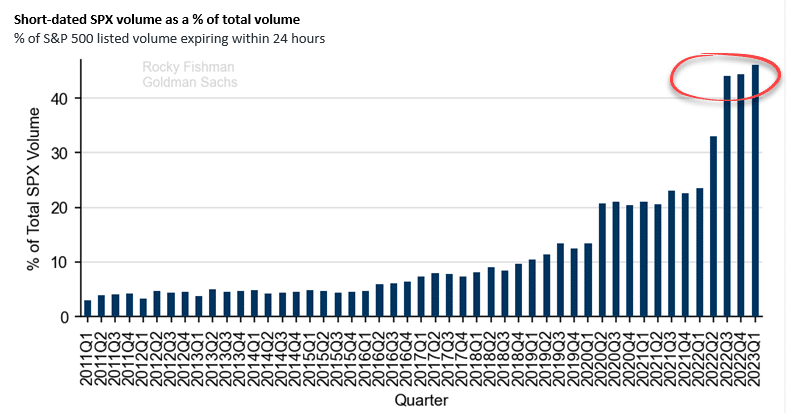

Despite its growing popularity among retail investors and influence on markets, 0DTE is probably a term most investors are unaware of. 0DTE stands for zero days until options expiration. These are put-and-call options on individual stocks and indexes that expire within 24 hours. As the graph from Goldman Sachs shows, almost half of the options volume on the S&P 500 is 0DTE. Such dwarfs the single-digit rates existing before the pandemic.

Given the extremely limited amount of time until expiration on these options, most of the activity in 0DTE options is likely due to speculators. In many cases, volume on 0DTE options spikes before important economic data releases. Wall Street banks who are on the other side of 0DTE trades must hedge them. To do so, they buy or short the underlying index as it moves in favor of the options owner. The growing concern is that as 0DTE option interest grows, dealers must actively hedge larger amounts. If the options trades are correct, bullish or bearish, banks would have to buy or sell aggressively. Such could exaggerate an already significant market move. It’s not unrealistic to consider the markets may be capable of daily moves exceeding 5% purely due to options hedging.

What To Watch Today

Economics

- 7:00 a.m. ET: MBA Mortgage Applications, week ended Jan. 13 (1.2% prior)

- 8:30 a.m. ET: New York Fed Services Business Activity, January (-17.5 prior)

- 8:30 a.m. ET: Retail Sales Advance, month-over-month, December (-0.9% expected, -0.6% prior)

- 8:30 a.m. ET: Retail Sales Excluding Autos, MoM, December (-0.5% expected, -0.2% prior)

- 8:30 a.m. ET: Retail Sales Excluding Autos and Gas, MoM, December (0.0% expected, -0.2% prior)

- 8:30 a.m. ET: Retail Sales Control Group, December (-0.3% expected, -0.2% prior)

- 8:30 a.m. ET: PPI Final Demand, month-over-month, December (-0.1% expected, 0.3% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, MoM, December (0.1% expected, 0.4% prior)

- 8:30 a.m. ET: PPI Excluding Food, Energy, and Trade, MoM, December (0.2% expected, 0.3% prior)

- 8:30 a.m. ET: PPI Final Demand, year-over-year, December (6.8% expected, 7.4% prior)

- 8:30 a.m. ET: PPI Excluding Food and Energy, year-over-year, December (5.6% expected, 6.2% prior)

- 8:30 a.m. ET: PPI Excluding Food, Energy, and Trade, YoY, December (4.6% expected, 4.9% prior)

- 9:15 a.m. ET: Industrial Production, MoM, December (-0.1% expected, -0.2% prior)

- 9:15 a.m. ET: Manufacturing (SIC) Production, December (-0.2% expected, -0.6% prior)

- 9:15 a.m. ET: Capacity Utilization, December (79.5% expected, 79.7% prior)

- 9:15 a.m. ET: Business Inventories, November (0.4% expected, 0.3% prior)

- 10:00 a.m. ET: NAHB Housing Market Index, January (31 expected, 31 prior)

- 2:00 p.m. ET: Federal Reserve Releases Beige Book

- 4:00 p.m. ET: Net Long-Term TIC Flows, November ($67.8 billion)

- 4:00 p.m. ET: Total Net TIC Flows, November ($179.9 billion)

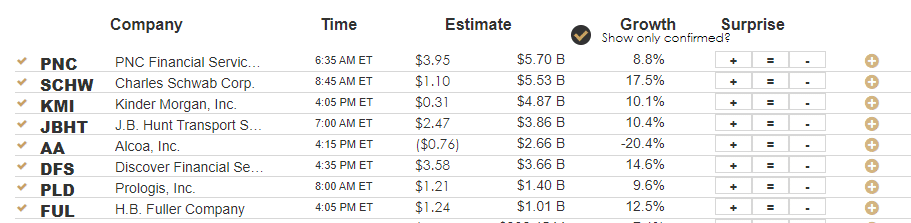

Earnings

Market Trading Update

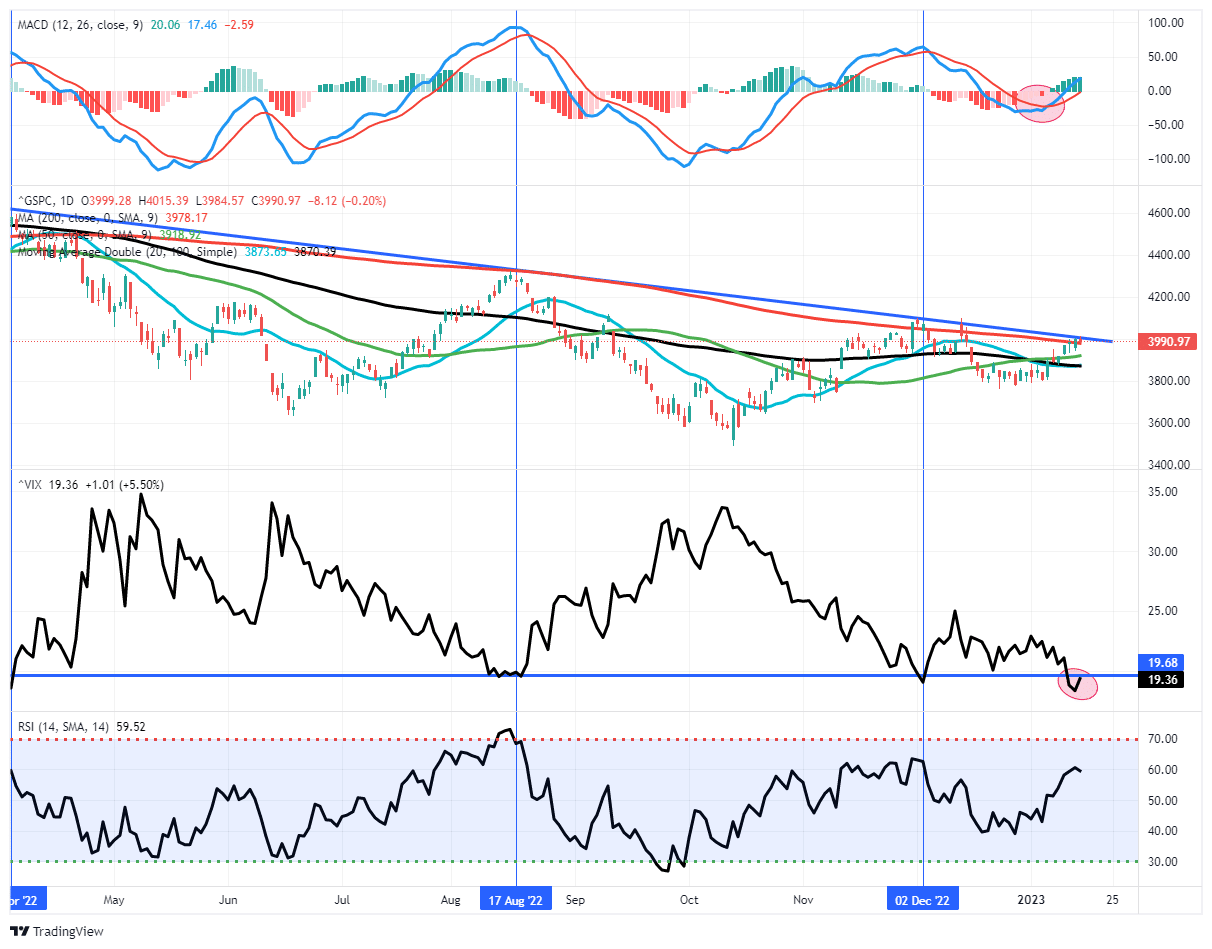

The market struggled with the first attempt to break above the 200-DMA yesterday. As earnings start to roll in, the market tone will be set by not just whether earnings can beat estimates but also what companies say about the rest of the year. As noted in yesterday’s Before The Bell video (be sure and subscribe to the channel), the “pain trade” remains higher for the moment. However, with the market’s short-term overbought condition, the market may struggle here for a few days.

However, keep a watch on that downtrend line (blue line) from the 2022 highs. A break above that level will clear the market to move higher.

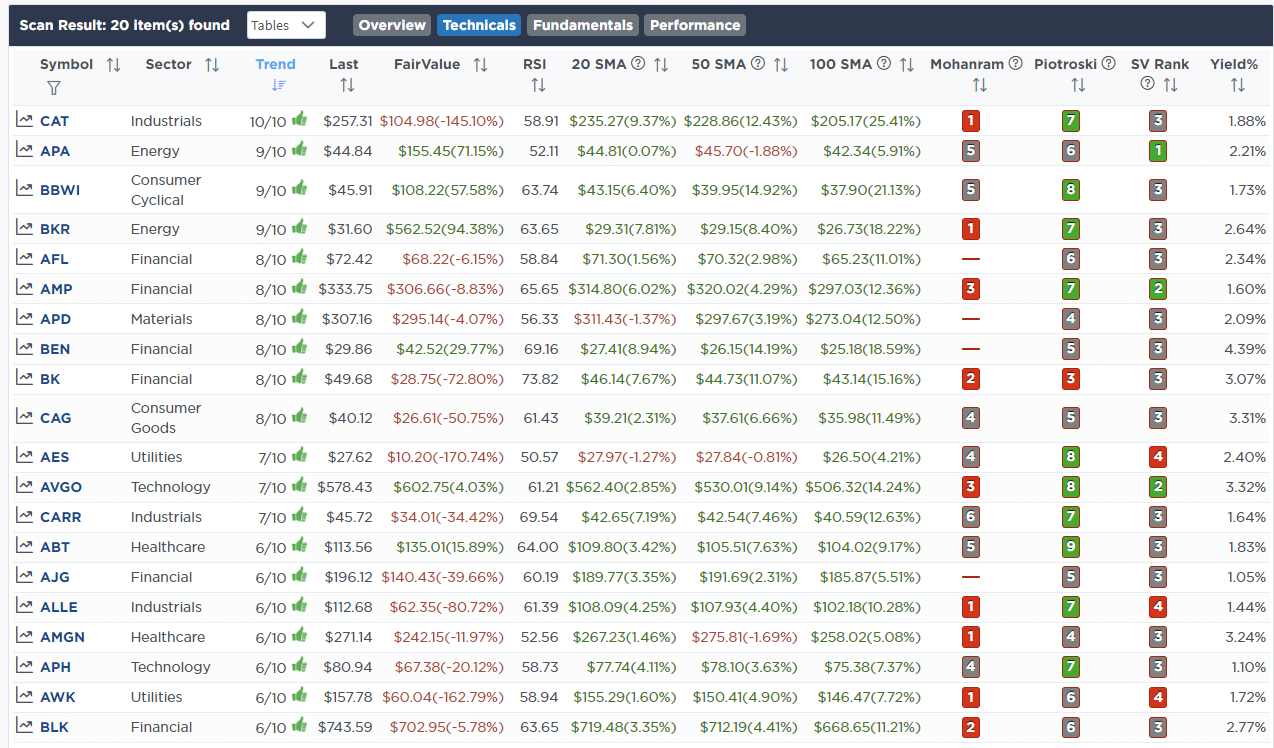

This year will likely be a year with increased volatility and a year where stock picking will win out over indexing. As such, we recommend using a product like SimpleVisor’s screener to scan for technically strong stocks with solid fundamentals and dividends. Here is a sample screen of 20 stocks in the S&P 500 that fit the list.

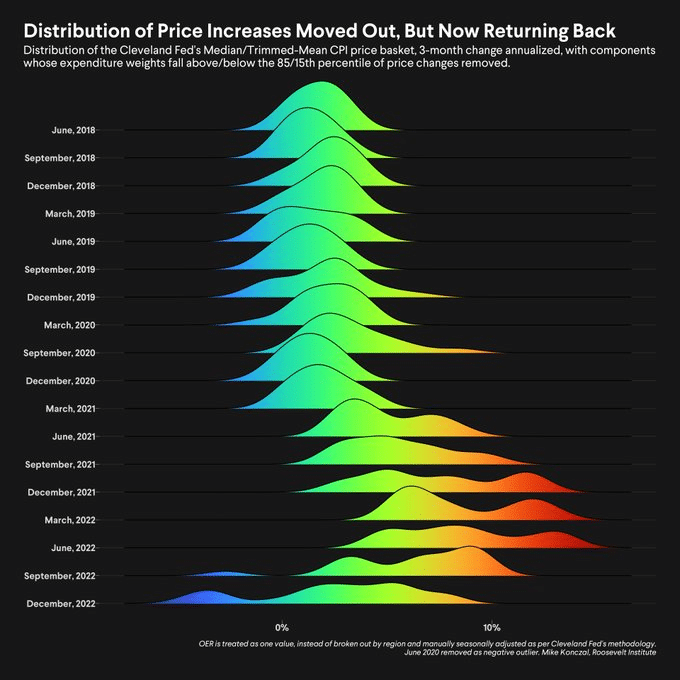

CPI Distribution is Far From Normal

The Cleveland Fed calculates a more stable version of CPI. Its trimmed-mean CPI figure excludes the goods with the top and bottom 15% of price changes. The remainder provides better information about the breadth of prices with less vulnerability to large price changes for a few items. The graph below shows how the price change distribution for individual goods has changed over the last five years.

The distribution curve was normally bell-shaped from June 2018 until the pandemic. Starting in June of 2021, when inflation started surging, the distribution became abnormal, with multiple peaks and longer tails. Recently, the range of distribution is flattening and widening. Essentially, there are few goods with price changes near the median or average. Instead, the CPI average poorly represents the bulk of price changes. Such a circumstance makes forecasting more difficult. Also note, recently there has been a growing number of goods with prices falling. As the economy and supply continue normalizing, we suspect the curve will trend toward a typical bell shape distribution.

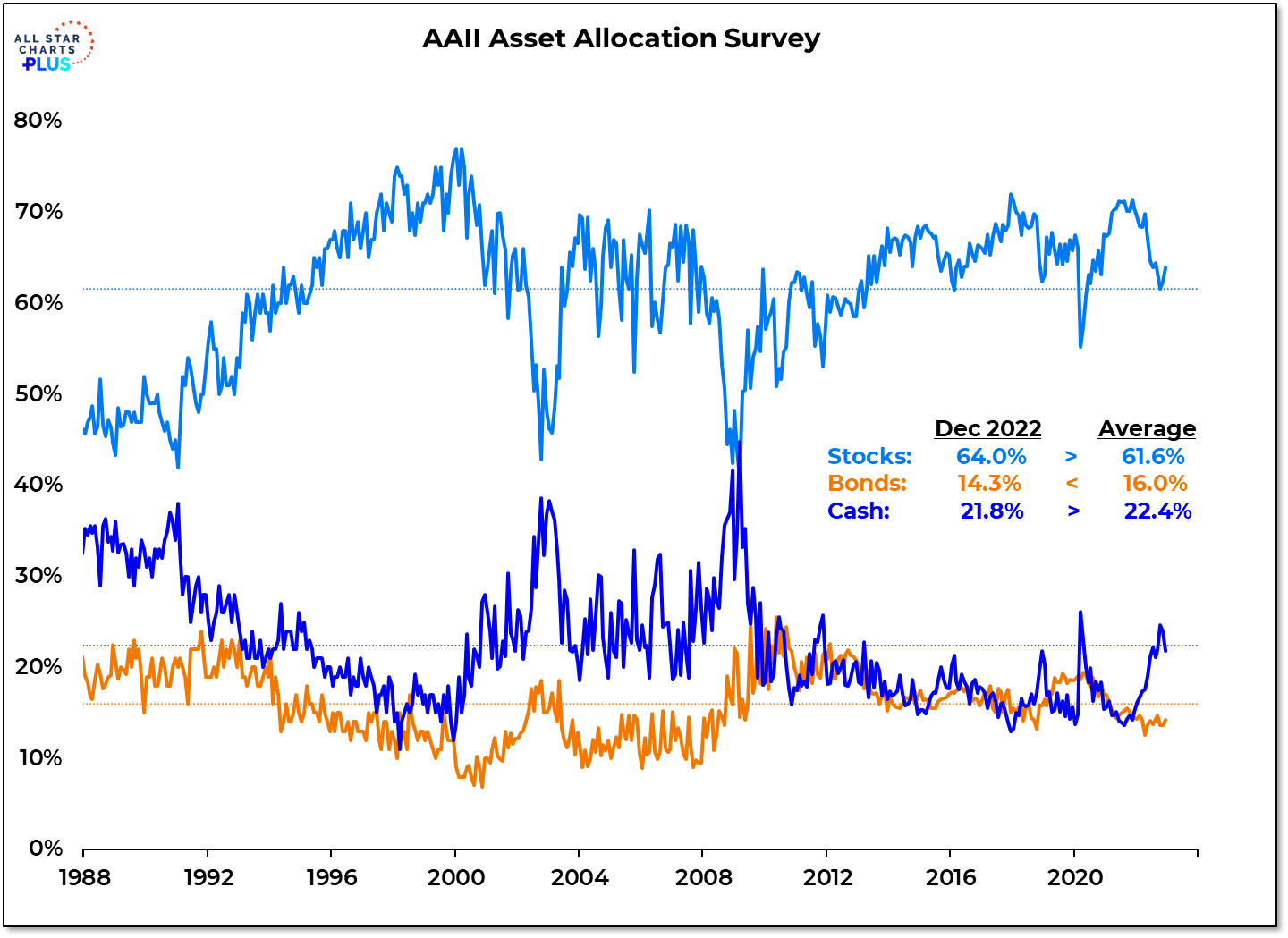

Individuals Are Not Bearish Despite What Some Surveys Say

For all the talk about rampant pessimism, retail investors are still holding stocks. The graph below shows that household equity exposure remains above its long-term average despite last year’s bearish trends and bearish sentiment surveys. Further, despite high yields, bonds and cash remain slightly below longer-term averages.

Interestingly, via its Global Fund Manager Survey, Bank of America claims that institutional investors may be leaning in the other direction. Per its survey, the number of managers claiming to be overweight equities is the lowest since 2008.

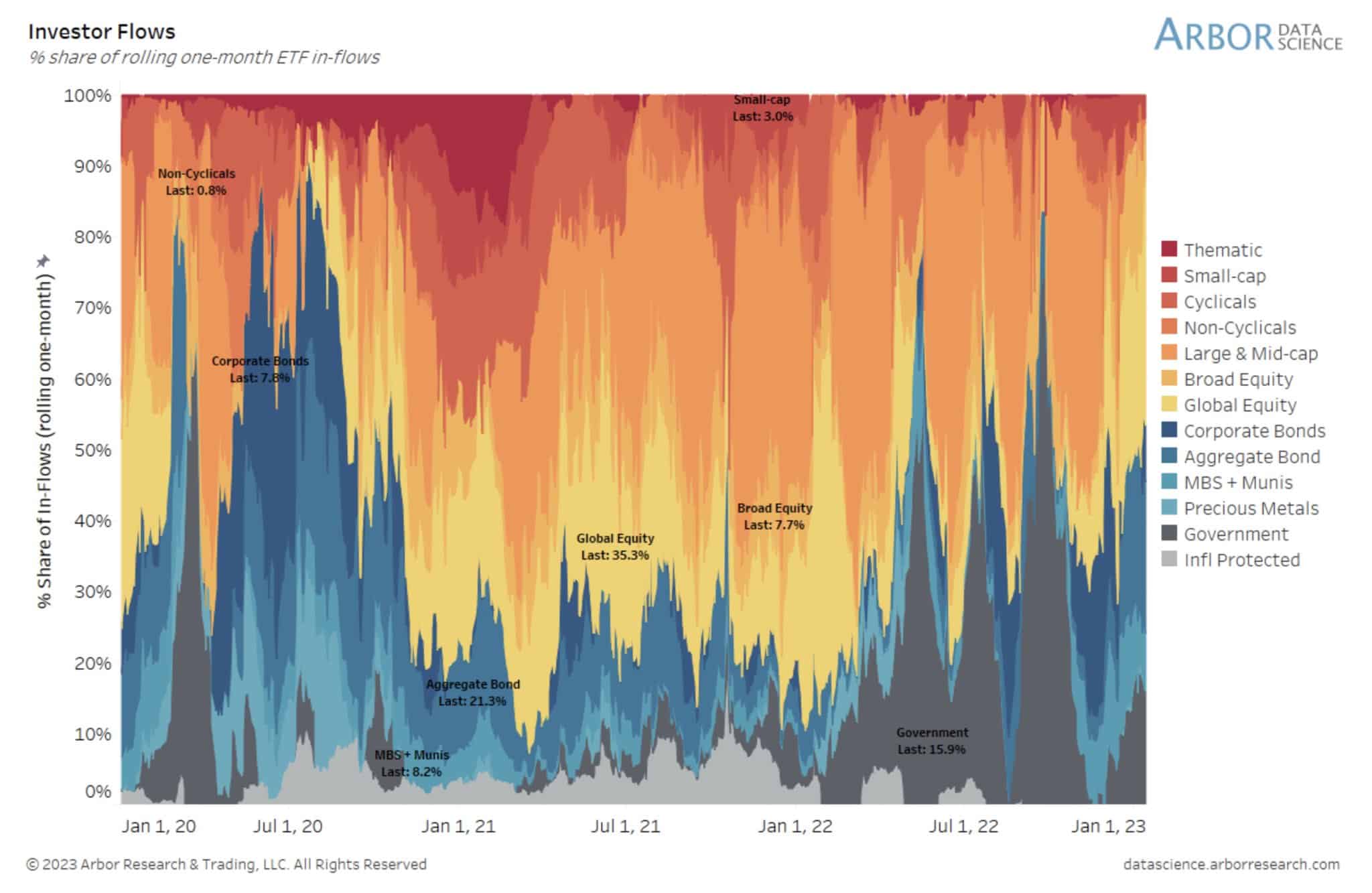

Who Is Buying This Rally?

The graph below shows investors are not piling into the riskier sectors despite the recent rally. The bulk of the investor inflows over the past few weeks are concentrated in government, aggregate bond funds and international markets. The riskier sectors like thematic, small-cap, and cyclical stocks are actually seeing a slight decline in their share of investors’ inflows. If the rally continues, we would like to see the riskier sectors garnering more significant inflows with fewer inflows to the more conservative sectors.

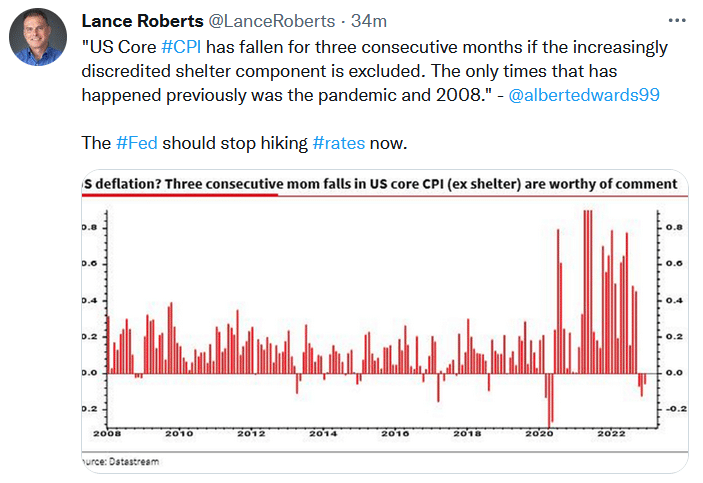

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.