The Fed and economists are encouraged because CPI is down to 3.3% from a high of nearly 9% in 2022. Despite the Fed’s “significant progress” in lowering inflation, most citizens are outraged and confused by economists’ relatively rosy inflation observations. Most citizens believe inflation is still rampant.

The Fed and economists are correct in that inflation is now tame. At the same time, citizens dissatisfied with high prices have solid grounds on which to base their disapproval.

Let’s better understand how such contradictory beliefs can both be factual. Furthermore, in the process, we can help Jerome Powell understand why economic sentiment is poor despite a near-record low unemployment rate.

You know, I don’t think anyone knows, has a definitive answer why people are not as happy about the economy as they might be. -Jerome Powell 6/12/2024

Visualizing Divergent Inflation Opinions

The graph below of the BLS CPI New Vehicles price index, a CPI component, demonstrates why economists and citizens have such grossly contrasting opinions of inflation.

Economists focus on the blue line, graphing the year-over-year change in new vehicle prices. Over the last year, the price index of new vehicles has decreased by .60%. Economists can say the cost of buying a new vehicle is in a deflationary state.

While the chart may warm the hearts of economists and the Fed, most individuals see the orange line, the CPI price index for new vehicles instead. It shows that new vehicle prices are up about 20% since the pandemic. Yes, they may have recently declined slightly, but today’s prices are nowhere close to where they were four years ago. In their minds, there is significant inflation in new vehicles.

Economists Prefer Growth Rates, Not Absolutes

Ask an economist what the nation’s GDP is, and they will quote an annualized growth rate to a decimal point. We bet almost all of them will get the answer correct within one or two-tenths of one percent.

Ask them again, but request the answer in dollars. It would not be surprising if many economists are off by a trillion or even two trillion dollars, representing anywhere from 3.00% to 7.00% of the economy.

Economists prefer to analyze and quote many economic data points in terms of percentage change. For instance, how much did industrial production or retail sales change versus last month or over the previous quarter or year? They vastly prefer growth rates because it gives them a comparable and insightful way of analyzing economic data. Let’s review why this is the case.

Comparative Analysis

Economists are more adept at comparing data from different periods, industries, and countries if they have a common measurement calculation. Instead of absolute change, which doesn’t account for the starting point, a growth rate captures the absolute change and the starting point. Consider the following:

If GDP increases by $1 trillion this year, how would that compare to a $1 trillion increase in 2000? The question is challenging to answer using absolute numbers. However, growth rates allow us to evaluate the two periods quickly. Today, GDP is $28.284 trillion; therefore, a $1 trillion increase would represent 3.50% growth. In 2000, GDP was close to $10 trillion. Adding a trillion dollars of economic growth would have resulted in a 10% growth rate. While a trillion dollars is a trillion dollars in absolute terms, there is a stark difference between 10% and 3.50% growth.

Trend Analysis

Growth rates highlight trends and changes over time more clearly than absolute numbers. They can show whether an economy is accelerating, decelerating, or maintaining a steady pace.

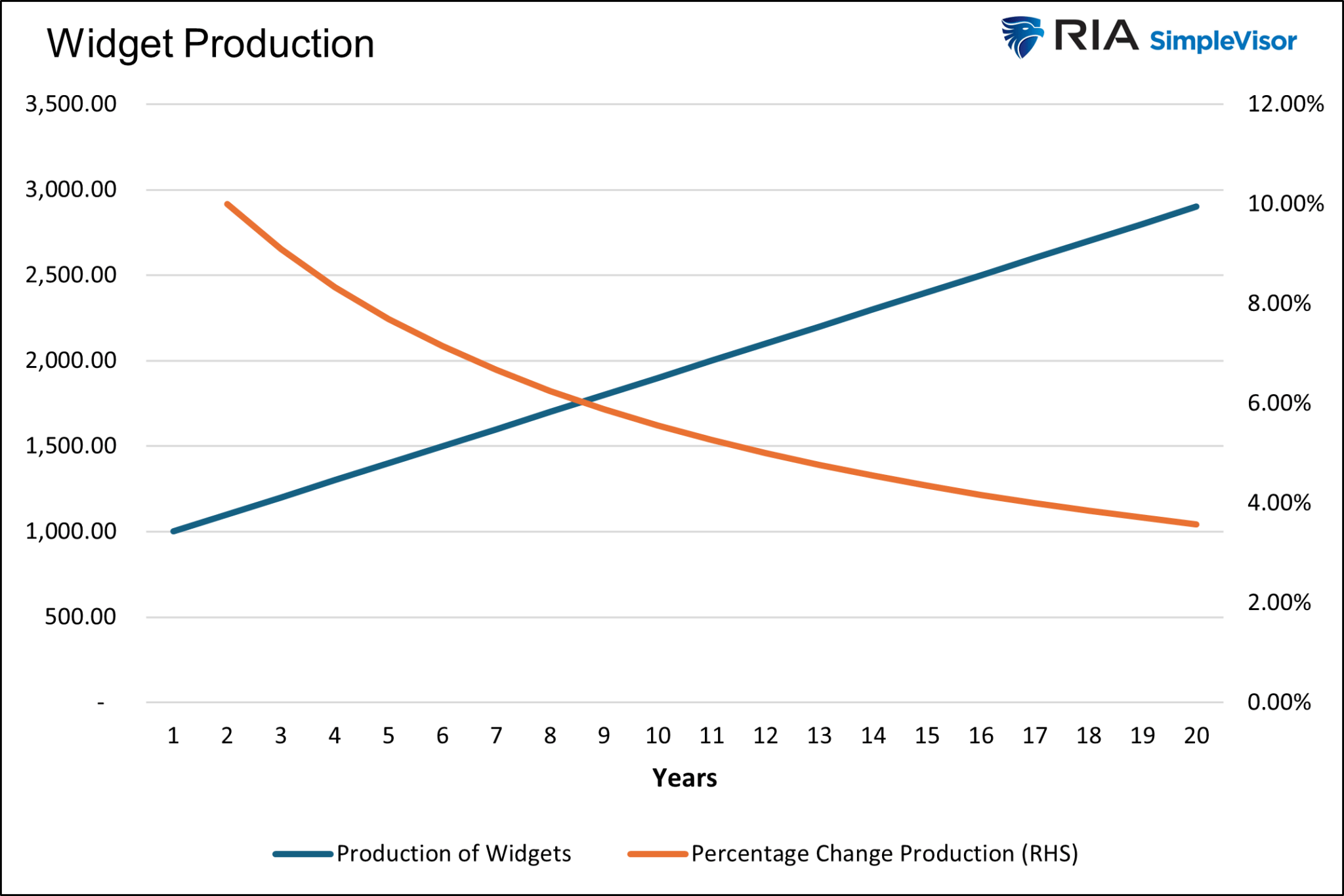

Consider the graph below. The blue line, showing the make-believe production of widgets, starts at 1,000 widgets and increases by 100 widgets annually. The steady growth in absolute terms is a linear upward trending line. However, the annual growth rate steadily declines from 10% to 4% by year 20. An economist looking at the graph would say the rate of the production of widgets is declining despite the upward trend in the number of widgets being produced annually.

Policy Decision Making

The Fed aims to promote stable economic growth. To do so they balance the level of interest rates with inflation and economic activity. Having like figures to analyze, such as growth rates, makes their task significantly more straightforward. Imagine if the Fed had to determine the appropriate interest rate given that the economy grew by $750 billion last year and the CPI price index rose by 2.45.

Investors prefer growth rates for the same reason. If I can estimate the economy’s growth rate and other critical economic figures, they can better determine a growth rate or interest rate they would accept for taking risks.

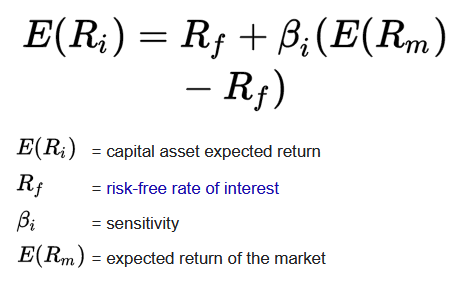

The capital asset pricing model (CAPM) is a bedrock for finance. The formula states that an asset’s expected return should equal the risk-free interest rate plus the asset’s sensitivity (beta) times the market’s expected return. This formula can only work with growth rates, not absolute numbers.

Consumer’s Point Of View

Regarding inflation, consumers are less concerned with growth rates and heavily focused on absolute prices. They remember that bread used to cost $4 a loaf and now costs $7. The graph below shows the price of white bread was stable between $1.25 and $1.50 a pound from 2008 to the pandemic. It is now close to $2 a pound.

That is significant inflation. But it doesn’t tell the whole story. If wages also rose similarly, purchasing power hasn’t changed. It is similar to hearing stories from your parents or grandparents about going to the movies and getting popcorn and a soda, all for $1. Did you ever ask them how much money they made at the time?

Summary

We want to make it clear that we do not condone inflation. It accelerates an already wide wealth gap and creates hardships for many citizens. For more, please read our article, Fed Policies Turn The Wealth Gap Into A Chasm.

We analyze inflation data similarly to economists. We accept that absolute prices are much higher today than a few years ago, but we also acknowledge that, in general, wages are higher as well. Just like we can’t realistically compare a 15-cent McDonald’s hamburger to a $3.00 one today, we should be careful comparing prices today to their prices a few years ago.

Prices are not returning to 2020 levels. In fact, any hint that aggregate prices retreat from current levels will cause the Fed to panic and quickly stimulate inflation via lower interest rates and QE. We remind you that the Fed was lamenting that we didn’t have enough inflation throughout most of the period between the financial crisis and the pandemic.