The Technical Value Scorecard Report uses 6-technical readings to score and gauge which sectors, factors, indexes, and bond classes are overbought or oversold. We present the data on a relative basis (versus the assets benchmark) and on an absolute stand-alone basis. You can find more detail on the model and the specific tickers below the charts.

Commentary 1-08-21

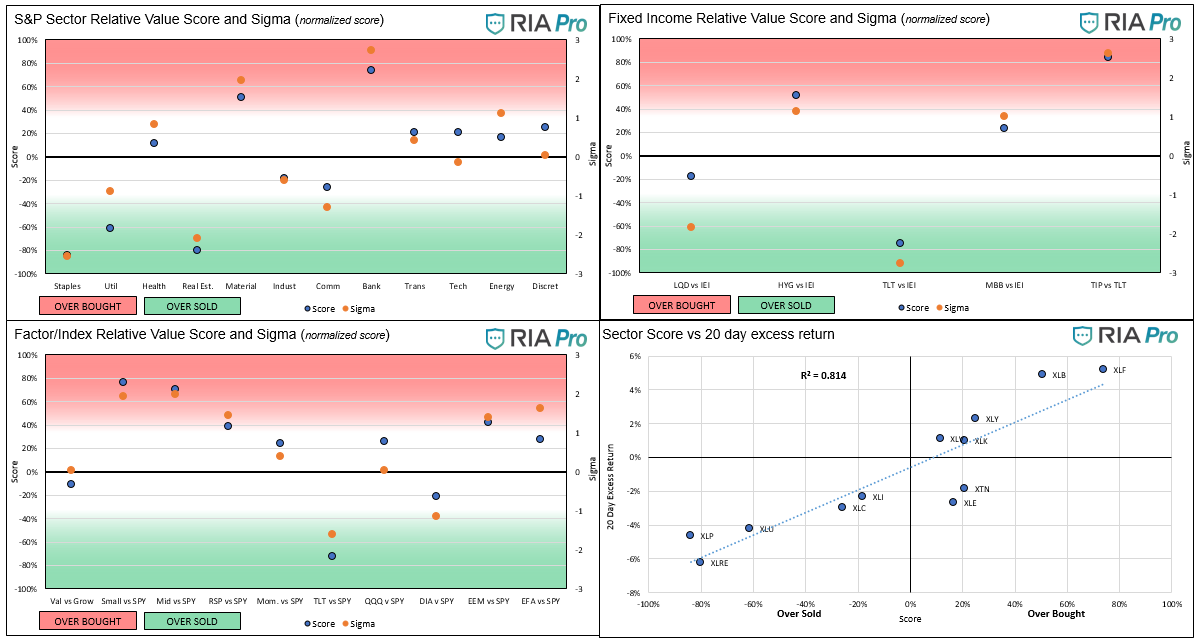

- The relative value graphs show the amazing divergence in fortunes that occurred over the past few weeks. Banks (XLF) are about as extreme overbought versus the S&P 500 as we witnessed this past year, while Staples (XLP) the most extreme oversold. In theory, banks benefit from the relation trade as the yield curve steepens and boosts profit margins. Conversely, many staples have to pay higher input costs to produce their goods and may find it difficult to fully pass the costs on to consumers, thus weaker profit margins.

- Materials are decently overbought, and Realestate is strongly oversold. Both sectors are also heavily affected by a perceived ramp-up in inflation. Most other sectors are close to their fair value versus the S&P.

- Not surprisingly, small-caps and mid-caps are deeply overbought versus the S&P. Emerging markets and Developed foreign markets are also overbought as the dollar continues to languish.

- We haven’t discussed bonds in a while but it’s worth noting that TLT (20yr UST) is about as deeply oversold versus IEI (5-7yr UST) as is possible. Again, as long as inflation remains a concern we can expect such underperformance. The same is true on the absolute level analysis in the second set of graphs.

- The sector score scatter plot has a very high R-squared of .814 denoting that most sector returns are in line with their respective relative performance versus the S&P.

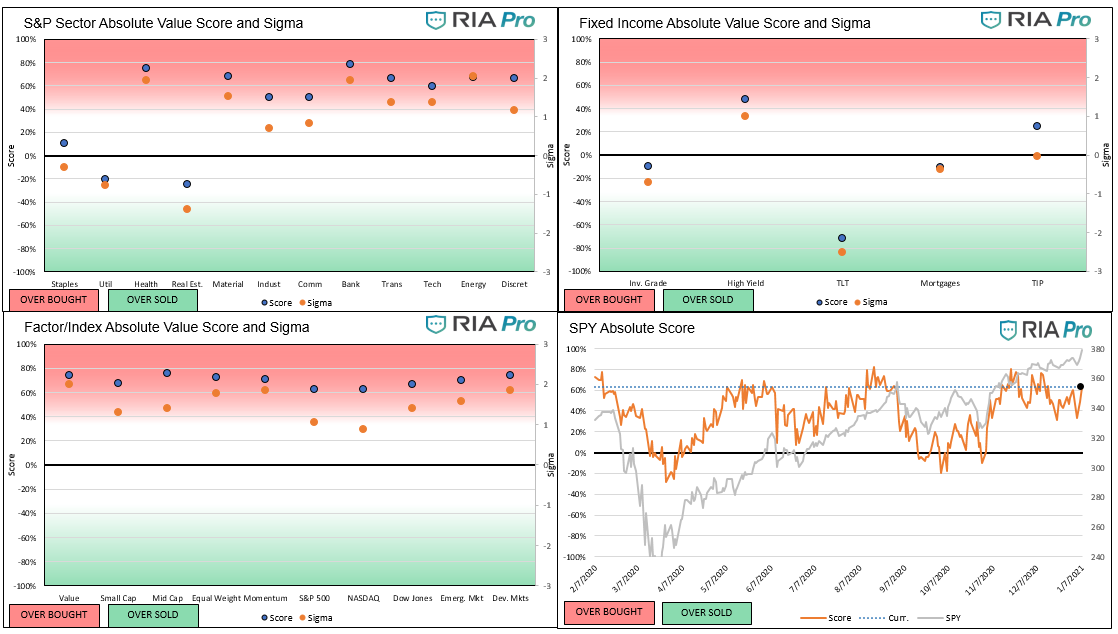

- On an absolute basis, most sectors are decently overbought with healthcare and banks leading the way. Staples, despite being grossly oversold versus the S&P, is fairly valued on an absolute basis. Utilities and Realestate are slightly oversold.

- On a factor/index level almost everything is nearing extreme overbought levels (>80%). The S&P 500, shown in the bottom right of the second set of graphs is also nearing the most extreme levels of the last year.

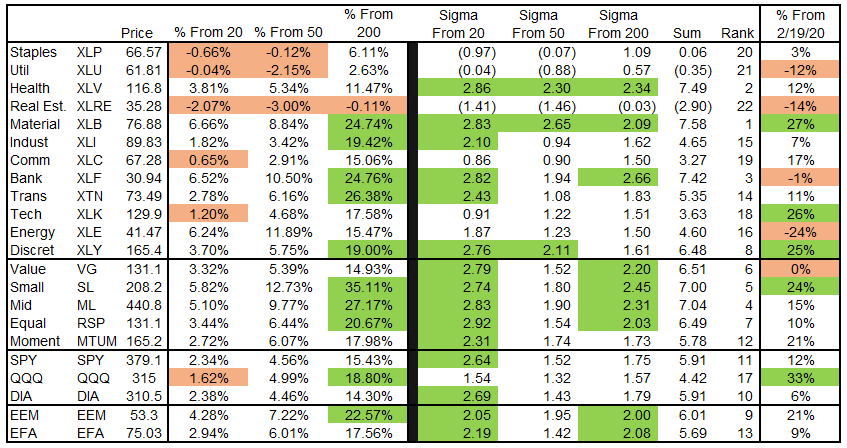

- The third graph below shows that many sectors, and all but one factor/index, are trading above 2 Bollinger bands versus their 20 day ma. There are also a handful trading 2 bands above their respective 50 and 200 day ma’s.

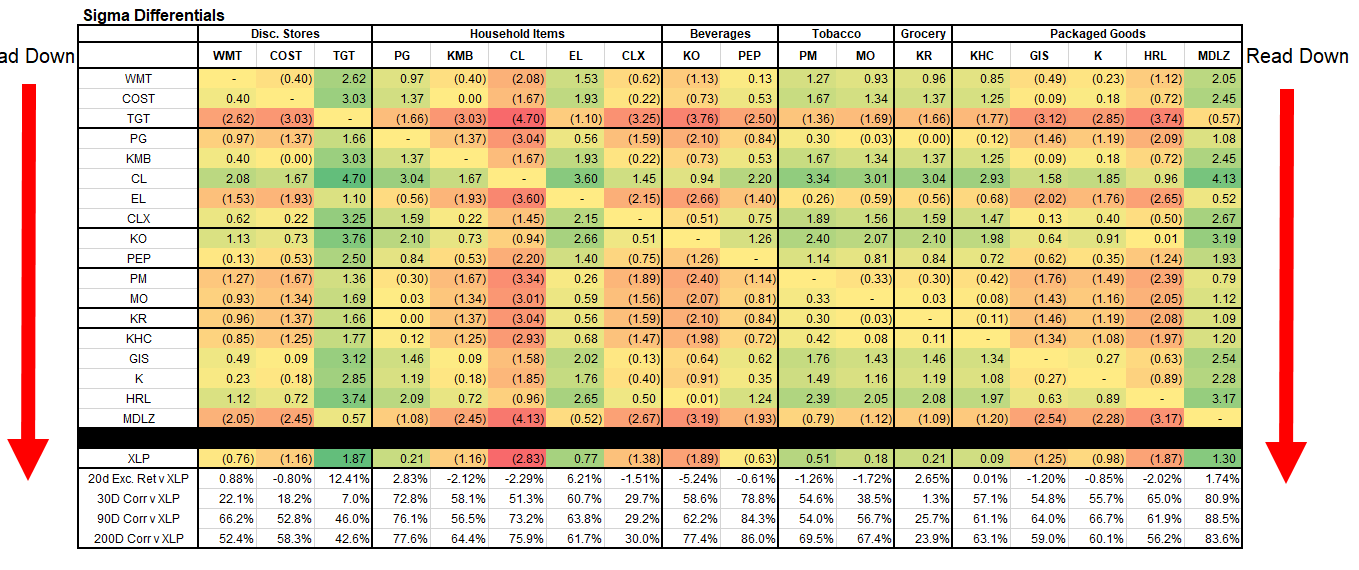

- It may be a little early to bottom fish in the staples sector, but if you are interested in keeping an eye on a few companies, the fourth table below shows the relative score of XLP’s leading companies against each other as well as against the sector ETF (XLP). Using this analysis, Colgate Palmolive (CL) appears to be the most oversold versus XLP and every other company. That said, its relative underperformance versus XLP over the last 20 days of -2.29% is not as bad as we would have guessed based on its score. The underlying companies are by and large trading in line with each other.

Graphs (Click on the graphs to expand)

Users Guide

The score is a percentage of the maximum/minimum score, as well as on a normalized basis (sigma) for the last 200 trading days. Assets with scores over or under +/-60% and sigmas over or under +/-2 are likely to either consolidate or change trend. When both the score and sigma are above or below those key levels simultaneously, the signal is stronger.

The first set of four graphs below are relative value-based, meaning the technical analysis score and sigma is based on the ratio of the asset to its benchmark. The second set of graphs is computed solely on the price of the asset. Lastly, we present “Sector spaghetti graphs” which compare momentum and our score over time to provide further current and historical indications of strength or weakness. The square at the end of each squiggle is the current reading. The top right corner is the most bullish, while the bottom left corner the most bearish.

The technical value scorecard report is just one of many tools that we use to assess our holdings and decide on potential trades. This report may send a strong buy or sell signal, but we may not take any action if other research and models do not affirm it.

The ETFs used in the model are as follows:

- Staples XLP

- Utilities XLU

- Health Care XLV

- Real Estate XLRE

- Materials XLB

- Industrials XLI

- Communications XLC

- Banking XLF

- Transportation XTN

- Energy XLE

- Discretionary XLY

- S&P 500 SPY

- Value IVE

- Growth IVW

- Small Cap SLY

- Mid Cap MDY

- Momentum MTUM

- Equal Weighted S&P 500 RSP

- NASDAQ QQQ

- Dow Jones DIA

- Emerg. Markets EEM

- Foreign Markets EFA

- IG Corp Bonds LQD

- High Yield Bonds HYG

- Long Tsy Bonds TLT

- Med Term Tsy IEI

- Mortgages MBB

- Inflation TIP