Is the “market melting-up?” Such was the question I received from my colleague at Cut The Crap Investing. It is an excellent question given the relentless increase in what investors believe is a “no risk” market.

Of course, we need a definition of precisely what constitutes a melt-up.

“A melt-up is a sustained and often unexpected improvement in the investment performance of an asset or asset class, driven partly by a stampede of investors who don’t want to miss out on its rise, rather than by fundamental improvements in the economy.“ – Investopedia

Currently, there is sufficient evidence to support the idea of an exuberant market. As noted previously:

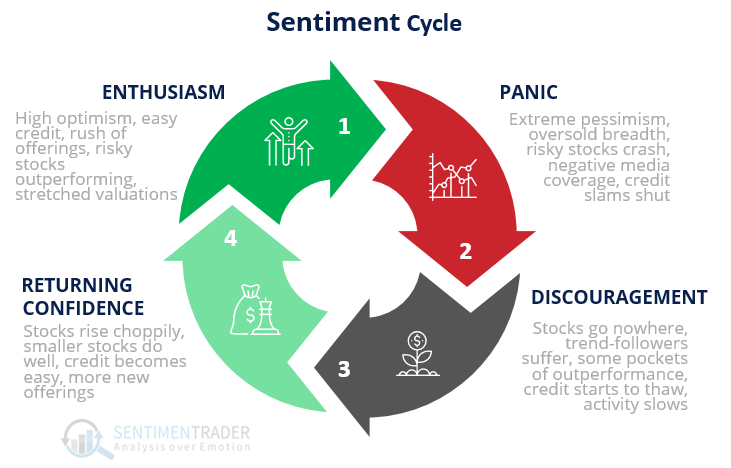

“Near peaks of market cycles, investors become swept up by the underlying exuberance. That exuberance breeds the “rationalization” that “this time is different.” So how do you know the market is exuberant currently? Via Sentiment Trader:”

‘This type of market activity is an indication that markets have returned their ‘enthusiasm’ stage. Such is characterized by:’

- High optimism

- Easy credit (too easy, with loose terms)

- A rush of initial and secondary offerings.

- Risky stocks outperforming

- Stretched valuations

However, while one would expect individuals to exhibit caution in such an environment, the opposite is true. Given the Fed’s ongoing balance sheet operations, investors fully believe they have protection from a decline.

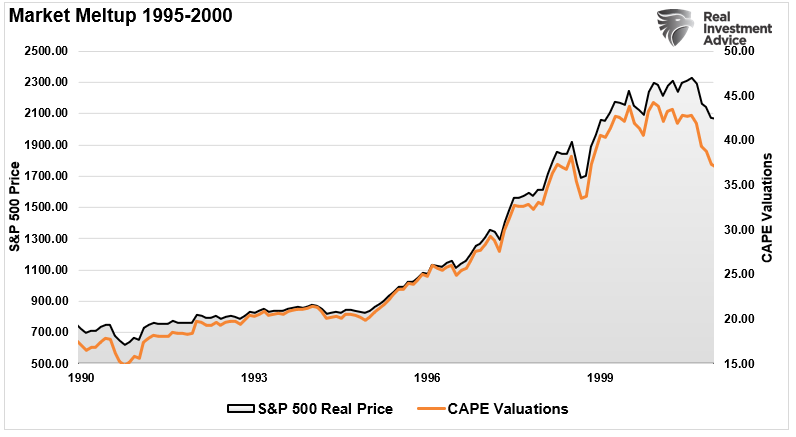

A Visualization Of A Market Melting-Up

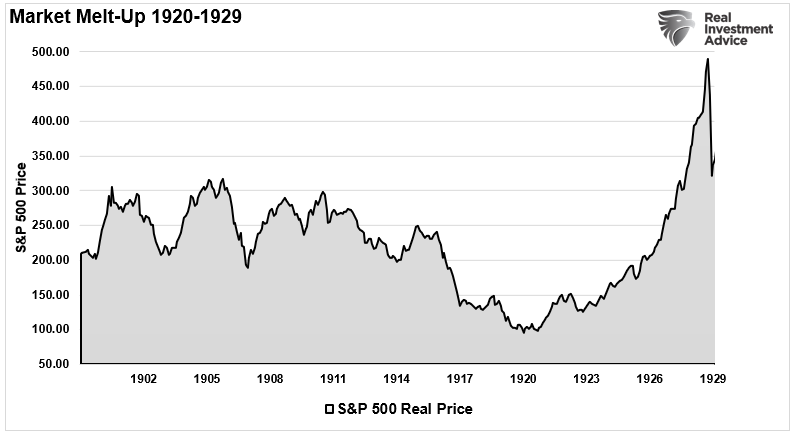

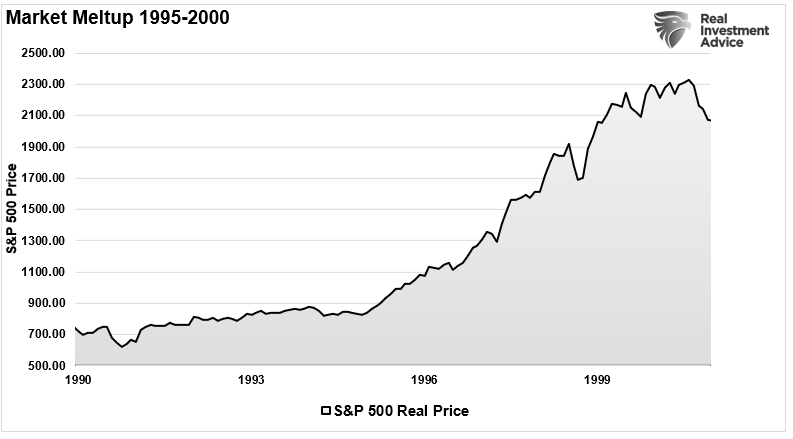

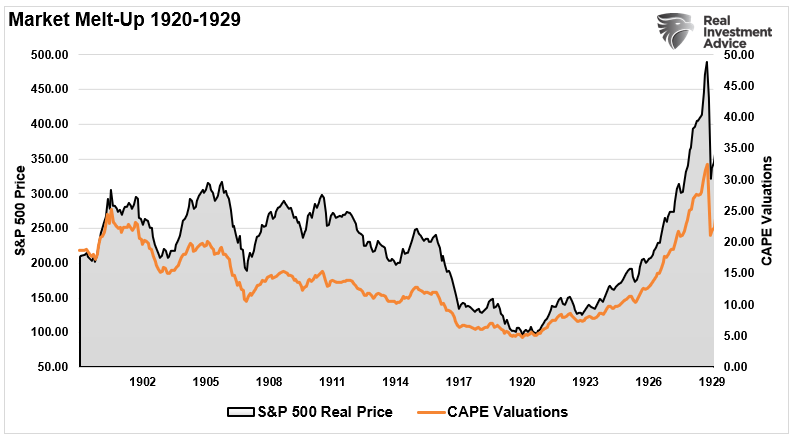

It is often easier to visualize something rather than explain it. Since 1900, only two previous market periods qualify as a melt-up: 1920-1929 and 1995-2000. The chart below shows both periods in terms of price.

However, the melt-up is also visually represented by the incredibly sharp rise in valuations. Such is essential because earnings are not rising at a fast enough clip to support higher prices. As is always the case, the investing public believes future earnings will justify higher prices during a melt-up. It just never works out that way.

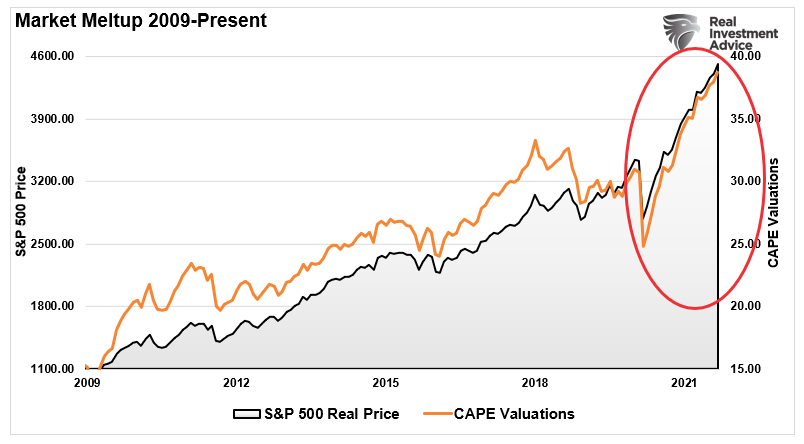

We can compare those two previous periods with the current advance from the March 2020 lows. Again, we see a very similar sharp advance in price combined with a surge in valuations. As expected, investors are currently hoping that future earnings will rise sharply enough to justify current prices. However, the justification for paying high prices is the Federal Reserve’s ongoing balance sheet expansion.

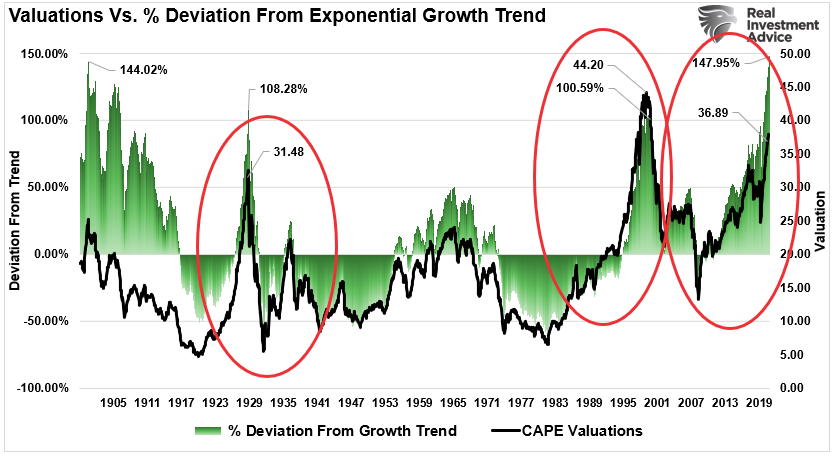

The following chart looks that the price advance and valuation measures a little differently. It shows the current deviation from the long-term exponential growth trend. Not surprisingly, during a market “melt-up,” there is a rapid deviation from the growth trend matching the acceleration in valuations.

The problem with market “melt-ups” is not the melt-up itself but what always follows.

Melting-Up Leads To Melting-Down

A market melting-up is exciting while it lasts. During melt-ups, investors begin to rationalize why “this time is different.” They start taking on excess leverage to try and capitalize on the rapid advance in prices, and fundamentals take a back seat to price momentum.

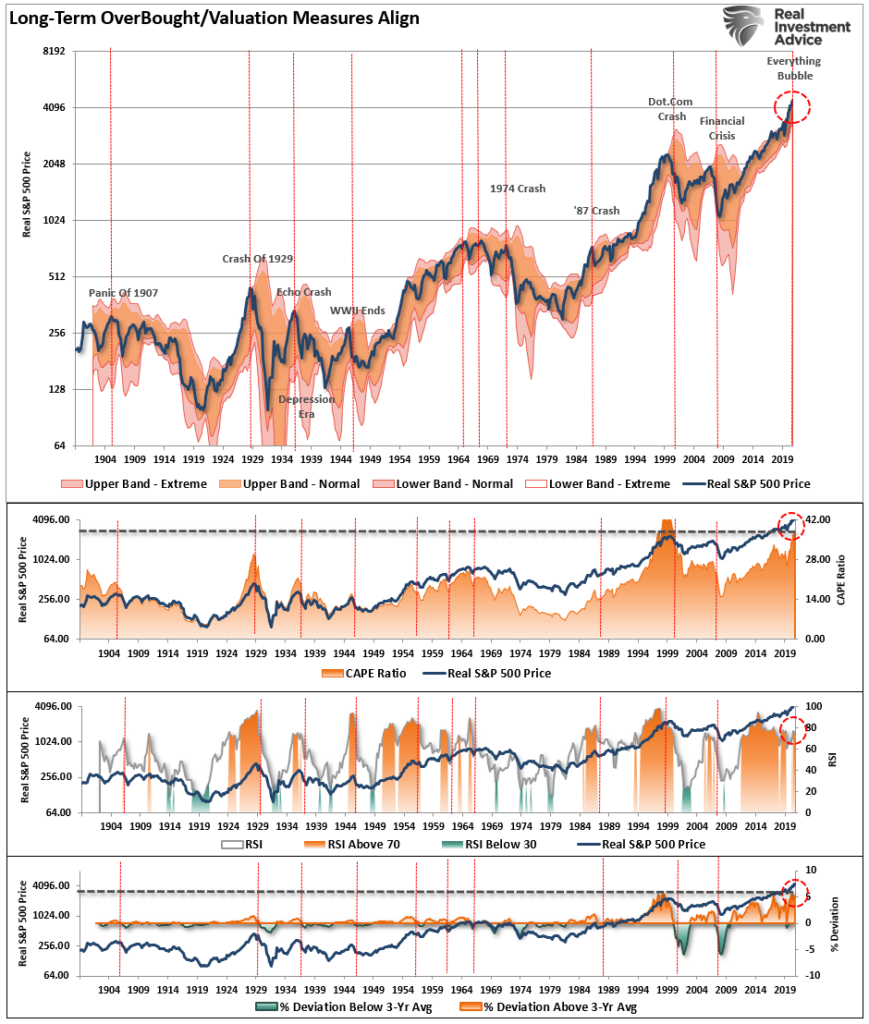

Market melt-ups are all about “psychology.” Historically, whatever has been the catalyst to spark the disregard of risk is readily witnessed in the corresponding surge in price and valuations. The chart below shows the long-term deviations in relative strength, deviations, and valuations. The previous ‘melt-up” periods should be easy to spot when compared with the advance currently.

Given that current extensions match only a few rare periods in history, a couple of points should be readily apparent.

- Melt-ups can longer than logic would predict.

- The prevailing psychology is always “this time is different.”

- Valuations are dismissed in exchange for measures of momentum and forward expectations.

- Investors take on excess leverage and risk in order to participate in a seemingly “can’t lose” market.

- Lastly, and inevitably, “melt-ups” end and always in the worst possible outcomes.

It is essential to recognize the markets are in a “melt-up,” and the duration of that event is unknowable. Therefore, investors need a strategy to participate in the advance and mitigate the damage from the eventual “melting-down.”

Surviving The Melt-Up

As noted, none of this means the next “bear market” is lurking. Given that a market melting-up is a function of psychology, they can last longer and go further than logic would predict. What is required to “end” a melt-up is an unanticipated exogenous event that changes psychology from bullish to bearish. Such is when the stampede for the exits occurs, and prices decline very quickly.

As such, investors need a set of guidelines to participate in the market advance. But, of course, the hard part is keeping those gains when corrections inevitably occur.

As portfolio managers for our clients, such is precisely the approach we must take. Accordingly, I have provided a general overview of the process that we employ.

- Tighten up stop-loss levels to current support levels for each position. (Provides identifiable exit points when the market reverses.)

- Hedge portfolios against major market declines. (Non-correlated assets, short-market positions, index put options)

- Take profits in positions that have been big winners (Rebalancing overbought or extended positions to capture gains but continue to participate in the advance.)

- Sell laggards and losers. (If something isn’t working in a market melt-up, it most likely won’t work during a broad decline. Better to eliminate the risk early.)

- Raise cash and rebalance portfolios to target weightings. (Rebalancing risk on a regular basis keeps hidden risks somewhat mitigated.)

Notice, nothing in there says, “sell everything and go to cash.”

There will be a time to raise significant levels of cash. A good portfolio management strategy will automatically ensure that “stop-loss” levels get triggered, exposure decreases, and cash levels rise when the selling begins.

While it is essential to take advantage of the melt-up while it lasts, just don’t become overly complacent “this time is different.”

It likely isn’t.