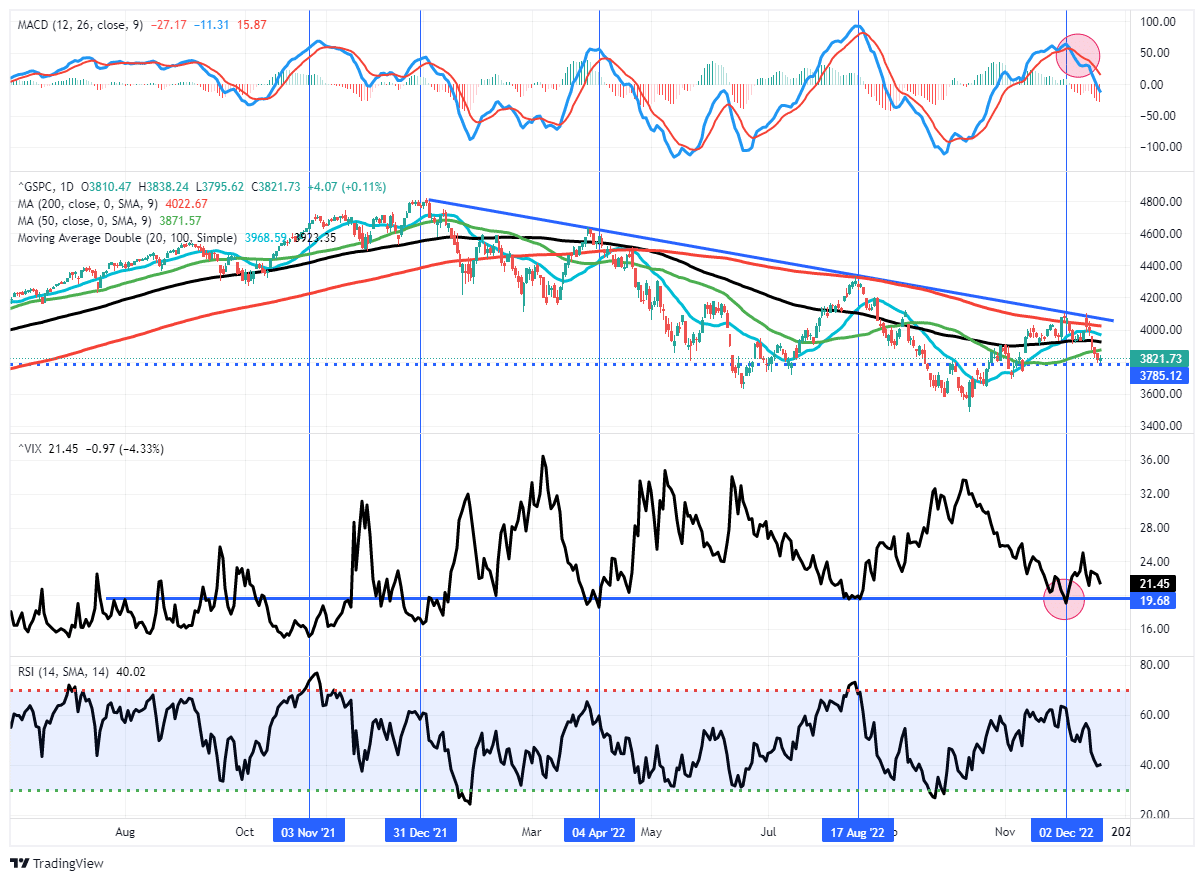

Market Trading Update

The market is in positive territory this morning as two crucial earnings reports from Nike (NKE) and FedEx (FDX) came in better than expected.

“Nike shares added 12% after the apparel maker beat Wall Street’s expectations for quarterly earnings and revenue. FedEx gained 4.7% even as it fell short of revenue expectations. The package delivery giant beat consensus earnings per share estimates on per-share.” – CNBC

Even with stock futures pointing higher this morning, it does little to change the current trajectory of the market. However, today could help start the “Santa Claus” rally but we will need to see some follow-through the rest of the week. Continue to remain risk-averse for now until some of our signals begin to improve. The market is decently oversold enough on a very short-term basis to elicit a rally, but that rally should be sold into until the market regains some positive footing.

Why Investors Should Care About The Bank of Japan

Japan set their Fed Funds equivalent borrowing rate at or below zero for the better part of the last twenty years. They introduced QE well before the Fed and more recently added yield curve control to keep longer-term yields close to zero. The Bank now owns over half of the Japanese Treasury debt outstanding. As a result, Japanese investors have been crowded out of the bond market. Further, unable or unwilling to accept near-zero yields they have been investing their capital abroad. For example, Japanese investors hold over $1.2 trillion of U.S. Treasury debt, making it the largest investor of Treasuries outside of the Federal Reserve. They also own stocks, corporate bonds, and other assets from many countries.

While Japan is finally tightening monetary policy, equally important, they are also protecting the yen and trying to get capital to flow back to Japan.

Macro Alf points out that Japanese derivative markets imply further restrictive monetary policy in the future. Investors are “listening to the BoJ and adjusting for a new monetary policy regime in Japan.” So what might that mean?

Now that Japanese investors are getting positively rewarded to keep their cash at home during a global economic slowdown and periods of high macro uncertainty… …they probably will choose to do that more. That strengthens the Yen, and negatively affects foreign assets.

When one of the largest capital exporters in the world decides to domestically reward savings with a higher risk-free rate, there are big macro consequences.

Another aspect to assess is the yen carry trade. Globally, institutional investors have been borrowing in yen and investing the funds in other countries to earn a spread. Assuming the yen strengthens and Japanese borrowing rates rise, the incentive to borrow in yen fades. As such, this source of leverage and therefore liquidity for global markets may be diminishing.

The graphic below shares Bloomberg’s summary on the Bank of Japan’s action to help appreciate the gravity of the announcement.

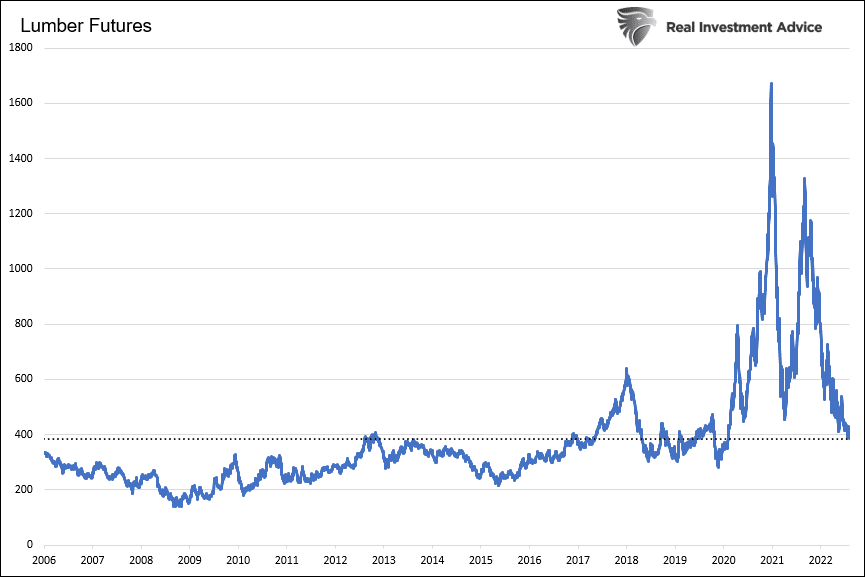

Timberrrrrr

On March 1, 2020, weeks before the pandemic shut down the economy, lumber futures were trading at $423. Stimulus checks and historically low interest/mortgage rates lead to a surge in demand for building supplies. Seemingly insatiable demand, supply line problems, and labor shortages pushed the price of lumber almost 4x higher to $1670 in a little more than a year. As we often find, the cure for high prices is high prices. High prices curtailed demand. At the same time, supply line problems were healing. As a result, the cost of lumber has been on quite the roller coaster. The current price is below where it was before the pandemic hit, but not without a lot of volatility.

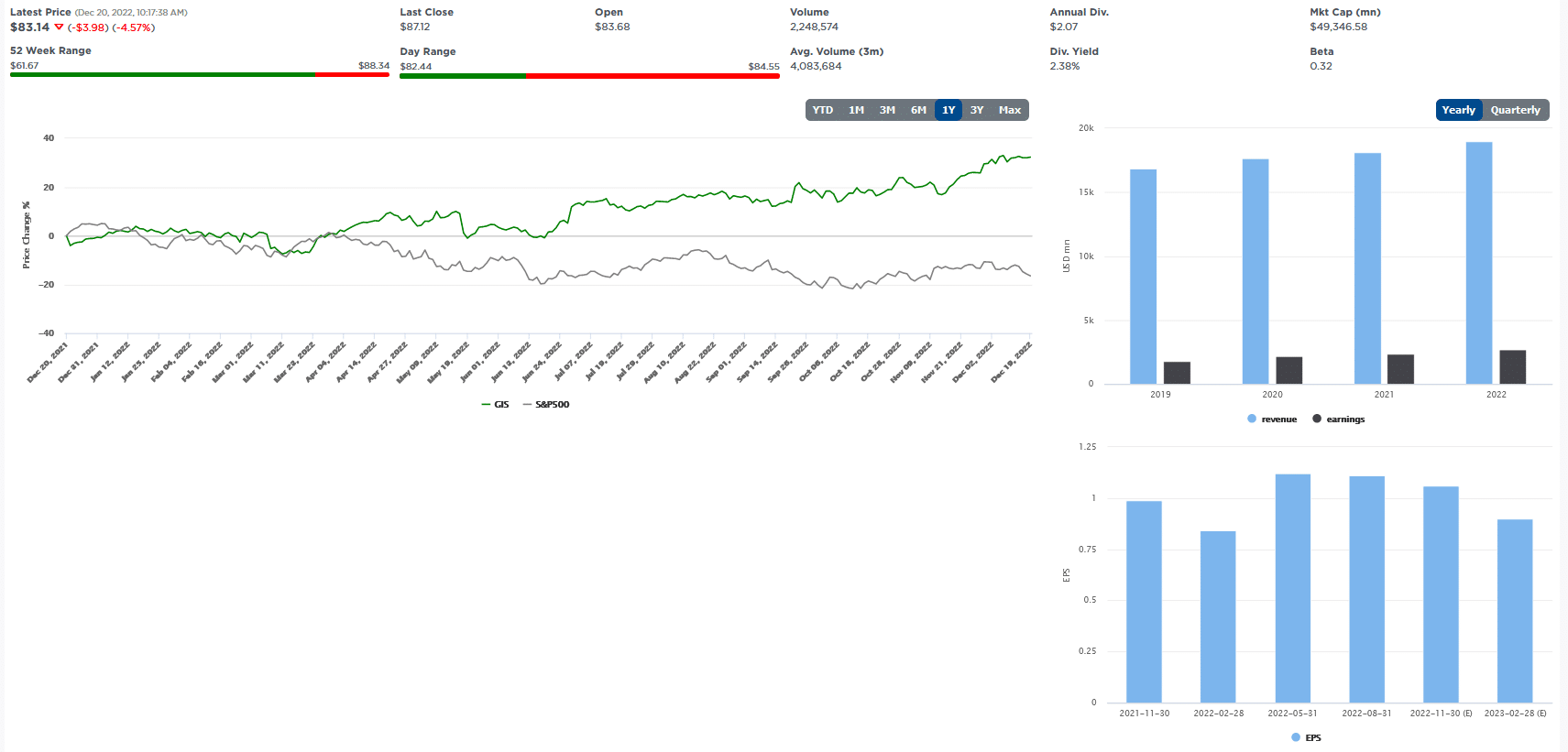

General Mills

As shown below, stock in General Mills (GIS) has been on a tear this year as investors seek safety and earnings stability. Yesterday, General Mills rewarded investors with a strong earnings report but the stock traded lower by nearly 5%. Might conservative stocks, like General Mills, have grossly outperformed the market hit valuations that are too high, especially if a recession occurs? GIS has a forward P/E of 20 and a PEG ratio of 3.9. While the forward P/E isn’t outlandish it is very high for a company with such slow growth, as the PEG ratio tells us.

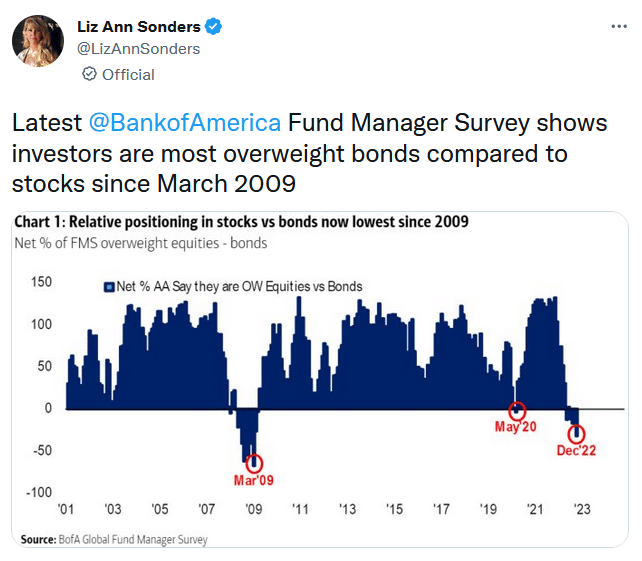

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.