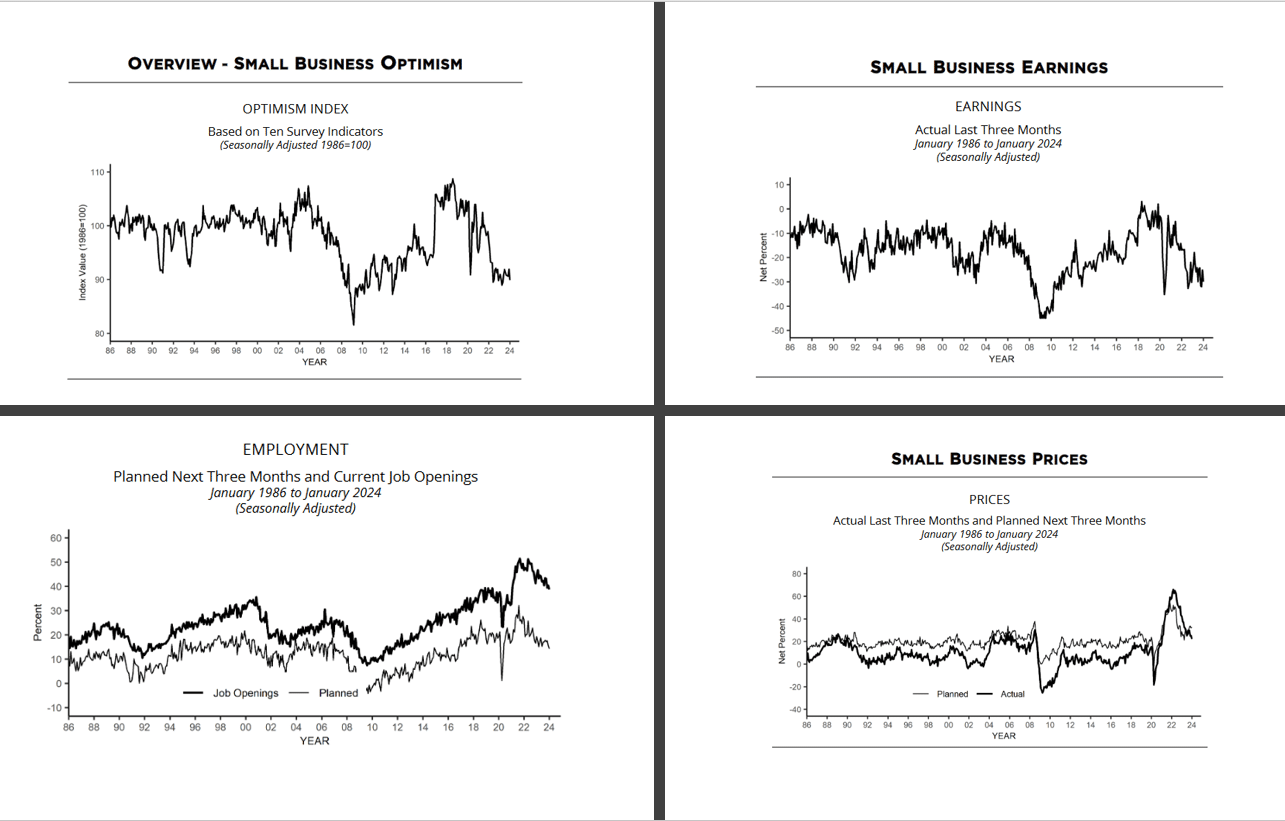

Per the U.S. Chamber of Commerce, 43.5% of GDP comes from small businesses. The Small Business Administration claims small businesses employ 46.4% of private sector employees, accounting for 62.7% of new jobs since 1995. With an appreciation for the economic importance of small businesses, let’s review Tuesday’s National Federation of Independent Business (NFIB) monthly sentiment index. The index fell by 2 points to 89.9, the largest decrease since December 2022. Jobs and inflation are the two most important factors guiding the Fed. Here is what the NFIB survey says about prices and employment trends for small businesses.

Jobs: 39% of small business owners reported job openings they could not fill in the current period. That is down slightly and the lowest reading since January 2021. Additionally, plans to fill open positions continue to soften, with a net 14% of owners percent planning to create new jobs in the next three months. That is the lowest since May 2020. The graph on the bottom left shows that job openings are back to their pre-pandemic peak, while planned hires are near 8-year lows. Inflation: The net percent of owners raising average selling prices declined 3 points to 22%. 15% of small business owners reported lower selling prices, the highest since August 2020. 20% reported that inflation was their single most important problem in operating their business. That is down 3 points from last month and 1 point behind labor quality as the top problem.

“Small business owners continue to make appropriate business adjustments in response to the ongoing economic challenges they’re facing,” said the NFIB’s chief economist Bill Dunkelberg. “In January, optimism among small business owners dropped as inflation remains a key obstacle on Main Street.”

What To Watch Today

Earnings

Economy

Market Trading Update

It was a tough day in the market yesterday, as a hotter-than-expected CPI report pushed rate cut odds out to July. As discussed in yesterday’s commentary, we started trimming positions on Monday with the expectation of correction coming, and yesterday may have signaled the start of a period of consolidation or further correction. Such also tends to align with the latter half of February, which tends to be weaker.

The selloff was board-based and reversed all the gains recently seen in the small and midcap markets which had shown a brief sign of life. However, continued negative sentiment from the NFIB reports suggests that small and mid-cap businesses continue struggling with slower economic growth and higher rates.

While a one-day correction doesn’t tell us much, any further concerted selling today could suggest a further retracement is forthcoming. While the CPI report pushed yields higher, we suspect the pressure in bonds will be short-lived. Such is particularly the case if the markets decline further and there is a rotation from risk to safety.

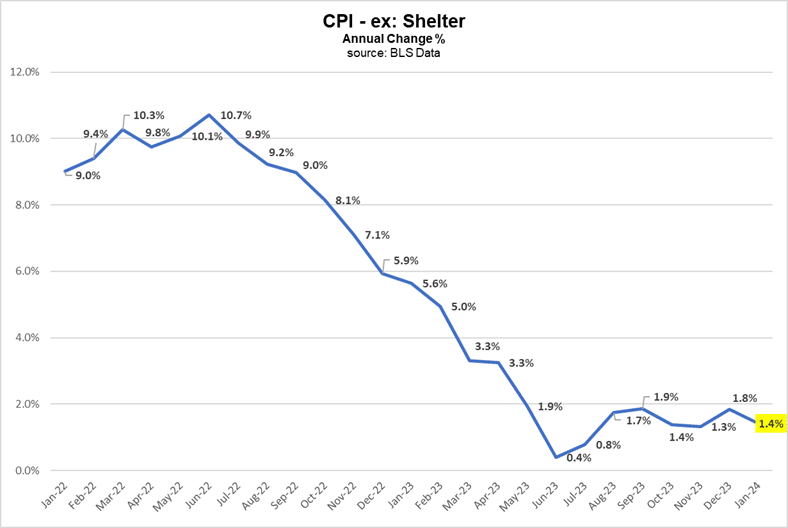

CPI Comes In HOT HOT HOT

The BLS CPI report was hotter than expected across the board.

- Core Inflation m/m was 0.4% vs forecast of 0.3%

- Core inflation y/y was 3.9% vs forecast of 3.7%

- Headline inflation m/m was 0.4% vs forecast of 0.2%

- Headline inflation y/y was 3.4% vs forecast of 3.1%

The most significant contributor to CPI, shelter costs, accounting for a third of CPI, rose unexpectedly by 0.2% to .06%. The shelter component lags real-time housing/rent data by at least six months. Rent prices fell, but imputed rent, based on a survey, rose. On a side note, the employment report imputes small business employment activity based on its survey of large companies. As we share in our opening, the BLS’s imputation does not align with what is actually occurring. We must question if the shelter prices are falling victim to the same problem.

Other factors were driving the hot inflation number. Per Goldman Sachs:

The increase largely reflected start-of-year price increases for labor-reliant categories such as medical services, car insurance and repair, and daycare, and we assume inflation in these categories returns to the previous trend on net in February and March.

To wit, auto insurance rose 20.6%, the largest increase since 1976. Nonprescription drugs increased by 9.2%, its largest gain ever. Lastly, the repair of household items grew by 18.2%, also the largest ever.

Stocks and bonds sold off significantly on the news as it implies that the Fed will stay on hold for longer. The Fed Funds market now prices the first rate hike for July. It was in June, prior to the CPI release. Additionally, there are only four rate cuts priced in for the year, down from a peak of seven.

Our take: Many factors that pushed CPI higher than expectations appear to be seasonal and temporary issues. While inflation rates may stay sticky for a while, we still think the overall direction of inflation will be lower. If the Fed stays on hold, that should help the overall inflation picture.

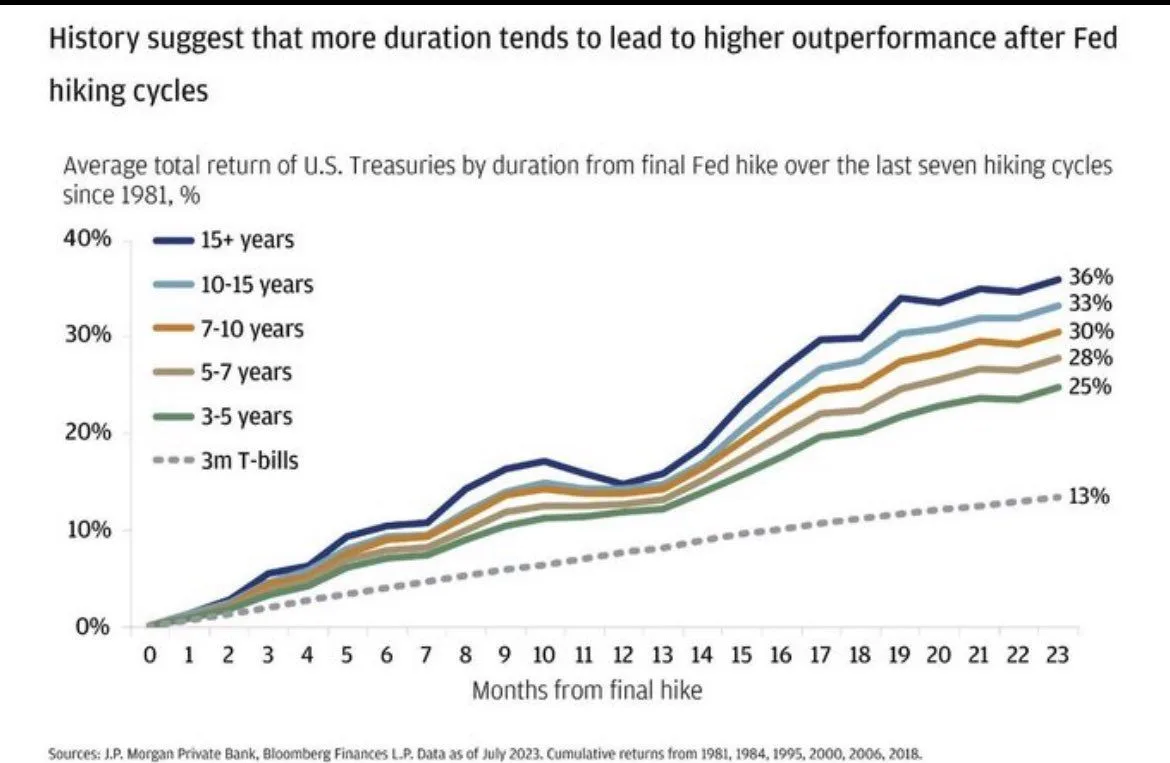

History Suggests Bond Prices Should Continue Upward

A look back at bond and Fed history offers bond investors optimism. If the Fed’s last rate increase on July 28, 2023, was the last of the cycle, then history says bond yields should continue to fall and prices increase. The biggest risk is what if the Fed raises rates again. We don’t think that will happen as the Fed remains vigilant against inflation.

Thus far, the last hike was 6.5 months ago. Since then, bond yields have underperformed the average path below. However, since bond yields peaked in mid-October, the gains are more aligned with historical averages. We attribute this to the fact that it was not evident that the Fed was done hiking rates in July.

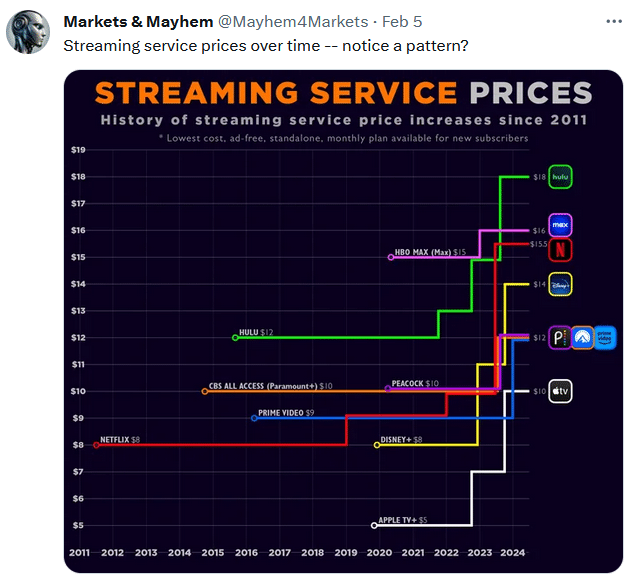

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.