Most equity markets are opening flat this morning, appearing unfazed with Chairman Powell’s important speech tomorrow. On the contrary, the VIX volatility index is showing some concern, up 4%, and worth keeping an eye on today. Click HERE to receive our daily market commentary in your email every morning and keep up to date on the coming Jackson Hole Conference.

What To Watch Today

Economy

- 8:30 a.m. ET:Initial jobless claims, week ended August 21 (350,000 expected, 348,000 during prior week)

- 8:30 a.m. ET: Continuing claims, week ended August 14 (2.772 million expected, 2.820 million during prior week)

- 8:30 a.m. ET: GDP annualized quarter-over-quarter, Q2 second estimate (6.7% expected, 6.5% in prior print)

- 8:30 a.m. ET: Personal consumption, Q2 second estimate (12.2% expected, 11.8% in prior print)

- 8:30 a.m. ET: Core PCE quarter-over-quarter Q2 second estimate (6.1% expected, 6.1% in prior print)

- 11:00 a.m. ET: Kansas City Fed Manufacturing Activity Index, August (25 expected, 30 in prior print)

Earnings

Pre-market

- 6:55 a.m. ET: Dollar General (DG) is expected to report adjusted earnings of $2.61 per share on revenue of $8.62 billion

- 7:00 a.m. ET: The JM Smucker Co. (SJM) is expected to report adjusted earnings of $1.86 per share on revenue of $1.80 billion

- 7:30 a.m. ET: Dollar Tree (DLTR) is expected to report adjusted earnings of $1.01 per share on revenue of $6.45 billion

Post-market

- 4:05 p.m. ET: Peloton (PTON) expects to report adjusted losses of 39 cents per share on revenue of $929.16 million

- 4:05 p.m. ET: HP Inc. (HPQ) expects to report adjusted earnings of 84 cents per share on revenue of $15.93 billion

- 4:15 p.m. ET: The Gap (GPS) is expected to report adjusted earnings of 46 cents per share on revenue of $4.13 billion

Politics

- The Federal Reserve‘s annual Jackson Hole Symposium kicks off virtually tomorrow.

- President Biden is focusing overseas today, receiving updates on Afghanistan and meeting with Naftali Bennett, Israel’s new prime minister. Bennett says he wants a reset from recent turmoil in the relationship with the U.S.

Courtesy of Yahoo

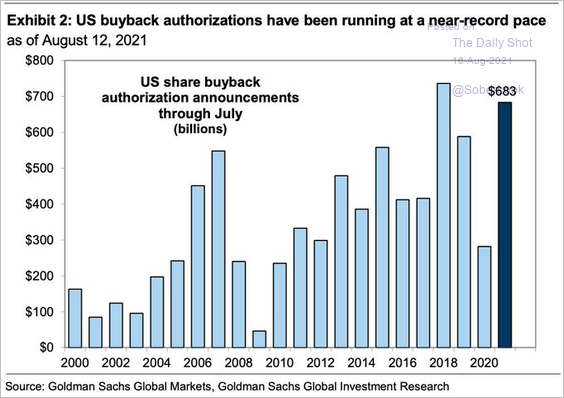

The Best Support For The Markets Storm Back

“In the years before the COVID-19 pandemic, one of the biggest sources of buying power in the stock market were the companies themselves.

At the post-crisis buyback peak of March 2018, members of the S&P 500 had spent a collective $823.2 billion repurchasing shares of their own company over the prior 12 months, a pace of more than $200 billion per quarter. During the second quarter of last year, in contrast, S&P 500 members spent a mere $88.7 billion repurchasing their shares.

But as the economy has improved, the stock market has rallied, and management teams can reward shareholders rather than hunker down to survive a recession, corporate buyers have returned as a force in the stock market.

Data from Bank of America Global Research published Tuesday showed that last week corporations spent the most repurchasing their own shares in more than five months.

‘Buybacks by corporate clients accelerated from the prior week to the highest level since mid-March, driven by Financials,” the firm said in a note to clients. “Financials has now overtaken Tech as the sector with the largest dollar amount buybacks so far this year.'” – Yahoo

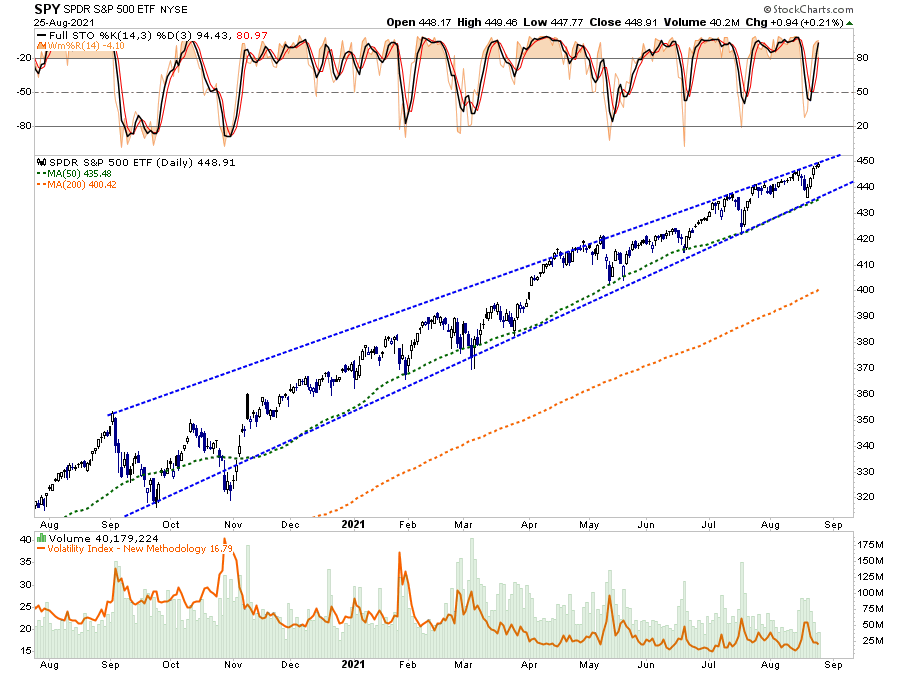

A Very Defined Channel

Since last November the market has traded in a very defined channel which is become more narrow. Importantly, there is a “dearth of buyers” as volume collapses on rallies with volatility spikes becoming more suppressed. At some point, the market will break out of this channel and there will be a big move in whatever direction that is. We suspect that move will be lower as volatility returns to the market.

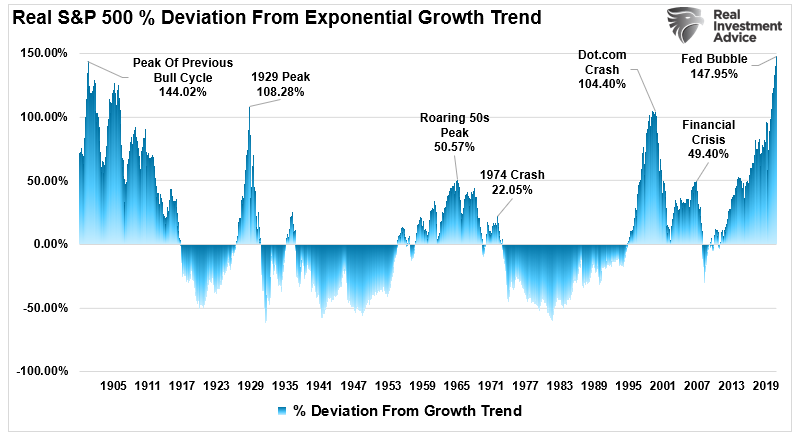

A Historical Deviation Extreme

Using Shiller’s monthly inflation-adjusted data from 1900-Present, the S&P 500 is more extended from the long-term exponential growth trend that at the peak of the markets in 1903, 1929, and 1999.

This time is truly different.

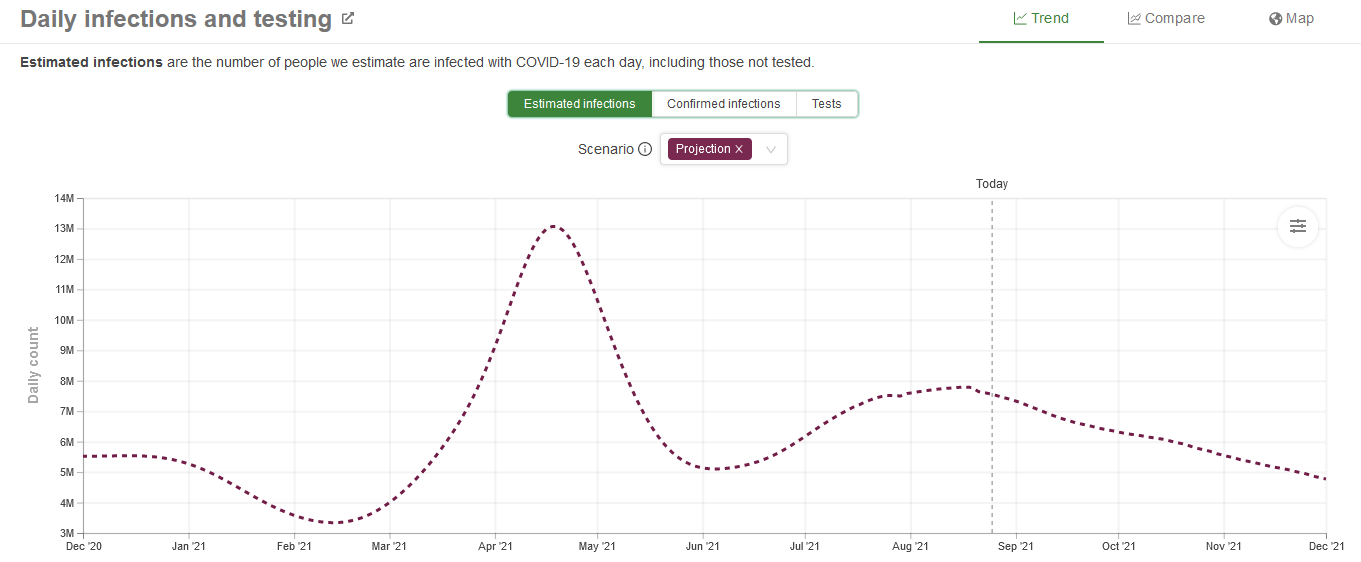

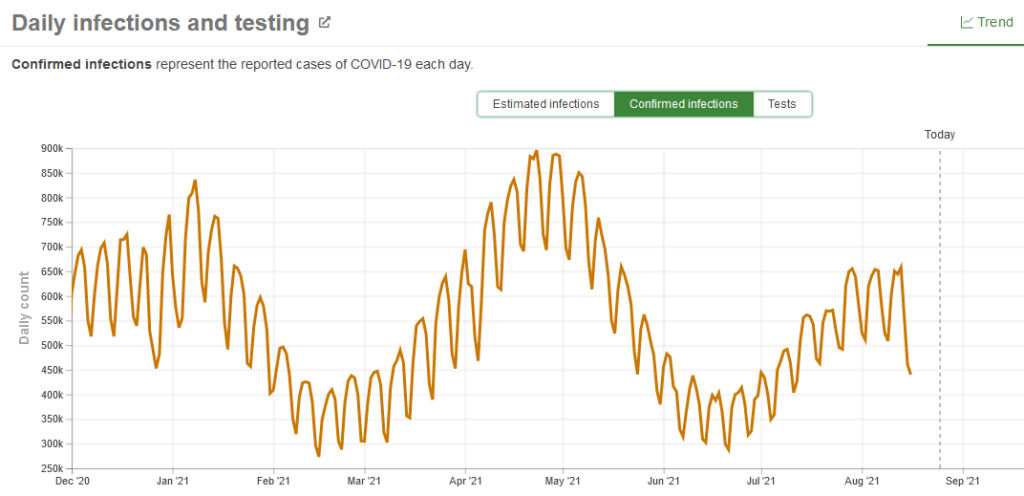

Fading The Delta Variant

Markets jumped earlier this week upon the announcement the Fed’s Jackson Hole conference is virtual. The market’s assumption being the Fed is worried about the variant and therefore likely to downplay taper given new vulnerabilities to the economy. The reality is that new Delta cases appear to be falling. The graphs below from IHME/University of Washington show confirmed infections are stabilizing or declining and IHME’s estimates are also moving lower.

Return of Meme Stocks

Biden’s Approval Rating

The graph below, highlighting President Biden’s declining approval rating, is an important macro factor emerging on the horizon. There are two points in regards to his ratings worth keeping an eye on.

First, Biden will try to improve his ratings. Will he push legislation for even more fiscal stimulus or other economic boosting measures to win approval? In a similar vein, will he back off on tax increases?

Second, will some Democratic Senators and Representatives, especially those facing tight reelection campaigns in a year, start to shy away from the President? If so, winning their votes for infrastructure, the budget, or anything else will become tougher.

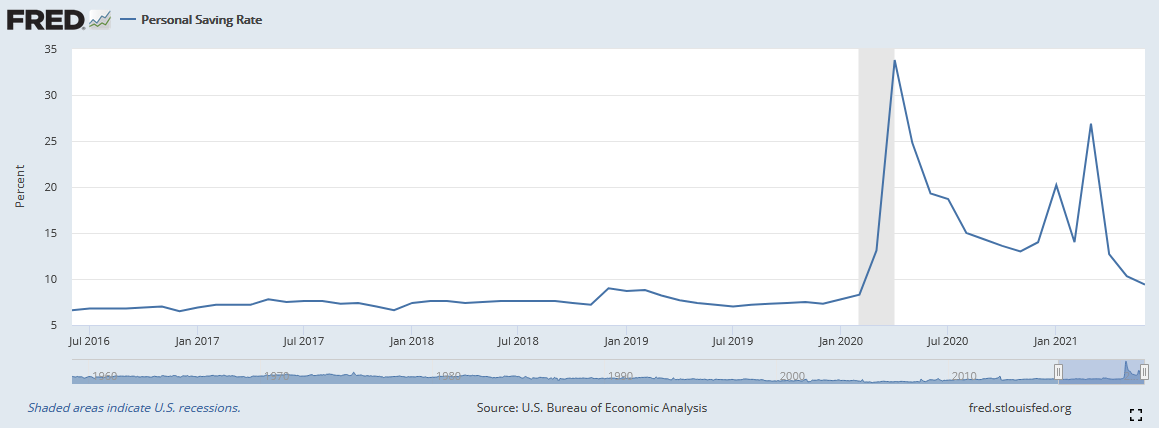

Savings Rate Normalizing

The savings rate spiked early in the pandemic due to the abundance of fiscal stimulus sent directly to individuals along with less consumption as important segments of the retail economy were shut down. Since then, additional savings and further rounds of stimulus boosted consumption and nominal economic growth to levels last seen in the 1950s. Both sources of economic activity are coming to an end which helps partially explain why consumer confidence fell sharply last month and retail sales have been weak. The economy is slowly but surely being left to stand on its own legs. Will the Fed hold of tapering QE as economic reality emerges?

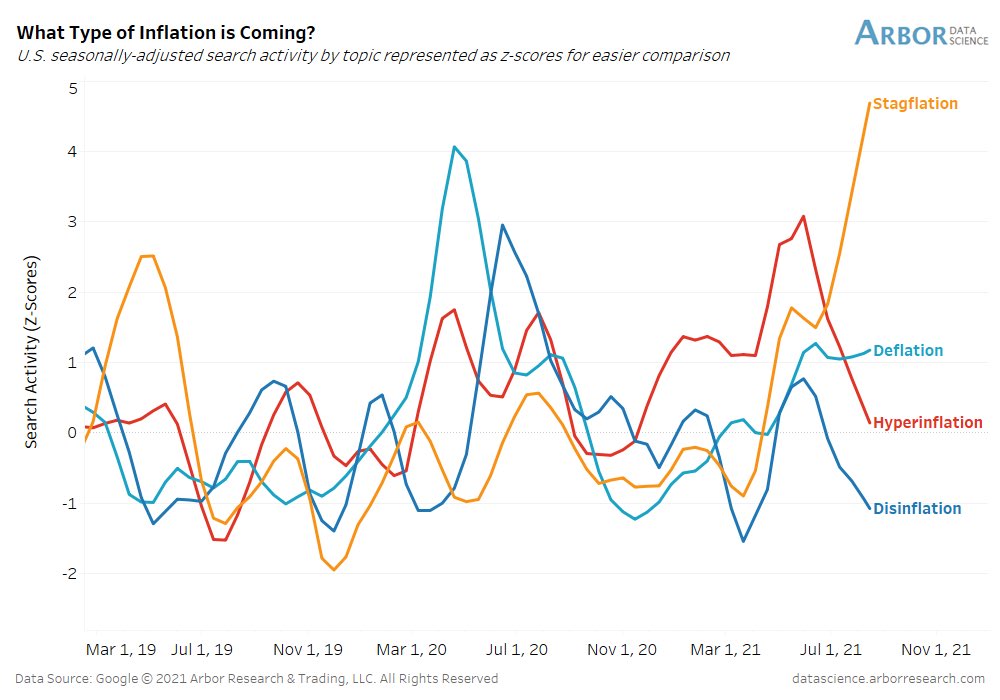

Which ‘Flation?

The graph below from Arbor Research provides a clue for the recent decline in consumer confidence. Based on Google search data, the term stagflation is now the leading ‘flation search word. Stagflation entails weak economic activity coupled with inflation. Stagflation results in higher unemployment and negative real wage growth.