A recent whitepaper by the Federal Reserve warns of “significantly lower profit growth and stock returns in the future.” In his article, End of an Era: The coming long-run slowdown in corporate profit growth and stock returns, Michael Smolyansky explains how the interest rate and corporate tax rate trends for the last thirty years provided a strong tailwind for corporate profits. As a result, stocks performed better than would have otherwise been the case.

Understanding why corporate profits and, ultimately, stock prices outperformed in the past is important. However, more critical for investors is the future and assessing how interest rates and tax rates will affect earnings growth and stock prices.

To expand on the article’s warning, we examine a few large well-known companies to see how lower interest and tax rates benefited their bottom lines. But first, we summarize the Fed article.

Key Takeaways

- GDP growth fell markedly over the last 30 years while corporate profit growth rose slightly.

- Lower interest and tax rates and increased leverage greatly benefited corporate net profits.

- McDonald’s, Pepsi, and Clorox support the Fed’s findings.

- Can profits maintain recent growth trajectories without the benefit of lower interest and tax rates?

End of an Era- Article Summary

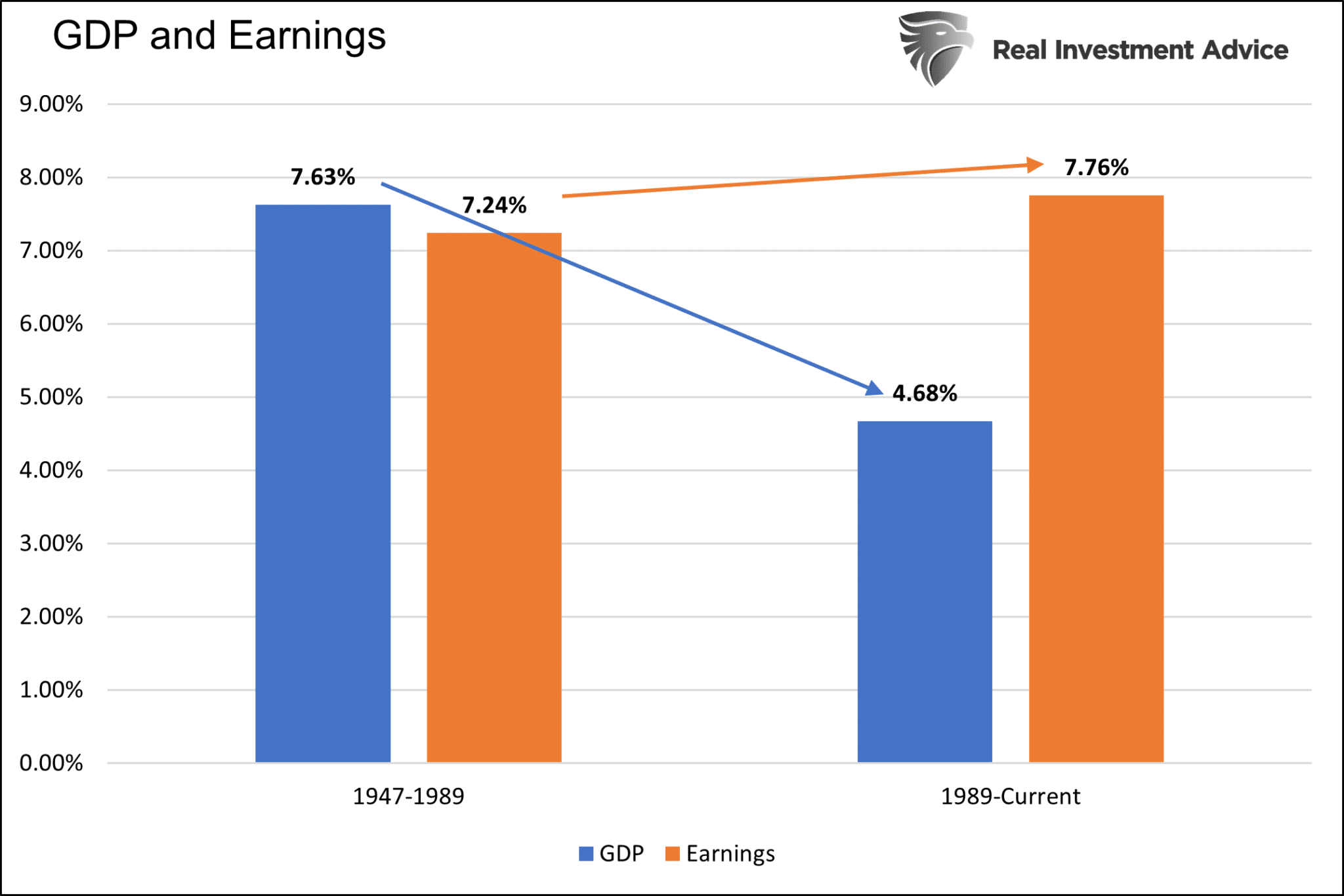

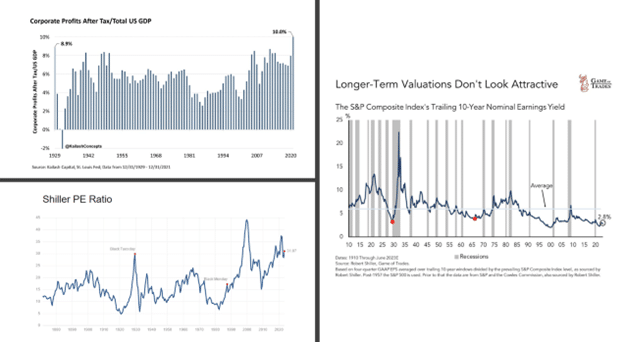

The graph below shows that corporate earnings have grown faster over the last 30 years than in the 40 years before. The robust earnings growth occurred despite economic growth shrinking markedly.

Michael’s article attributes two key factors to explain the significant disconnect between the two growth rates. Per the article:

My central finding is that the 30-year period prior to the pandemic was exceptional. During these years, both interest rates and corporate tax rates declined substantially. This had the mechanical effect of significantly boosting corporate profit growth. Specifically, I find that the reduction in interest and corporate tax rates was responsible for over 40 percent of the growth in real corporate profits from 1989 to 2019.

Corporate profits would have grown by 4.50%, not 7.76% annually, without the boost from interest rates and taxes, assuming his 40% contribution calculation is correct. Such would be on par with GDP growth for the last thirty years. As we share later, it appears 40% is a reasonable estimate.

Interest Rates

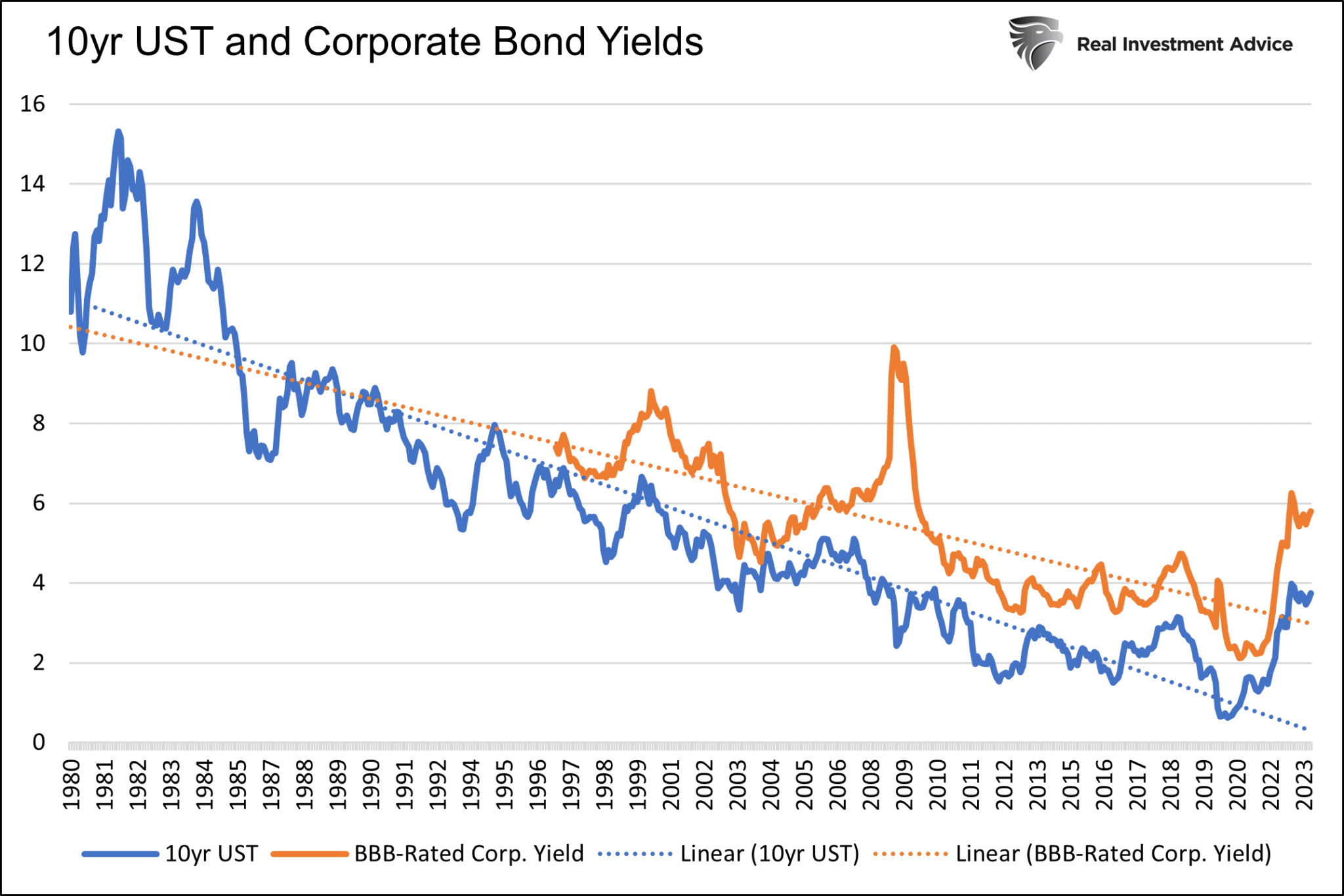

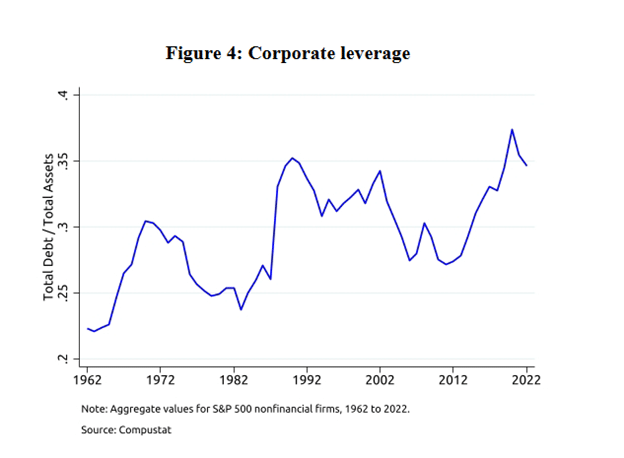

As shown below, Treasury and corporate interest rates have fallen steadily over the last thirty years. As a result of cheap financing, corporate leverage, per the second graph below, has risen substantially to record highs. More leverage and reduced interest costs are a bona fide way to boost profits.

Tax Rates

Per the article:

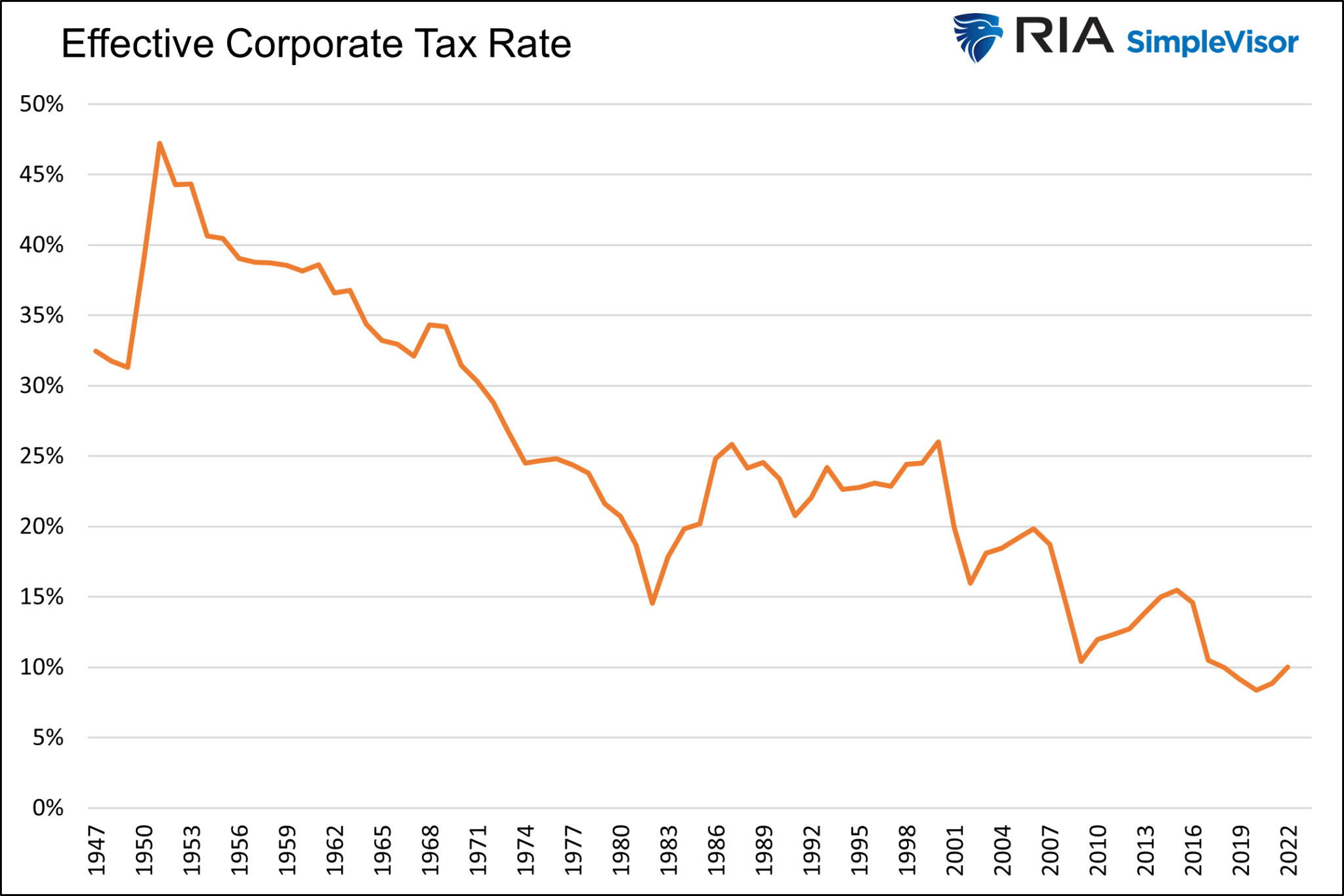

By 1989, the effective corporate tax rate—measured as aggregate tax expenses divided by aggregate pre-tax income—stood at 34 percent, having fallen from an average of 44 percent over the period 1962 to 1982. From 1989 to 2007, ending just prior to the financial crisis, effective corporate tax rates averaged 32 percent. They then drifted somewhat lower in the years immediately following the financial crisis. The next major step down occurred following the passage of the Tax Cuts and Jobs Act of 2017, which cut the statutory corporate tax rate from 35 percent to 21 percent. With this reform, effective corporate tax rates fell from 23 percent in 2016 to 15 percent in 2019.

The graph below shows effective corporate tax receipts as a percentage of pre-tax income are now around 10% versus 25% in the late 1980s.

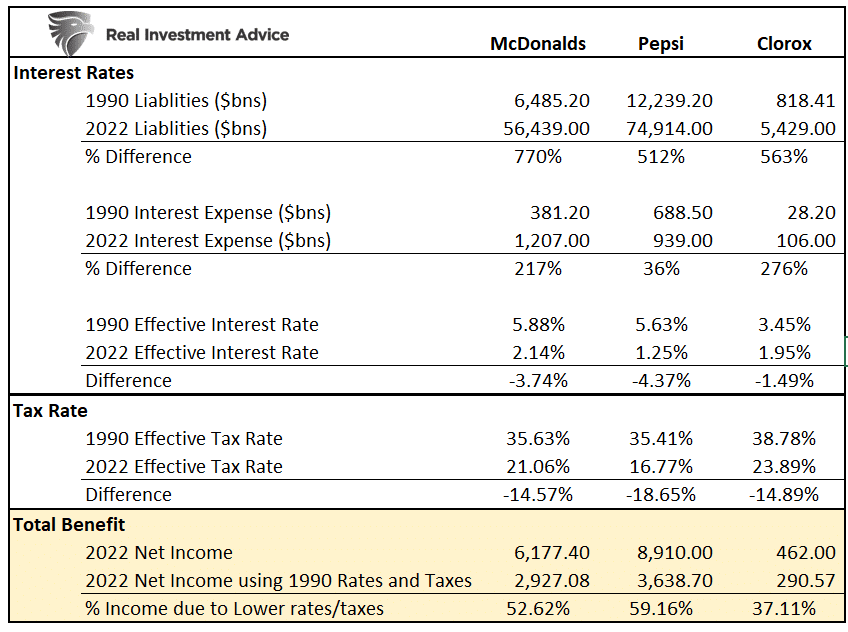

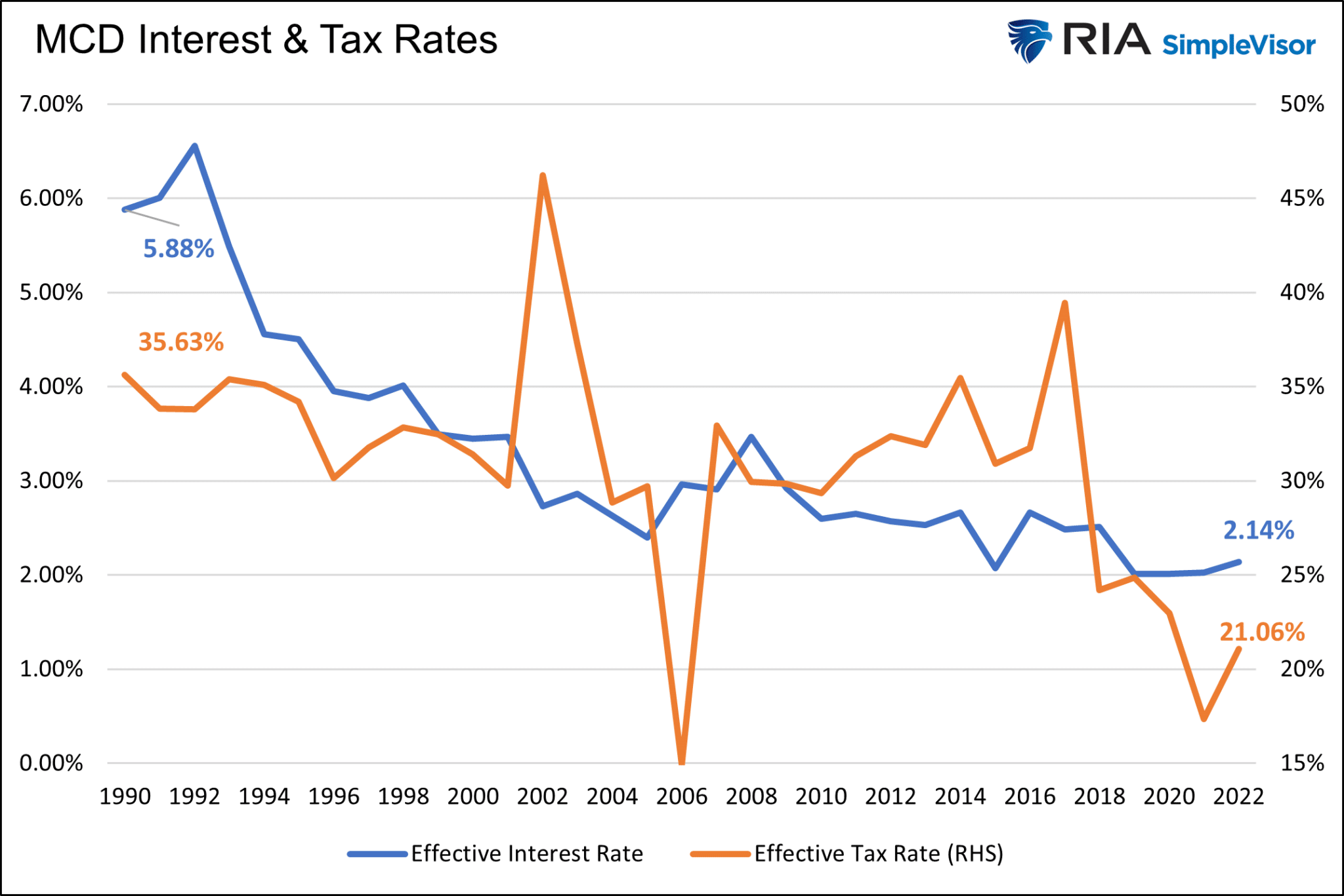

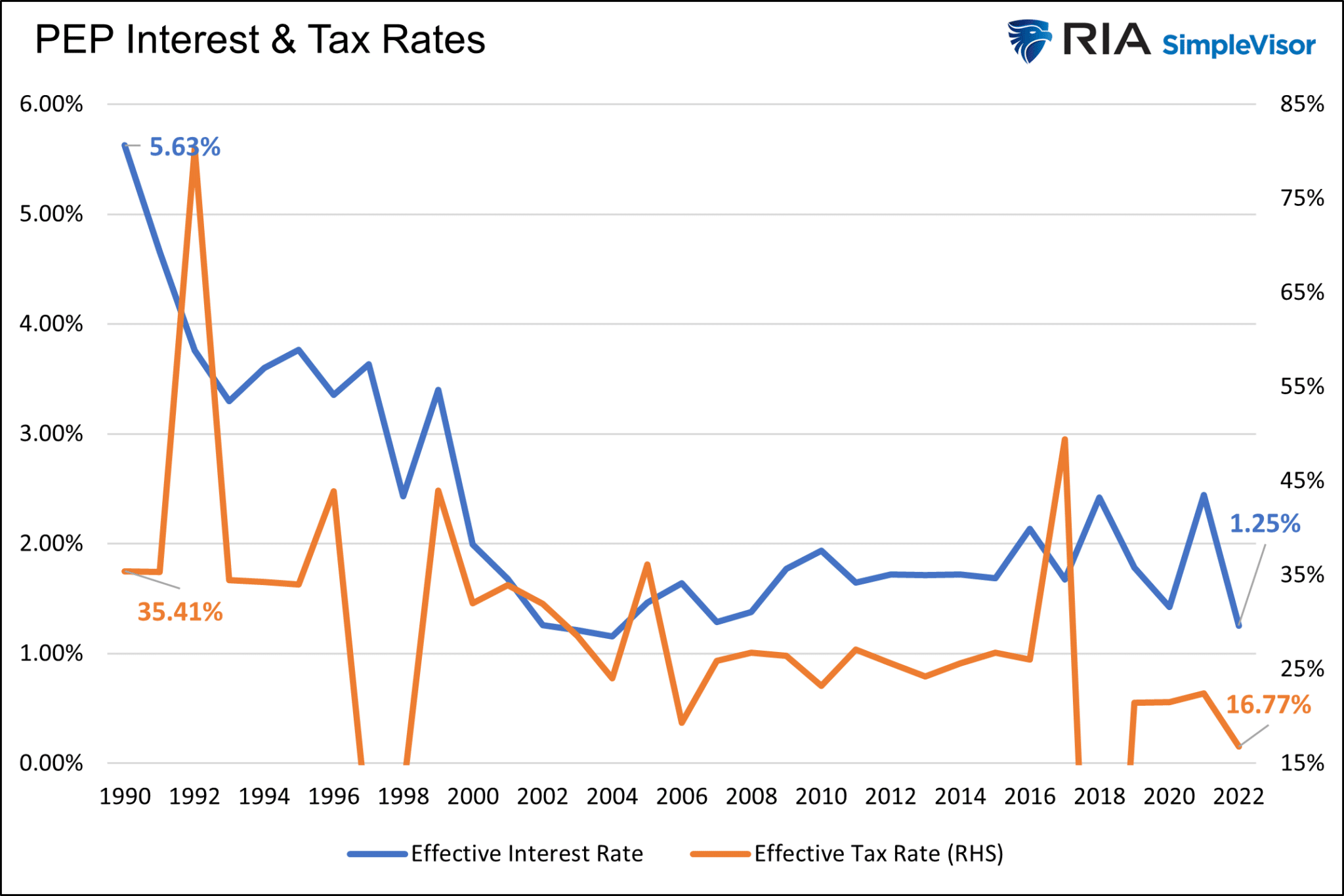

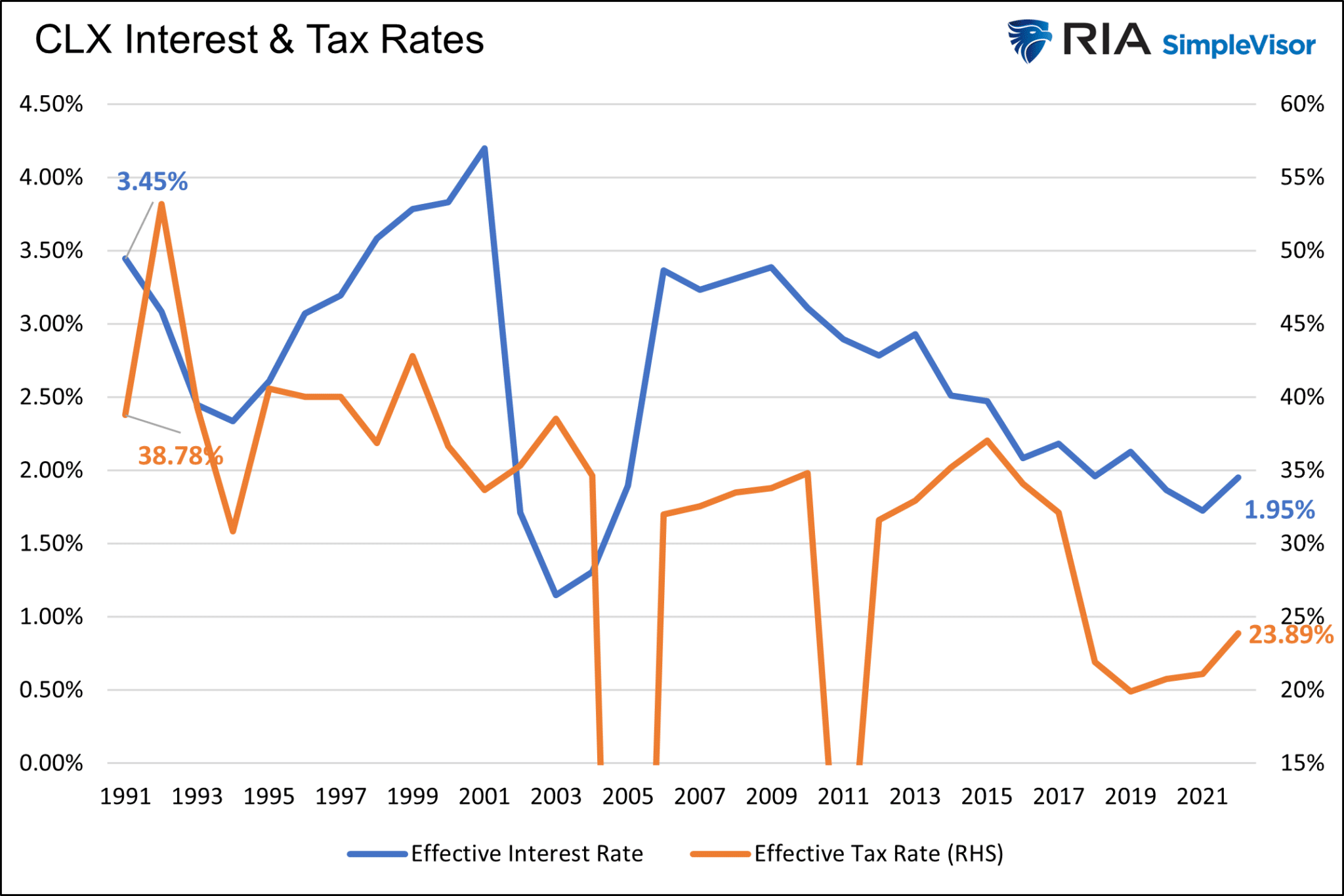

McDonald’s, Pepsi, and Clorox

To prove the benefit of lower interest and tax rates, we calculate how they helped improve profits for three large, well-known companies. The table below compares the debt levels, interest, and effective tax rates from 1990 to 2022 for McDonald’s, Pepsi, and Clorox.

All three companies increased their debt load much more than their interest expenses due to lower rates. The effective interest rate decline was significant for McDonald’s and Pepsi. While not as dramatic, Clorox had a meaningful decline. Similarly, the effective tax rates for the companies fell between 15% and 20%.

Lower interest and tax rates had a meaningful impact on earnings, as shown at the bottom of the table. Michael Smolyansky’s estimate that interest and tax rates boosted earnings by about 40% in aggregate seems to be in the ballpark with our analysis. The graphs below the table show the change in interest and tax rates for the three companies over the last 30 years.

Future Interest and Tax Rates

While lower interest and tax rates boosted growth significantly, the ability for that to continue is negligible. The end of a rewarding era for stocks is likely behind us. Given that government deficits will continue to grow faster than the economy, it becomes increasingly unlikely that the government can afford to reduce corporate taxes. In fact, the odds favor raising taxes. Interest rates may fall back to the low levels of the last ten years. Still, unless rates go negative, there is little room on the margin for corporations to reduce their effective interest rate meaningfully.

Consequently, its likely corporate profit growth in aggregate will be closer to GDP growth rates in the future. The gap between GDP and profits we highlighted at the article’s opening will likely close. 4%’ish profit growth isn’t bad. But current high valuations are predicated on solid profit growth. GDP-like growth is not forecasted and will likely weigh on stock prices. Simply put, investors will not be willing to pay an above-average valuation for what will seem like below-average profit growth.

Summary

Per the Fed’s End of an Era article:

It may be tempting to assume that the exceptional stock market performance over the last three decades will continue indefinitely. My analysis, however, indicates otherwise. Both stock returns and corporate profit growth are very likely to be substantially lower in the future. This conclusion follows from the minimal assumption that interest rates and effective corporate tax rates have very little scope to fall below 2019-levels.

The tailwinds of the last thirty years propelling profit growth by about 3% more than GDP are likely over. Without said help, profits are likely to track nominal GDP. However, we must remember that higher interest and tax rates are not out of the question. 4% profit growth may be the upside with a meaningful downside if interest rates stay around current levels and or tax rates increase.

As we wrote earlier:

Simply put, investors will not be willing to pay an above-average valuation for what will seem like below-average profit growth.