The past week’s labor market data continued to show strength. However, the week’s data varied wildly between reports, confusing investors. After ADP showed a whopping gain of 497k jobs last month, the BLS followed a day later with a relatively paltry 209k new jobs. Such was slightly below expectations. As we share in the Tweet of the Day, it was the first time in 15 months economists overestimated the jobs number. Before the pandemic, ADP and the BLS correlated well. But, over the last three years, they have proven less reliable indicators of each other. Consequently, forecasting labor market data has proven difficult.

While “only” 209k jobs were added in June, that is still a good number. From 2015-2019, the average gain was 188k, as shown below. Further, the unemployment rate fell from 3.7% to 3.6%, slightly above 50-year lows. Of concern for the Fed, average hourly earnings were a tenth of a percent above expectations on a monthly and annual basis. The Fed remains fearful about a price-wage spiral. This week’s labor market data will not dispel that notion. Barring an unexpected collapse in CPI next Wednesday, the Fed will hike rates by 25bps at the July 26th meeting.

What To Watch Today

Earnings

Economy

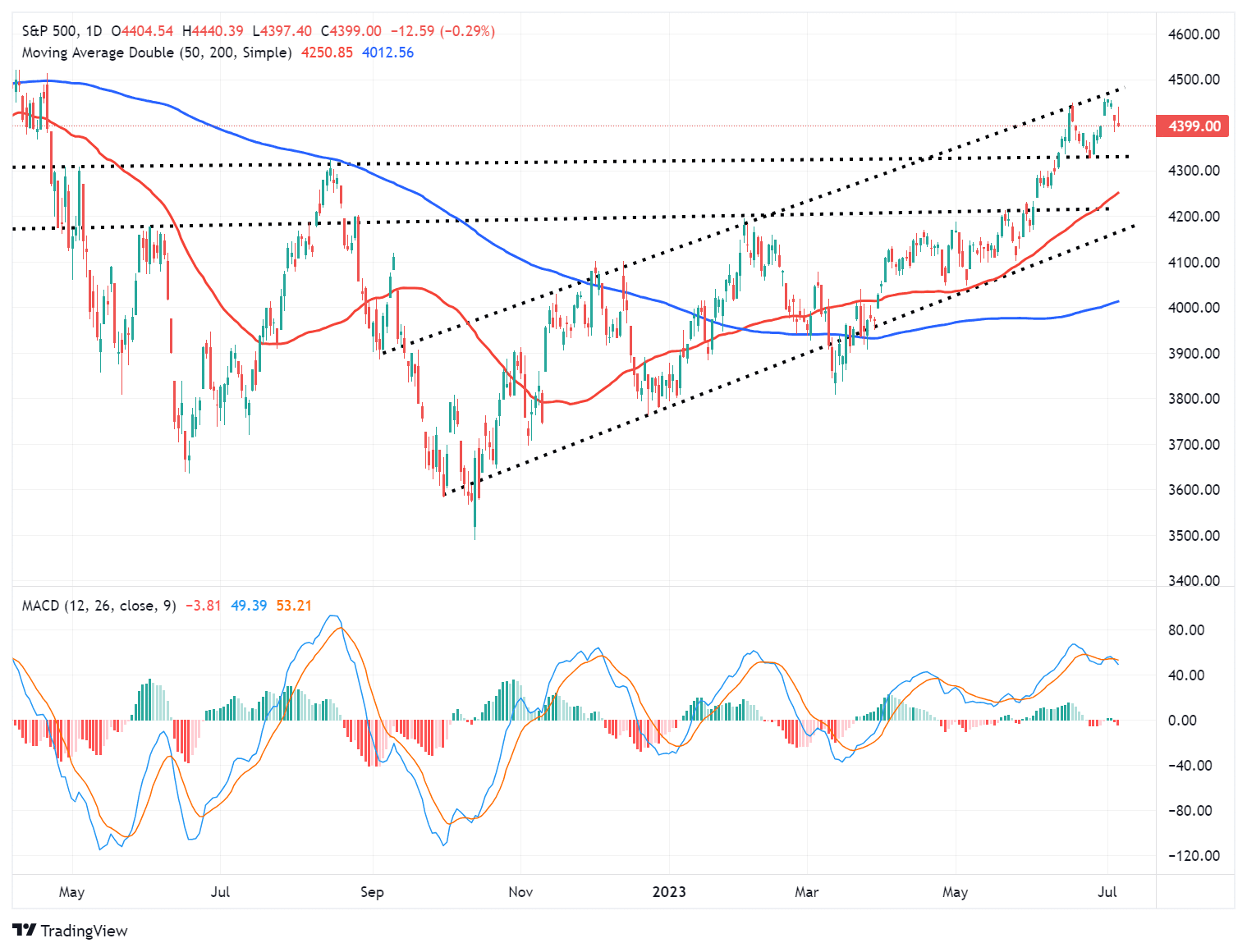

Market Trading Update

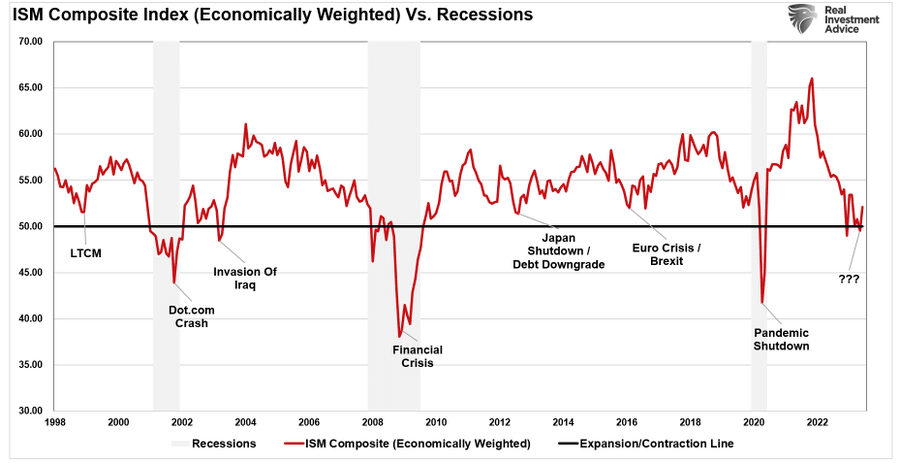

Last week’s economic data sent confusing messages through the market. A stronger-than-expected ISM Services number suggests that no recession is on the horizon currently. As noted in the chart below, there has never been a recession since the turn of the century when services (which comprise 80% of the economy) are not in contraction.

However, on Friday, there was a deterioration in the employment report which suggests the economy is slowing down. That news was received as bullish, sending stocks higher, as hope rose that the Fed would not need to continue hiking rates.

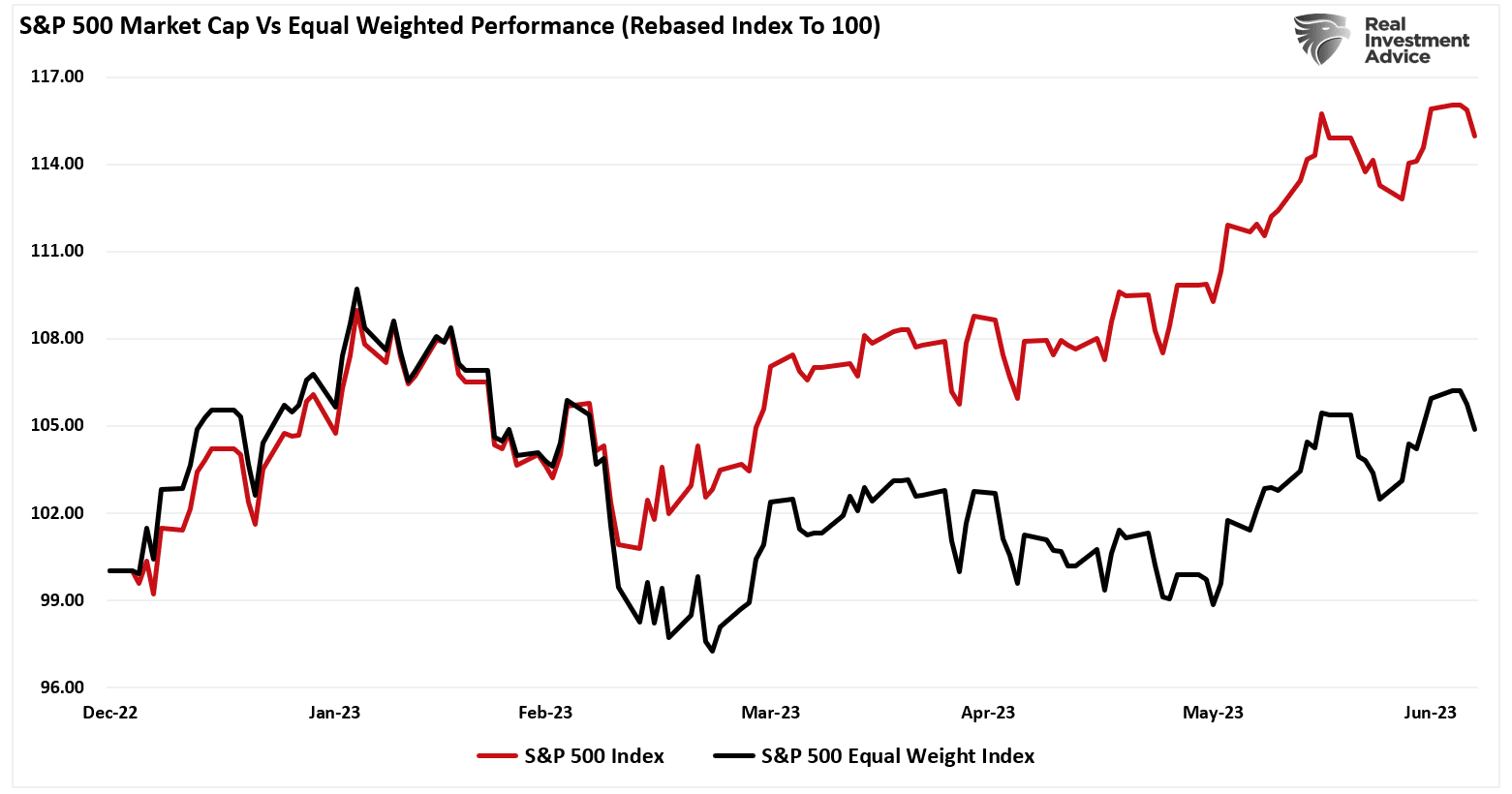

With Q2 earnings season set to start next week, the current momentum behind the market remains strong as investors continue to buy even the slightest dips in fear of missing out (F.O.M.O.) on further upside. Unfortunately, the bulk of the advance remains driven mainly by only a small handful of stocks, but breadth has improved somewhat in recent weeks.

Regardless, the market remains short-term overbought and deviated above longer-term moving averages. As noted, while momentum will continue to propel markets, such does not preclude an eventual correction resetting some of the overbought conditions. It is unknown when such a correction will occur or what will cause it. However, such a correction would provide a much better entry point to increase portfolio equity risk.

For now, hope remains that the Q2 earnings season will continue to support the bulls.

The Week Ahead

Following last week’s slew of labor market news, this week’s focus will be inflation. CPI on Wednesday, PPI Thursday, and Import/Export prices on Friday will update investors and the Fed on inflation trends. The headline year-over-year CPI data should be very encouraging. Expectations are for annual inflation to fall from 4% to 3.1%. Economists expect the monthly inflation rate to rise by .2%, which equates to 2.4% annually. While inflation is falling back to norms in those headline numbers, the Fed will focus on core price data which has proven much stickier. Unlike the broad CPI, the year-over-year core inflation rate is only expected to fall from 5.3% to 5%.

The graph below shows the problem with forecasting CPI. Housing accounts for over 30% of CPI, yet CPI price data tends to lag real-world data significantly. The catch-up should help bring CPI back toward the Fed’s 2% objective.

PPI, which tends to lead CPI, is more encouraging. The PPI Core rate is expected to fall from 2.8% to 2.6%, while the headline PPI is only expected to be 0.4%.

Also, this week will be a bunch of Fed speakers. We expect them to largely warn of a rate hike at the next meeting and then a wait-and-see approach regarding future hikes. Second quarter earnings releases will start as well this week. Many of the largest banks, including JPM, WFC, C, and BLK, will report earnings on Friday.

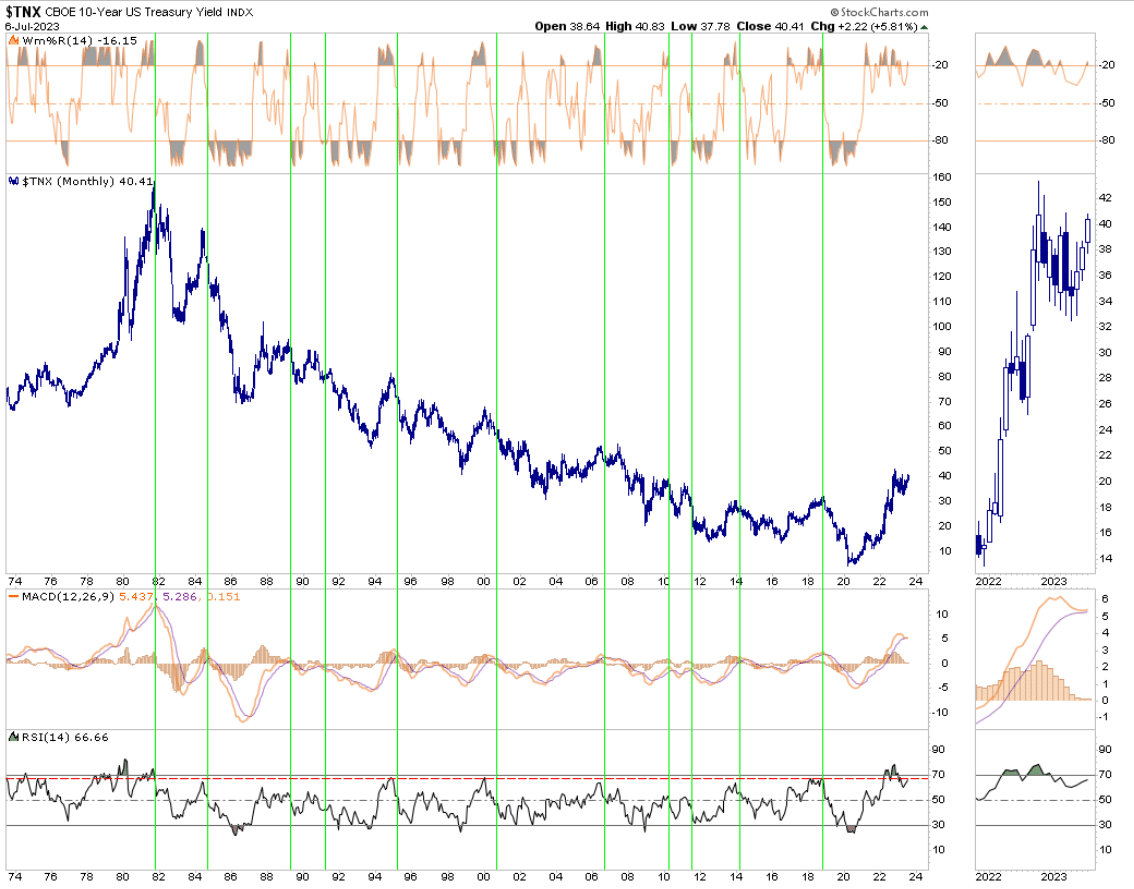

Got Bonds?

The recent increase in bond yields may not be over, but two critical technical indicators signal lower yields may be ahead. The graph below charts monthly ten-year UST yields. Using monthly versus the more common daily prices allows us to step back from the daily yield variations and get a broader perspective. Technical signals on longer-term graphs tend to be stronger than shorter-term graphs but are also harder to time as you possibly have to wait up to a month for a technical confirmation.

The graph below shows the MACD is very high and just about to cross. As the green vertical lines highlight, such a cross since 1980 has been bullish. The RSI tends to line up well with the MACD and is also at a very overbought level, again meaning yields are likely to decline. While longer-term technicals tell a nice story, the current fundamentals work against lower yields. The markets seem to believe that inflation will stay elevated, economic activity will remain robust, and the Fed will keep rates at current levels or higher for a year. It will likely take weaker economic data, including the labor market, along with signals from the Fed that they will not raise rates further before a durable bond rally can start. While that may take a while, history reminds us that shifts in sentiment can occur relatively quickly. As we shared yesterday:

In 2007, the Fed started reducing Fed Funds in July, corresponding with the peak in 5 year real rates. Six months later, the 5 year real rate was near zero. The decline was solely a function of falling yields. In 2018, the Fed halted raising rates, and the 5 year real rate peaked at 1.08%. It fell to zero in about six months, again almost entirely due to yield not expected inflation.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.