U.S. Investors woke to the following headline yesterday morning: “JAPAN TOP CURRENCY DIPLOMAT KANDA: FOREX ACTION CAN BE TAKEN ANY DAY, ANYWHERE, INCLUDING ON HOLIDAYS.”

The Bank of Japan (BOJ) is now publicly intervening in the currency markets to support the slumping yen. While they have likely been intervening behind the scenes to stem yen deprecation, they are now doing it publicly. Japan appears to be drawing a line in the sand regarding how far they will let the yen fall. Japan has a tough battle ahead of them. They have significantly more debt than the U.S. and other developed nations. As such, their ability to fight inflation with higher interest rates, as all other central banks are now doing, is minimal. Overtly buying the yen, versus adapting hawkish monetary policy, may not yield their desired results as large institutional investors may bet against their efforts given its poor fundamental backdrop.

What To Watch Today

Economy

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, September Preliminary (51.1 expected, 51.5 prior)

- 9:45 a.m. ET: S&P Global U.S. Services PMI, September Preliminary (45.0 expected, 43.7 prior)

- 9:45 a.m. ET: S&P Global U.S. Manufacturing PMI, September Preliminary (46.0 expected, 44.6 prior)

Earnings

- No notable earnings releases today

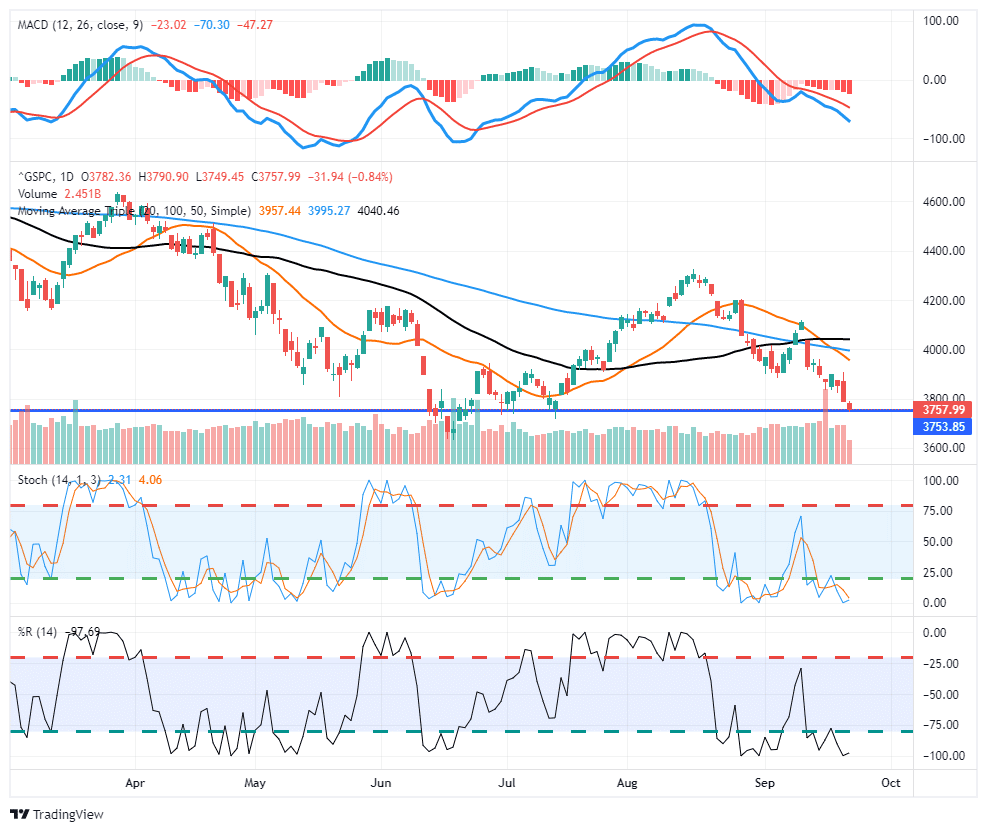

Market Trading Update

Markets sank again yesterday following the Fed’s more aggressive stance and signaled that “no pivot” in policy is coming. Such disappointed the markets in desperate need of some “encouraging news,” but none was to be had. The Fed slashed economic growth drastically, upped their unemployment projections, and kept inflation expectations at high levels through next year.

With markets sitting on the last level of support above this year’s lows, the oversold conditions could provide a relief rally short-term. However, there is little to get excited about currently. We will likely cut equity exposure levels on the next rally to even lower levels heading into the end of the year.

Keep a watch on the MACD signal (top of the chart), as it will provide the best guidance for a more sustainable rally near term.

Bank of England Follows the Fed

The Bank of England (BOE) followed the Fed’s footsteps and raised rates by 50bps to 2.25%. Further, they will be selling (QT) some of its bond holdings. They plan to reduce the balance sheet by about 10%, or £80 billion, over the next year. While much smaller than the Fed’s $95 billion a month, their actions are similar as a percentage of the balance sheet.

The Swiss, Taiwanese, and Norwegian central banks also raised rates yesterday. As you may recall, the ECB increased rates by 75bps two weeks ago. As the world’s central bankers finally start to take the fight against inflation seriously, dollar strength should run into a headwind.

The dollar rose in part this year because the Fed was aggressively raising rates while the other central banks did nothing. Not only did Fed actions cause higher interest rates for dollar investments, but they also reduced the odds inflation would become a bigger problem. With other central banks finally taking action and the Fed starting to near their terminal rate, dollar appreciation may slow or even reverse. However, the dollar is the world reserve currency and often a safe harbor when financial instability occurs. Higher interest rates often result in financial difficulties. As such, the dollar may rise further even if other central banks are on par with the Fed’s fight against inflation.

Happy Anniversary Plaza Accord

It’s fitting Japan chose September 22 to intervene in the currency markets. On September 22, 1985, the world’s largest economic forces signed the Plaza Accord. The Plaza Accord was a joint–agreement signed at the Plaza Hotel in New York City. At that time, France, West Germany, Japan, the UK, and the U.S., agreed to depreciate the dollar versus the currencies of the aforementioned nations.

The graph below shows the incredible dollar appreciation leading to the accord. Equally stunning is dollar depreciation following the signing of the Plaza Accord. From 1980 to September 1985, the dollar index rose from $95 to $165, or about 70%. Over the last two years, the dollar has appreciated by about 25%. While today’s appreciation pales in comparison to 1985, the amount of debt and leverage in the global economy is significantly higher now. As such, the effect of the recent appreciation may be much more akin to the early 80s than it appears.

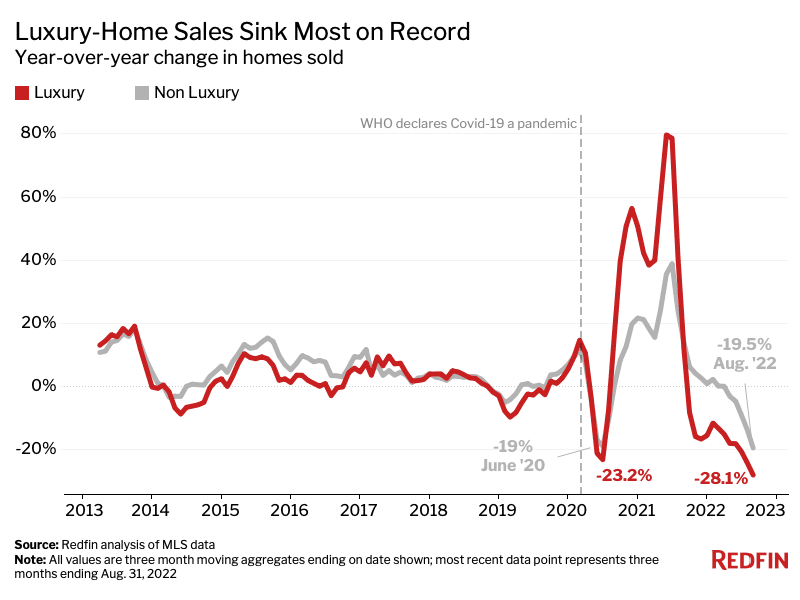

Luxury Home Sales Plummet

A recent RedFin report states: “luxury-home purchases plummet 28%, the biggest drop on record.” Higher mortgage rates, inflation, and falling stock prices are weighing on high-end home purchases. Per the report:

High-end-house hunters are getting sticker shock when they see the impact of rising mortgage rates on paper. For a luxury buyer, a higher interest rate can equate to a monthly housing bill that’s thousands of dollars more expensive,” Fairweather said. “Someone who was in the market for a $1.5 million home last year may now have a maximum budget of $800,000 thanks to higher mortgage rates. Luxury goods are often the first thing to get cut when uncertain times force people to reexamine their finances.

While sales plummet, prices have yet to fall. We suspect that will change in the coming months.

Home sales: Luxury home sales fell in all top 50 metros. The biggest declines were in Oakland, CA (-63.9% YoY), San Jose, CA (-59.6%), Miami (-55.5%), San Diego (-55.3%) and Seattle (-52%). The smallest decreases were in Indianapolis (-7.5%), Kansas City, MO (-10.4%), Columbus, OH (-11.4%), New York (-11.8%) and Boston (-14.7%).

Prices: The median sale price of luxury homes rose in all top 50 metros, with the largest gains in Florida. It was up the most in Tampa (39.3% YoY), West Palm Beach (34.2%), Jacksonville (30.5%), Orlando (29.6%) and Fort Lauderdale (28%). It climbed the least in St. Louis (3.5%), New York (4%), Washington, D.C. (6.7%), Nassau County, NY (7.8%) and Portland, OR (8.4%).

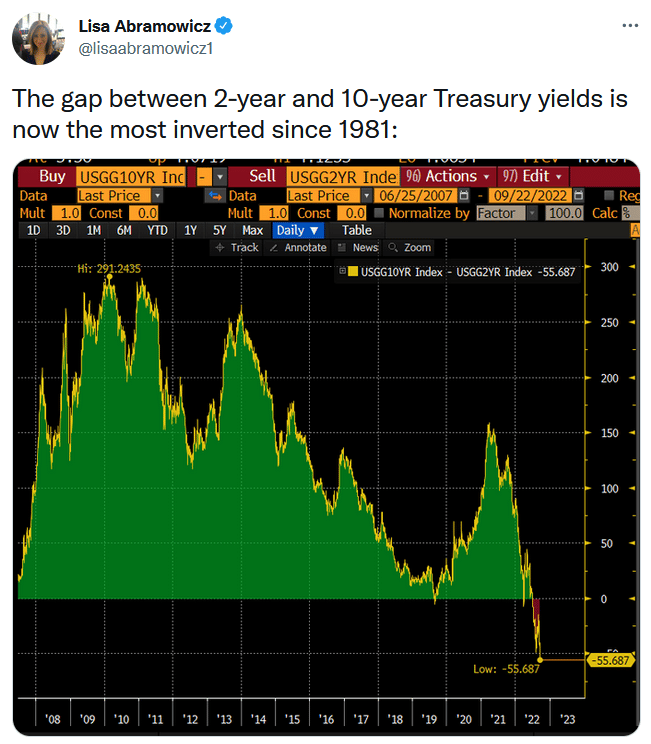

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.