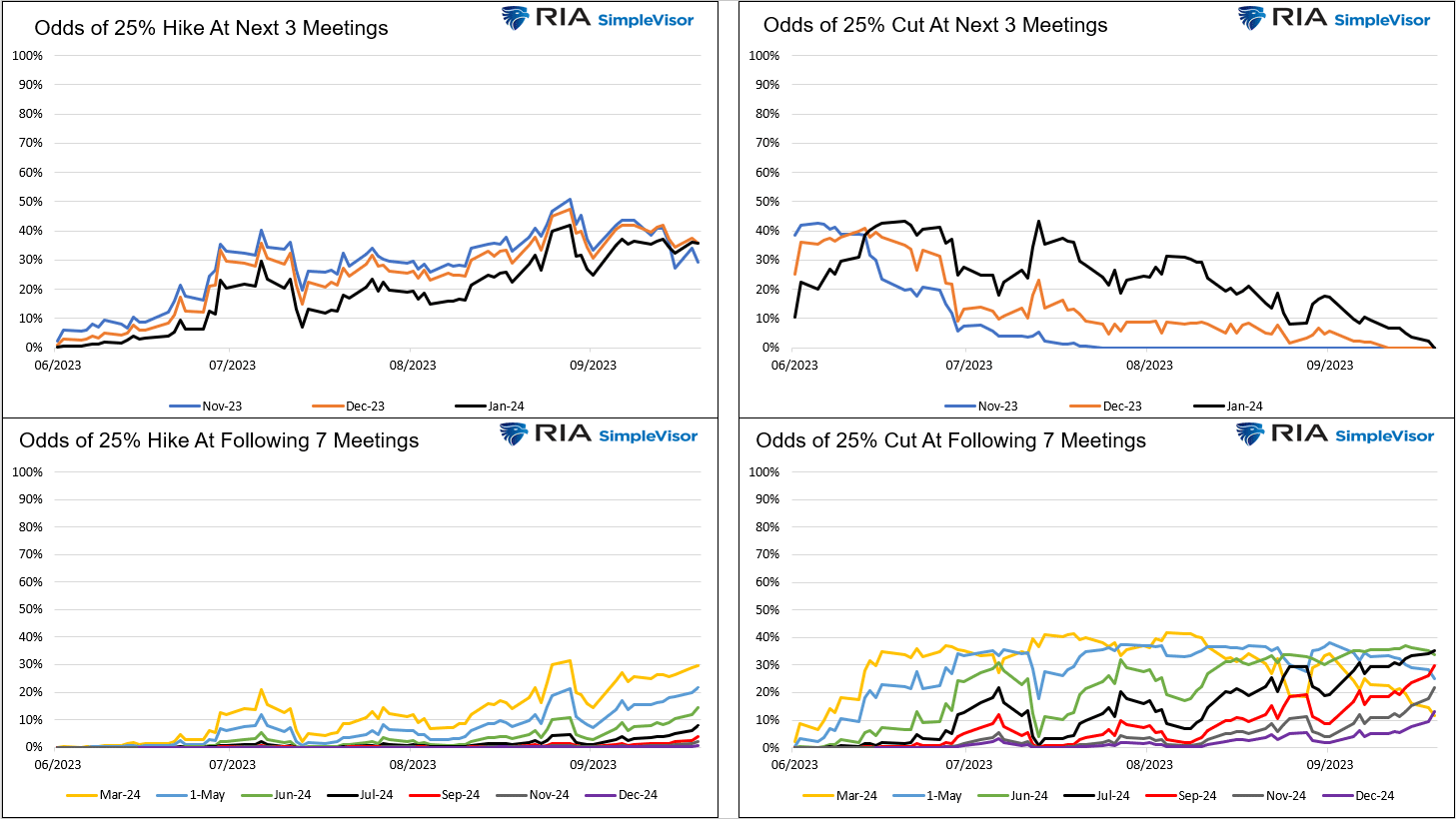

Jerome Powell and the Fed have been pounding the “higher for longer” table to prepare the markets for a sustained period of high interest rates. Powell did not waiver from the stance at yesterday’s post-FOMC press conference. Until the last few months, the Fed Funds futures market didn’t agree with the Fed’s higher-for-longer mantra. However, the Fed’s consistent messaging, sticky inflation, and robust economic growth have the market rethinking its stance. For example, with Fed Funds at 4.25-4.50% last January, the odds of the Fed raising rates to its current level (5.25-5.50%) by year-end were only 1.5%. The odds greatly favored a 1% rate cut by year-end. Simply, the market did not believe in higher or longer.

The graphs below quantify how the market has adjusted to the Fed’s persistence since June. The left graphs show the odds of a rate increase at the next 3 Fed meetings and the following 7. The odds of another hike by January are clustered around 35% but have been slightly declining recently. Conversely, the odds of another hike between March and December 2024 are rising. The graphs on the right show the odds of rate cuts. The top chart shows the odds of a rate cut by January 2024 are now zero. They were nearing 50% in June. The odds of a Fed rate cut in March or May 2024 are falling. From July 2024 and out, the odds of a cut have been increasing. The bottom line is the market is estimating higher for longer until July 2024 but not ruling out higher for longer for the entire year.

What To Watch Today

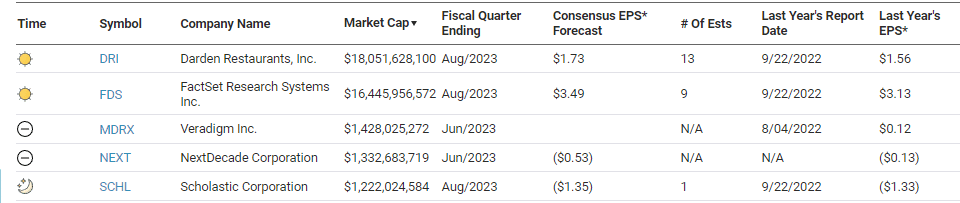

Earnings

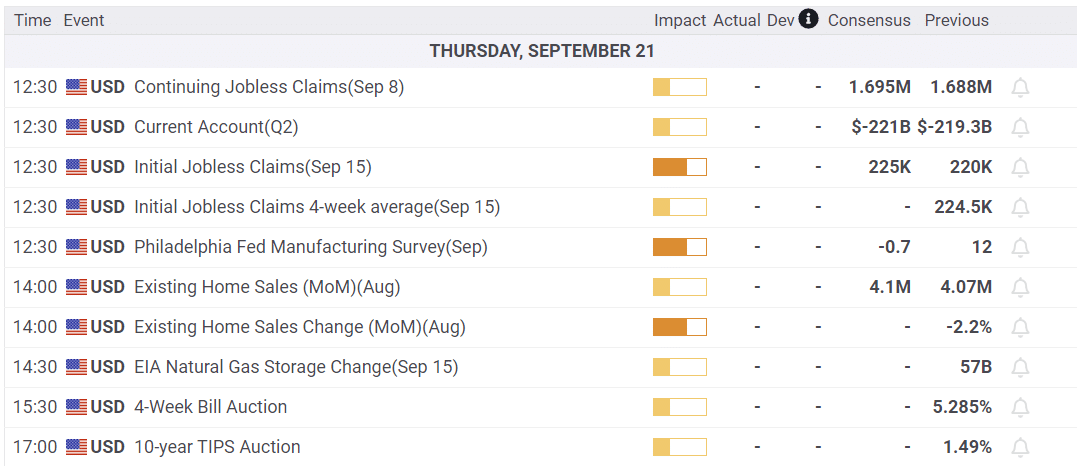

Economy

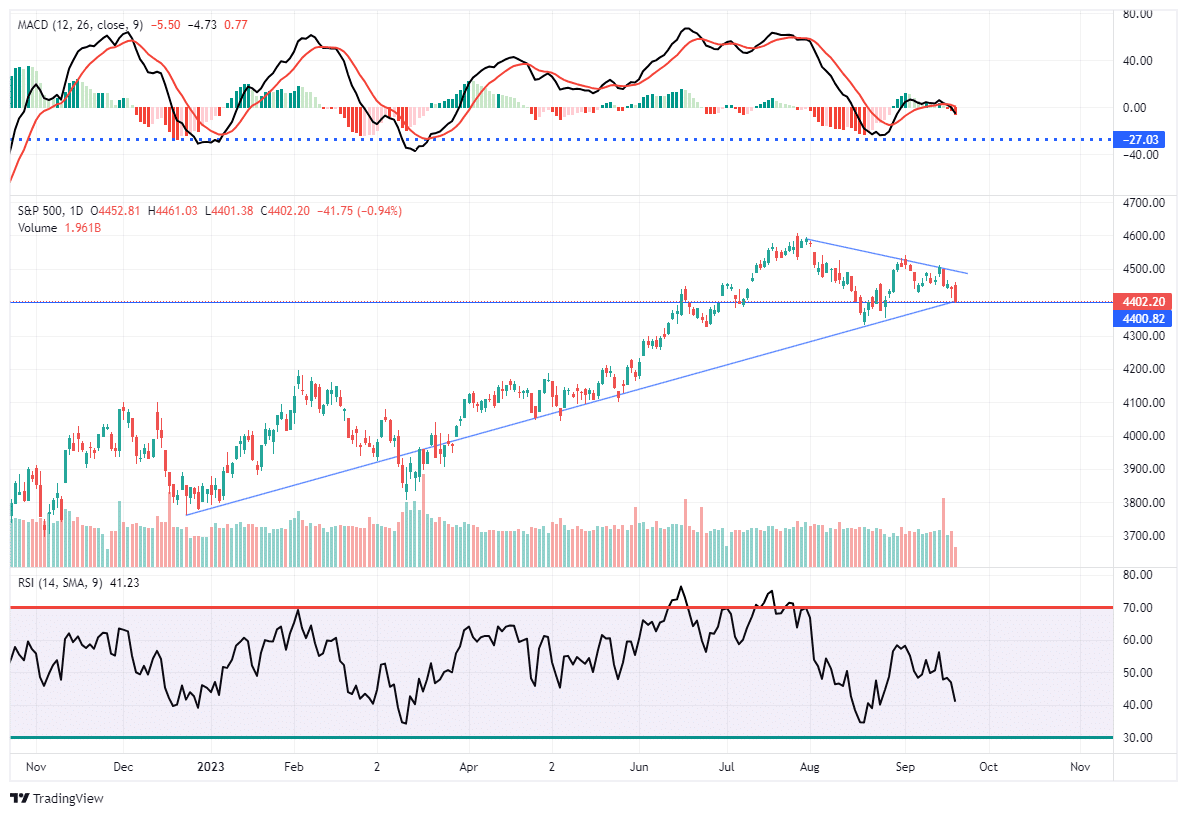

Market Trading Update

The market traded off yesterday following the Fed’s statement, which, unsurprisingly, was virtually no different than what was said last time. However, the projections seemed to startle the markets, with the central bank’s benchmark overnight interest rate peaking this year in the 5.50%-5.75% range, just a quarter of a percentage point above the current range.

“But from there, the Fed’s updated quarterly projections show rates falling only half a percentage point in 2024 compared to the full percentage point of cuts anticipated at the meeting in June.

With the federal funds rate falling to 5.1% by the end of 2024 and 3.9% by the end of 2025, the central bank’s main measure of inflation is projected to drop to 3.3% by the end of this year, to 2.5% next year and to 2.2% by the end of 2025. The Fed expects to get inflation back to its 2% target in 2026, which is a later date than some officials had thought possible.”

The trouble for the markets, of course, is that they have been banking on rate cuts sooner rather than later. As such, the “later” upset market participants, and duration-sensitive stocks, read Technology, came under pressure. Nonetheless, the market remains bullish for now, and the short-term sell signal suggests some continued sloppy action over the next week or so before earnings season can lift the bulls.

The Fed Statement and Jerome Powell

The Fed did not hike interest rates as was widely expected. The FOMC statement, redlined below by ZeroHedge, shows the Fed made minimal edits to the statement from the July 26 meeting. They acknowledge some slowing of job growth but that the labor market remains strong.

Powell’s comments were similar to his prior post-meeting press conference. Here are key takeaways:

- The full effect of rate hikes “remains to be felt.”

- He is determined to get inflation back to 2% as quickly as possible.

- There was unanimous support for no rate hike, but there seems to be less agreement about whether to hike at the next two meetings. Incoming economic data and perceived risks will determine upcoming decisions.

- “We are fairly close to where we need to get.”

- Jerome Powell says a soft landing is NOT his baseline expectation, but he didn’t expand on whether that implies a recession or a continuation of strong economic growth. That said, he stressed that a soft landing is the Fed’s primary objective.

- On numerous occasions, Powell mentions the lag effects and the risk they pose to the economy and Fed forecasts.

- Is stronger than historical GDP growth an impediment to getting inflation back to 2%? That question appears to be a primary Fed concern.

- The Fed is looking through recent increases in oil prices, but they will reconsider the risks if oil prices remain at current levels or higher. He reiterates core inflation, excluding food and energy, is their preferred method for assessing inflation.

- “The worst thing we can do is fail to restore price stability.” Their primary goal is to get inflation to 2%, and he stressed multiple times it will take precedence over economic weakness and higher unemployment.

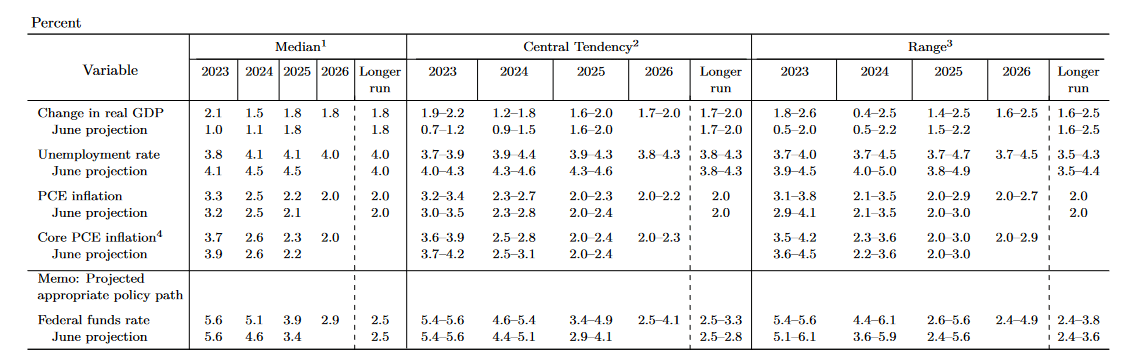

Federal Reserve Economic and Rate Projection Revisions

Every quarter, the Fed releases its summary of economic projections, aka Fed dot plots. Investors compare the most recent release versus the prior one to help assess how the Fed’s collective mindset is changing. The four categories the Fed projects are GDP, unemployment rate, inflation, and Fed Funds.

The table below shows the latest projections and the changes from June. As we led with, “higher for longer” is the theme of the projections. To wit, the Fed Funds rate projection for 2024 and 2025 rose by .50%. Further, the 5.60% ending rate for 2023 implies they are forecasting one more rate hike this year. Of the projections of the 19 Fed members, 12 see one more rate hike, while seven think the Fed is done hiking for this cycle.

The reason for the higher for longer Fed Funds forecast is an increase in their GDP expectations for 2023 and 2024 and lower unemployment forecasts for 2023, 2024, and 2025. However, their inflation projections were largely unchanged. They reduced their core PCE forecast for year-end 2023 to 3.7% from 3.9% but increased the broader PCE forecast by a tenth of a percent. They do not appear worried about a resurgence in inflation, but their projections lead us to believe they are concerned they will linger above their 2% target.

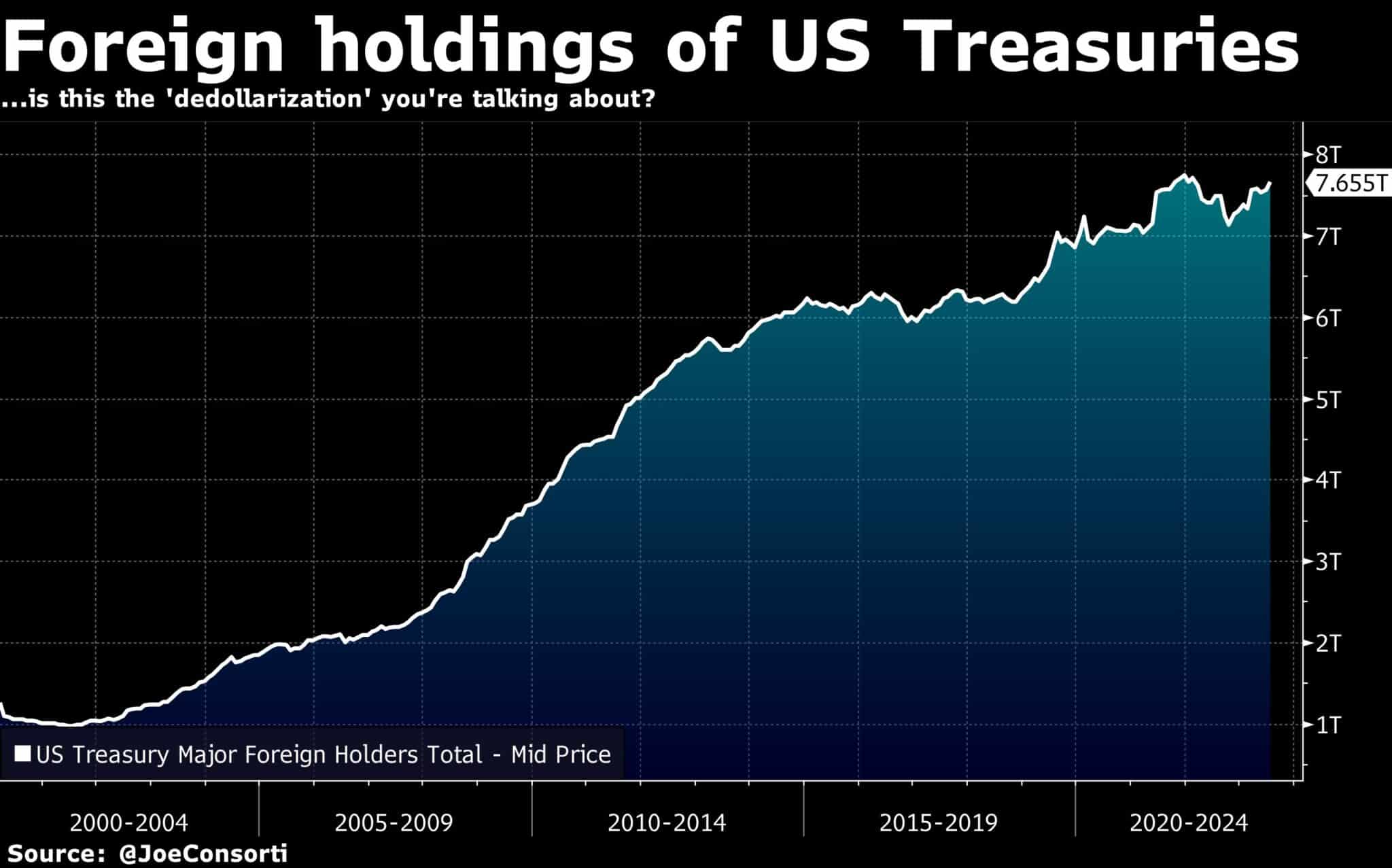

Foreign Holdings of U.S. Treasurys Continue to Rise

For those claiming the world is moving away from the dollar as the world’s reserve currency, evidence of such action is hard to find. We have discussed de-dollarization numerous times and provided proof that even the loudest de-dollarization advocates are taking pro-dollar actions. The graph below furthers our claim that foreigners continue to require dollars. It shows that foreign holdings of U.S. Treasuries rose to $7.655 trillion in July, which is 2% higher over the last year, and sits just below all-time highs. If de-dollarization were the goal for some countries, they would have to sell U.S. Treasury securities to convert their reserves to another currency.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.