The hard asset, commodity, trade has sprung to life over the last couple of months. Such is commensurate, and logical, with the surge in inflation. However, is the hard asset trade a sustainable one? Or is it a trap that will disappoint investors in the years to come?

When it comes to the commodity, or hard asset, trade, it is usually avoided by the mainstream media. They would rather focus on whatever “hot stock” or investment meme is leading the market at the time. However, from “gold bugs” to “oil traders,” the commodity trade is a source of booms and busts along the way.

For our analysis, we are going to focus on the CRB Commodity Index as a proxy for commodities. From the index, we can then explore how the dollar, interest rates, economic growth, and inflation drive commodity prices.

Is the commodity trade is here to stay, or is this another “boom” waiting to “bust.”

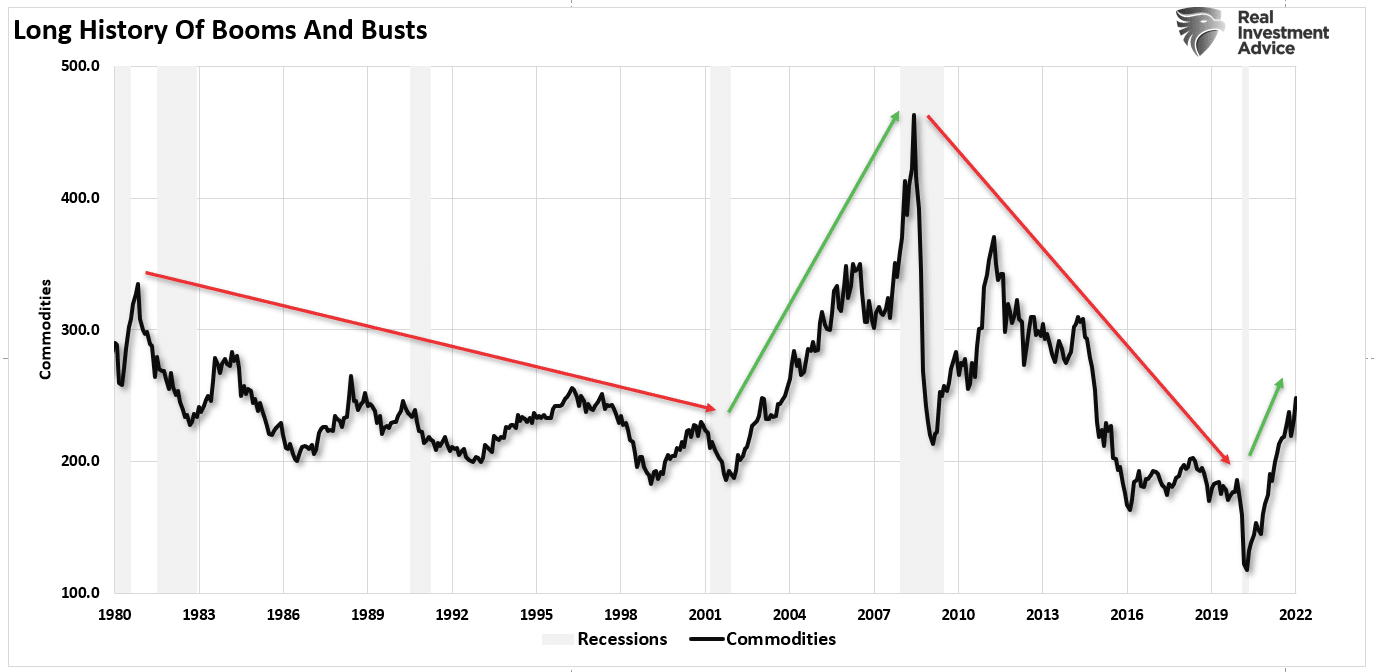

A Long History Of Booms And Busts

Since 1980, the start of my data feed for the CRB Index, there have been 4-distinct cycles in commodities.

From 1980 to 2000, the trend of commodity prices fell as the economy shifted from manufacturing to financialization. Beginning in 2001, as the dot.com era came to an end, investment flows shifted to commodities and emerging markets in anticipation of a global resurgence. Housing demand boomed as mortgage rates fell, and energy demand rose on fears of “peak oil production.”

However, as quickly as it came, the demand for commodities faded as the financial crisis crippled the entire global economy. That deflationary trend continued until March 2020. As the Covid-pandemic locked down economies, governments injected billions of dollars to stimulate demand. Not surprisingly, inflation surged and demand for inflation protection in the form of commodities rose.

Since the demand-side of the equation was driven by artificial liquidity, the question is now the sustainability of higher prices?

To answer that question, we must understand that commodities, and hard assets in general, do not live in a vacuum. Rather, they are very subject to the supply-demand equation which ultimately sets their price. Therefore, and not surprisingly, economic growth, interest rates, the dollar, and the money supply weigh heavily on that equation.

A review of those factors, relating directly to inflation is useful in determining the current trend of rising commodity prices. Or, whether deflation is a bigger threat.

All lndicators Suggest Commodity Run Is Limited

If commodities, and hard assets, are driven by demand, particularly in manufacturing, then there are several indicators pointing to the ongoing demand for those assets.

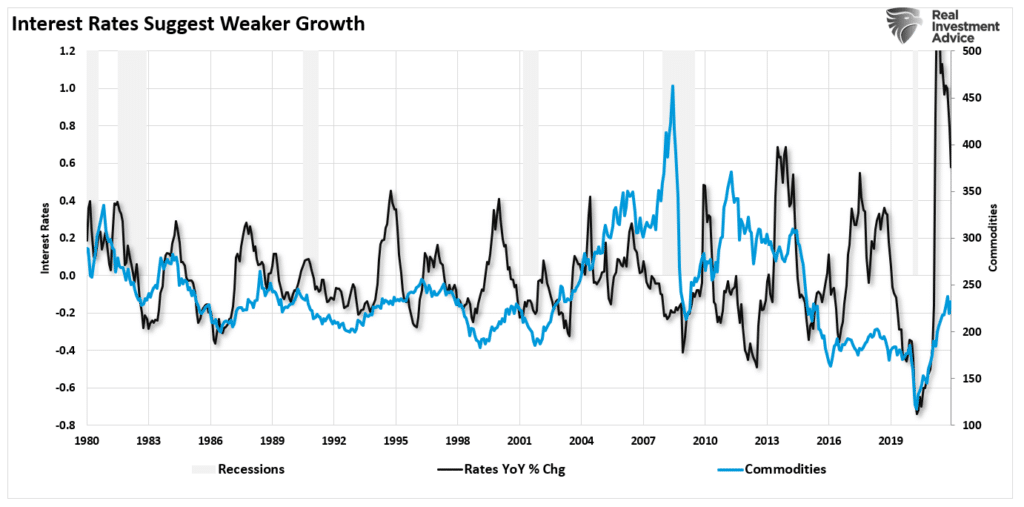

Interest rates are important as rates reflect the strength of economic growth, inflation, wages, and overall demand. There is a decent correlation between the annual change in interest rates (reflecting economic strength or weakness) and commodity prices.

Not surprisingly, the recent surge in commodity prices, from the 2020 lows, corresponds with the jump in rates. Such corresponds with the flood of fiscal policy allowing demand to outpace the economic production capacity. However, with the liquidity now reversed, rates are reversing to levels consistent with weaker economic growth rates.

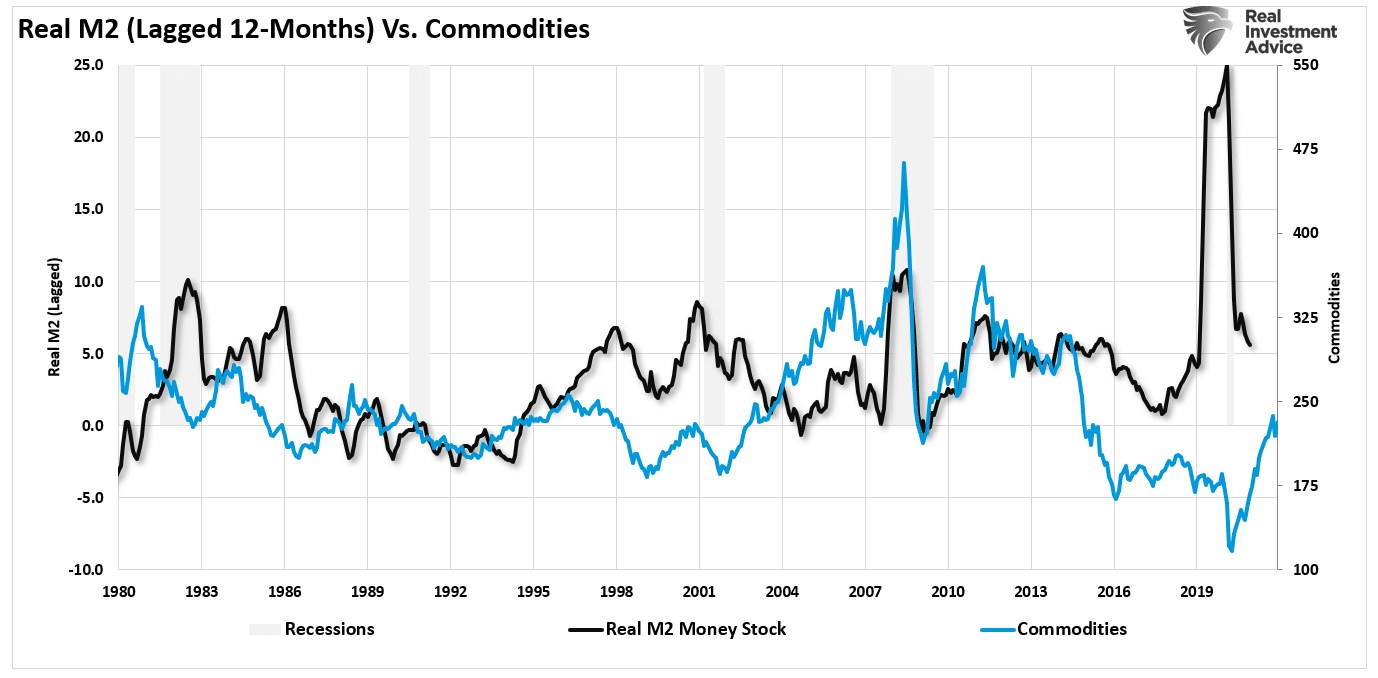

A consequence of that reversal in liquidity, as measured through M2, is the reversal of inflation over the next 9-months. Again, since commodities are highly correlated to inflation, it suggests the peak in the “hard asset” trade as the economy normalizes.

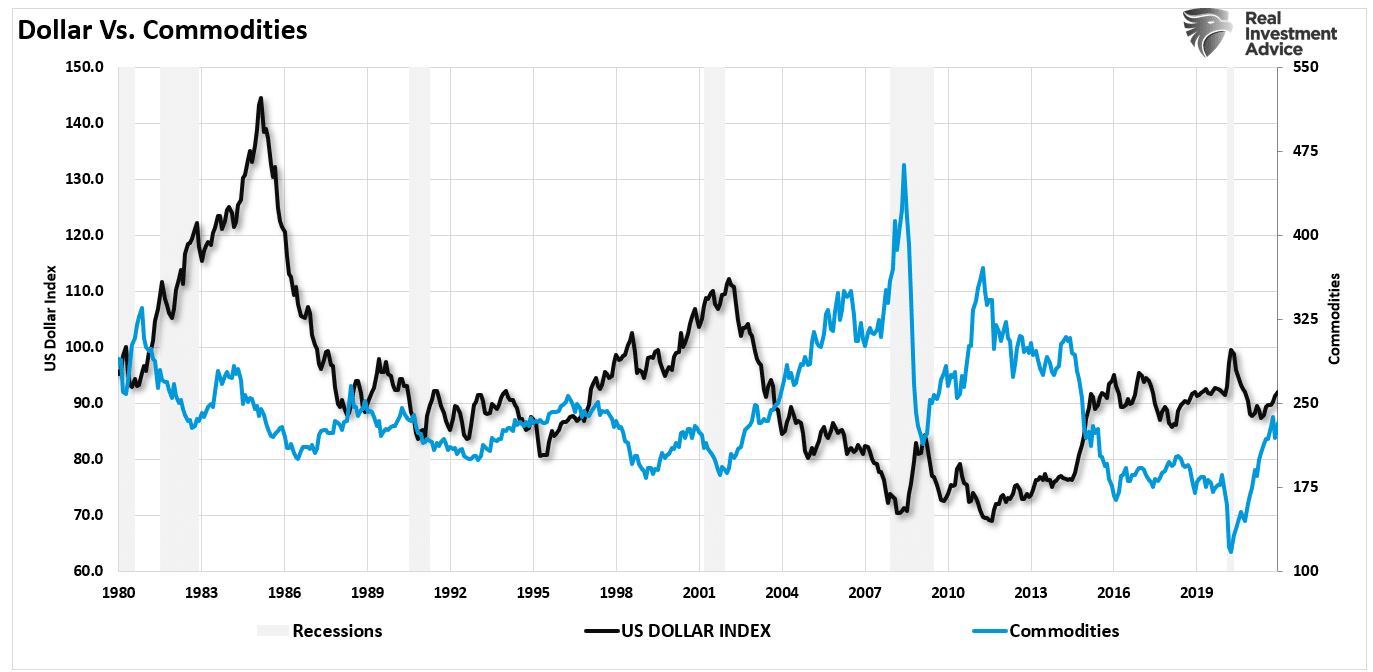

Lastly, commodities, and hard assets in general, trade globally in U.S. dollars, and the trend and direction of the currency are important. As the dollar strengthens, such makes commodities more expensive for our foreign partners. A weaker dollar allows U.S. consumers to buy more increasing demand. Such explains why there is an inverse correlation between the dollar and commodities.

Where the dollar goes next will largely depend on the relative strength of the U.S. economy to the rest of the world. We suspect that while the U.S. economy will weaken in the months ahead, the rest of the globe will be worse. The U.S. has, and will likely remain, the “cleanest shirt in the dirty laundry.”

It’s The Economy, Stupid

While interest rates, inflation, money supply, and the dollar can give us clues about the commodity and hard asset trade, in the end it really is “the economy, stupid.”

As stated above, all commodity and hard asset prices are ultimately set by supply and demand. If the economy is strong, then demand for finished goods, real estate, housing, autos, etc., will be strong. The strength of that demand will increase production increasing the demand for raw materials. If the economy weakens, that demand falls leading to an inventory glut and a fall in prices. Not surprisingly, commodities track nominal GDP growth.

The surge in economic growth following the pandemic-driven shutdown was, as stated, an artificial “sugar rush” of liquidity flooding the system. Such caused a massive surge in money supply, leading to inflation given the lack of productive capacity. However, as is already the case, economic activity is reverting to its more normal levels.

“As the budget deficit grows over the next few years, interest payments alone will absorb a larger chunk of tax revenue. Such comes at a time when that same dollar of tax revenue only covers the entitlement spending of the 75-million baby boomers migrating into the social safety net.

By the way, the only other time government income support exceeded taxes paid was during the “Great Depression” from 1931 to 1936.

The debt problem remains a massive risk to monetary and fiscal policy. If rates rise, the negative impact on an indebted economy quickly depresses activity. More importantly, the decline in monetary velocity clearly shows that deflation is a persistent threat.

The last sentence is the most important when it comes to hard assets.

The Hard Asset Trade Tends To End Badly

When it comes to commodities and hard assets in general, they can be an exhilarating and profitable ride on the way up. However, as shown in the long-term chart above, that trade tends to end badly.

Will this time be different? Such is unlikely to be the case for two reasons.

As shown by Goldman Sachs, inflation will reverse later this year.

Secondly, as the country moves toward a more socialistic profile, economic growth will remain constrained to 2% or less with deflation remaining a consistent long-term threat. Dr. Lacy Hunt suggests the same.

Contrary to conventional wisdom, disinflation is more likely than accelerating inflation. Since prices deflated in the second quarter of 2020, the annual inflation rate will move transitorily higher. Once these base effects are exhausted, cyclical, structural, and monetary considerations suggest that the inflation rate will moderate lower by year-end and undershoot the Fed Reserve’s target of 2%. The inflationary psychosis that has gripped the bond market will fade away in the face of such persistent disinflation.

As he concludes:

The two main structural impediments to traditional U.S. and global economic growth are massive debt overhang and deteriorating demographics both having worsened as a consequence of 2020.

The last point is crucial. As the liquidity gets removed from the system, the debt overhang will weigh on consumption as incomes are diverted from productive activity to debt service. As such, the demand for commodities will weaken.

Let me conclude with this point from Michael Lebowitz:

The multitude of dynamics that determine commodity prices means there are no quick and easy answers to determining an effective strategy.

While the commodity trade is certainly “in bloom” with the surge in liquidity, be careful of its eventual reversal.

For investors, deflation remains a “trap in the making” for hard assets.