In this issue of, “The Bullish Test Comes As Earnings Season Begins:”

- A Breakout Of Consolidation

- Updated Estimates As Earnings Begin

- A Quick Note On The Jobs Report

- Portfolio Positioning

- MacroView: The Fed Has Inflated Another Asset Bubble

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Upcoming Event – CANDID COFFEE

Sign up now for this virtual “Financial Q&A” GoTo Meeting

July 25th from 8-9 am

Send in your questions, and Rich and Danny will answer them live.

Catch Up On What You Missed Last Week

Note:

I am on vacation this week for a quick break. However, I did want to post a short market and portfolio positioning update.

If you have any questions, I will continue to answer every question, every day. That is between sleeping on the beach, fishing, skiing, or eating.

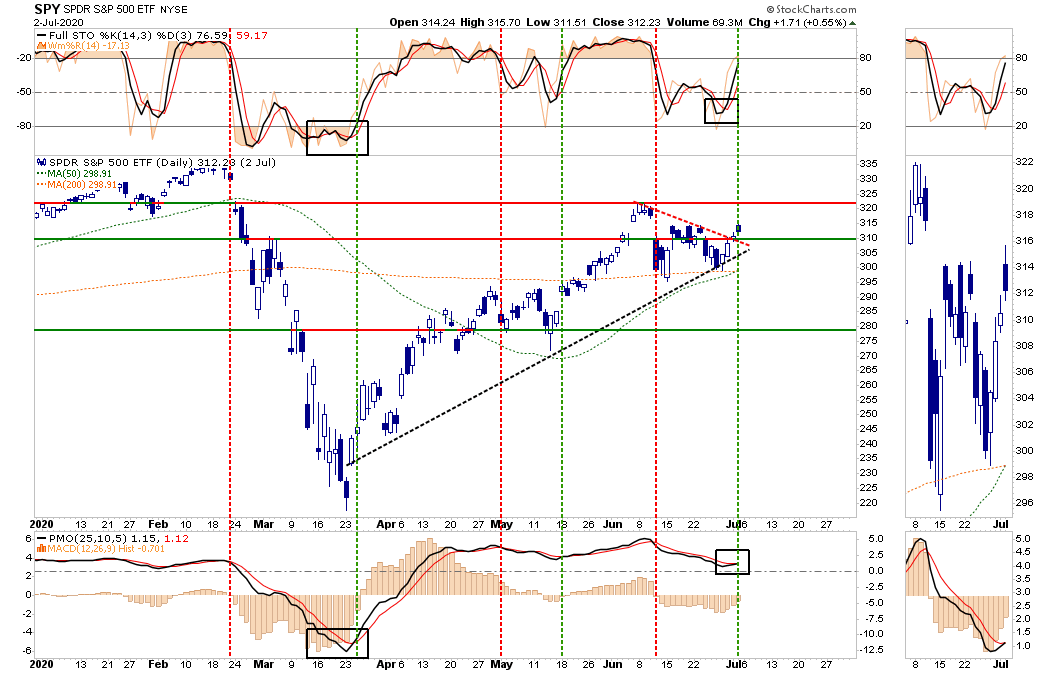

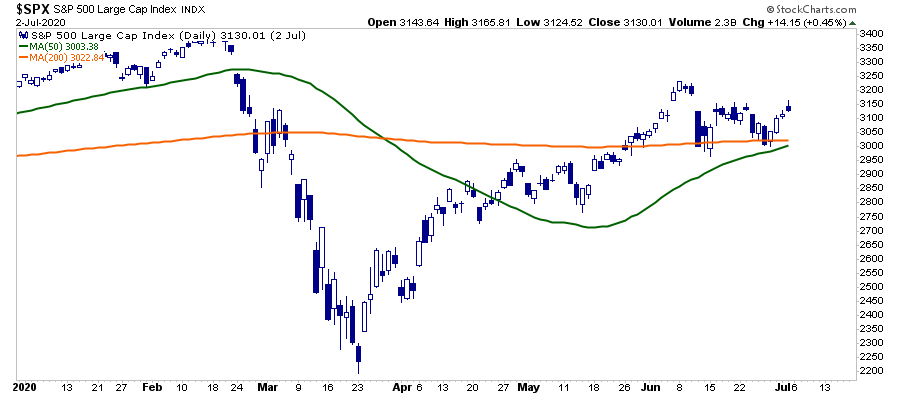

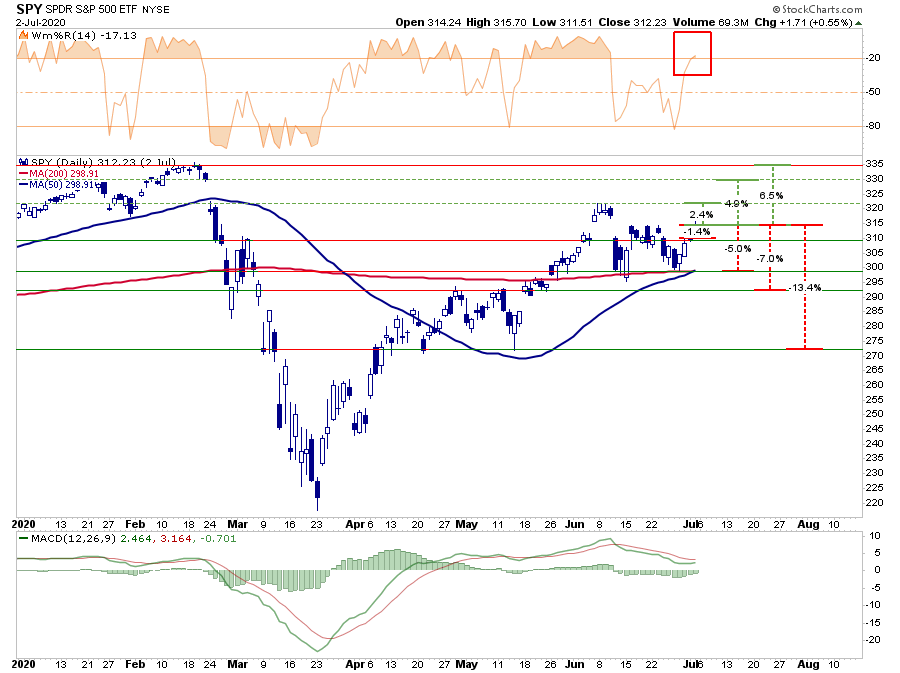

A Breakout Of Consolidation

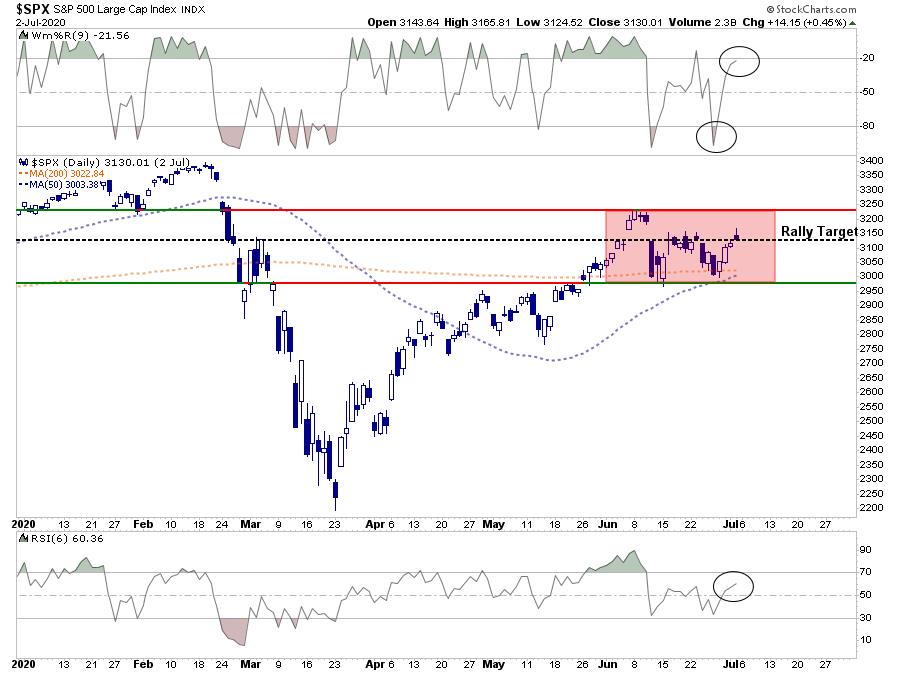

Over the last few week’s we have noted the continuing consolidation of the market since the June peak. When markets are overbought short-term, that condition is resolved through a correction or consolidation process. Such is what occurred during the last part of June and completed last week.

As shown below, the market broke out of that consolidation and triggered a “buy signals” across multiple measures. This breakout will give the “bulls” an advantage in the short-term with a retest of the June highs becoming highly probable.

The bulls will also gain some additional support from the “Golden Cross” (when the 50-dma crosses above the 200-dma). That “bullish signal” will likely occur over the next week or two depending on market action.

The “bullish supports” for the market are currently in play. Such keeps our portfolio allocations weighted towards equity risk. However, there are many fundamental and economic headwinds that could quickly derail the bullish thesis.

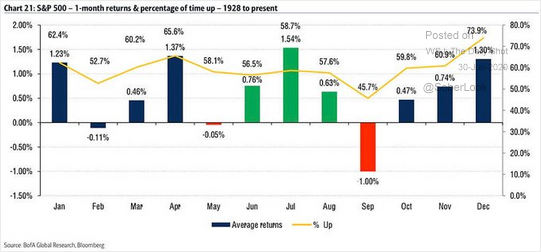

Seasonality In Play

In the short-term, the bulls remain in charge currently, and as such, we must be mindful of those trends. Also, the month of July tends to be one of the better performing months of the year.

“With the sell-off on Friday, the short-term oversold condition, a reflexive rally next week would not be surprising.”

That rally reversed much of the short-term oversold condition. While the bulls are in control of the market currently, the upside is somewhat limited. However, the downside risks are reduced with the improvement in the technical underpinnings. Such puts the risk/reward dynamics to a more equally balanced, than opportunistic, positioning. As such, risk controls and hedges should remain for now.

- -1.4% to breakout level vs. +2.4% previous rally peak. (Neutral)

- -5% to 50/200 dma support vs. +4.9% to January peak (Neutral)

- -7% to previous consolidation peak vs. +6.5% to all-time highs. (Neutral)

- -13.4% to previous consolidation lows vs. +6.5% to all-time highs. (Negative)

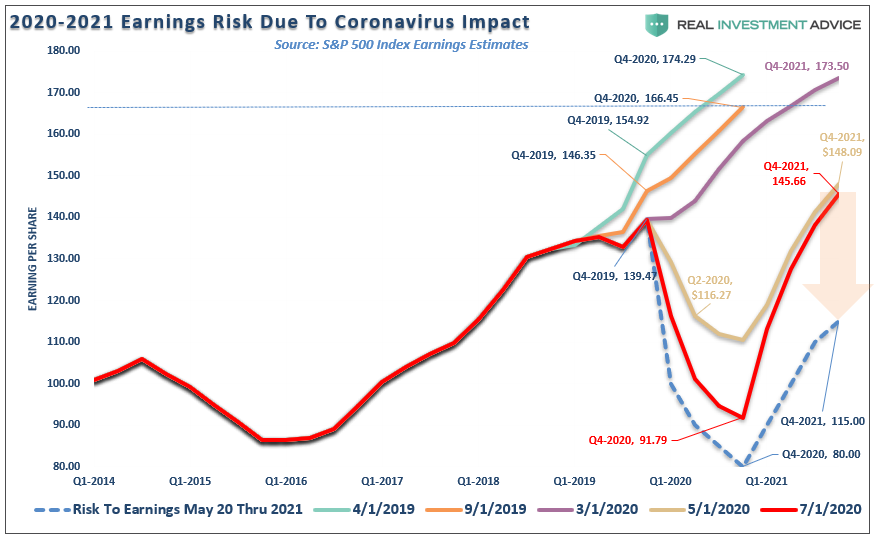

Earnings Estimates Update

Over the next two weeks, we will enter the earnings season for all publicly traded corporations. Of course, we will mostly hear about those companies which comprise the S&P 500 index. I am writing a more comprehensive report on the earnings estimates for Tuesday’s “Technically Speaking.” Still, I did want to make a quick comment about what is coming.

As with every quarter, we are about to play “Millennial Soccer.” Such is where Wall Street analysts continually lower earnings estimates for the quarter until companies can beat them. When you see the analysis that 70% of companies beat their estimates, just remember analysts lowered the bar to a point where “everybody gets a trophy.”

What will be important to pay attention to is “revenue,” which happens at the top of the income statement. Companies can do a lot to fudge bottom-line earnings by using accruals, “cookie jar” reserves, share buybacks, and a variety of other accounting gimmicks. It is much more difficult to manipulate revenue.

However, the market will focus on reported earnings. As stated, the estimates have fallen sharply over recent weeks, and are far lower than where they were set previously.

Importantly, while Wall Street has dramatically lowered estimates for the coming quarter, expectations remain for a rapid recovery in the economy. Given the rise in COVID-19 cases as of late, states pausing reopening, and depressionary levels of unemployment, it is highly likely those future estimates will ratchet sharply lower.

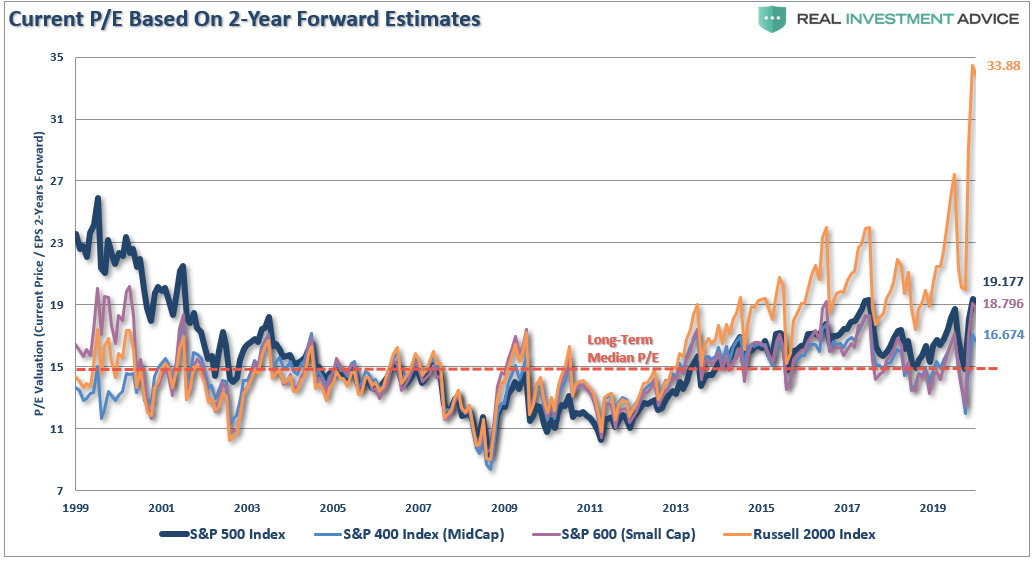

Such makes the mantra of using 24-month estimates to justify paying exceedingly high valuations today even riskier.

“Price is what you pay, value is what you get.” – Warren Buffett

A Quick Note On The Jobs Report

While the BLS reported a massive 4.8 million in employment for June and a drop in the unemployment rate to 11.1%, these numbers remain distorted by bad data gathering and analysis.

As Mish Shedlock noted on Thursday:

“I question both the strength of the rise in jobs and the decline in the unemployment rate based on claims data and the reference week.”

I agree.

It’s hard to reconcile a 4.8 million increase in jobs in a month where you added over 4-million to initial jobless claims and continuing claims continued to remain near the highest levels on record.

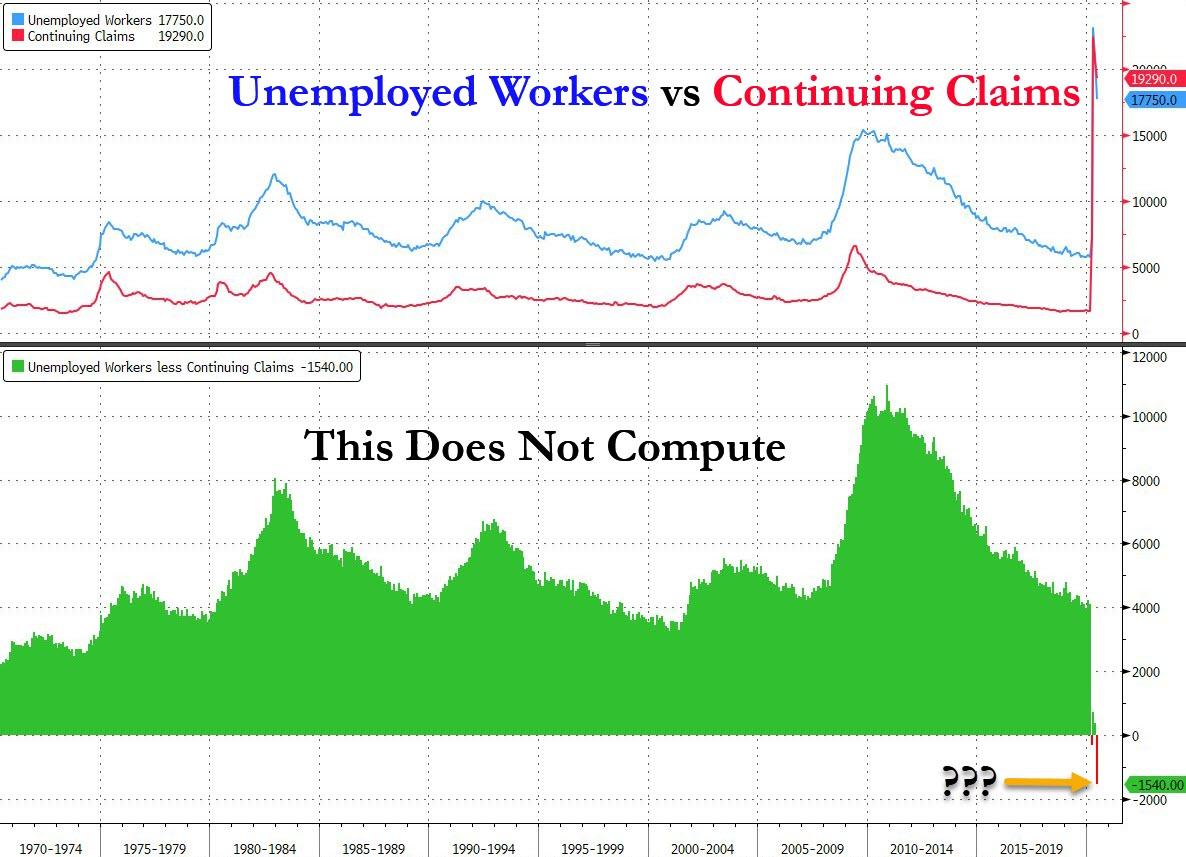

More importantly, as noted by Zerohedge, there is a problem in the data when you have more people getting unemployment benefits than there are unemployed workers.

“As the DOL reported today, there were 19.29 million workers receiving unemployment insurance. And yet, somehow, at the same time, the BLS also represented that the total number of unemployed workers is, drumroll, 17.75 million.

If you said this makes no sense, and pointed out that the unemployment insurance number has to be smaller than the total unemployed number, you are right. And indeed, for 50 years of data, that was precisely the case.”

The main point here is that employment is what drives earnings, corporate profits, and GDP. Given the exceedingly high level of unemployment, in real terms, the recovery to earnings will much slower than expected.

Such suggests that expectations for the bull market to continue “to infinity and beyond,” will likely prove disappointing.

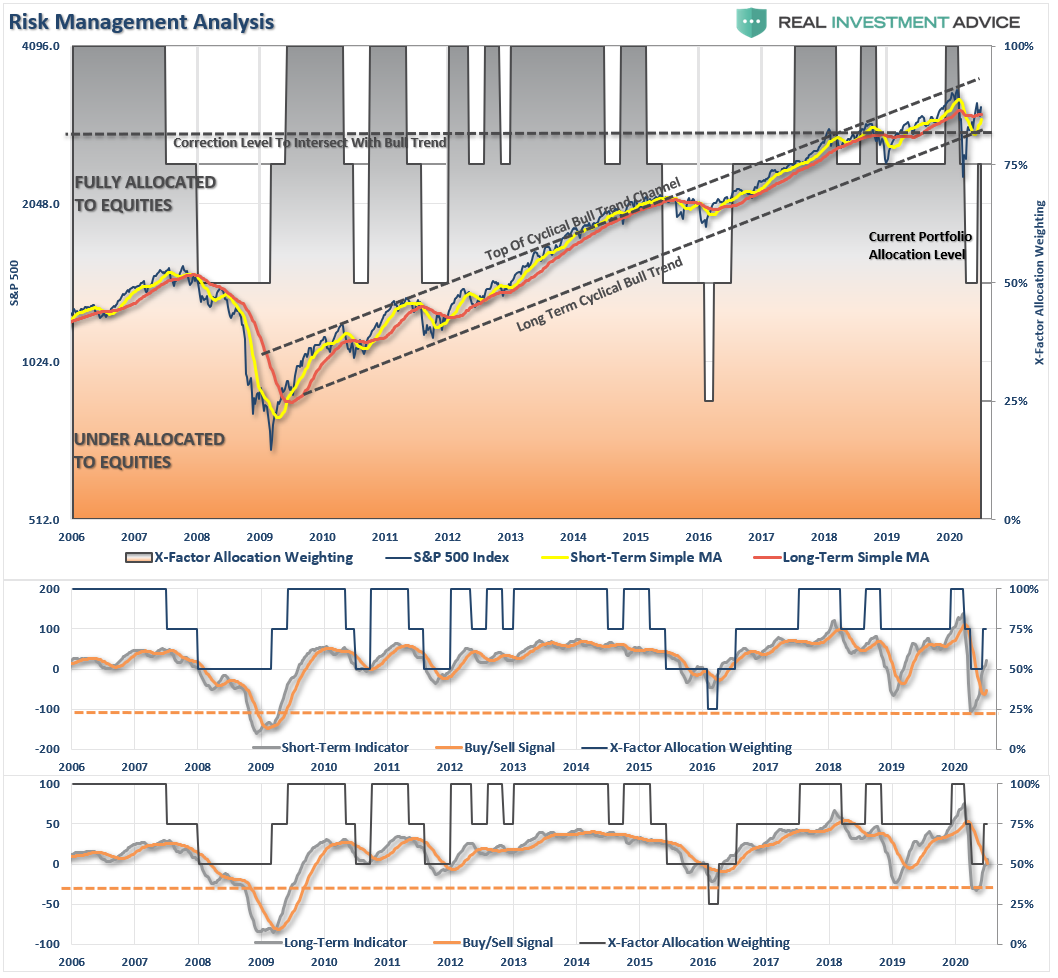

Portfolio Positioning Update

Let me restate our position from last week:

“With our portfolios almost entirely allocated towards equity risk in the short-term, we remain incredibly uncomfortable.”

Such remains the case this week.

As noted last week, with the market having gotten very oversold short-term, the reflexive rally off of support came as expected and achieved our first rally target.

Given that we are not yet to more extreme short-term overbought conditions and expectations of future earnings, the market can still retest the June highs.

As noted last week, we used the counter-trend bounce to rebalance exposures. We took profits in CLX and UPS and rebalanced our “core positions” by reducing DIA and adding SPY. Our focus remains on capital preservation for the next couple of months, so our hedges in fixed income remain.

With the virus resurfacing, the potential risk of disappointment to the earnings and economic recovery story has risen. Our job remains the same, protect our client’s capital, reduce risk, and try to come out on the other side in one piece.

While we are certainly more bullish on markets currently, as momentum is still in play, it doesn’t mean we aren’t keenly aware of the risk.

Pay attention to what you own, and how much risk you are taking to generate returns. Going forward, this market will likely have a nasty habit of biting you when you least expect it.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauge

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

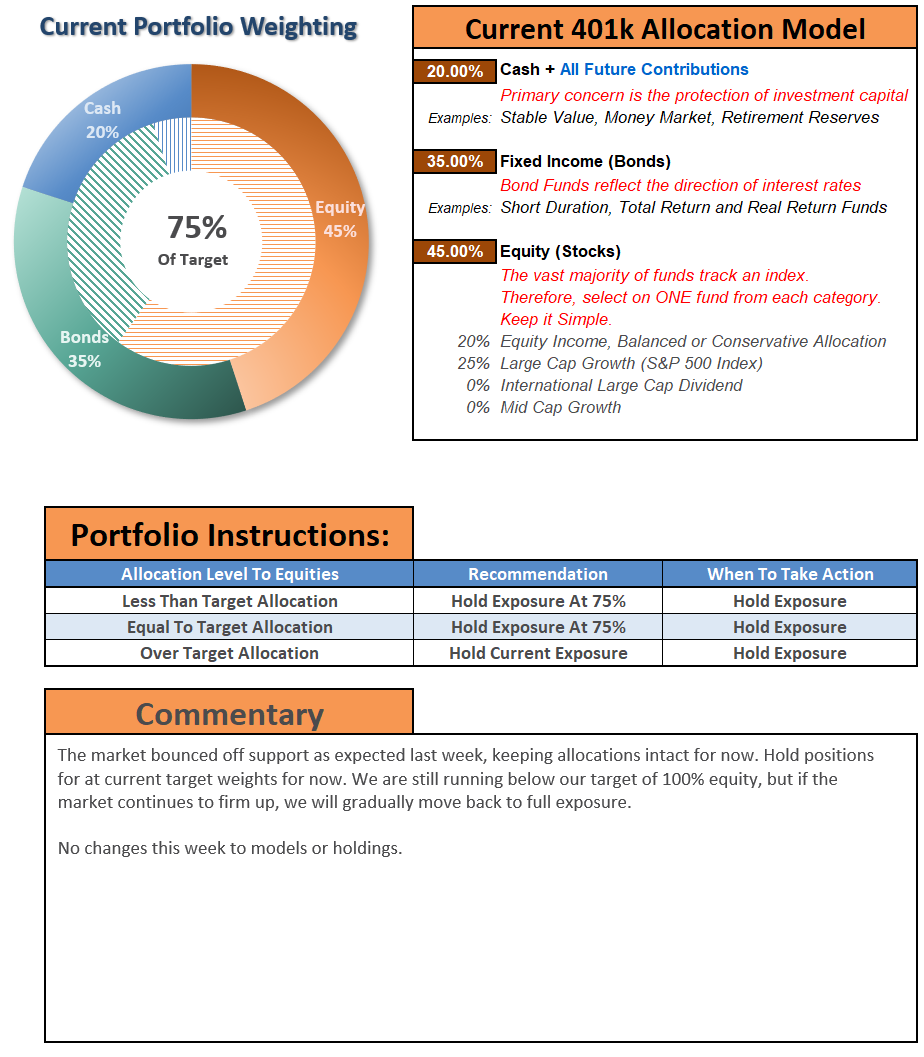

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert; do not hesitate to contact me

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only and should not be relied on for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k plan manager.

Compare your current 401k allocation, to our recommendation for your company-specific plan as well as our on 401k model allocation.

You can also track performance, estimate future values based on your savings and expected returns, and dig down into your sector and market allocations.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.