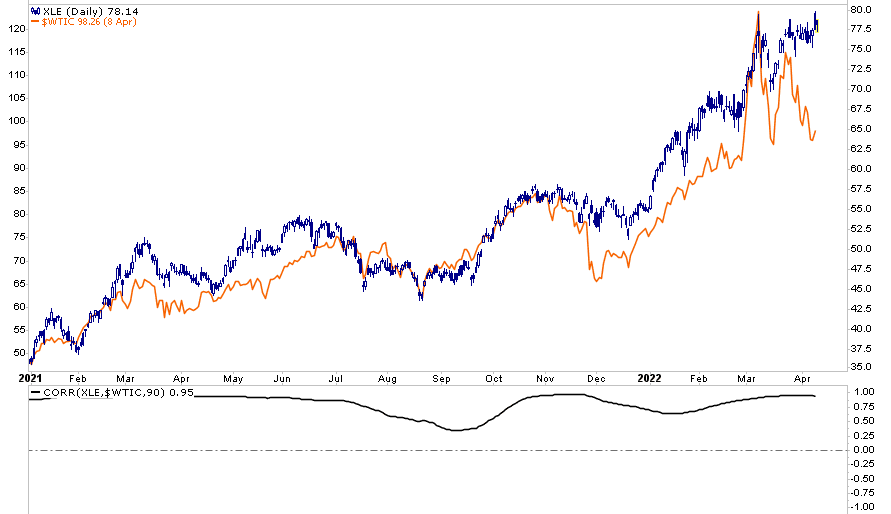

Within today’s Commentary, we point out a few concerning market divergences. We lead with the split between energy stocks (XLE), which are at all-time highs, and the price of crude oil, which is almost 25% off recent highs. As shown in the lower graph, the correlation between energy stocks and crude oil is not perfect but statistically robust. The price divergence will close in time. The question is how. Recent weakness in crude oil may portend a growing recessionary mindset among investors. If a recessionary bias continues, we think energy stocks will likely fall back in line with crude oil. Over the last 90 trading days, energy stocks have beaten the S&P 500 by 45%. After such an unusual move, a period of underwhelming performance for energy stocks should be expected.

[dmc]

What To Watch Today

Economy

- 8:30 a.m. ET: NFIB Small Business Optimism, March (95.0 expected, 95.7 during prior month)

- 8:30 a.m. ET: Consumer Price Index, month-over-month, March (1.2% expected, 0.8% during prior month)

- 8:30 a.m. ET: CPI excluding food and energy, month-over-month, March (0.5% expected, 0.5% during prior month)

- 8:30 a.m. ET: CPI year-over-year, March (8.4% expected, 7.9% during prior month)

- 8:30 a.m. ET: CPI excluding food and energy, year-over-year, March (6.6% expected, 6.4% during prior month)

- 8:30 a.m. ET: CPI Index NSA, March (287.413 expected, 283.716 during prior month)

- 8:30 a.m. ET: CPI Core Index SA, March (289.188 expected, 287.878 during prior month)

- 8:30 a.m. ET: Real Average Hourly Earnings, year-over-year, March (-2.6% prior, revised to -2.5%)

- 8:30 a.m. ET: Real Average Weekly Earnings, year-over-year, March (-2.3% prior, revised to -2.2%)

- 2:00 p.m. ET: Monthly Budget Statement (-185.5 billion expected, -$216.6 billion prior)

Earnings

- Albertsons (ACI) to report adjusted earnings of $0.65 on revenue of $16.9 billion

- CarMax (KMX) to report adjusted earnings of $1.32 on revenue of $7.4 billion

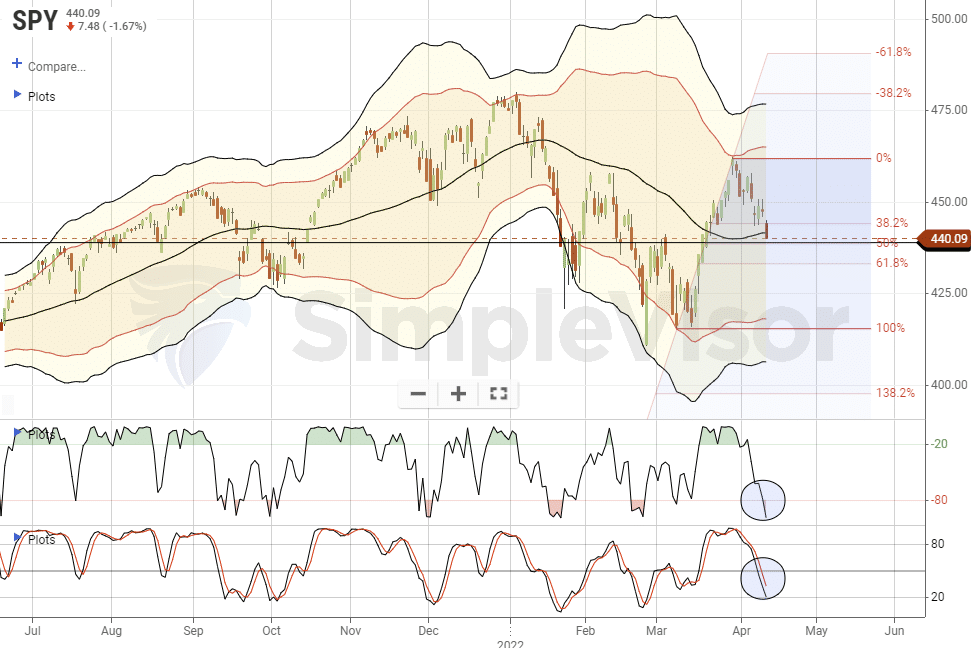

Market Trading Update – S&P 500 Violates Support

Yesterday was a rough start to a holiday-shortened trading week. The good news, if you want to call it that, is the market is now very oversold on a short-term basis AND has completed a 50% retracement of the recent rally. The bad news, is the market violated the 50-dma, so it needs to rally tomorrow or Wednesday back above it or we will likely start to retrace to the recent lows.

Energy and Technology were the most under pressure, but there was a lot of red across the market.

Given that Friday is a holiday, options expiration will be on Thursday this week, so a pick up in volatility on light volume will not be surprising. That light volume, short trading week, is also notorious for whipsawing traders when the action picks up next week. So be cautious reading too much into the market action this week.

Bonds Are A Screaming Buy – Which Is Why Everyone Hates Them

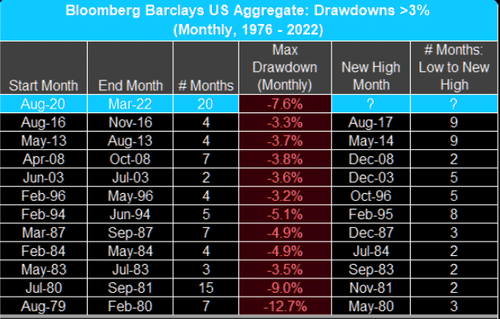

“The 10-year has seen its largest weekly increase in yield since the week Trump was elected in 2016. The 2s10s yield curve has steepened by 27 bps this week. It hasn’t steepened that much in a week since 2013. (Bespoke)

This is the longest US bond market drawdown in history. At 20 months and counting. It is also the largest (-7.6%) since 1981. In 1981 the 10-year yield was at 15.8%, and the bond market hit a new high 2 months after bottoming. Today it’s at 2.7%.” – @TheMarketEar

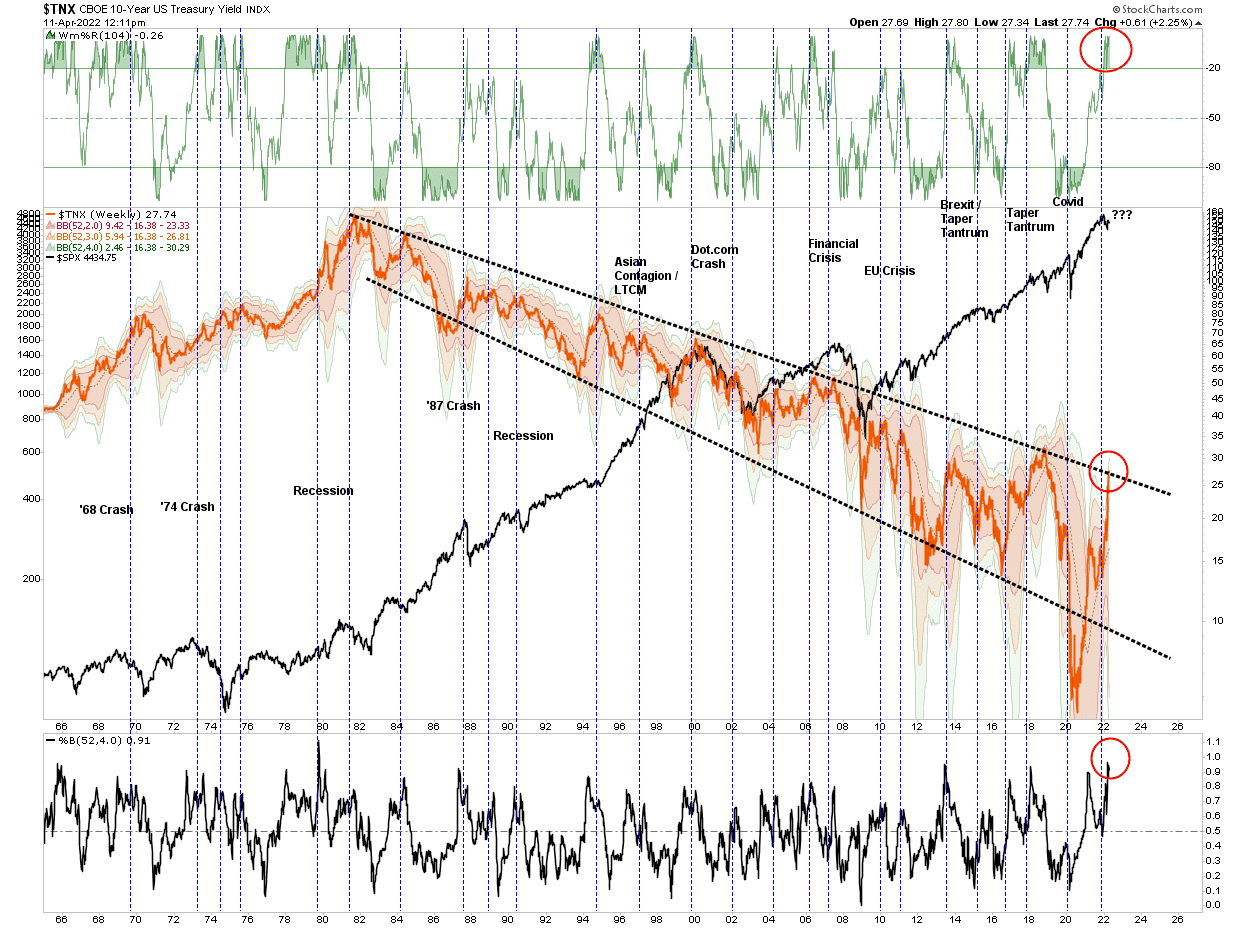

As shown, the 10-year yield has fully retraced to the top of the long-term downtrend line. The yield is currently 4-standard deviations above the 52-week moving average and is massively overbought on a long-term basis. As the vertical blue lines show, at every coincident point in history yields were near a peak which almost always coincides with a recession, bear market, or worse.

Of course, it is always possible this time could be different. It just never has been previously.

S&P 500 Sector Dispersion Beneath The Surface

The S&P 500 is down about 7% for the year to date. Beneath the surface, plenty of stocks are doing much worse than the index, and some are doing better. The table below breaks out the 12 S&P 500 sectors and shows their excess returns (vs. S&P 500) over various time frames. The shading helps identify which sectors out or underperformed in each time segment. As shown, in the 10 day period, the value/conservative sectors like staples (XLP), utilities (XLU), and healthcare (XLV) are outperforming. On the other hand, transportation stocks (XTN) are grossly underperforming the broader market. The sector dispersion gives the appearance that investors are bracing for a recession.

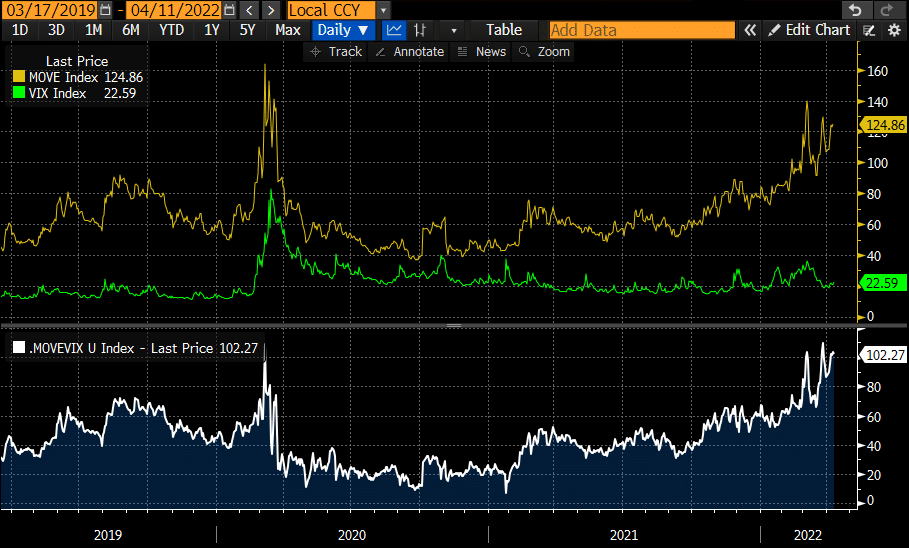

Stocks or Bonds? Whose Got It Right?

As we share below, implied volatility in the S&P 500 (VIX) has been relatively mild compared to the implied volatility in bonds (MOVE index). The difference between the two is now the largest in at least three years, surpassing the early days of the pandemic. Bond investors are clearly concerned about the future outlook, while stock investors are more complacent. Will stock volatility rise to close the gap, or will bond volatility fall? That is an important stock/bond allocation question to keep top of mind. We believe bonds are due for a bounce which should reduce volatility.

Possible Massive Head and Shoulders Pattern- Japanese Yen

There are quite a few divergences and concerning movements in many asset markets. We share another one in the graph below. The Japanese yen is now trading at six-year lows and is down about 20% in just the last year and a few months. Yen depreciation is likely a function of their central bank. The Bank of Japan (BOJ) continues to perform QE to keep interest rates capped. At the same time, most other central banks are raising rates and reducing their balance sheets due to inflation.

The value of the yen presents a lot more than an economic issue for Japan and its trade partners. The yen is an important currency used to fund many carry trades. As such, and the topic for an upcoming article, the value of the yen matters. The graph below bears watching. One can interpret the pattern as a head and shoulders. If so, a break below the red line suggests a significant decline lies ahead. However, a bounce from crucial support might force the unwinding of many carry trades. These carry trades prop up asset prices in many markets.

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.