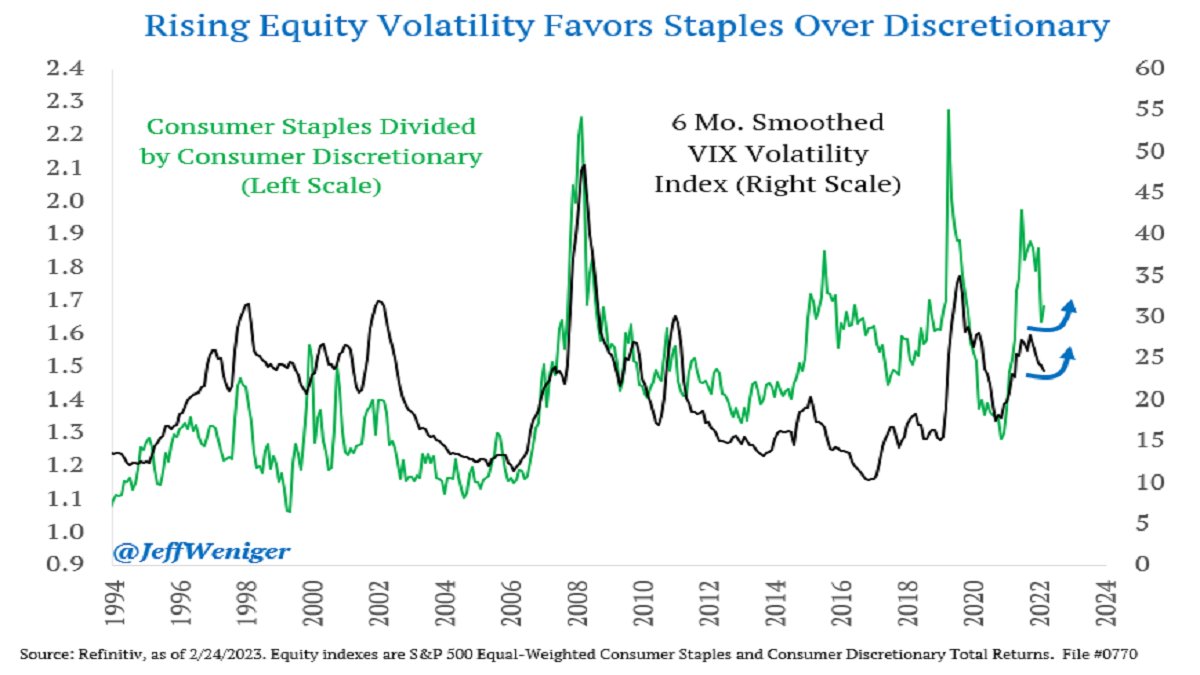

Consumer staple companies typically include companies that sell essential goods. As such, earnings growth tends to be limited but reliable, even during a recession. Proctor Gamble, the maker of many household items we use daily, is the most significant contributor to the sector. Conversely, discretionary stocks sell non-essential goods. Amazon and Tesla make up a third of the sector. Discretionary stocks have more earnings volatility than staples. Earnings volatility tends to translate into stock price volatility.

In last year’s downward trend, staples outperformed discretionary stocks. Lower betas and valuations, along with steady earnings, proved to benefit staples. The graph below shows the strong correlation between the staples to discretionary stocks ratio and the VIX volatility index. The chart affirms what we witnessed. Periods of higher volatility, often accompanying market drawdowns, saw staples outperform.

What To Watch Today

Economy

- MBA Mortgage Applications, week ended Feb. 24 (-13.3% prior)

- S&P Global U.S. Manufacturing PMI, February Final (47.8 prior)

- Construction Spending, month-over-month, January (0.4% expected, -0.4% prior)

- ISM Manufacturing, February (47.9 expected, 47.4 prior)

- ISM Prices Paid, February (44.5 prior)

- ISM Employment, February (50.6 prior)

- ISM New Orders, February (42.5 prior)

- Wards Total Vehicle Sales, February (15.00 million, 15.74 million prior)

Earnings

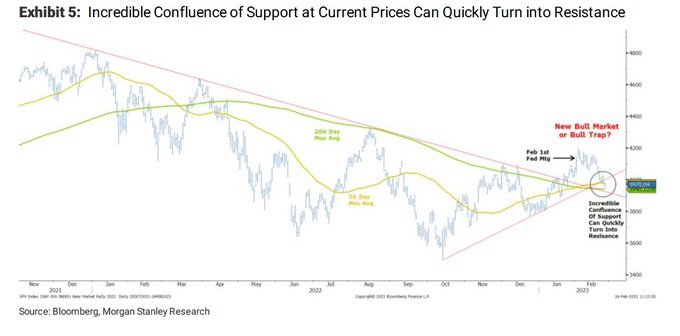

Market Trading Update

Yesterday morning, I posted the following tweet:

Here is a larger version of that chart.

Yesterday was disappointing, again, with the market opening higher and selling into the close. However, the good news is that the market continues to cling to support at the 50-DMA and the uptrend line. However, yesterday’s decline is eating into the very small “margin of error” the market currently maintains between a “bull market” and a “bull trap.”

Overall, trading remains tepid, which is dangerous in a corrective market, as a break of support will likely bring program sellers into the market all at once. That critical level is the 200-DMA, where most programmed sell orders are currently stacked up.

Remain cautious and use modest advances to reduce equity risk and rebalance portfolios.

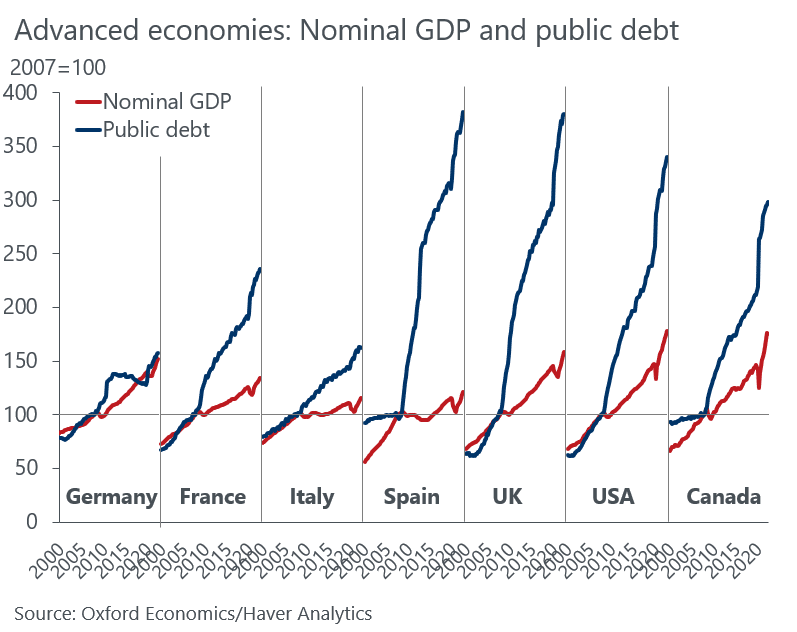

The Leverage Tax

The calls for a soft landing and no landing by many “esteemed” economists are startling, given the enormous headwinds in higher interest rates. The graph below shows the ratio of the amount of debt versus the ability to pay for the debt (GDP) has skyrocketed in many countries, including the U.S. The U.S. ratio was about 1:1 before the 2008 financial crisis. In only 15 years, it has doubled. Simply, the economy is more leveraged. Therefore, economic activity is also much more sensitive to interest rates.

Interest rates are now at or above levels seen in 2008. The tax on leverage, via higher interest rates, is coming due. As companies, individuals, and the government refinance maturing debt or issue new debt, their interest expenses will increase markedly. To compensate for the higher rates, consumers will spend less. Corporations will find ways to cut costs, including laying off employees. Lastly, the government may limit spending to keep the deficit somewhat contained. Bottom line- more money will be spent on debt servicing, leaving less for economic growth. This matters when sustainable economic growth is sub 2%.

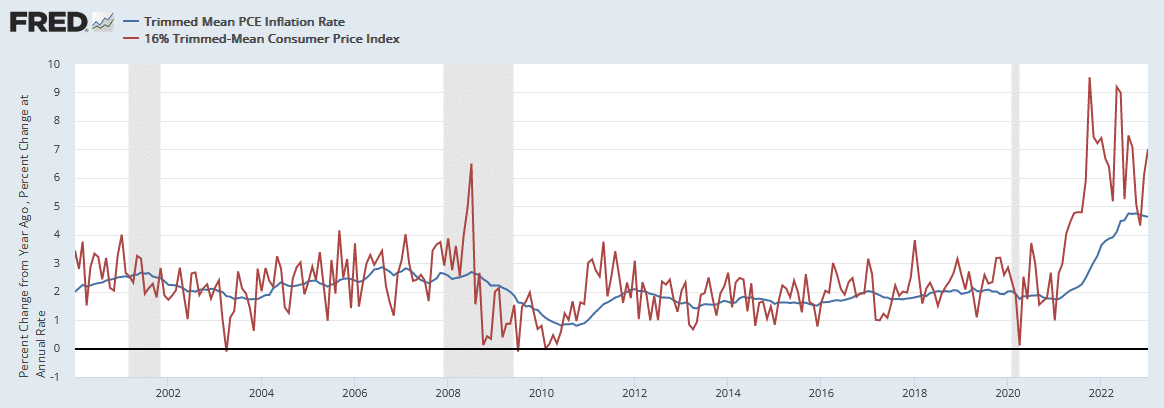

Trimmed Mean Inflation Worries the Fed

The Fed likes to slice and dice inflation data to understand its intricacies. The chart below, for example, shows two closely followed Fed inflation measures that the public often overlooks. The Dallas and Cleveland Feds put out Trimmed Mean inflation measures. They compute the average after stripping out the highest and lowest price changes. The figures attempt to show the price changes for the bulk of goods. As we share below, both gauges show the prices for most goods are not falling nearly as much as CPI and PCE.

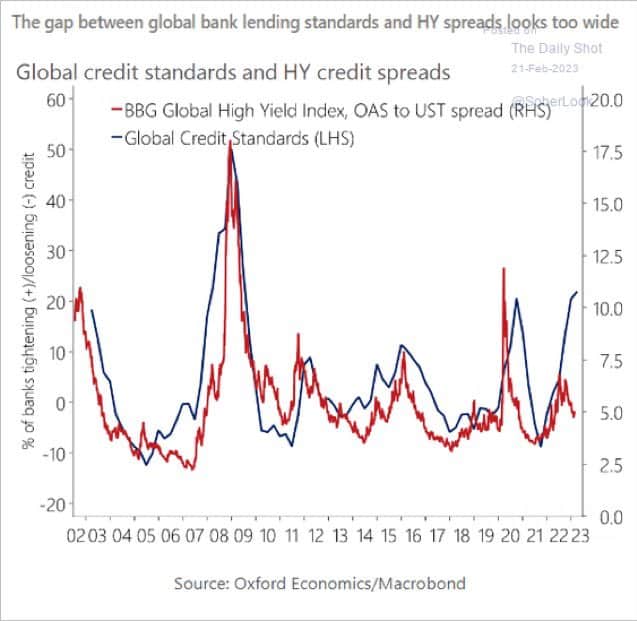

Another Confounding Look at Credit Spreads

In Corporate Bonds Have No Recession Fears, we discussed how corporate credit spreads versus Treasuries were below average despite the growing possibility of a recession. To wit: “The term “picking up pennies in front of a steam roller “comes to mind when looking at the graph below.”

Further to the conversation, consider the graph below. As it shows, the high-yield bond index and credit standards tend to be well correlated. Currently, the correlation has broken down. The risk is that yields catch up to credit standards, as is the norm.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.