This past weekend, I was in Florida with Chris Martenson and Nomi Prins discussing the current backdrop of the markets, economic cycles, and future outcomes. A bulk of the conversations centered around the current “everything bubble” that currently exists globally. Elevated valuations in stock prices, extremely low yields between in “junk bonds,” or intense speculation around “cryptocurrencies” all suggest we have entered once again into “bubble” territory.”

Let me state this:

“Market bubbles have NOTHING to do with valuations or fundamentals.”

Hold on…don’t start screaming “heretic” and building gallows just yet. Let me explain.

Stock market bubbles are driven by speculation, greed, and emotional biases – therefore valuations and fundamentals are simply a reflection of those emotions.

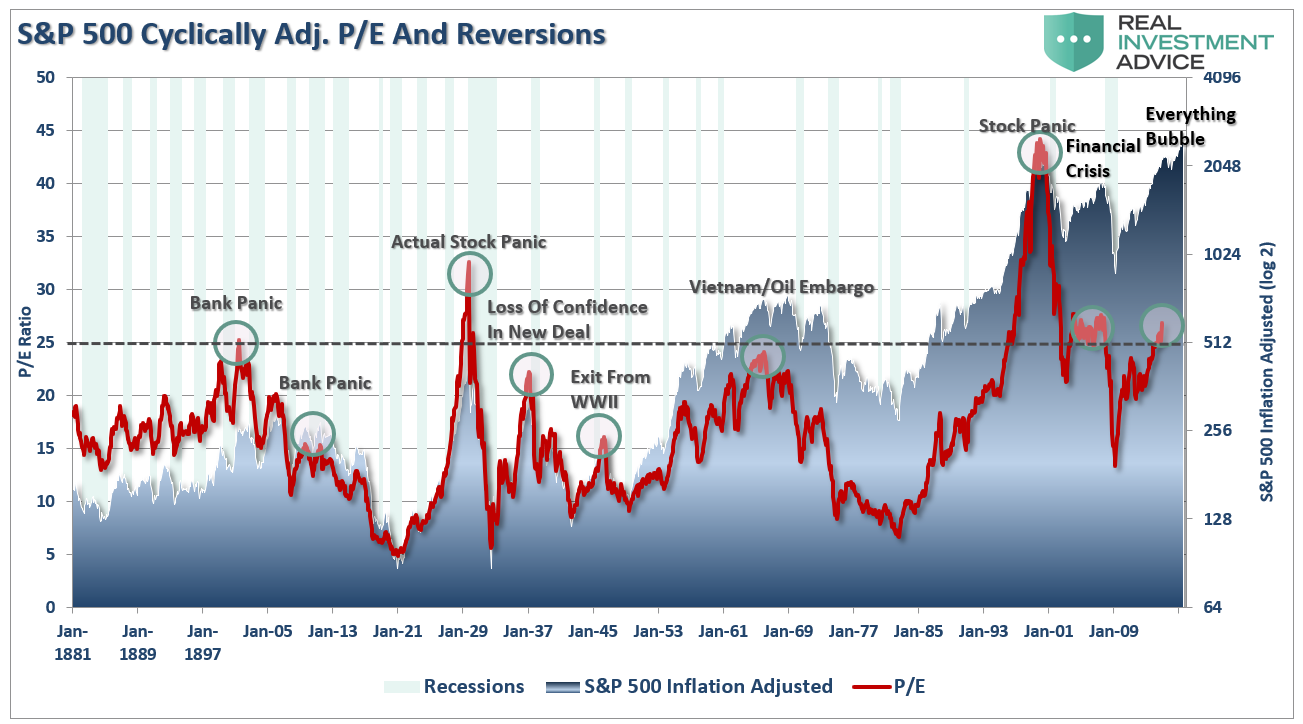

In other words, bubbles can exist even at times when valuations and fundamentals might argue otherwise. Let me show you a very basic example of what I mean. The chart below is the long-term valuation of the S&P 500 going back to 1871.

First, it is important to notice that with the exception of only 1929, 2000 and 2007, every other major market crash occurred with valuations at levels LOWER than they are currently. Secondly, all of these crashes have been the result of things unrelated to valuation levels such as liquidity issues, government actions, monetary policy mistakes, recessions or inflationary spikes. However, those events were only a catalyst, or trigger, that started the “panic for the exits” by investors.

Market crashes are an “emotionally” driven imbalance in supply and demand. You will commonly hear that “for every buyer, there must be a seller.” This is absolutely true. The issue becomes at “what price.” What moves prices up and down, in a normal market environment, is the price level at which a buyer and seller complete a transaction.

In a market crash, however, the number of people wanting to “sell” vastly overwhelms the number of people willing to “buy.” It is at these moments that prices drop precipitously as “sellers” drop the levels at which they are willing to dump their shares in a desperate attempt to find a “buyer.” This has nothing to do with fundamentals. It is strictly an emotional panic which is ultimately reflected by a sharp devaluation in market fundamentals.

Bob Bronson once penned:

“It can be most reasonably assumed that market are sufficient enough that every bubble is significantly different than the previous one, and even all earlier bubbles. In fact, it’s to be expected that a new bubble will always be different than the previous one(s) since investors will only bid up prices to extreme overvaluation levels if they are sure it is not repeating what led to the last, or previous bubbles. Comparing the current extreme overvaluation to the dotcom is intellectually silly.

I would argue that when comparisons to previous bubbles become most popular – like now – it’s a reliable timing marker of the top in a current bubble. As an analogy, no matter how thoroughly a fatal car crash is studied, there will still be other fatal car crashes in the future, even if the previous accident-causing mistakes are avoided.”

He is absolutely right. Comparing the current market bubble to any previous market bubble is rather pointless. Financial markets have already studied and adapted to the causes of the previous “fatal crashes” but this won’t prevent the next one.

I previously discussed George Soros’ theory on bubbles which is worth reviewing at this juncture:

“First, financial markets, far from accurately reflecting all the available knowledge, always provide a distorted view of reality. The degree of distortion may vary from time to time. Sometimes it’s quite insignificant, at other times it is quite pronounced. When there is a significant divergence between market prices and the underlying reality the markets are far from equilibrium conditions.

Every bubble has two components:

- An underlying trend that prevails in reality, and;

- A misconception relating to that trend.

When a positive feedback develops between the trend and the misconception, a boom-bust process is set in motion. The process is liable to be tested by negative feedback along the way, and if it is strong enough to survive these tests, both the trend and the misconception will be reinforced. Eventually, market expectations become so far removed from reality that people are forced to recognize that a misconception is involved. A twilight period ensues during which doubts grow, and more people lose faith, but the prevailing trend is sustained by inertia.

As Chuck Prince, former head of Citigroup, said, ‘As long as the music is playing, you’ve got to get up and dance. We are still dancing.’ Eventually, a tipping point is reached when the trend is reversed; it then becomes self-reinforcing in the opposite direction.”

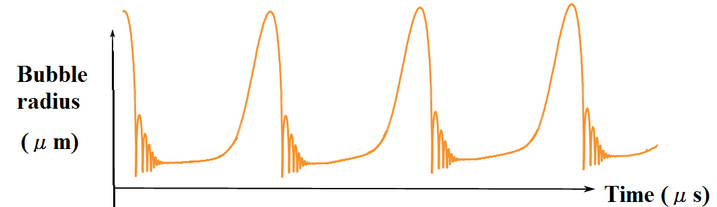

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.

The chart below is an example of asymmetric bubbles.

The pattern of bubbles is interesting because it changes the argument from a fundamental view to a technical view. Prices reflect the psychology of the market which can create a feedback loop between the markets and fundamentals.

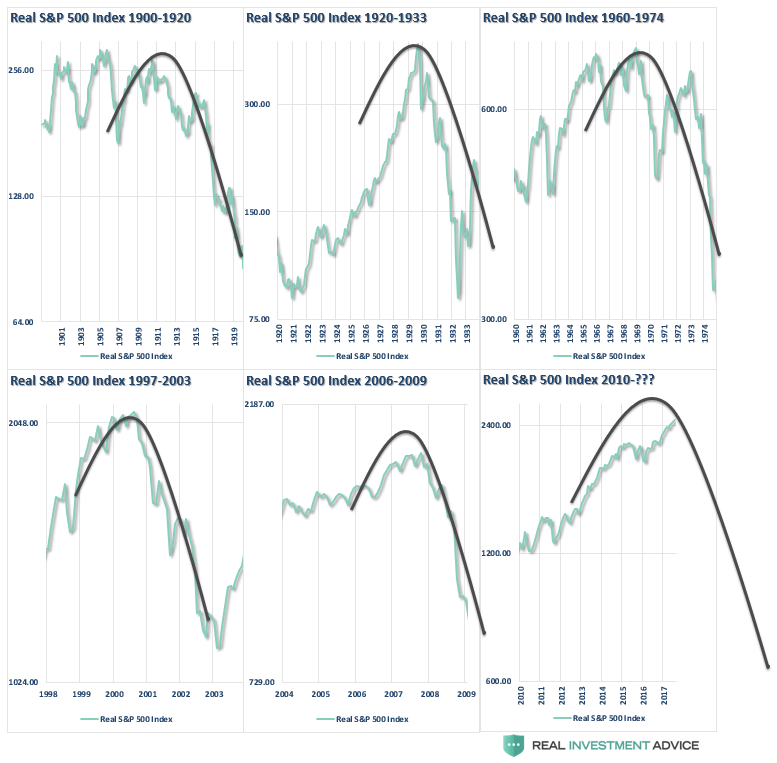

This pattern of bubbles can be clearly seen at every bull market peak in history. The chart below utilizes Dr. Robert Shiller’s stock market data going back to 1900 on an inflation-adjusted basis with an overlay of the asymmetrical bubble shape.

There is currently a strong belief that the financial markets are not in a bubble. The arguments supporting those beliefs are all based on comparisons to past market bubbles.

The inherent problem with much of the mainstream analysis is that it assumes everything remains status quo. However, the question becomes what can go wrong for the market?

In a word, “much.”

Economic growth remains very elusive, corporate profits appear to have peaked, and there is an overwhelming complacency with regards to risk. Those ingredients combined with an extraction of liquidity by the Federal Reserve leaves the markets more vulnerable to an exogenous event than currently believed.

It is likely that in a world where there is virtually “no fear” of a market correction, an overwhelming sense of “urgency” to be invested and a continual drone of “bullish chatter;” markets are poised for the unexpected, unanticipated and inevitable reversion.

As Chris Martenson recently penned:

“I hate to break it to you, but chances are you’re just not prepared for what’s coming.

These bubbles – blown by central bankers serially addicted to creating them (and then riding to the rescue to fix them) – are the largest in all of history. That means they’re going to be the most destructive in history when they finally let go.

Millions of households will lose trillions of dollars in net worth. Jobs will evaporate, causing the tens of millions of families living paycheck to paycheck serious harm.

These are the kind of painful consequences central bank follies result in. They’re particularly regrettable because they could have been completely avoided if only we’d taken our medicine during the last crisis back in 2008. But we didn’t. We let the Federal Reserve –the institution largely responsible for creating the Great Financial Crisis — conspire with its brethren central banks to ‘paper over’ our problems.

So now we are at the apex of the most incredible nest of financial bubbles in all of human history.”

I am not trying to scare the “bejeebers” out of you, but he is right.

“All financial assets are just claims on real wealth, not actual wealth itself. A pile of money has use and utility because you can buy stuff with it. But real wealth is the “stuff” — food, clothes, land, oil, and so forth. If you couldn’t buy anything with your money/stocks/bonds, their worth would revert to the value of the paper they’re printed on (if you’re lucky enough to hold an actual certificate). It’s that simple.

But trouble begins when the system gets seriously out of whack.

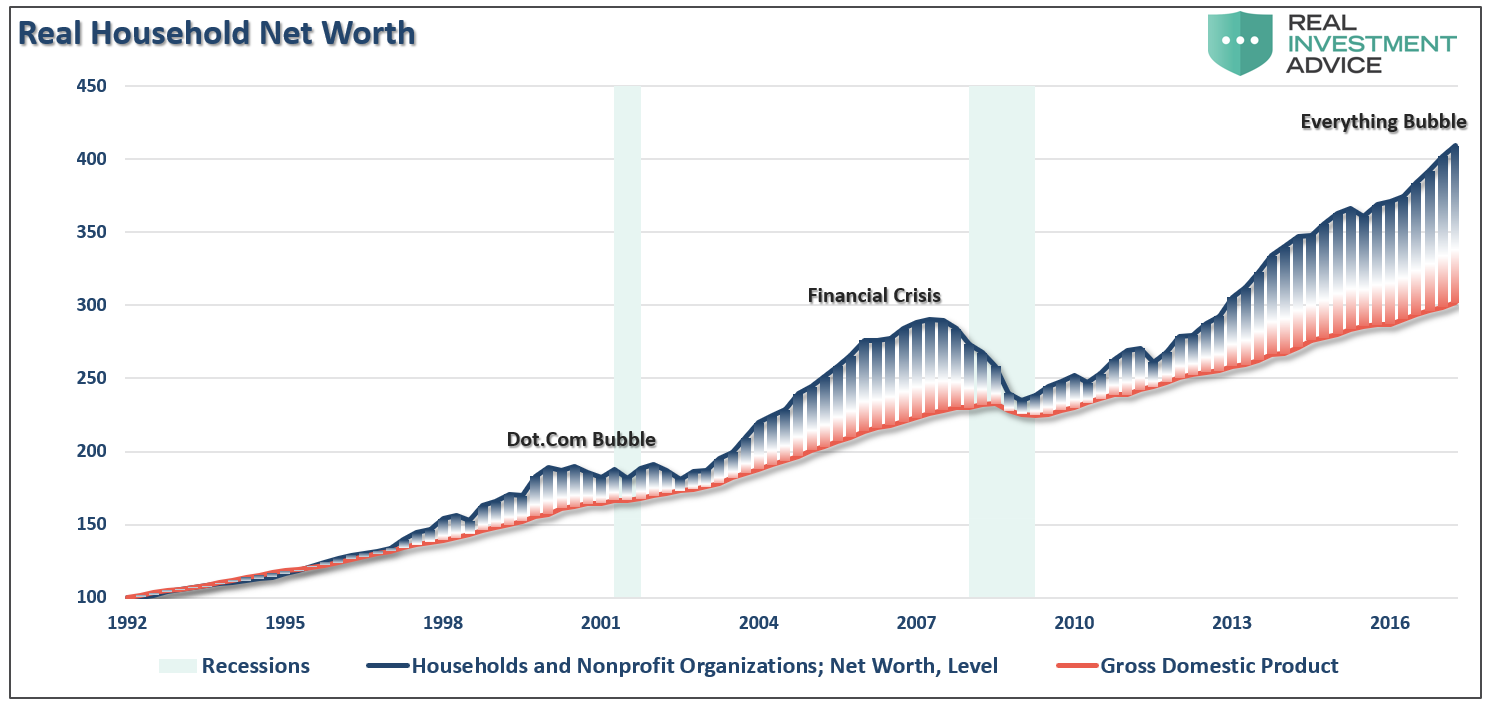

‘GDP’ is a measure of the number of goods and services available and financial asset prices represent the claims (it’s not a very accurate measure of real wealth, but it’s the best one we’ve got, so we’ll use it). Look at how divergent asset prices get from GDP as bubbles develop.

“What we see in the above chart is that the claims on the economy should, quite intuitively, track the economy itself. Bubbles occurred whenever the claims on the economy, the so-called financial assets (stocks, bonds, and derivatives), get too far ahead of the economy itself.

This is a very important point. The claims on the economy are just that: claims. They are not the economy itself!”

Take a step back from the media, and Wall Street commentary, for a moment and make an honest assessment of the financial markets today. If our job is to “bet” when the “odds” of winning are in our favor, then exactly how “strong” is the fundamental hand you are currently betting on?

This “time IS different” only from the standpoint that the variables are not exactly the same as they have been previously. Of course, they never are, and the result will be “…the same as it ever was.”