- Market Review & Update

- MacroView: Is This A Repeat Of 2018?

- Sector & Market Analysis

- 401k Plan Manager

Follow Us On: Twitter, Facebook, Linked-In, Sound Cloud, Seeking Alpha

Catch Up On What You Missed Last Week

Market Review & Update

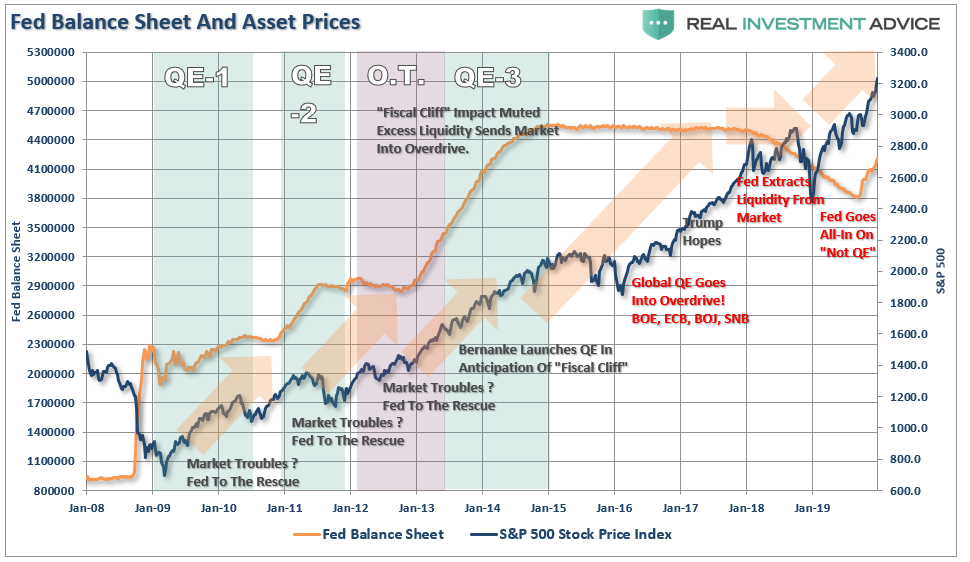

The first trading day of the year started with a “bang” with the S&P 500 rising more than 20 points. However, the gain was abbreviated on Friday as news shook the market the U.S. had taken out a top Iranian commander in Baghdad. But concerns over potential Iranian conflict quickly abated as the markets returned their focus to the Federal Reserve, and the continued pump of monetary liquidity into the markets. A point noted in our MacroView below.

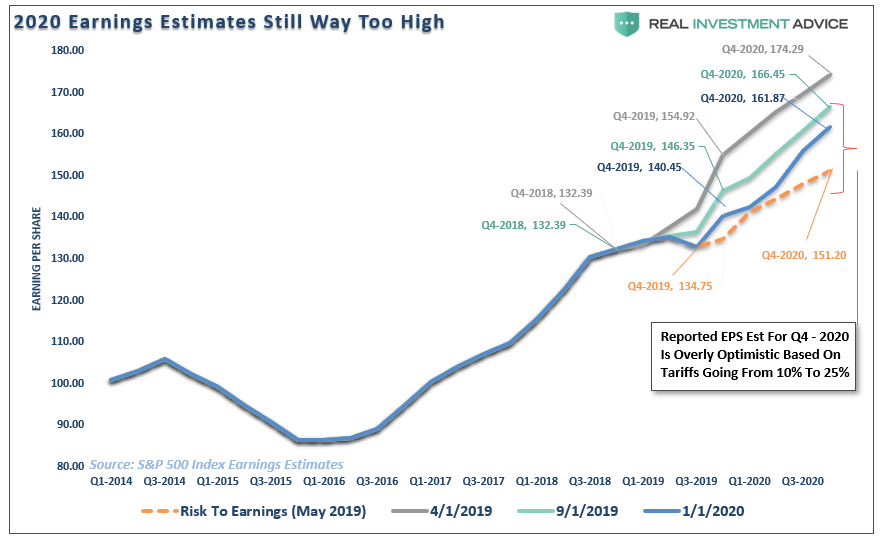

While the pump of liquidity continues to push asset prices higher, earnings continue to fall. Economic growth remains weak, and despite hopes for a “revival,” it has yet to be seen. Ultimately, stocks are a reflection of economic activity, and, as I predicted in May of last year, estimates were far too high relative to economic growth. Since then, earnings have continued to decline toward our original estimate. In fact, in just the last month, estimates for the end of 2020 fell by almost $2 per share. This is occurring at a time where investors are piling into stocks regardless of price or valuation. Such is just the “Pavlovian” response to more monetary stimulus.

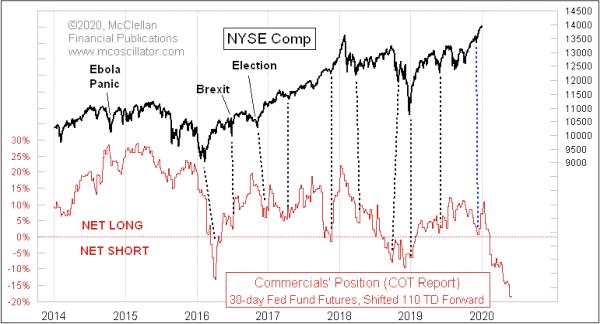

This was a point made by Tom McClellan this past week:

“The efforts of the Federal Reserve to inject extra liquidity into the banking system over the past 2-months have helped to fuel the year-end (2019) rally. Questions remain about how long the Fed may choose to keep up that effort, and whether the Fed has enough ink in the printing presses to overcome other market forces.”

“The indicator in this chart depicts the net position of the ‘commercial’ traders of Fed Fund futures, expressed as a percentage of total open interest. The fun part comes when we realize that the movements of that indicator get repeated roughly 110 trading days later in stock prices.

Over the past 100 or so trading days, we have seen a big move in the commercial traders’ net position, moving from net long the Fed Funds futures to net short in a big way. It is the biggest such move we have seen in a few years; its implication is that there is a big down move coming for stock prices.”

Given the more extreme extension of stocks currently, Tom’s suggestion of a correction is likely particularly if the Fed decides to slow their monetary inputs.

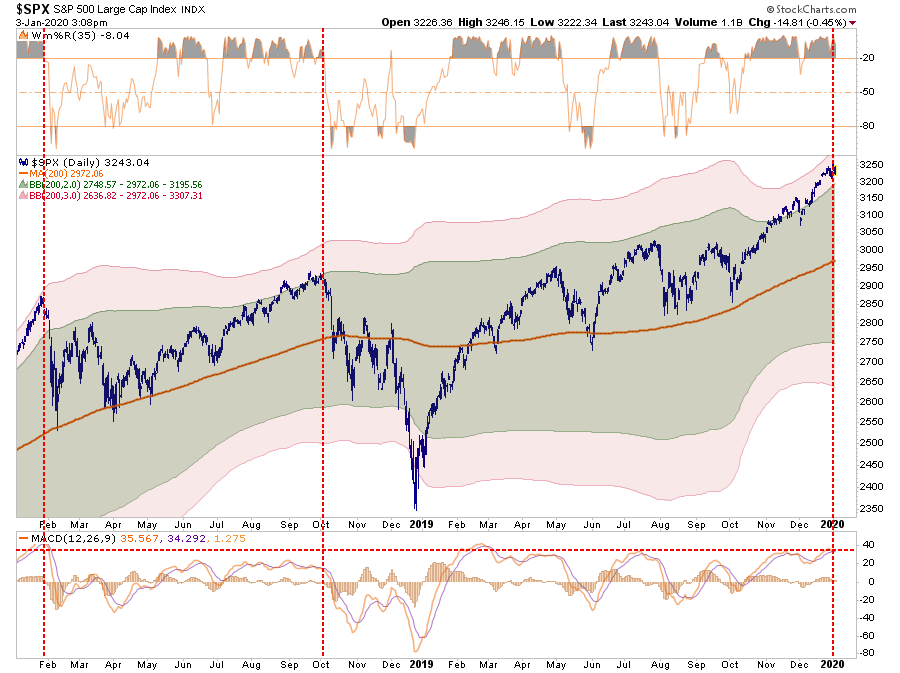

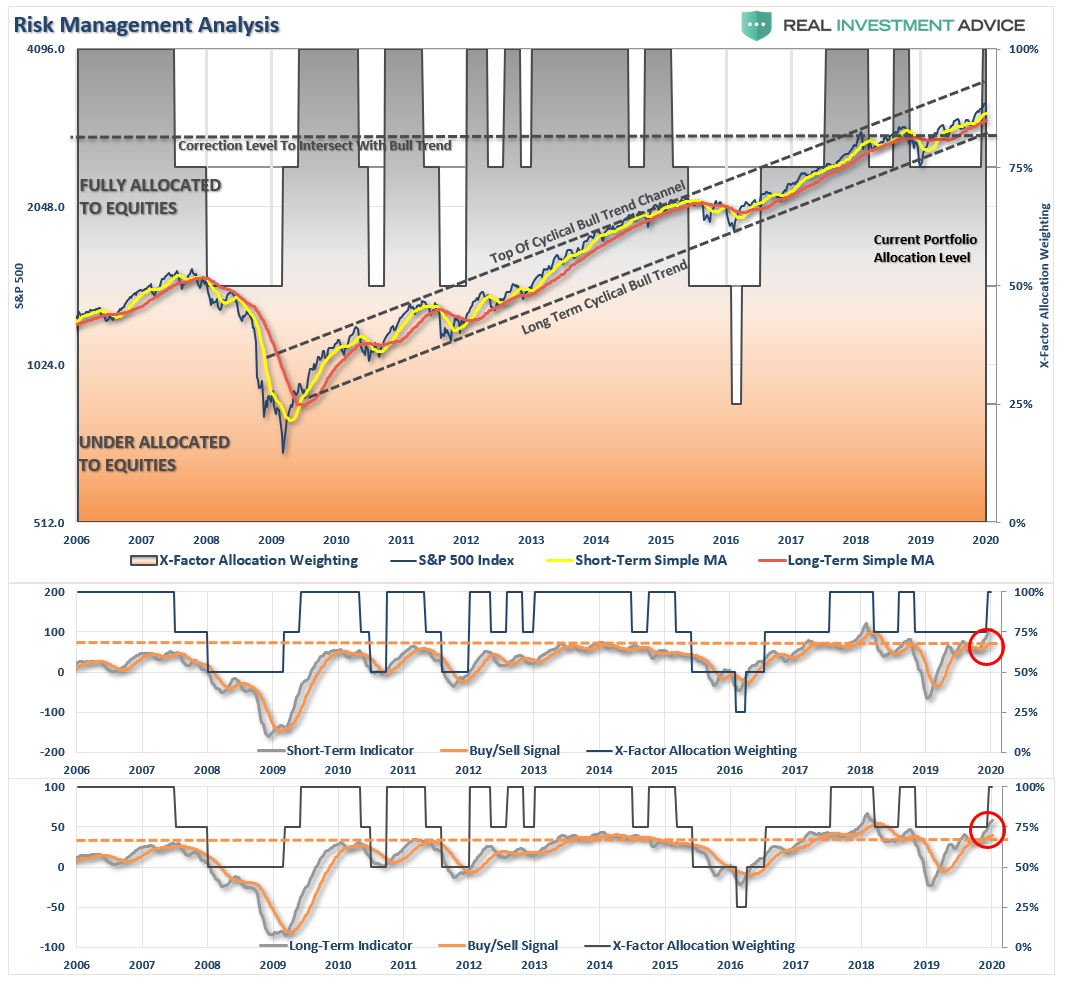

As shown in the chart below, the market is currently trading 3-standard deviations above the 200-dma, which is somewhat of a rarity until just the last couple of years. Since the beginning of 2018, there have been three occurrences, with the previous two leading to short-term corrections.

There is an important difference between the previous two incidents and today as the Fed was reducing monetary liquidity instead of increasing it.

Portfolio Positioning

As we kick off the “New Trading Year,” we remain long our current portfolio exposures in both the Equity and ETF Portfolios. We have also started building a new “Dynamic Portfolio,” which is a “go anywhere, do anything” portfolio of our “best ideas.”

You can view all of our portfolio models, which are live accounts, at RIA PRO. (You can try out the service for 30-days FREE)

As we head into 2020, our major theme is the potential decline of the U.S. Dollar, relative to other currencies, which has a profound impact on many other sectors of the market. Those areas include:

- International markets

- Emerging markets

- Oil

- Gold

- Commodities

- Energy

- Interest Rates

These are themes we have been discussing with RIA PRO subscribers, and building into our portfolios, over the last few months.

We also continue to suspect the yield curve will steepen as we head further into the year. Higher rates will result from flows out of the U.S. dollar into foreign-denominated assets initially, BUT, higher rates will then trigger much weaker economic growth domestically. With weaker growth, comes weaker earnings and lower stock prices.

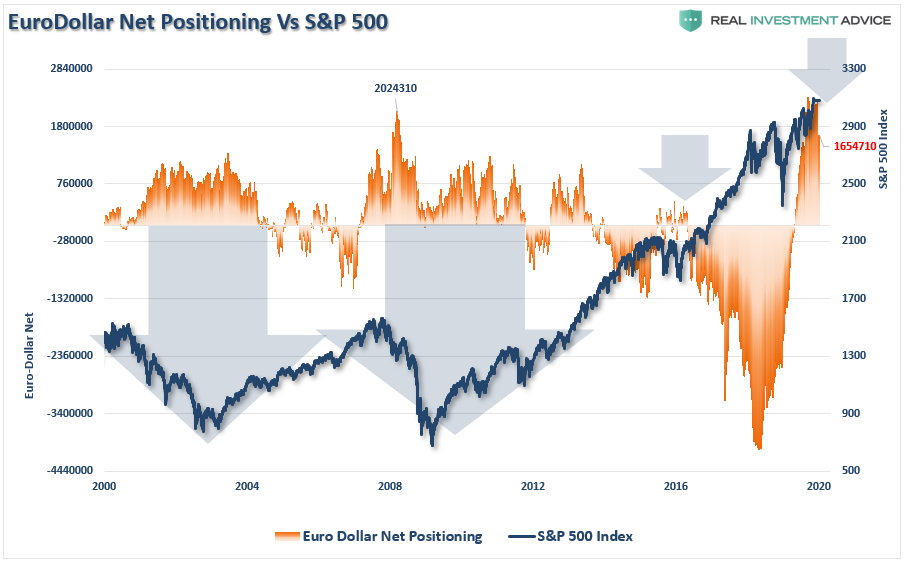

Again, we are focused on the U.S. Dollar as foreign speculative positioning has reached extremes. Reversals in positioning have not been kind to stock prices but bode well for alternative asset classes which can hedge long equity risk.

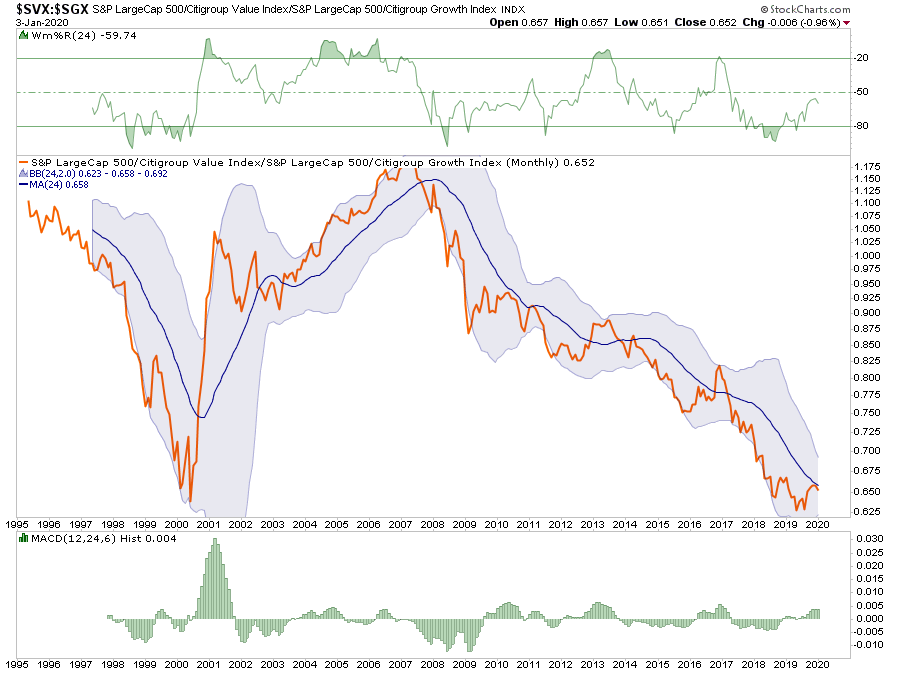

Lastly, we are also looking for a return of value relative to growth. As shown in the chart below, the deviation in performance has reached historic extremes.

The last time that “value” underperformed “growth” by such a large degree was heading into the “dot.com” crisis. At that time Warren Buffett was being ridiculed for underperforming the S&P 500 by such a large degree.

He was vindicated for his “value” approach shortly thereafter.

Interestingly, here we are once again, and this was the headline of an article that came across my desk on Friday:

“One of the most reliable rules of American investing over the last 50 years may have finally been broken. Warren Buffett’s Berkshire Hathaway is not the sure bet it once was.” – Motley Fool

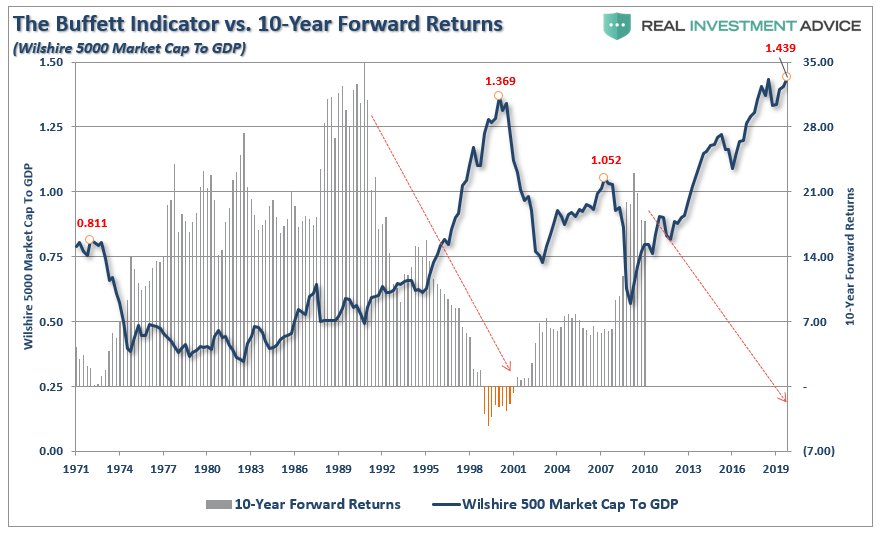

Of course, a major reason for that underperformance is the $128 Billion in CASH that Buffett is holding on his balance sheet. Of course, for a value investor like Buffett, it is hard to invest cash into a market where there is little to no value, and forward 10-year returns are expected to be low.

In other words, when the media starts dismissing Warren Buffett, maybe its time to start considering the “why” he is sitting on so much cash.

Importantly, it is for this reason that we are beginning to add “value” plays to our portfolio in small bits until we see the rotation begin to gain traction. In the meantime, this is a great time to review the trading rules needed to be a better investor as we head into 2020.

Remember, our job as investors is pretty simple – protect our investment capital from short-term destruction so that we can play the long-term investment game.

The Macro View

If you need help or have questions, we are always glad to help. Just email me.

See You Next Week

By Lance Roberts, CIO

Financial Planning Corner

You’ll be hearing more about more specific strategies to diversify soon, but don’t hesitate to give me any suggestions or questions.

by Danny Ratliff, CFP®, ChFC®

Market & Sector Analysis

Data Analysis Of The Market & Sectors For Traders

MISSING THE REST OF THE NEWSLETTER?

This is what our RIAPRO.NET subscribers are reading right now!

- Sector & Market Analysis

- Technical Gauges

- Sector Rotation Analysis

- Portfolio Positioning

- Sector & Market Recommendations

- Client Portfolio Updates

- Live 401k Plan Manager

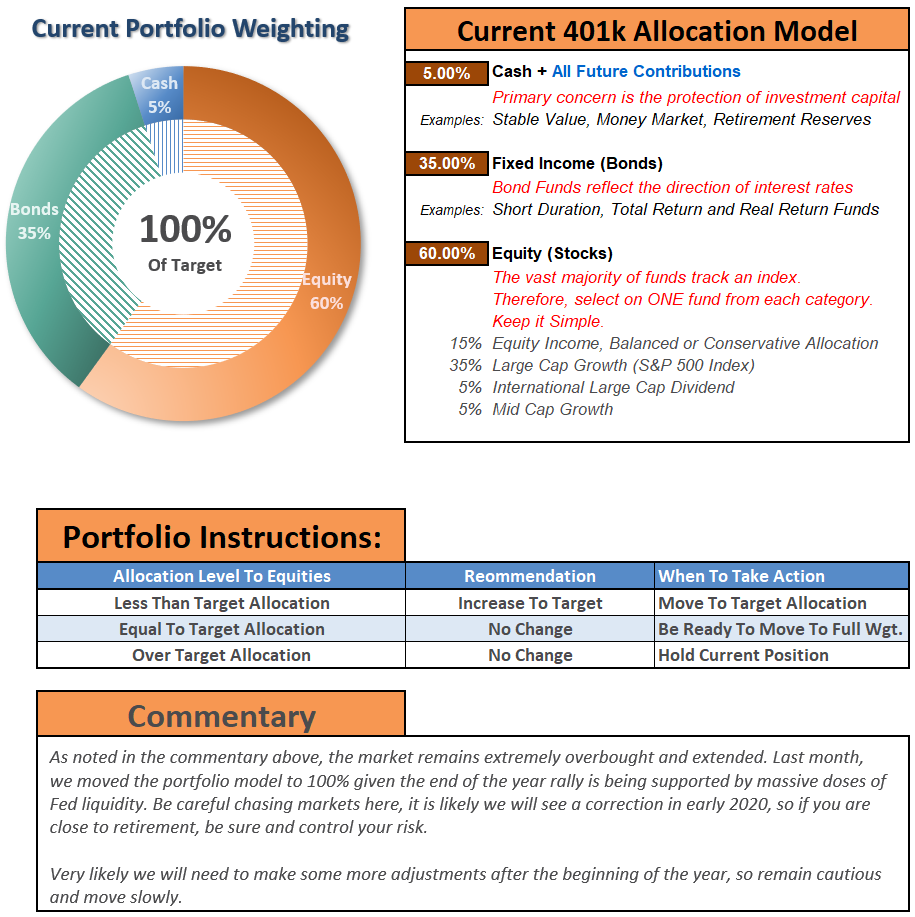

THE REAL 401k PLAN MANAGER

A Conservative Strategy For Long-Term Investors

The 401k plan allocation plan below follows the K.I.S.S. principle. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

If you need help after reading the alert; do not hesitate to contact me.

Click Here For The “LIVE” Version Of The 401k Plan Manager

See below for an example of a comparative model.

Model performance is based on a two-asset model of stocks and bonds relative to the weighting changes made each week in the newsletter. This is strictly for informational and educational purposes only and should not be relied upon for any reason. Past performance is not a guarantee of future results. Use at your own risk and peril.

401k Plan Manager Live Model

As an RIA PRO subscriber (You get your first 30-days free) you have access to our live 401k p

The code will give you access to the entire site during the 401k-BETA testing process, so not only will you get to help us work out the bugs on the 401k plan manager, you can submit your comments about the rest of the site as well.

We are building models specific to company plans. So, if you would like to see your company plan included specifically, send me the following:

- Name of the company

- Plan Sponsor

- A print out of your plan choices. (Fund Symbol and Fund Name)

If you would like to offer our service to your employees at a deeply discounted corporate rate, please contact me.