What Causes “Transitory” Inflation to Become “Persistent”?

You are the CEO of Acme Widget Factory. Among your many duties is overseeing production and profit margins related to your core product, widgets. Competition in your industry is stiff, with over a half dozen widget producers.

The pandemic and recovery are throwing the widget industry for quite a loop. In the spring of 2020, there was no demand for widgets. You laid-off employees and limited production while focusing on survival. During the summer of 2020, fiscal stimulus was percolating through the economy, and demand soared. It continues at a robust pace.

Acme’s future is brighter, but as CEO, you face a new set of problems. Your factories are running at full force, as are your competitors, but demand appears insatiable. At the same time, the prices of the materials needed to make widgets keep rising. Further, new and existing workers are demanding higher wages.

The problem facing Acme’s CEO is occurring in executive suites across America. Their decisions about how to navigate through 2022 and beyond in this unprecedented period illuminates a potential source for “persistent” inflation.

Acme Widgets

The price of widgets is up 20% in just the last year. However, demand weakens with each recent price increase. In economic speak, demand for widgets is elastic. Consumers demand fewer widgets as prices rise.

Even with the slight reduction in demand, the industry cannot produce enough widgets. The good news is profit margins are higher than average as widget prices are rising faster than expenses.

As the CEO of Acme, you have a tough decision to make. Do you keep production capabilities as is or boost production with a new factory and more employees?

The CEO’s Transitory Dilemma

The biggest unknown you, the CEO, face in making the decision above is forecasting the future. In particular, the following questions:

- How will widget sales be in 2023 and beyond?

- Will input prices continue to rise?

- Can you pass on rising costs to consumers?

- Assuming inflation remains hot, will employees demand higher wages and more benefits?

- If needed, can I even hire more capable employees?

Most CEOs closely track economic activity and forecasts. Unless they are hiding under a rock, they recognize recent economic strength is primarily driven by the pandemic – specifically, the government’s massive spending and benefits programs.

CEOs, aiming to make the right decisions, must appreciate the economy’s heavy reliance on Washington in their strategic plans.

The President and Democrats are trying to keep money flowing through the economy. They are currently proposing massive spending bills. Blocking their plans is the upcoming 2022 midterm elections. Political games will make it much trickier to pass spending bills than in 2020. Democrats in office realize weak economic growth is not a winning ticket. Those Republicans, wanting their seats, also understand that.

As CEO, we are beholden to our lobbyists to help us make decisions about Widget production. A strong economy typically results in better widget sales. As the economy continues to re-open and consumer behaviors normalize, personal consumption is likely to revert to longer-term averages unless Uncle Sam continues to be very generous to consumers.

As the CEO, we must determine if continued massive fiscal spending is likely or a one-time pandemic action.

The Fed’s Opinion

CEOs also need to decipher what the Fed thinks of future economic growth and how they may steer policy.

Per the Fed- “The Federal Reserve Board employs just over 400 Ph.D. economists, who represent an exceptionally diverse range of interests and specific areas of expertise.”

The Fed has the greatest army of economists in the world. What they say and their economic forecasts should have a profound impact on our decisions. Unlike guessing about how Washington plans on spending money, the Fed is easier to decipher.

Transitory

Via official policy statements and minutes, the Fed describes the recent bout of strong economic growth and inflation as “transitory.” By this, they suggest economic growth will moderate, and swelling inflation will revert to norms.

According to Merriam-Webster’s dictionary, transitory implies a short period.

Transitory is a vague term. It can mean minutes or hours or infer years or even decades. 400+ economics Ph. D.s are not dumb. They likely chose the word because it has no clear-cut definition.

Had they defined the period of excessive price and economic growth with a specific range of months, they risk being wrong. They will be technically correct with the current phrasing if inflation and growth normalize tomorrow or in two years.

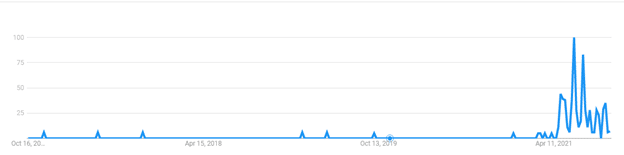

The graph below from Google Trends shows the search term “transitory inflation” is popular after being largely non-searched.

Fed Forecasts

Since the Fed is not defining transitory in terms of a specific time, we need another way to quantify their vagueness. Fortunately, the Fed’s FOMC members periodically put out expectations for growth, inflation, and unemployment. While the results are based on the forecasts of FOMC board members, we have little doubt they represent the work of the Ph.D. army.

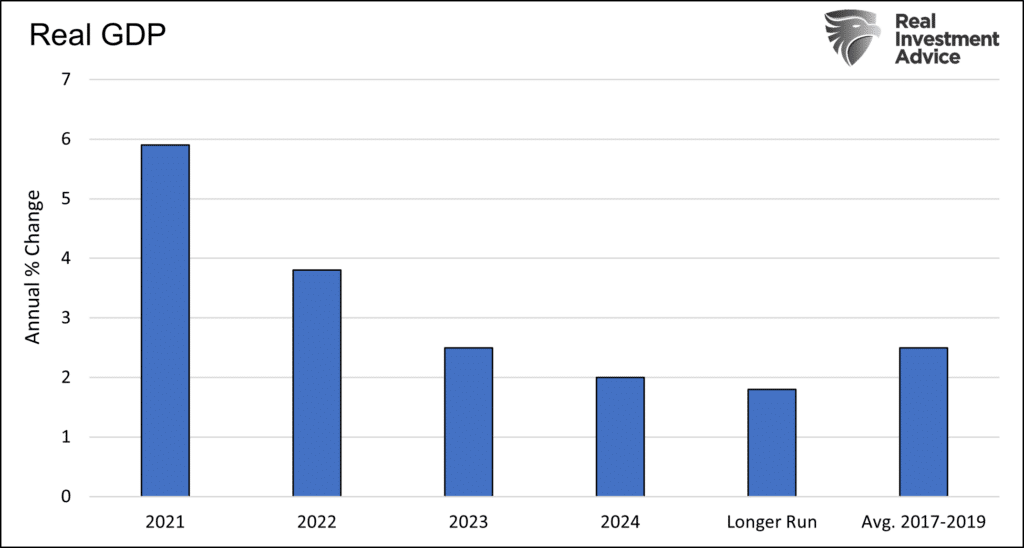

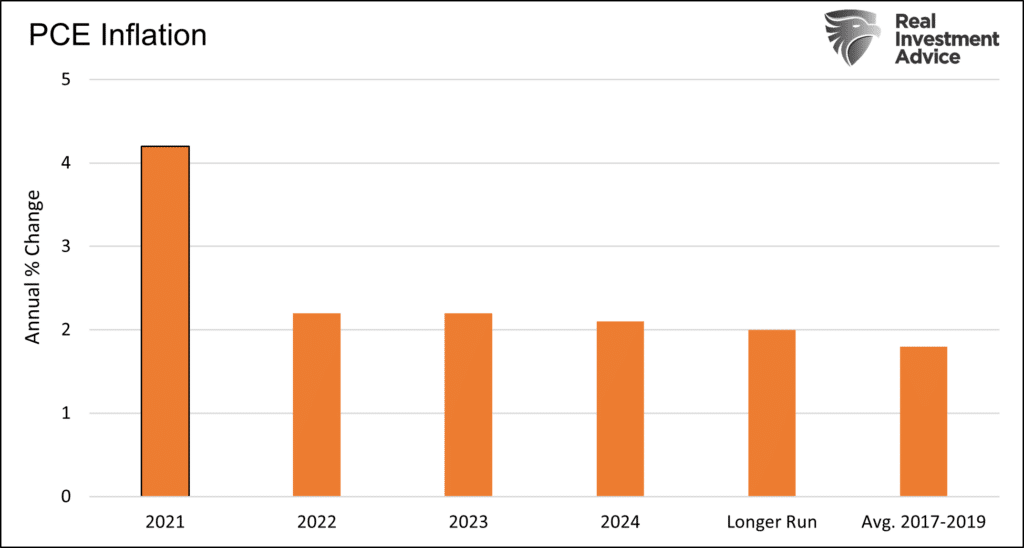

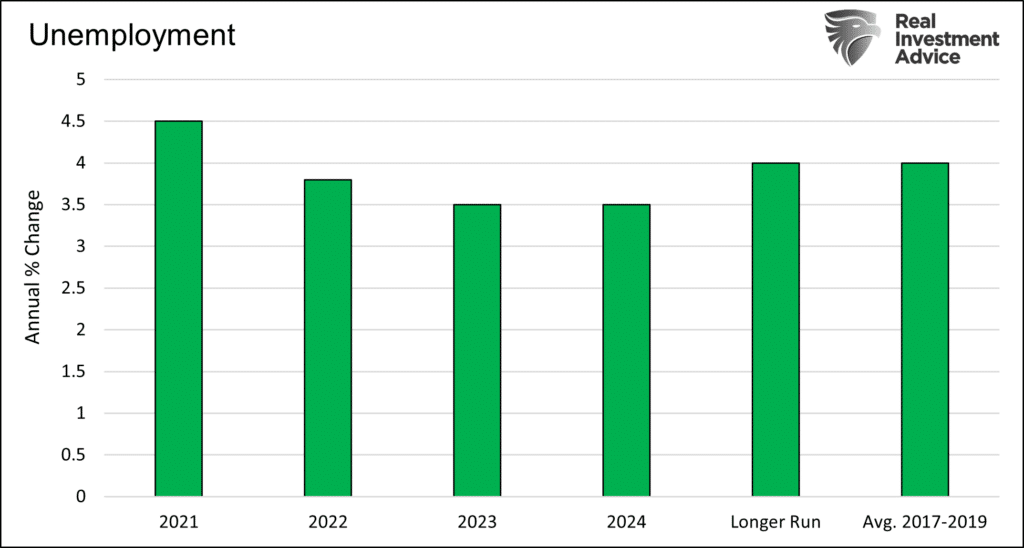

The three charts below show their expectations for the remainder of this year as well as 2022, 2023, and 2024. We also include their “long-run” forecast and the average from 2017-2019 for historical context.

The first graph points to economic growth normalizing in 2023. After that, they expect GDP growth to be weaker than pre-pandemic levels.

Inflation will return to near normal but run a little hotter than before the pandemic.

Fed members expect the unemployment rate to fall below the pre-pandemic average in 2022 and remain there for at least two more years.

Transitory vs. Persistent

With our fiscal policy expectations and the opinions of over 400 Ph. D.s, we, as CEO, have a tough decision to make. Should we construct a new factory, hire workers, and boost production to meet current demand?

If the Fed is correct, the recent boost in widget sales is transitory. Further, per their expectations, future economic growth, ergo widget sales, may be weaker than pre-pandemic levels. Adding a new factory and more workers may be profitable while the boom lasts. However, doing so may result in excess capacity and too many workers in the long run. If the industry adds production capability, supply will certainly outstrip demand and reduce prices down the road.

In addition to weaker expected economic growth, we must also consider expectations for a lower unemployment rate and higher prices than were normal pre-pandemic. In theory, those conditions should result in higher wages and production costs in a few years.

As CEO, we must think in terms of at least 5-10 years. While the current outlook is good, it may also be transitory. Per the Fed forecasts, our sales and margins are likely to shrink. Boosting capacity into such an environment seems foolish.

Taking permanent steps to cure short-term needs can be a costly trap. Unless runaway fiscal spending becomes the norm.

Conclusion

As COVID spread around the globe, economies were shuttered. At the same time, governments around the world flooded consumers and some companies with unprecedented amounts of cash.

As a result of limited production and strong demand, prices soared. This is the source of current inflation.

If demand stays high, in part due to more fiscal spending and supply lines and production remain fractured, inflation will continue to run hot. If such a scenario plays out as many CEOs decide not to invest in new production facilities, “persistent” inflation becomes much more likely.

We strip you of the CEO title. As an investor with CEO insight, you have a lot to consider. Primarily, “persistent” is not “transitory.” Nor is persistent in the Fed’s forecast. Persistent inflation requires the Fed to take detrimental actions to investors.

This is not our outlook but given the oddities of the current environment and our fiscal leaders’ carelessness, it’s one we must consider.