Powell delivered remarks to Congress yesterday on the outlook for the economy and banking system. His prepared remarks were strikingly similar to those made at last week’s FOMC press conference. This is no surprise as Powell is making an effort to avoid speculation that the Fed is near the end of its tightening cycle. In response to a question, he implied that the Fed pause is temporary but emphasized the FOMC’s dependence on incoming data.

The Fed funds futures market remains on the same page as Powell, at least through the end of this year. The table below, courtesy of the CME’s FedWatch tool, shows that traders expect one more hike at the July meeting. In contrast, the dot plot from last week’s FOMC meeting showed participants expect two more rate hikes this year. Either way, the pause is temporary, most likely, for now.

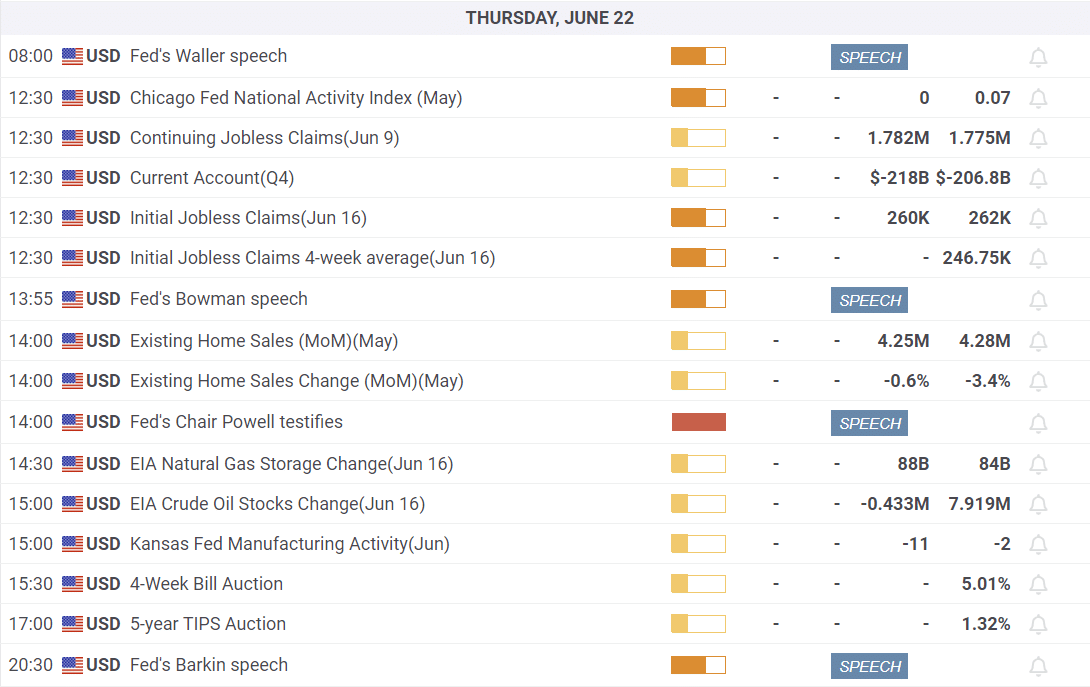

What To Watch Today

Earnings

Economy

Market Trading Update

Yesterday, Jerome Powell remained very hawkish about the prospect of further rate hikes, suggesting “pause” is temporary.

“Inflation pressures continue to run high, and the process of getting inflation back down to 2 percent has a long way to go. Nearly all [officials] expect that it will be appropriate to raise interest rates somewhat further by the end of the year.”

Such is certainly not the commentary the market’s have been betting on hoping for rate cuts. However, the makret largely dismissed it yesterday despite the fact the Fed continues to reiterate its position to slow both economic growth and employment.

“Reducing inflation will likely require slower economic growth and “some softening of labor market conditions. The economy is facing headwinds from tighter credit conditions for households and businesses, which are likely to weigh on economic activity, hiring, and inflation, though the extent to which remains uncertain.“

Nonetheless, given current momentum, combined with rising sentiment and still weak positioning, the market shook off these comments yesterday ending down only slightly. Overall the market continues to remain overbought, but the correction process, and sector rotation, we have mentioned over the last couple of weeks appears to have started. There is still some downside risk currently heading into month end, also the end of the quarter, where portfolios will need to be rebalanced.

Remain cautious for the moment and look for the market to find some support and reduce the current overbought condition somewhat before substantially increasing equity exposure.

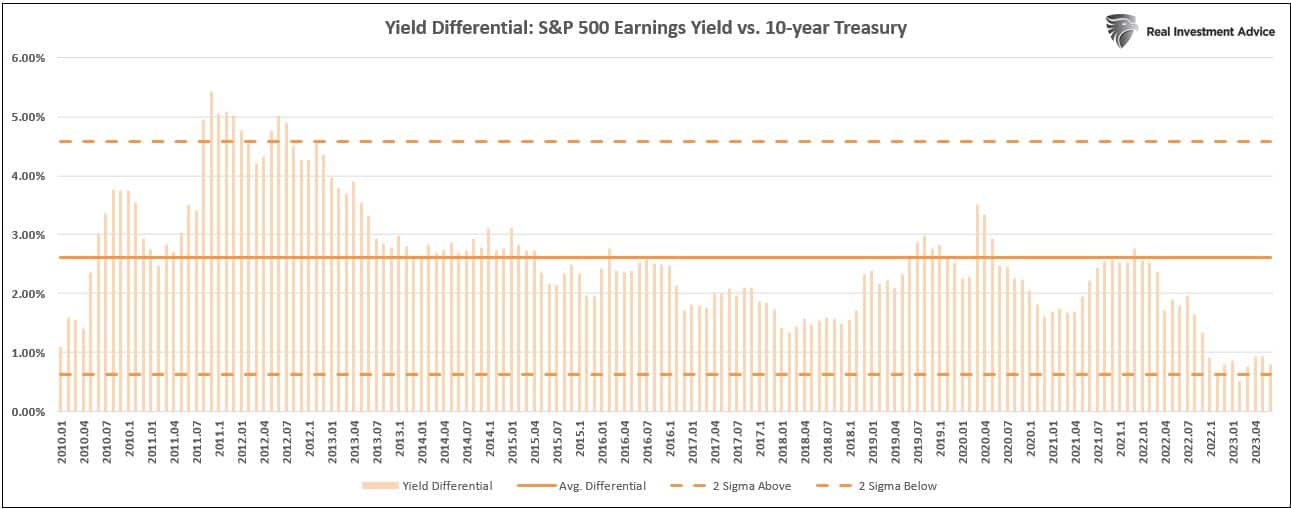

A Variation of the Fed Model

The Fed Model is a valuation technique that compares the S&P 500 earnings yield to the 10-year treasury note yield. Traditionally, the Fed model posits that the index is overvalued when the earnings yield falls below the treasury yield. Likewise, it’s undervalued when the earnings yield is higher than the treasury yield. Its utility has diminished since the Fed embarked on QE overload, but we can still examine this relationship over time.

The chart below shows how the yield differential has evolved in the period following the Great Financial Crisis. While the differential has been positive over the entire period, it typically stays within a one standard deviation band around the average. However, the differential currently resides nearly two standard deviations below the average. This chart is another illustration of how far extended the market is on a fundamental basis, given the current level of interest rates. Something must give before this chart normalizes, again making a fundamental case for limited upside potential in equities from here.

An Emerging Risk to Financial Stability

Concerns about systemic financial risks tied to cloud technology are growing in the eyes of regulators. The US Treasury recently launched the “Cloud Executive Steering Group”, an oversight committee for cloud computing, which has largely gone unnoticed. In an opinion piece published by the Financial Times last week the author highlights a few reasons for regulators’ concern.

According to a report from the Treasury’s Financial and Banking Information Infrastructure Committee, more than 90% of American Bankers Association members are migrating their activities to the cloud. Furthermore, the report estimates a tripling of cloud usage in the next three years. As the author states, a significant issue is that financial regulators are unprepared to manage this growth. This stems from their historical lack of tech expertise and that cloud activity places much of financial activity under Big Tech companies that central banks have never scrutinized. Moreover, available data indicate growing concentration risks due to cloud computing’s domination by an oligopoly of Amazon, Microsoft, and Google. Systemic shocks would be likely in case of cyber-attacks or other disruptions of these major players. The author concludes,

Sadly there are no easy solutions; or not unless the US government does something it seems unwilling or unable to contemplate — namely, break up Big Tech and/or impose tight government controls. But if nothing else, the issue shows that AI is not the only tech topic that matters now.

Pandemic Superstars: Where are they now?

Some stocks offering the most explosive returns throughout the early stages of the pandemic have fallen sorely out of favor. The chart below shows the value of $1,000 invested at the start of the pandemic through May 22, 2023. Of the five trades pictured, only two (MRNA and ETSY) are still sitting in positive territory. Yet even they have come sharply off their peak. The moral of the story is twofold. Stay grounded in fundamentals when valuations explode, and try not to overstay your welcome in an opportunistic trade.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.