The Technical Backdrop: When Flows Meet a Hawkish Fed

Here’s the setup most investors are underrating right now. Over the next two weeks, the tape will trade on plumbing rather than fundamentals. We just cleared the largest options expiration in history. Quarter-end pension selling comes next, and then July […]

Bull Market Pullback: Why The 4.5% Dip Held The 50-DMA

Key Takeaways Two weeks ago, after the S&P 500 logged its ninth consecutive weekly gain, we discussed that a bull market pullback was coming. It came. From the May 27 record near 7,621, the index slid 4.5% and bottomed almost […]

Equity Supply Surge: What Historically Comes Next

This past week, the market hit an all-time high. At the same time, Alphabet (GOOG) told investors it would raise $80 billion by selling stock to fund its AI buildout, and the shares fell about 4% on the news. Within days, […]

Risk Management For Retirees: When To Reduce Exposure

Last week, a viewer of the Morning Show emailed me about risk management for retirees. He asked the single most important question retirees face, and rarely get a straight answer to. “From an already retired perspective, and as one whose […]

Corrections vs. Bear Markets: Why 20% Declines Are Obsolete

After three decades of watching market cycles play out from both sides of the trade, I’ve come to a simple conclusion: Wall Street’s love of simple rules is one of the most dangerous aspects of investing. When stocks fall 10%, […]

Buffett Cash Hoard: Why $397 Billion Sits On The Sidelines

$397 billion. That’s how much “Buffett cash” now sits on Berkshire Hathaway’s balance sheet after Greg Abel’s first quarter as CEO. Warren Buffett left $373 billion behind when he stepped down at the end of 2025. Three months later, after Abel’s […]

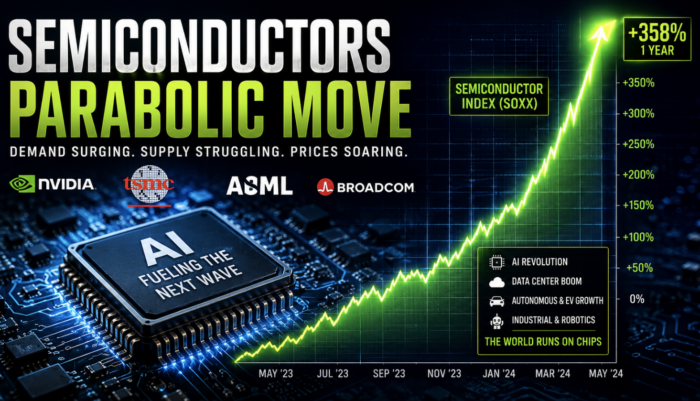

Parabolic Semiconductor Rally Is Pricing In 2028 Already

The parabolic semiconductor rally crossed a line this week. SOXX, the iShares Semiconductor ETF, closed Friday at $509.77 after touching a fresh intraday high of $511.68. That’s a gain of roughly 244% from the April 2025 low of $148.31. Most […]

Market Correction Risk: Why Summer 2026 Looks Risky

Collapsing breadth. Stretched positioning. The worst seasonal window of the year. The worst year of the political cycle. And a war that won’t end. Market correction risk is stacking up. The S&P 500 hit a fresh record high last week. […]

Hormuz: Why Markets Are Shrugging Off The Oil Shock

As of this writing, the Strait of Hormuz remains effectively closed since February 28. Roughly 20% of the world’s seaborne oil stopped moving through the chokepoint. The International Energy Agency described the event as “the largest supply disruption in the […]