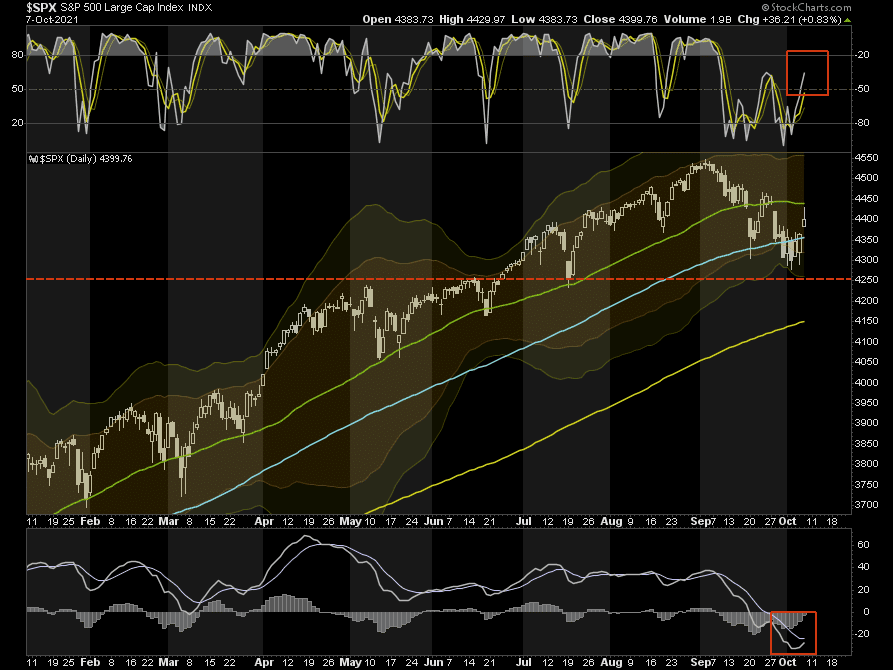

After Wednesday’s impressive rebound the bulls are regaining confidence and attempted a run for the 50-dma yesterday. With control back in their hands, the first big test will be getting the ball past the 50-dma for an attempt at the “end zone” of all-time highs. The bears will likely set us a strong defensive front at the 50-dma, leading to a battle royale for market control in the coming days. Today’s BLS unemployment report may play a big role in picking the winner of this battle.

This morning futures are flattish (at the time of this writing) as we await the employment report at 7:30 am this morning. Will the report be strong enough to cement the Fed’s “taper” decision in November? Or, will a weak report potentially put a pause on the reduction of liquidity? For the markets, this could be bad news is good news if a poor jobs report keeps the “punch bowl” full.

[dmc]

What To Watch Today

Economy

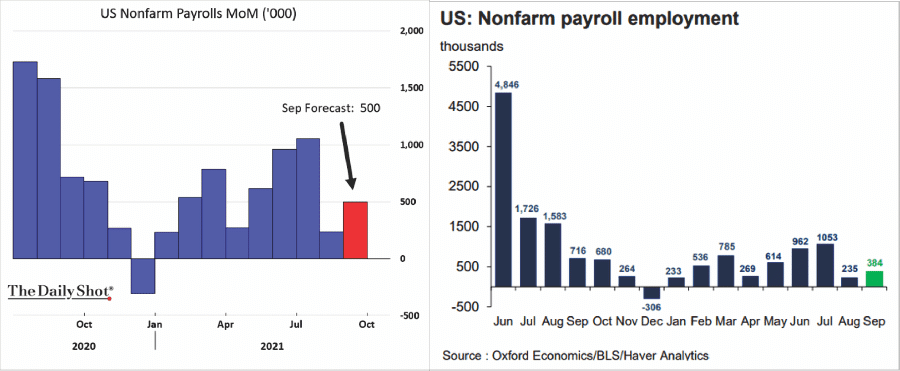

- 8:30 a.m. ET: Change in non-farm payrolls, September (500,000 expected, 235,000 in August)

- 8:30 a.m. ET: Unemployment rate, September (5.1% expected, 5.2% in August)

- 8:30 a.m. ET: Average hourly earnings, month-over-month, September (0.4% expected, 0.6% in August)

- 8:30 a.m. ET: Average hourly earnings, year-over-year, September (4.6% expected, 4.3% in August)

- 8:30 a.m. ET: Labor force participation rate, September (61.7% in August)

- 10:00 a.m. ET: Wholesale inventories, month-over-month, August final (1.2% expected, 1.2% in prior estimate)

Earnings

- No notable reports scheduled for release

Politics

- The debt-ceiling expansion passed by the Senate last night goes to the U.S. House of Representatives, which is expected to vote on the measure Tuesday. Eleven Republican Senators, including Senate Minority Leader Mitch McConnell, voted yes to push the bill past the 60 vote limit filibuster to make it to the simple-majority vote for passage. The Senate voted 50-48 to pass the bill that temporarily averts default.

Courtesy of Yahoo

A Run For The 50-dma

As noted, the market cleared the all-important hurdle of the 100-dma resistance level yesterday and made an initial attempt at the 50-dma. However, such proved to be “too far, too fast” for the bulls. The key is with the markets not yet overbought, and the MACD signal still on a sell signal, but improving, that the 100-dma holds and becomes support.

With earnings season approaching, the bulls have their work cut out for them. Risk is elevated, so we still consider this rally a counter-trend bounce until the 50-dma is taken out.

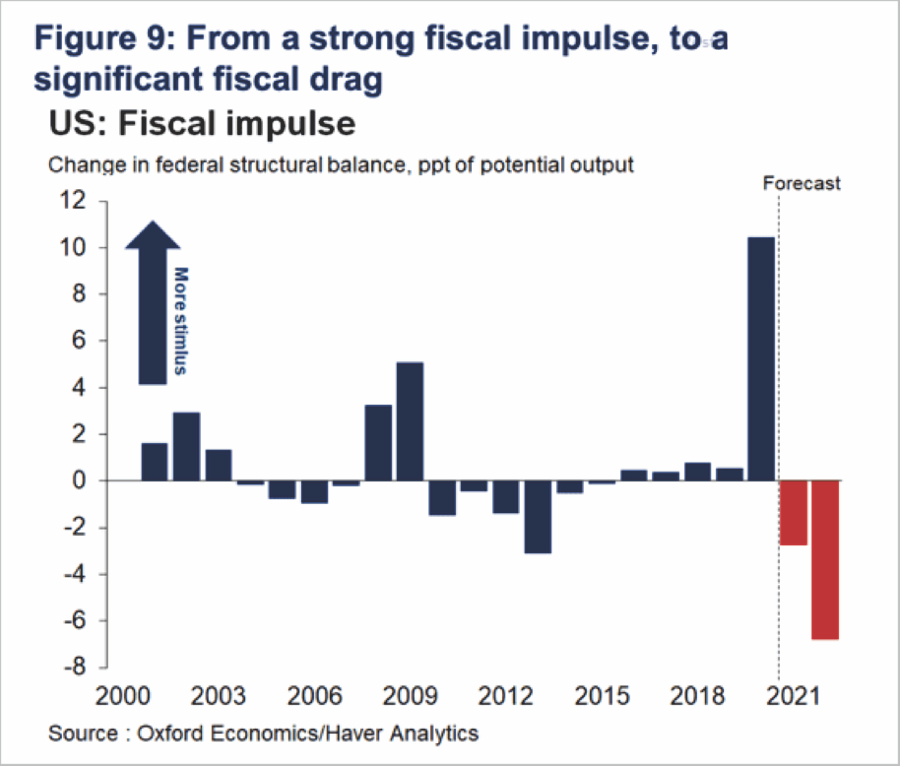

The concerns over the next several months are several.

- Economic growth is slowing fast.

- Earnings and revenue are tied to economic growth which puts equities at risk.

- The fiscal drag is become much more prevalent.

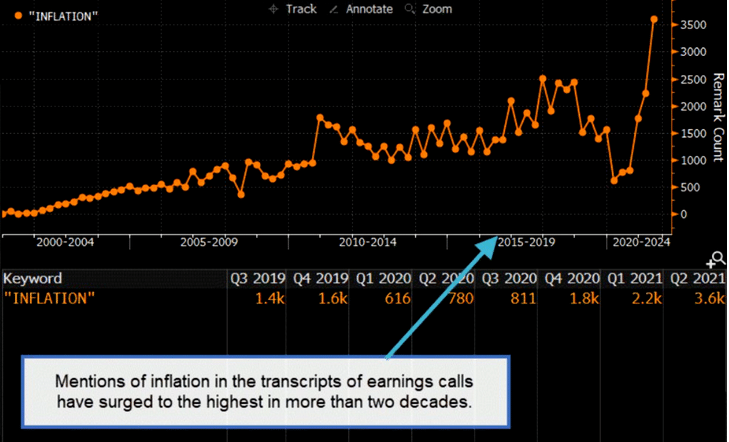

“Inflation” is Coming Next Week

The graph below, courtesy of the Market Ear, shows how mentions of inflation are a hot topic for earnings calls. As we gear up for another round of earnings releases starting in earnest next week, there is little doubt the number of “inflation” mentions will increase further. The question facing shareholders is how well can companies deal with inflation? Can they take advantage of higher prices or will they negatively impact profit margins? Each company and industry has different factors to consider that will help answer those questions.

From a macro perspective, we will also learn a good deal about expectations for continued inflation in the coming quarters. The Fed speaks with executives at many large companies, so this information will also help us better assess our outlook on the potential pace at which the Fed tapers QE.

Jobless Claims

Following yesterday’s strong ADP report, the labor market showed more improvement. Weekly Initial Jobless Claims fell back toward a post-covid low of 326K. This was below expectations of 348k and well below last week’s 364k.

Market Rise On Debt Ceiling Increase

St. Louis Fed Expects an Ugly Jobs Report While JPM is Optimistic

Per Market News (MNI), the St. Louis Federal Reserve expects to see an 818k decline in tomorrow’s BLS payrolls report. St. Louis Fed economist Max Dvorkin states: “There’s still “a lot of uncertainty around these figures,” but the model has tracked actual CPS employment “quite well” through the summer, he said.” He blames the recent uptick in Covid cases and the impact on global supply lines. The current forecast is for a gain of 410k jobs. If the Fed’s forecast is proven correct the Fed might delay what appears to be a tapering announcement in early November.

On the other hand, JP Morgan is optimistic “we are looking for a 575,000 gain in jobs and a drop in the US unemployment rate to 5%. The driver for an above-consensus forecast is the expected rebound in the leisure and hospitality sectors.”

Our expectations are roughly in line with JPM in that we will see a seasonal adjustment boost to the employment report which could make it look stronger than reality.

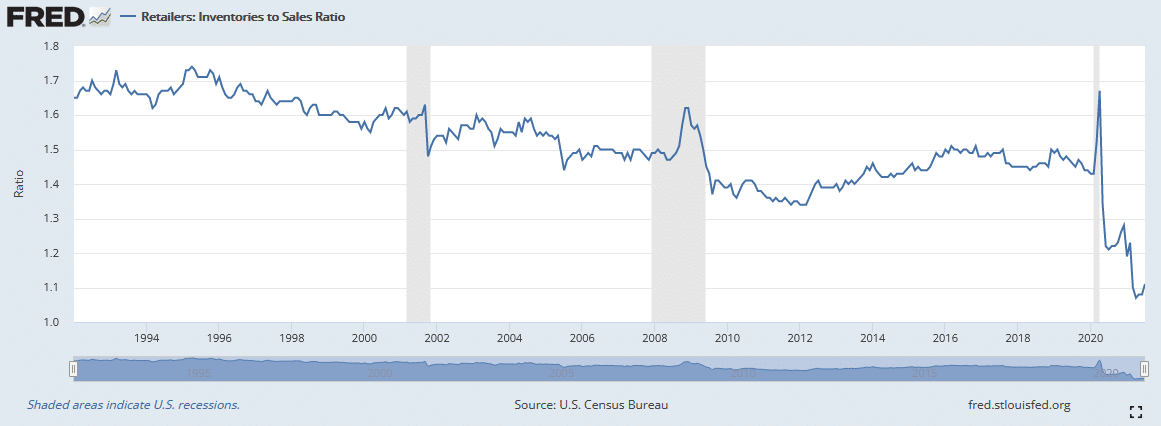

Retail Inventories are Low

Price pressures, especially on retail goods, will likely continue into the holiday season. The graph below shows the ratio of Retailers’ inventories to sales is at a 25+ year low and well below pre-pandemic levels. Given there appears to be little let-up in supply line problems, it’s becoming increasingly probably that many retailers will not be able to fully stock their shelves to meet the heavy demand for Christmas presents. With, the limited inventory we suspect many stores, both online and brick and mortar, will be able to raise prices over the next few months.