The PCE Price Index is the Fed’s preferred inflation gauge, and it’s the inflation reading used by the BEA to calculate real GDP. On Friday, the PCE Price Index was 0.1% higher than expectations on the monthly and year-over-year readings. The core PCE Price Index, excluding food and energy, was also 0.1% higher than expectations and last month’s reading. Also, within the report, personal expenditures rose 0.8%, well above expectations of 0.3%. The data point to solid consumption, which in turn is keeping inflation sticky at relatively high levels.

The Fed recently said the decision to hike or not at the coming meeting would highly depend on recent data. Consequently, the PCE Price Index and consumption data will sway them toward hiking rates. Employment this week and CPI/PPI data next could certainly change the outcome. The table below shows that the Fed Funds futures market is now pricing in a 58% chance the Fed will hike rates in June. Further, it implies a 26% chance they will do a cumulative of 50bps in rate hikes by the July meeting. Also, traders have greatly diminished the odds of a rate cut by year-end.

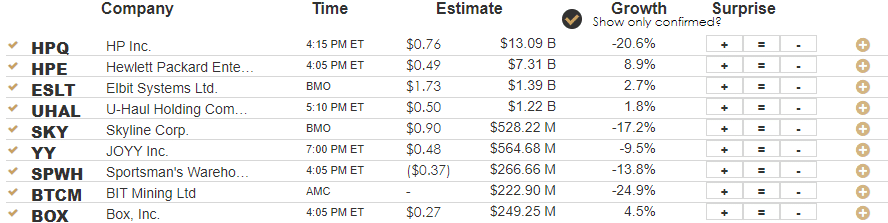

What To Watch Today

Earnings

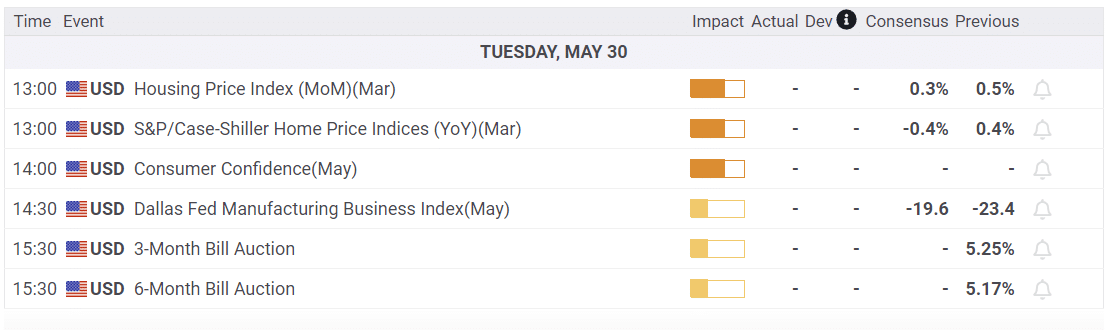

Economy

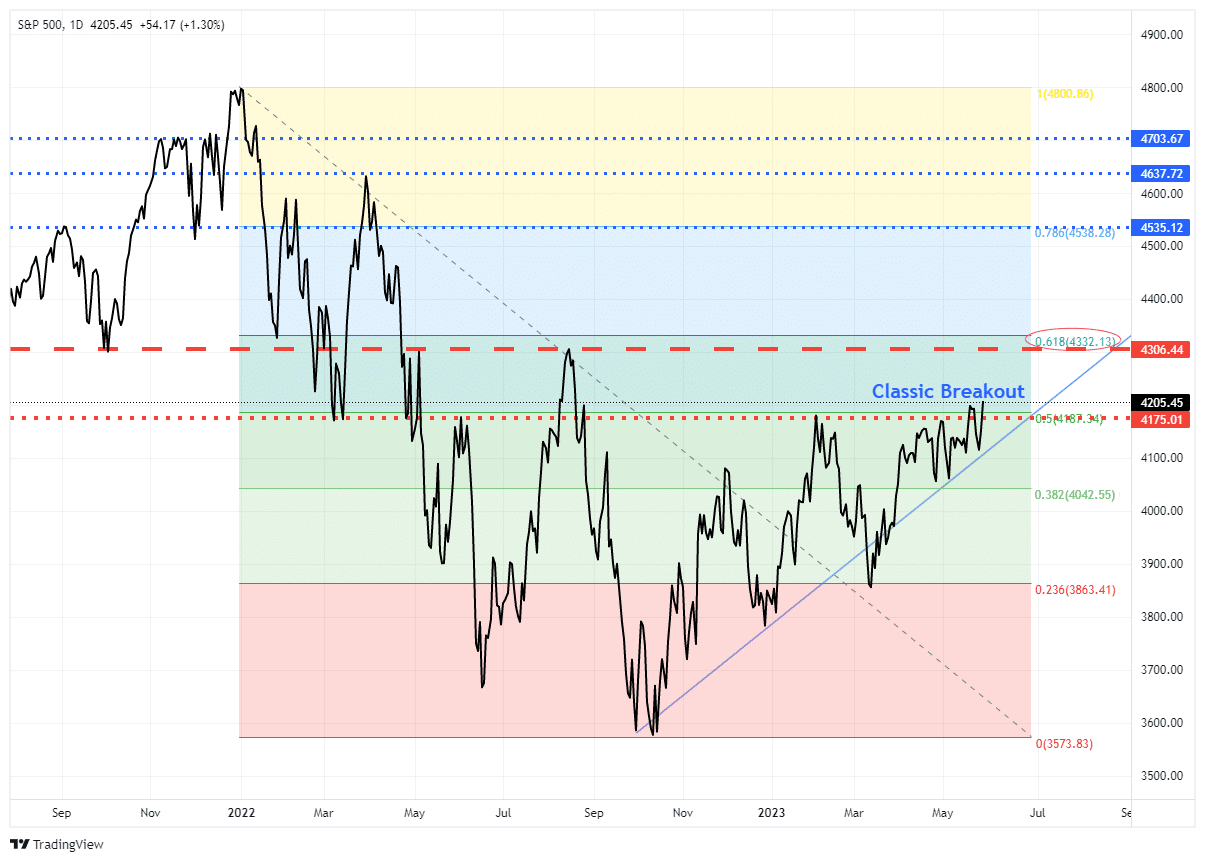

Market Trading Update

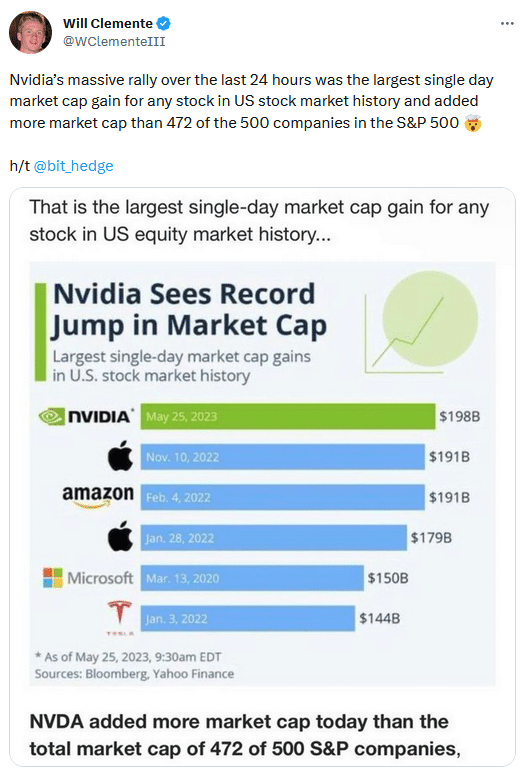

Following the breakout Friday before last, the market declined early last week, sparking concerns of a “fake out.” The market initially tested the rising bullish trend line from the October lows sparking concerns of more selling pressure. However, following Nvidia’s stellar earnings report on Thursday, the market staged a strong comeback and confirmed the breakout on Friday by setting a new closing high. This is a classic breakout of the consolidation range over the last couple of months.

This breakout is very bullish for two reasons. First, the market has completed a 50% retracement of the 2022 decline, which sets the stage for a further advance. Secondly, the breakout confirms the bullish trend that started from the October lows.

While many reasons exist to bearish, the market clearly suggests those concerns are misplaced. At least for now. The next resistance level for the market is the 61.8% Fibonacci retracement level at 4332 which is slightly above the July 2022 high of 4306. A break above those levels, and there is only some minor resistance to fully recovering from the 2022 decline.

The Week Ahead

Jobs data will be the focus of the economic calendar this week. JOLTs on Wednesday, ADP and Jobless Claims Thursday, and the BLS Labor report on Friday will update us on the state of the labor markets. Current expectations are for a slight weakening of data but nothing of concern.

Fed speakers will be vocal as it’s their last chance to speak before their self-imposed media blackout, heading into the June 15th FOMC meeting, which starts on Saturday. Based on comments and their minutes from the last meeting, it seems the Fed wants to retain the option to increase rates but does not want the market to think they will lower them. Per the May 2nd minutes:

Some participants stressed that it was crucial to communicate that the language in the postmeeting statement should not be interpreted as signaling either that decreases in the target range are likely this year or that further increases in the target range had been ruled out.

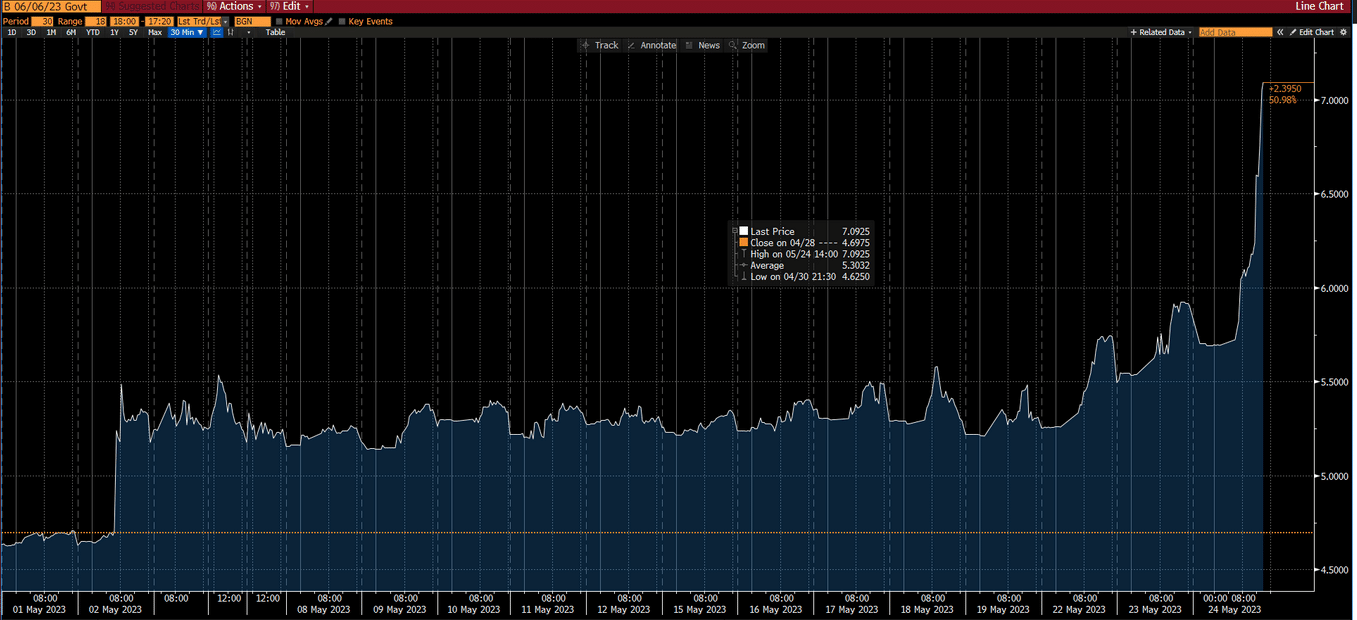

7% Treasury Yields are Not Concerning

The yields on very short-term Treasury bills rose over 7% as worries about the debt crisis and delayed interest, and principal payments loom. The graph below shows the yield of the Treasury bill maturing on June 6.

Some media outlets offered the high yield as evidence that the market is pricing in a default. They are wrong! What is occurring is that bill investors are worried interest and principal payments from the Treasury could be delayed.

Yields are presented on an annualized basis. Therefore a small yield change for a bill maturing in a week or two can greatly exaggerate its annualized yield. If we de-annualize the 2% difference between a 7% and 5% two-week bill, the yield pickup is four basis points or $40 per $100,000. On an annualized basis, each day of delayed coupon payment on a two-week bill equates to .40% of yield. As such, the market implies the Treasury could be five days late on Treasury bill payments. Remember that includes the potential for weekends when the Fed can’t make a payment even if the cap is resolved.

More on the Market’s Bad Breadth

We have discussed the market’s bad breadth on numerous occasions. What is important to consider is that periods like today of such narrow breadth are not sustainable. But they can last longer than you think. We share a few graphs below to highlight the current environment.

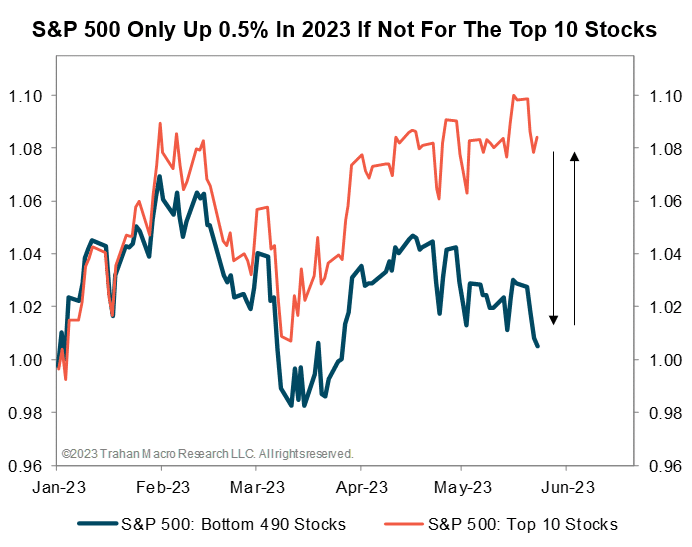

Ten stocks are responsible for nearly all of this year’s gains.

Over the last three months, only 20% of S&P 500 stocks are beating the index. Such nearly matches the low set in March 2000, on the eve of the dot com crash.

Similarly, the performance spread between the S&P 500 and the equal-weighted S&P 500 (RSP) is the widest since December 1999.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.