In this issue of “Market Breaks Above 200-DMA, Are All-Time Highs Next?”

- Market Breaks Above 200-DMA

- Are Bulls TOO Optimistic

- Technical Review

- Portfolio Positioning

- MacroView: CFNAI Crashes Most On Record,

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Upcoming Event – CANDID COFFEE

Sign up now for this virtual “Financial Q&A” GoTo Meeting

June 13th from 8-9 am

Send in your questions and Rich and Danny will answer them live.

Catch Up On What You Missed Last Week

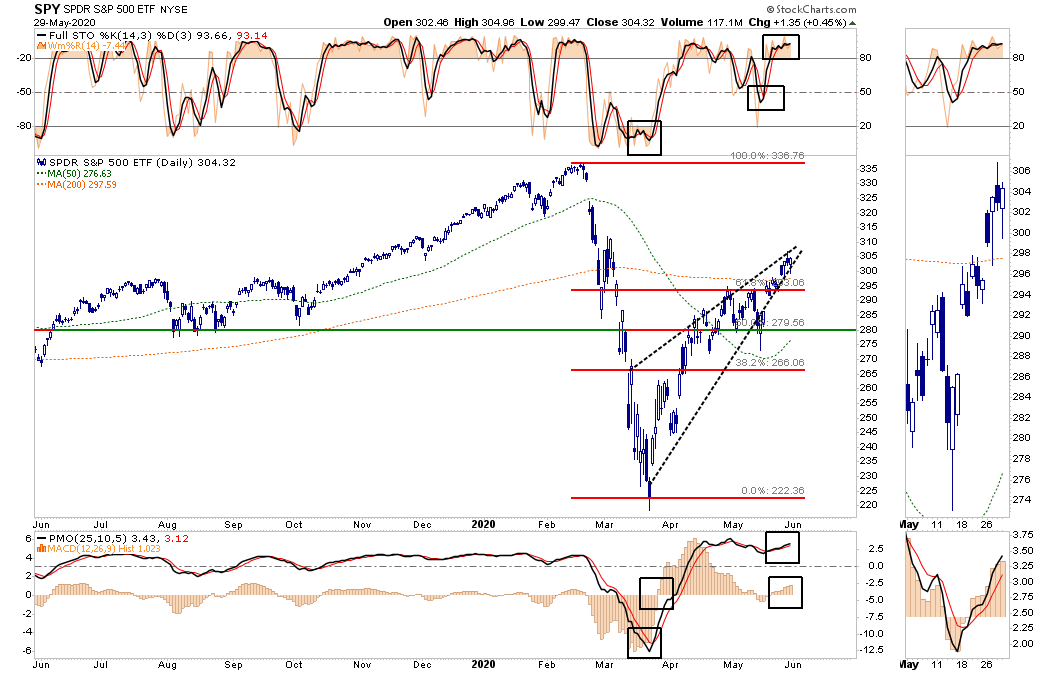

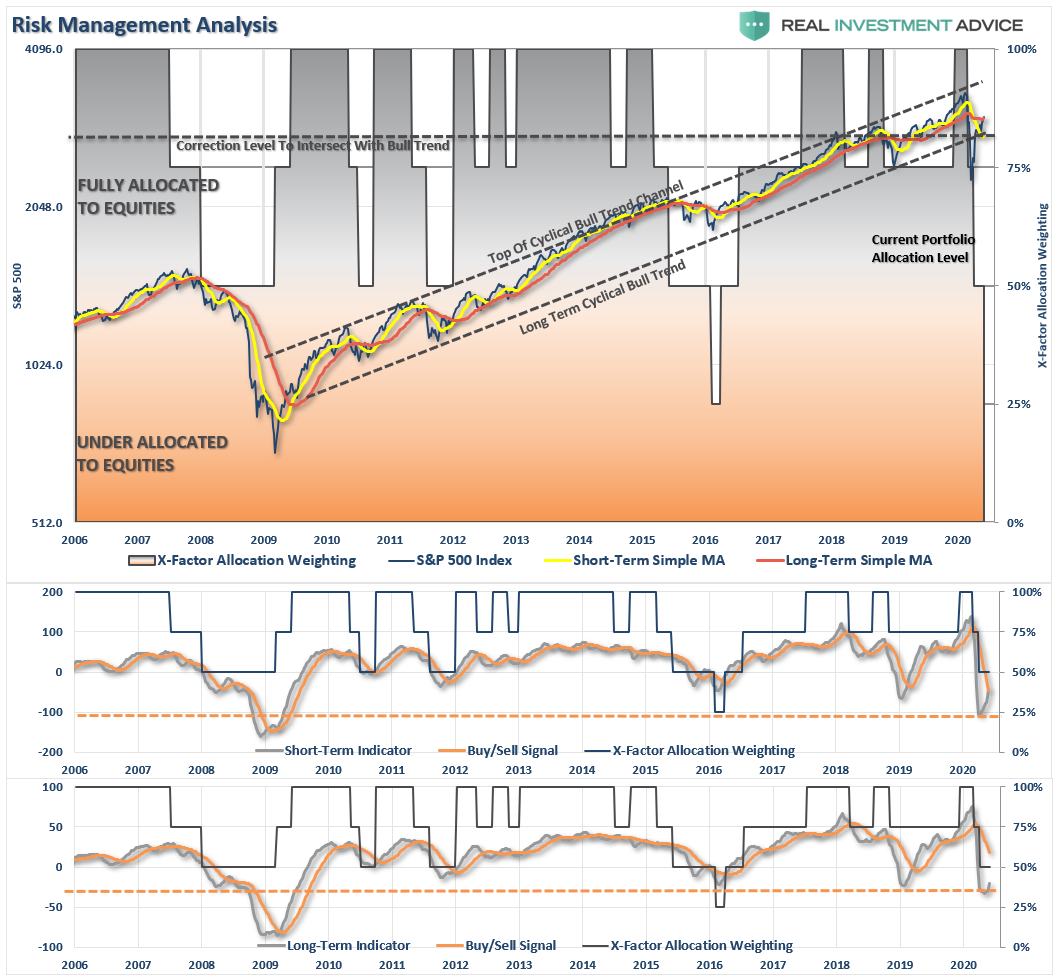

Market Breaks Above The 200-DMA

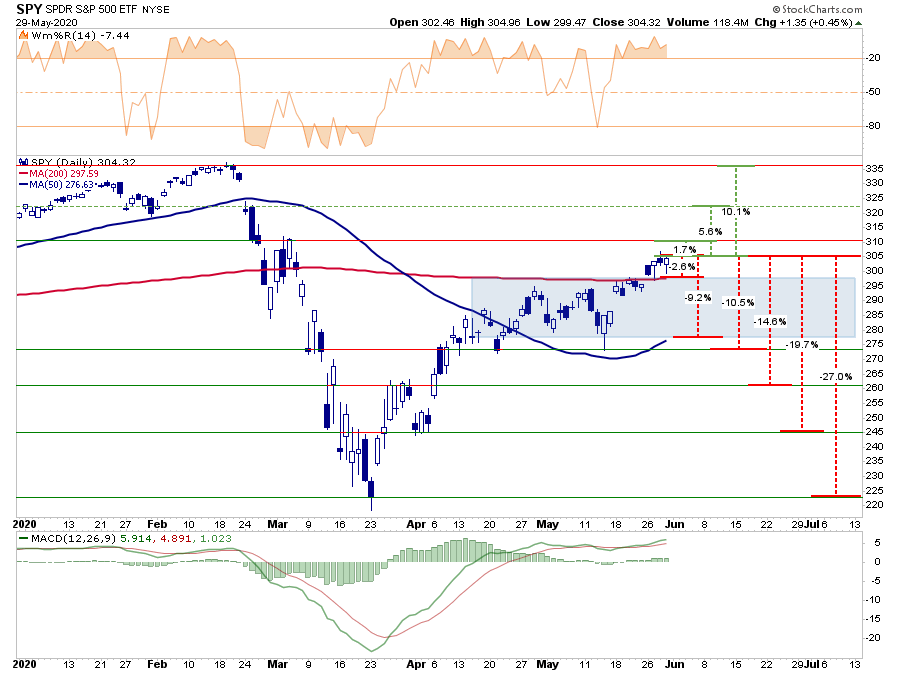

In last week’s missive, we discussed how the market remained stuck between the 50- and 200-dma. At that time, we noted the risk/reward ranges, which encompassed a breakout or retracement within that range. (The chart is updated through Friday’s close.)

The shaded blue area shows the containment of the market between the two moving averages. With the market very overbought short-term (orange indicator in the background), there is downside pressure on prices short-term.

While the market did break above the 200-dma, such does not change the negative risk/reward characteristics of the market.

- -2.8% to the 200-dma vs. +1.7% to the March peak. Negative

- -9.2% to the 50-dma vs. 5.6% to February gap down. Negative

- -10.5% to the consolidation support vs. +10.1% to all-time highs. Neutral

- -19.7% to April 1st lows vs. +10.1% to all-time highs. Negative

- -27% to March 23rd lows vs. +10.1% to all-time highs. Negative

However, as stated last week, the break above the 200-dma is currently changing the complexion of the market.

“If the markets can break above the 200-dma, and maintain that level, it would suggest the bull market is back in play. Such would change the focus from a retest of previous support to a push back to all-time highs.

While such would be hard to believe, given the economic devastation currently at hand, technically, it would suggest the decline in March was only a ‘correction’ and not the beginning of a ‘bear market.'”

While the negative risk/reward dynamics are evident, the more negative outcomes are becoming less probabilistic. However, on a longer-term basis, a deeper correction becomes more possible, given the deviation in prices from the underlying fundamentals.

Are Market Bulls Too Optimistic

Currently, the markets are rallying in hopes of a “V-Shaped” economic recovery, which will be supported by a COVID-19 vaccine and no second wave of the virus. If such is the case, then it is expected the depression level readings of unemployment and GDP will quickly reverse, supporting the stock market’s current valuations.

There are several underlying problems with this narrative:

- There is a very high probability that as states reopen their economies, there will be a “second-wave” of COVID-19.

- Out of the dozens of companies that are in the process of developing both therapeutics and a potential vaccine, the odds are incredibly high the vast majority, if not all, will fail.

- Corporate profits and earnings were already struggling, heading into the recession. While they will rebound as the recession passes, they are unlikely to return to levels to support current valuations.

- Unemployment will likely remain higher for longer than expected. Up to 50% of small businesses, which account for about 25% of all employment, are expected to shutdown. Consumption, which is where earnings and profits come from, will be cut accordingly.

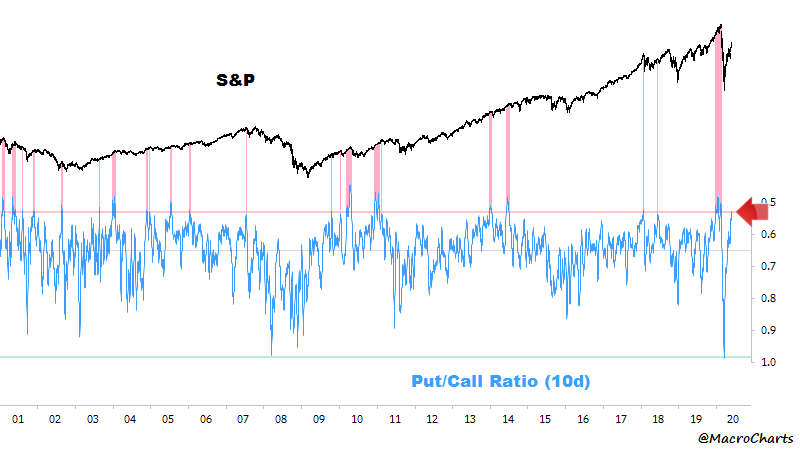

Currently, investors have gotten back to more extreme stages of bullishness as the market has relentlessly rallied from the lows.

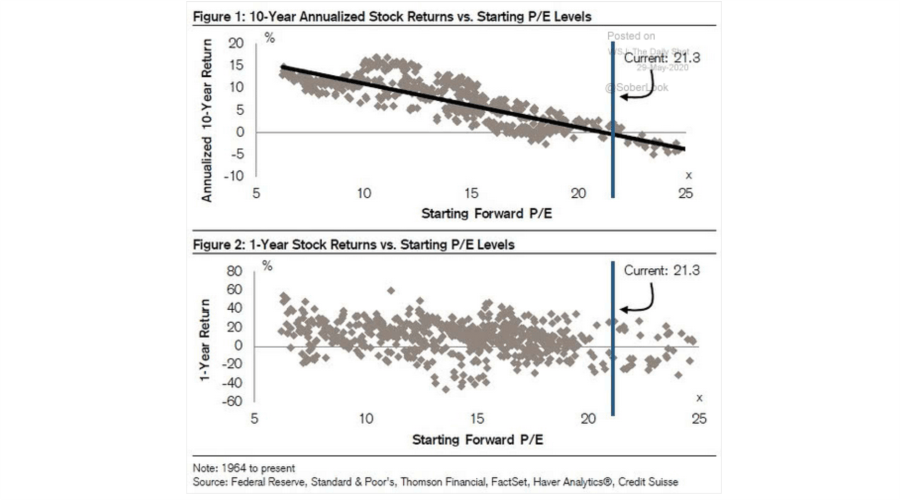

Valuations Matter Long-Term

However, the complete detachment from the underlying fundamentals is likely to weigh on the markets soon than later. Irrespective of Fed stimulus, valuations do matter over the longer-term time and will drive forward returns.

The problem is the valuation levels are worse than shown as earnings are still being revised lower, and will get worse. We know this because corporate profits were released this past week for Q1 and showed a record drop. That drop was for a quarter where the shutdown accounted for only 2-weeks of the reporting period. The decline in the second quarter will be materially worse as the entire month was lost to the pandemic.

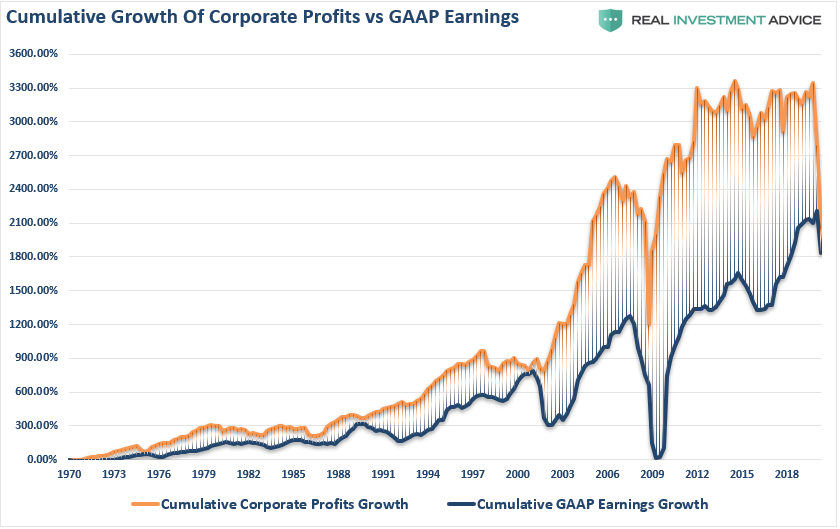

Castle Of Sand

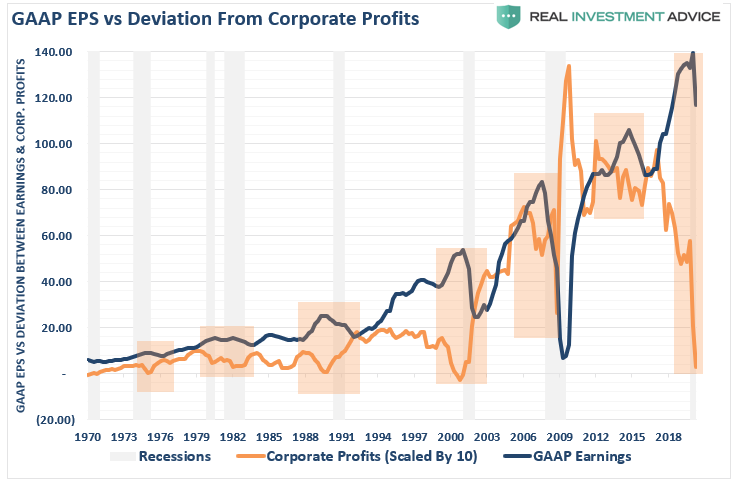

We can see the deviation between GAAP earnings and corporate profits if we use the data for first-quarter.

The shaded areas show the lag between the decline in profits and the decline in GAAP earnings. Over the next couple of quarters, profits are forecasting a much deeper decline for S&P 500 earnings. With estimates still in the $95/share range, we could see a rather substantial decline.

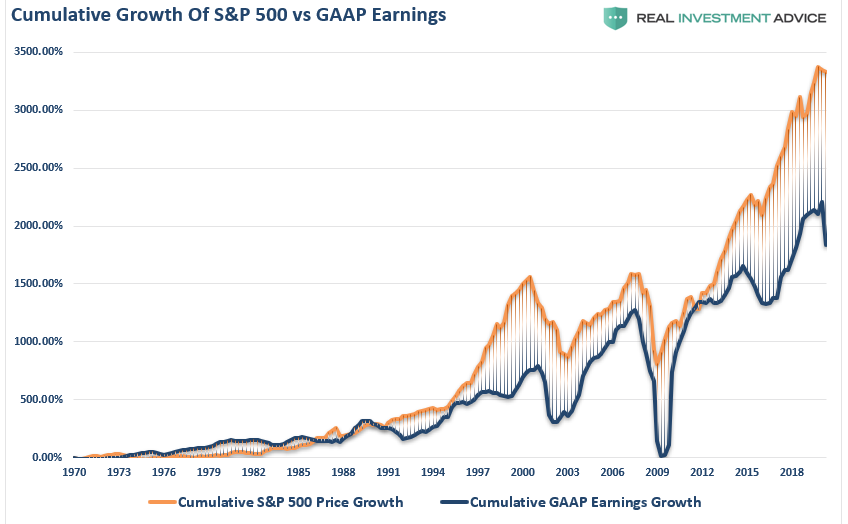

As stated, investors have priced in a “perfect” economic recovery story. Such leaves much room for disappointment as the deviation between what investors “expect,” and “reality” is at the highest level on record.

Historically, sharp declines in corporate profits are met by equally sharp declines in GAAP earnings.

While investors are “hopeful” this time will be different, the reality of 40-million unemployed, mass failures of small businesses, and a contraction in consumption, argues differently.

“It’s too ‘happy days are here again. It’s just not going to work like that. Not with 38 million unemployed. You can’t keep building on a castle of sand. I see a lot of quicksand underneath some moves. I wish we would just calm down and digest some of these things.” – Jim Cramer, Mad Money

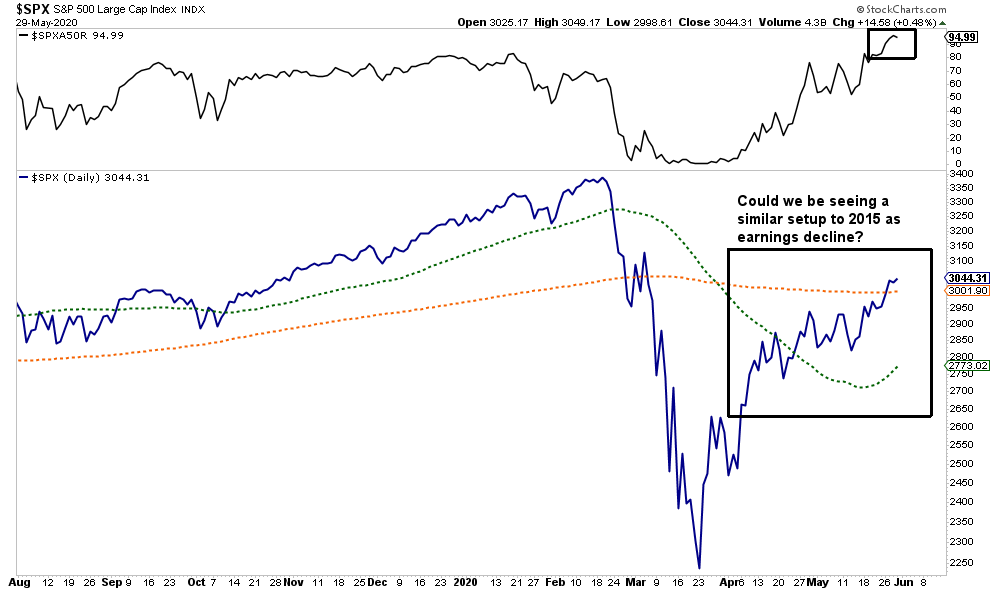

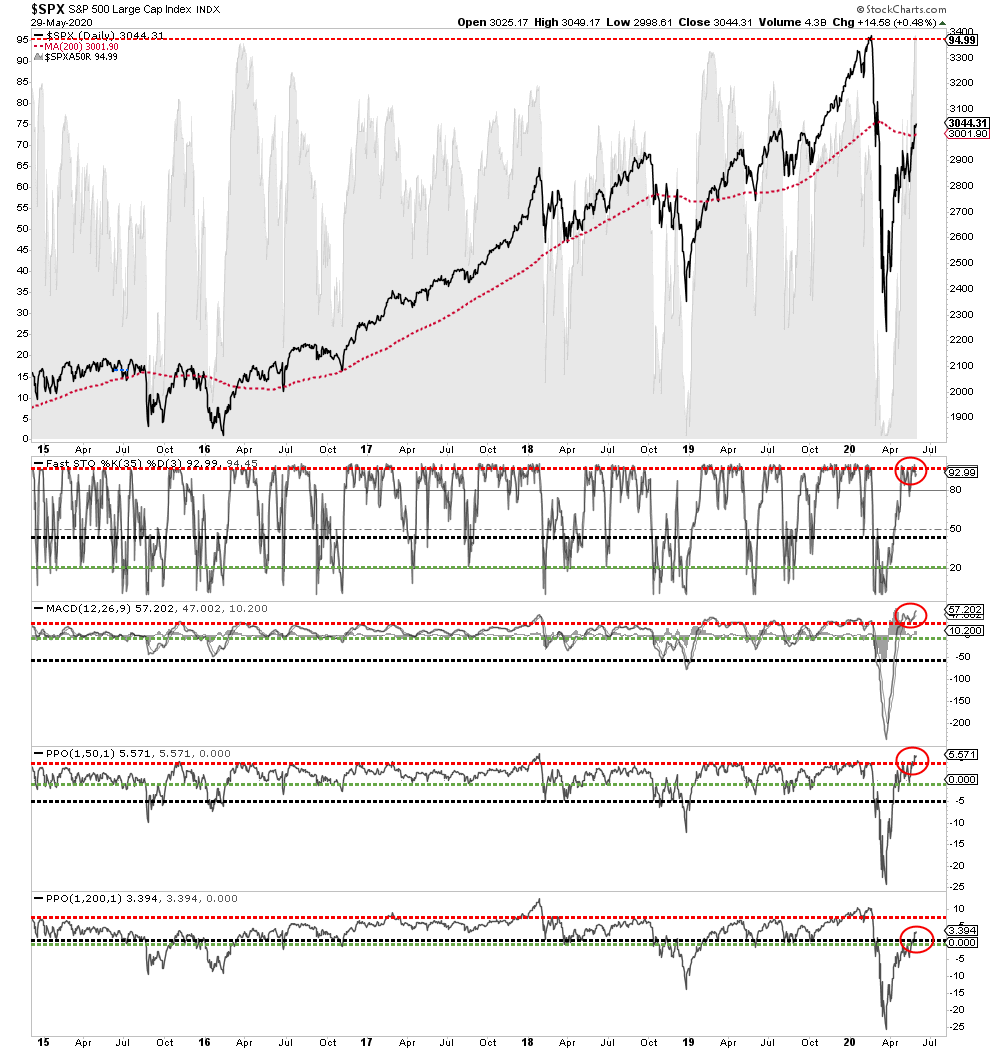

Technical Review Of The Market

No matter how you want to slice the data, the markets are back to more egregious overbought conditions on a short-term basis. With the markets very overbought, and in a very tight ascending wedge, watch for a break to the downside to signal the start of a correction.

Also, with roughly 95% of stocks now trading above the 50-dma, such has historically signaled short-term corrections to resolve the overbought condition.

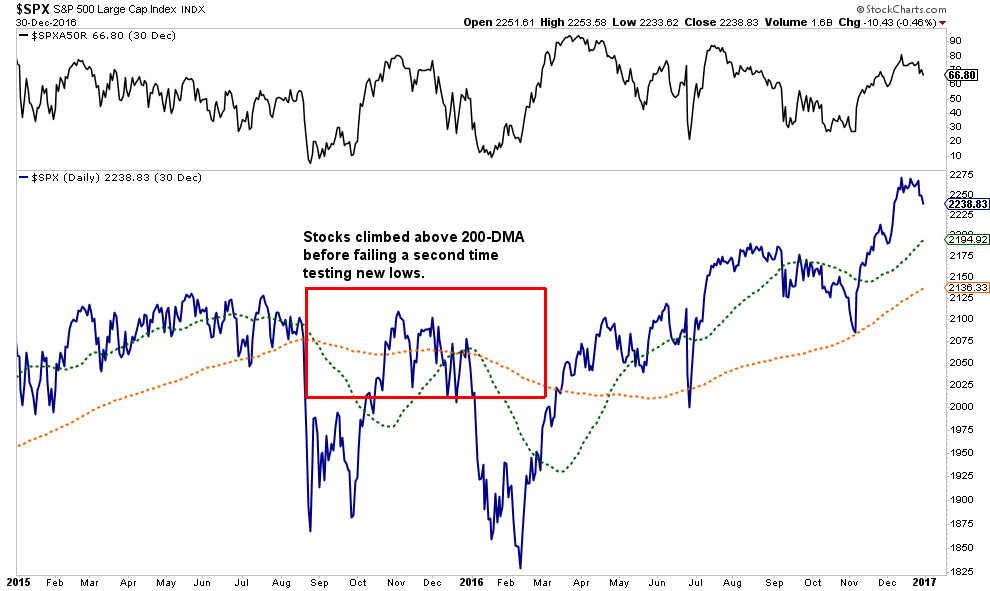

While much of the media has been talking about positive returns from stocks over the next 12-24 months, we could also have a 2015-2016 type scenario.

At that time, the markets climbed above the 200-dma, combined with a “Golden Cross” as the 50-dma also “crossed the Rubicon.” While the media bristled with bullish excitement, it was quickly extinguished as the markets set new lows as “Brexit” engulfed the headlines.

Importantly, while concerns about a “Brexit” on the global economy were valid, “Brexit” never materialized. Conversely, the economic devastation in the U.S., and globally, is occurring in real-time. The risk of a market failure as “reality” collides with “fantasy” should not be dismissed. It CAN happen.

Lastly, speaking of the number of stocks above the 50-dma, that indicator is laid behind the S&P 500 in the chart below. Historically, whenever all of the overbought/sold indicators have aligned, along with the vast majority of stocks being above the 50-dma, corrections were close.

Such doesn’t mean the next great “bear market” is about to start. It does mean that a correction back to support that reverts those overbought conditions is likely. Therefore, some prudent risk management may be in order.

Portfolio Positioning For An Overbought Market

This analysis is part of our thought process as we continue to weigh “equity risk” within our portfolios.

Positioning, and the related risk, remains our primary focus. This past week made changes that reduced risk in our overall portfolio by taking profits out of the largest gainers and adjusting weightings in defensive holdings. The following is trade commentary provided to our RIAPRO subscribers (30-day Risk-Free Trial)

Rebalancing The Equity Portfolio

In the equity portfolio we have rebalanced our exposures to align with our Relative Value Sector Report:

We are taking profits in:

- AAPL – 1.5% to 1% portfolio weight

- MSFT – 1.5% to 1%

- CHCT – 1.5% to 1%

- MPW – 1.5% to 1%

- RTX – 1.5% to 1.25%

- ABBV – 1.5% to 1.25%

We added exposure to:

- UNH – 1.5% to 2% portfolio weight

- DUK – 1.5% to 2%

- AEP – 1.5% to 2%

- NFLX – 1% (Trade only – see Jeffrey Marcus commentary)

Taking profits in our portfolio positions remains a “staple” in our risk management process. We have also increased our treasury bond and precious metals to hedge our increased risk over the last two months.

We don’t like the risk/reward of the market currently, and continue to suspect a better opportunity to increase equity risk will come later this summer. If the market violates the 200-dma or the ascending wedge, as noted above, is breached to the downside, we will reduce equity risk and hedge further.

I will conclude this week with a quote from my colleague Victor Adair at Polar Trading:

“The growing divergence between the ‘stock market’ and the economy the past couple of months might be a warning flag that Mr. Market is too exuberant. The Presidential election is just over 5-months away with polls showing that Biden may be the next President. The U.S./China tensions have been escalating, and the virus’s first wave continues to spread around the globe. However, the ‘stock market’ continues to be pulled higher by a handful of ‘Megacaps.’ The late Friday rally after Trump’s ‘punish China’ speech shows ‘animal spirits’ are alive and well!”

I agree, and while such may be the case for the moment, markets like this have a nasty habit of delivering unpleasant surprises.

Pay attention to how much risk you are taking.

The MacroView

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Market & Sector Analysis

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now! Risk-Free For 30-Day Trial.

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

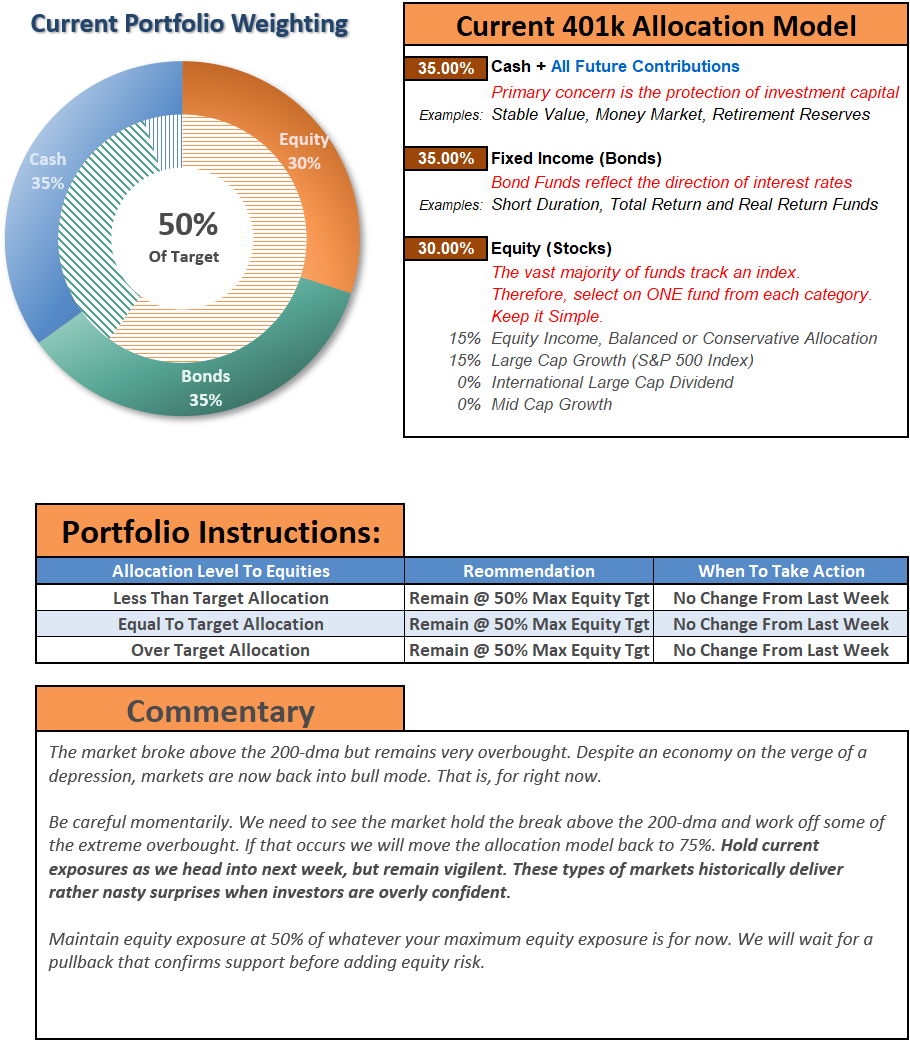

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

If you need help after reading the alert; do not hesitate to contact me

Model performance is a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. Such is strictly for informational and educational purposes only and should not be relied on for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k plan manager.

Compare your current 401k allocation, to our recommendation for your company-specific plan as well as our on 401k model allocation.

You can also track performance, estimate future values based on your savings and expected returns, and dig down into your sector and market allocations.

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.