Annuity.

Say the word and watch facial expressions.

They range from fear, disgust, confusion.

Billionaire money manager and financial pitchman Ken Fisher appears as the senior version of Eddie Munster in television ads for his firm.

He stares. Deep eyes ablaze with intensity. The tight camera shot. A dramatic pause, then solemnly he delivers the line:

“I hate annuities. I’d rather go to hell then sell annuities.”

Which obviously means you should too. The financial professional with a net worth of 500,000 Americans put together doesn’t need to worry much about lifetime income or portfolio principal loss. Obviously, he doesn’t believe you need to, either.

No offense but…

Let’s face it.

Ken Fisher is a master marketer. There’s no doubt of his prowess to pitch his wares. He’s raised megabucks for his firm. However, what he knows academically about annuities and how they mitigate life expectancy risk can fit in to a dollhouse thimble. And that’s fair because he doesn’t need to worry about running out of wealth. You most likely do.

Based on past comments he made in print about the financial planning industry, deeming it ‘unnecessary,’ I understand why he isn’t a fan of anything or anyone but himself. If you’re close to retirement or in retirement income distribution mode, you will pay for his overconfidence.

Unfortunately, what Ken Munster (I kid), is correct about is you as a consumer and investor must be skeptical of annuities as they are customarily offered. As they ‘sold first and planned for later.’

An annuity solution shouldn’t be on the radar until holistic financial planning is completed to determine whether there’s longevity risk – a strong probability of an investor outliving a nest egg. Annuities, especially deferred and immediate income structures, take the stress off a portfolio to generate lifetime income and places that risk with insurance companies. Fixed annuities that allow owners to participate in the upside of broad stock market indexes can be used as bond replacements.

Respected Professor Emeritus of Finance at the Yale School of Management and Chairman, Chief Investment Officer for Zebra Capital Management, LLC Roger G. Ibbotson, PhD, in a comprehensive white paper released last week, outlined how fixed indexed annuities which provide upside market participation and zero downside impact may be attractive alternatives to traditional fixed income like bonds.

In an environment where forecasted stock market returns may be muted due to rich valuations and bond yields still at historic lows, FIAs eliminate downside stock market risk and offer the prospect of higher returns than traditional asset classes. Ironically, at our Clarity investment committee two weeks ago, one of our partners, Connie Mack showcased a similar strategy based on our organization’s lowered return projections for traditional stock and bond portfolios.

Per Roger Ibbotson:

“Generic FIA using a large cap equity index in simulation has bond-like risk but with returns tied to positive movements in equities, allowing for equity upside participation. For these reasons, an FIA may be an attractive alternative to (long-term government bonds) to consider.”

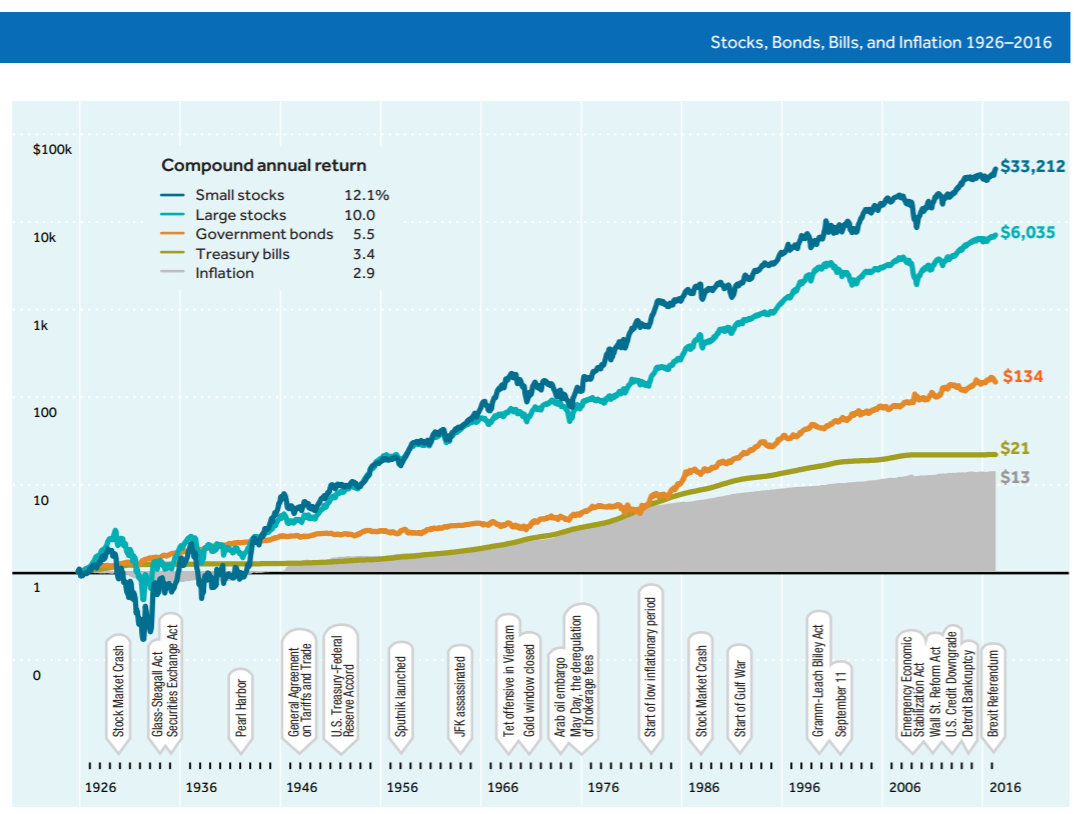

In financial services, Ibbotson is a god. Brokers and advisors have been misrepresenting to consumers his seminal chart of 100-year stock market returns for as long as I’ve been in the business. The chart outlines how domestic large and small company stocks compound at 10-12% and beat the heck out of bonds, bills and inflation; financial professionals showcase the lofty past returns and convince customers that without buying and holding stocks for the long term (whatever that is), they’ll succumb to the vagaries of inflation. Adhere to the chart and your portfolio will have it made in the shade! (if invested in stocks for 100 years plus).

In all fairness to Roger Ibbotson, it’s not his fault that his data and graphics have been used to seduce investors to bet their hard-earned wealth on investment fantasy. He’s been in favor of annuities in retirement portfolios and in accumulation portfolios leading up to retirement for a long time.

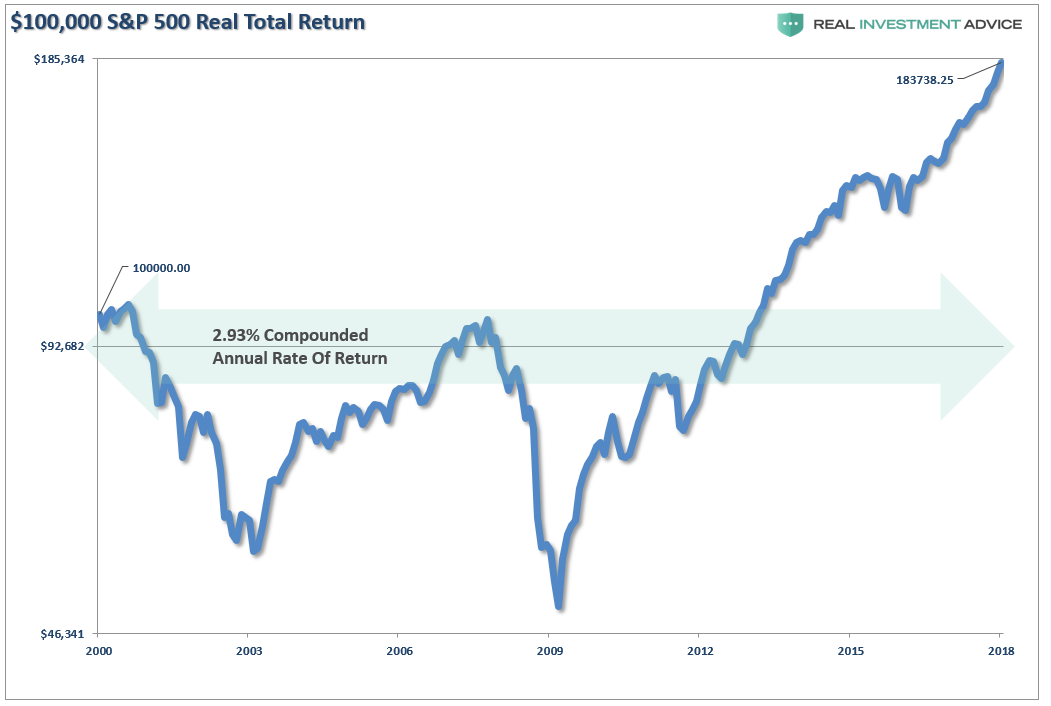

Investment fantasy:

Investor reality:

It took nearly 14-years just to break even and 18-years to generate a 2.93% compounded annual rate of return since 2000. (If you back out dividends, it was virtually zero.) This is a far cry from the 6-8% annualized return assumptions promised to “buy and hold” investors and the 10-12% promised by financial pros who misrepresent Ibbotson’s work.

Investors if lucky, have 20 years to save interrupted. As labor economist and nationally-recognized expert in retirement security professor Teresa Ghilarducci shared with us recently on the Real Investment Hour – “Life has a way of getting in the way.”

I have yet in my 28 years in the business to meet a Main Street investor who’s achieved or achieving the long-term returns displayed in Ibbotson’s chart. The information is correct; how it’s used to sucker investors into “buy & forget” portfolios regardless of valuations and market cycles is unfortunate.

It’s time to provide the real story about annuities – the most popular types available, financial guardrails or rules to consider before annuities are purchased, what consumers should look for in a product and most important, what should be avoided.

Not every annuity product is ‘the devil.’

Unfortunately, all annuity types get lumped together and blanketed by the same sordid reputation. Those who push annuities to collect attractive commissions ostensibly leave buyers confused (annuities by nature are complex), and regretful; these products are not explained well upfront and once the sale is complete, the consumer is usually left to figure out alone the intricacies of the contract.

Sales people tend to attach expensive riders (add-ons), to annuities that consumers may or may not need. Overall, the process is not a positive experience. Bad press and poor sales practices make annuities one of the most misunderstood products out there. It’s a shame because annuities can help mitigate longevity risk and increase the survival rate of traditional stock and bond retirement portfolios.

Good-intentioned and knowledgeable financial professionals are not inured against falling for pervasive horror stories when in fact they could be doing their clients a disservice by ignoring benefits annuities can bring to the table for those who have high probabilities of outliving assets that generate income in retirement.

So, let’s get basic. Ground floor.

What is an annuity, anyway?

An annuity is a sum of money, generally paid in installments over a contract owner’s lifetime or that of the owner and a spouse or a beneficiary. Annuities are insurance products that guarantee a lifetime income stream. Pensions are considered annuities. Yes, Social Security is an annuity (guaranteed by the Federal Government).

For years, several well-known money managers and syndicated financial superstars have overwhelmed social, television and weekend radio media with negative information about annuities.

Several types of annuities can be incorporated into a holistic financial plan.

It’s time Real Investment Advice readers understand the truth.

Here’s real investment advice lessons for three of the most popular annuity structures:

Variable Annuities: “The Black Sheep.”

Variable annuities are a hybrid. A blend of mutual funds and insurance. Guarantees come in the form of death benefits to beneficiaries or payouts for life if annuitized which means the investment is converted by the respective insurance company into a series of periodic payments over the life of annuitant or owner of the contract. Variable annuities are ground zero for negative press as they can be expensive and generate big commissions for brokers.

Earnings are tax deferred and taxed as ordinary income upon withdrawal. Investments in variable annuities are best outside of tax-sheltered accounts like IRAs which are already tax deferred. Investment choices are plentiful. There are various riders that may be attached. The most common is the GLWB or Guaranteed Lifetime Withdrawal Benefit rider which guarantees a lifetime income withdrawal percentage on the principal invested or the account value, whichever is greater. Owners barely understand how variable annuities operate; many don’t realize their contracts contain riders, how much they cost, or what they do. I frequently deal with the frustration people feel.

Candidly, I cannot consider a valid reason for consumers to purchase variable annuities. In its purest form, an annuity should provide lifetime income, increase retirement portfolio longevity and possess zero downside risk to principal. Most investors possess exposure to variable assets such as stocks and bonds through company retirement plans already. I see little rationale to mix financial oil and water through variable annuities that combine insurance and mutual funds. The marriage of these two appears to be nothing more than a mission to generate revenue for the respective industries.

If you own a variable annuity within an IRA, consider liquidating it and transferring to a traditional IRA, preferably at a discount brokerage firm. Be wary of surrender charges that may occur upon liquidation. Non-qualified or variable annuities purchased with after-tax dollars can be liquidated however, taxes and withdrawal penalties may apply. It’s best to sit with a fiduciary who is proficient with annuities to assist with a strategy to unwind from this product.

Fixed Annuities. “The Quiet Ones.”

Fixed annuities or “multi-year guaranteed” annuities or MYGAs are essentially CD-like investments issued by insurance companies. They pay fixed rates of interest in many cases higher than bank certificates of deposit over similar periods.

An important difference is while CDs are FDIC-insured, fixed annuities are only as secure as the insurance companies that issue them; financial strength of the organizations considered, is paramount. A.M. Best is the rating service most cited. Search the rating service website for the insurance company under consideration here. There are six secure ratings issued by Best. Consider exclusively companies rated A (Excellent) to A++ (superior). For ratings of B, B- (Fair), understand thoroughly your state’s coverage limits. Avoid C++ and poorer rated companies altogether.

Fixed annuities in the case of insurance company insolvency, are backed by the National Organization of Life & Health Insurance Guarantee Associations and each state has a level of protection. For example, in Texas, the annuity benefit protection is $250,000 per life.

The predictability of a set payout and limited risk to principal make MYGAs a popular option for retirees who seek competitive fixed rates of interest.

Fixed Indexed Annuities – “A Cake & Eat Some Too.”

Fixed indexed annuities get under the skin of one financial superstar asset allocator who dismisses stock market losses as no big deal (I mean markets rebound eventually, correct?). Losses don’t appear to be a big concern for him or his clients.

As the granddaddy of financial radio personalities, the gentleman relishes the calls in to his radio show that express concerns about annuities, especially fixed indexed annuities as he gets another opportunity to proudly remind his national audience – “so, with these products, you don’t get all the market upside!” Believe me, he’s all about the upside because markets only move in one direction from where he sits. From where you sit and what Roger Ibbotson believes, there’s a strong probability ahead for lower returns on traditional asset classes which include long-term bonds.

So, what are fixed indexed annuities?

First, they are not products that invest directly in stock markets. They are insurance vehicles that provide the potential for interest to be credited based on performance of specific market indexes. Selections within these fixed annuities allow owners to participate in a fixed percentage of the upside of a market index or earn a maximum rate of interest that’s based on the percentage change in an index from one anniversary date (effective date of ownership), to the next. A strategy identified as “point-to-point.”

Second, fixed indexed annuities are characterized by a ‘zero floor,’ which simply means there’s no risk of market downside. Owners may get a goose-egg of a return for a year, that’s true. However, there’s no need to make up for market losses, either.

As stated in the academic research published by Mr. Ibbotson:

“This downside protection is very powerful and attractive to many individuals planning for retirement. In exchange for giving up some upside performance (the 60% participation rate), the insurance company bears the risk of the price index falling below 0%. The floor is one way to mitigate financial market risk, but also gain exposure to potentially higher equity performance than traditional fixed income investments.”

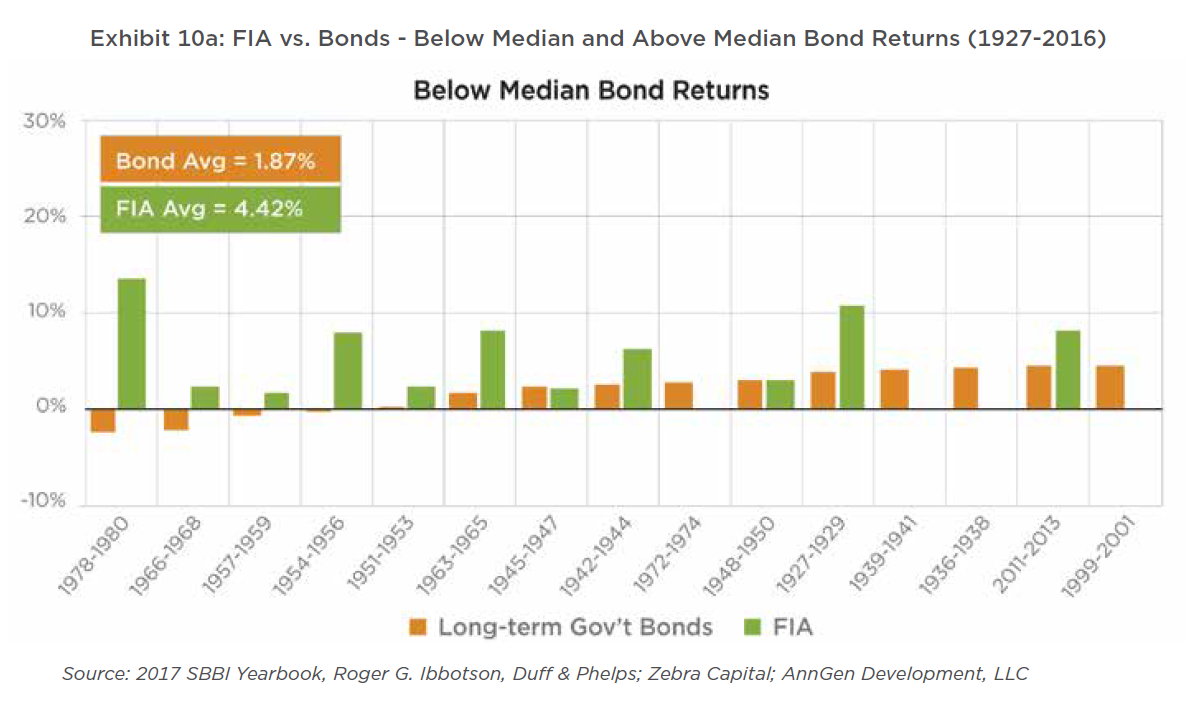

Third, Roger Ibbotson and his team analyzed fixed index annuities performance compared to periods of outperformance and underperformance for long-term government bonds. They isolated 15 three-year periods where bonds performed below the median like above, where the average 3-year annualized return was 1.87% compared to the FIA average of 4.42%. Through fifteen 3-year timeframes where bonds performed above median, returns for bonds and fixed index annuities averaged 9% and 7.55%, respectively.

Last, the research is limited to a simulation of the net performance of a fixed index annuity tied to a large cap equity index with uncapped participation rates. A participation index rate strategy is mostly effective under strong stock market conditions as interest credited is a predetermined percentage multiplied by the annual increase in a market index’s return. For example, a fixed indexed annuity offers an uncapped point-to-point option with a 40% participation rate. If the chosen market index the participation rate is connected to increases by 10%, your return for the year will be 4%. The participation percentage may be changed annually.

A “point-to-point” cap index strategy incorporates a ceiling on the upside and will not perform as well during periods when stocks are characterized by strong performance. The point-to-point cap index choice is best when markets are expected to provide limited growth potential and provides 100% participation up to the annual cap set by the insurance company. Let’s say a fixed indexed annuity has a 3% index cap rate and is tied to the performance of the S&P 500. For the year, the S&P 500 returns 2%. The interest credited to your account would be 2%, which is under the 3% cap. Under the participation index rate strategy outlined above, interest credited would be less at 40% of the S&P return, or .8%.

Since credited interest increases the original investment and downside protection is provided, your money compounds in the true sense of the definition. As we’ve written previously at Real Investment Advice – compounding works only when there is NO CHANCE of principal loss.

Fixed indexed annuities offer a fixed interest rate sleeve in addition to stock market participation options. There’s the choice to select multiple strategies (to equal 100%) and change allocations every year on your anniversary or annuity effective date.

Generally, annuities are immediate or deferred as well as fixed and variable as described above. Deferred annuities are designed for saving and interest accumulation over long periods, usually 5-10 years. They most popular are outlined here in Part 1. Immediate and guaranteed income annuities which I’ll cover in Part 2, are designed to provide lifetime income and longevity insurance for consumers who are concerned about outliving their retirement investments.

Below are Real Investment Advice and Clarity’s financial guardrails or rules to consider before the purchase of accumulation and income annuities:

- Annuities tend to get sold, not planned. Annuities are primarily product-sales driven. Comprehensive financial planning which includes your current asset allocation, ongoing savings and investing habits, anticipated income needs in retirement and survivability of investment assets based on estimated life expectancies either for you or you and a spouse, should be a mandatory first step. Most annuity salespeople are not going to undertake a holistic planning approach before an annuity solution is offered; it’s important to partner with a Certified Financial Planner who is also a fiduciary to complete a financial plan before you commit resources to annuities. A plan can determine whether an annuity improves retirement income sustainability and specifically, how much investment to commit. If your plan reflects the probability of meeting your retirement goals at 85% or greater, forgo the annuity and create an action plan to bolster savings, reduce debt or work a year or two longer.

- Consider fixed indexed annuities as intermediate to long-term bond replacements. Or to improve risk-adjusted portfolio returns during market cycles of extended stock valuations and/or less potential for appreciation in bond prices (like we’re in now). Roger Ibbotson estimated that a 60% stock, 20% traditional bond, 20% fixed indexed annuity allocation returned 8.12% from 1927-2016 in periods where bond returns were below median, compared to a traditional 60/40 portfolio which returned 7.6%. If future returns for traditional risk assets will be muted due to rich stock valuations and lower capital appreciation for bonds (which we believe is the case), a fixed indexed annuity may be employed to replace up to 20% of a total fixed income allocation. A FIA may provide attractive returns compared to stocks and bonds combined with zero downside risk.

- Avoid or minimize exposure to variable annuities. Variable annuities do not appear worthy of investment in our opinion. Meet with a financial professional, preferably a fiduciary, to create and implement a liquidation or transfer plan.

- Understand surrender charges, costs, tax and withdrawal penalty implications. Annuities must be considered long-term products designed solely to meet retirement goals. Deferred annuities will include a hefty 5-10 year decreasing annual percentage charge to discourage liquidations. There will be ordinary income taxes incurred and possibly penalties (if younger than 59 ½), upon withdrawals. Charges are incurred for commissions and cost of insurance, too. Most annuities will permit up to 10% annual withdrawals free of surrender charges. It’s important to understand how to withdraw as a last resort if a financial emergency arises.

- Slow your riders. Riders are supplementary features and benefits that can add anywhere from .35 to 1.50% in additional costs per year. Available riders range from enhanced liquidity benefits (ELBs) which allow surrender-charge free return of premiums in the second year, ADL (activities of daily living such as bathing & dressing), or custodial care withdrawals that provide access to up to 100% of accumulation value without surrender charges, to the most popular – GLWBs or Guaranteed Living Withdrawal Benefits for one life or for you and a spouse. Lifetime income is guaranteed even if the accumulation value of the annuity falls to zero. I have yet to encounter an annuity owner who can explain to me why they purchase riders or how they’re supposed to work. Unless a comprehensive financial plan indicates a 25% or greater probability of outliving your retirement savings (75% success rate), and expected single or joint life expectancies are age 95 or older, paying 1-1.5% a year for a living withdrawal benefits rider seems excessive. If outliving your investment source of retirement income is a concern, there are deferred and immediate income annuities on the market that can fill the gap along with other solutions like reverse mortgages.

- Seek a second opinion. An annuity is a long-term financial commitment. Before purchase, due diligence is mandatory. A fiduciary professional can outline the pros and cons of your prospective purchase. A deliberate, well-researched decision will minimize regret, later. Contact us for objective guidance.

See? Annuity is not such a scary word. In some cases, it’s the difference between a secure retirement or not. Along with a strategy backed by a comprehensive plan, fixed indexed annuities can be employed to minimize losses or enhance portfolio returns.

Indeed, annuities are complicated. There’s no getting around that obstacle. However, I hope our guardrails will help you gain perspective.

Annuity means ‘check for life,’ and who is against that?

The billionaire Ken Fisher. That’s who.

You may need to think differently.