Inflation is now running at 7-percent, well above the Fed 2% objective. Following the CPI report, Cleveland Fed President Mester mentioned the Fed should sell some of their bond holdings and not merely let them roll off as they mature. This new hawkish wrinkle would greatly speed up balance sheet normalization. Despite the bearish implications for market liquidity, investors not need not worry. Ms. Mester also said they should reduce the balance sheet “as fast as it can without disrupting financial markets.” The Fed’s vocal concern for the stock market helps explain why stocks were relatively calm on the day inflation reached 7-percent, a 40 year high.

[dmc]

What To Watch Today

Economy

- 8:30 a.m. ET: Producer Price Index (PPI), month-over-month, December (0.4% expected, 0.8% in November)

- 8:30 a.m. ET: PPI excluding food and energy, month-over-month, December (0.5% expected, 0.7% in November)

- 8:30 a.m. ET: PPI year-over-year, December (9.8% expected, 9.6% in November)

- 8:30 a.m. ET: PPI excluding food and energy, year-over-year, December (8.0% expected, 7.7% in November)

- 8:30 a.m. ET: Initial jobless claims, week ended Jan. 8 (200,000 expected, 207,000 during prior week)

- 8:30 a.m. ET: Continuing claims, week ended Jan. 1 (1.733 million during prior week)

Earnings

7:25 a.m. ET: Delta Air Lines (DAL) to report adjusted earnings of $0.225 on revenue of $8.452 billion

Market Trading Update

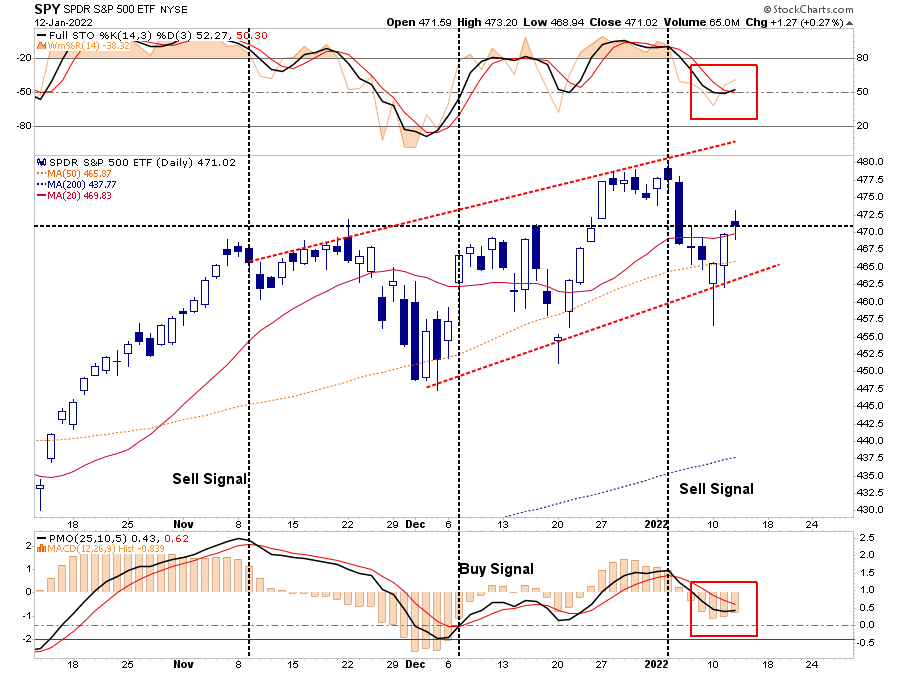

Despite a much more hawkish Fed in recent testimony, 7-percent inflation, and a lot of hand-wringing over the recent decline, the market has done “nothing” wrong. The uptrend channel that began in early December remains intact, the current “sell-signals” are starting to turn towards “buys,” and the market pushed above resistance with yesterday’s rally.

Currently, market action remains well contained and there remains little need to get overly concerned, for now. However, as always, things can, and will, change so it remains prudent to be slightly more cautious as we head into 2022.

Value Versus Growth

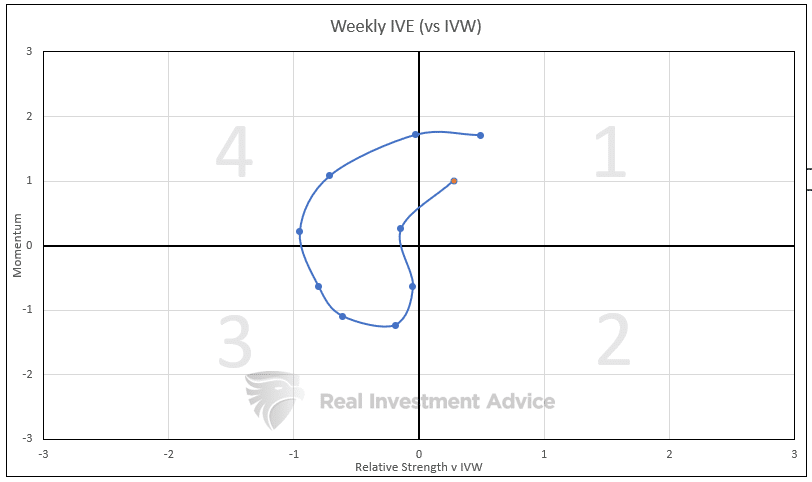

For the first time in a while, value stocks seem to be gaining momentum versus growth stocks. Is it lasting or just another false breakout for value? We have developed a tool to help us better monitor value versus growth.

The graph below is a weekly scatter plot comparing value’s (IVE) momentum versus its relative strength as compared to growth (IVW). When dots appear in the top right corner it signals that value stocks have strong momentum and relative strength. We should expect the best returns as it heads toward that corner. Conversely, the bottom left corner is the worst area for value stocks. The current level is denoted in orange and the line shows us the path it has traveled over the last 10 weeks. As shown, IVE’s momentum improved over the last four weeks and its relative strength versus IVW slightly improved as well. Based solely on this graph it appears the value trade is still on. Note, the axes are represented in standard deviations. A level of 2 or more is strong but may warn a trend is nearing a possible reversal.

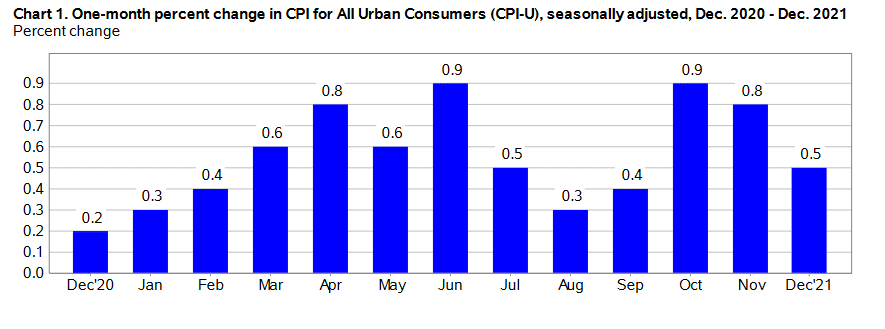

CPI

The BLS CPI report came in largely as expected. Monthly CPI rose half a percent, which is a slight reprieve from last month’s .8% increase. The annual inflation rate is now 7-percent, the highest since March of 1982. The core inflation rate, the Fed’s preferred inflation gauge, rose to 5.5% annually. This level excludes food and energy prices. The breadth of the report remains troubling. Over half of the 251 subcomponents rose by more than 5-percent and a fifth of them rose by more than 10-percent. On an annual basis, the only major component increasing less than the Fed’s 2-percent inflation objective is medical care.

The Math Behind CPI

Why did the annual inflation rate increase despite the monthly rate falling from the previous month? The chart below from the BLS helps us answer the question. As we see below, the monthly rate fell from .8% to .5%. However, when we compute the annual inflation rate, the latest figure, 0.5%, replaces last December’s 0.2%. Next month, we need to see monthly inflation of 0.2% or lower to see a decline in the annual inflation rate. It will probably not be until March or April until the annual rate declines. At those points in time, it becomes more likely the monthly inflation rates are lower than those of a year ago.

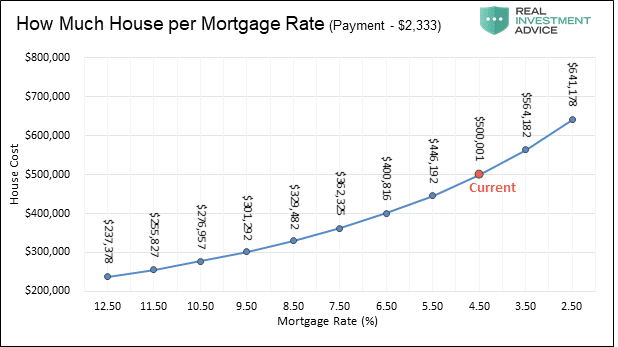

Mortgage Rates Matter

Since August, mortgage rates have been risen by 0.75% as shown below. While the rate increase may seem small it can have a big effect on mortgage payments and how much house a prospective homebuyer can afford. The second graph from our 2018 article The Headwinds Facing Housing demonstrates this.

“The sensitivity of mortgage payments to changes in mortgage rates is about 9%, meaning that each 1% increase or decrease in the mortgage rate results in a payment increase or decrease of 9%. From a home buyer’s perspective, this means that each 1% change in rates makes the house more or less affordable by about 9%.”

Needless to say, the recent increase in mortgage rates is certain to restrain further house price appreciation and may actually cause them to decline. A continuation of the trend upwards in mortgage rates further increases the odds that home prices fall.

Chasing AMC? Buy Video Games Instead

Over the past year, one of the more famous “meme” stocks was AMC Theaters. Individuals ran the stock price “to the moon” on the assumption that somehow a return from the pandemic would mean a surge in theater profitability. It was a faulty premise, to begin with, but with 7-percent inflation, the return to profitability will become even more challenging.

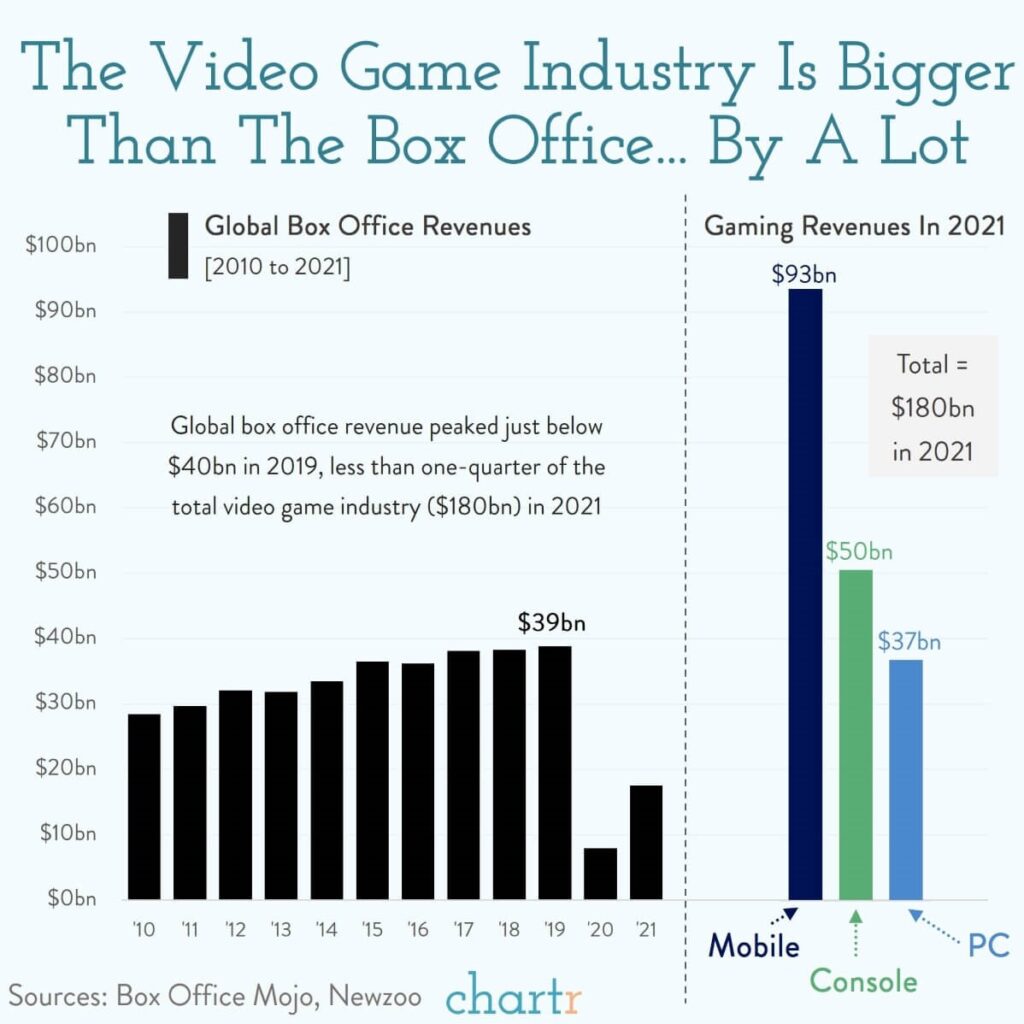

However, as noted by Chartr, gaming revenues are where it’s at. To wit:

“The chart below gives some context on just how big the video game biz is. Last year the video game industry was pegged at somewhere around $180bn by Newzoo. That’s roughly ten times what the global movie industry brought in at the box office last year. Ten times. Admittedly last year the movie industry was still dealing with a pandemic hangover, but even in its best ever year the box office only brought in $39bn.

Video games may not carry the cultural impact of movies yet, but as a market they are in a completely different league.“

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.