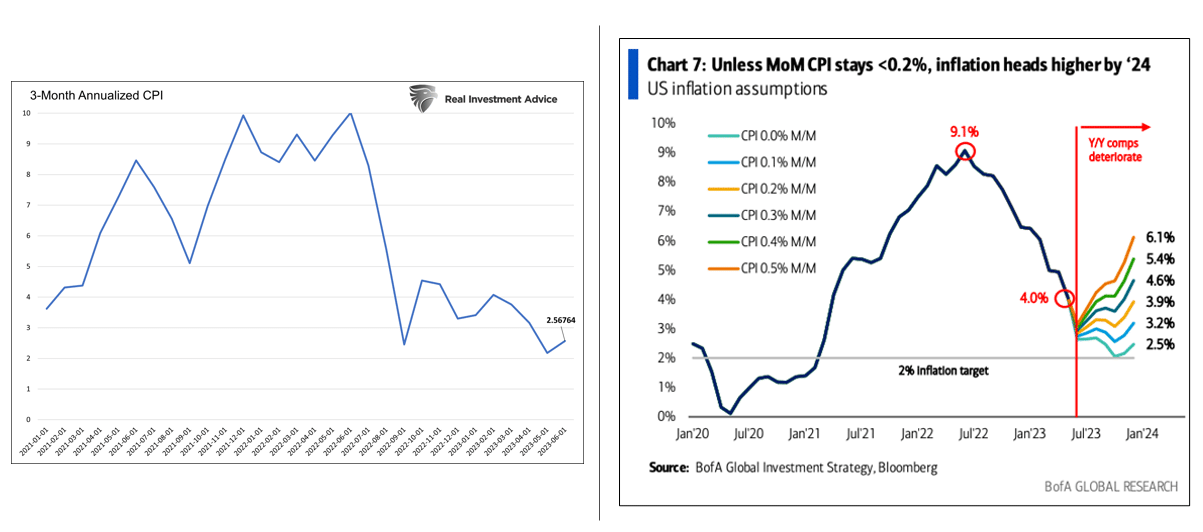

The BofA graph below (right) is making the rounds on Twitter and causing investors quite a dilemma on how to think about CPI. Barring zero monthly rates of CPI for the rest of the year, CPI, computed on a year-over-year basis, will increase. Investors’ dilemma is decoding the stark differences between changes and absolute levels of monthly and annual CPI figures. For example, yesterday’s annual CPI fell from 4.0% to 3.0%. The reason for the considerable drop has little to do with the latest monthly CPI figure. Instead, the 1.2% monthly increase in CPI from a year ago fell out of the annual calculation. Thus the dilemma facing investors is how much stock we should put into recent CPI data versus older inflation data.

To appreciate the dilemma, if next month’s monthly CPI figure is 0.1%, the year-over-year inflation rate will increase from 3.0% to 3.1%. Despite an annualized monthly inflation rate of only 1.2%, annual CPI will increase as a 0.00% monthly figure from a year ago will fall out of the calculation. When CPI is not volatile, as was the case pre-pandemic, year-over-year CPI provides a good inflation trend. However, when it’s volatile, we prefer to follow annualized data from the last three months. Such reasonably estimates recent inflation and ignores older and less relevant data points.

What To Watch Today

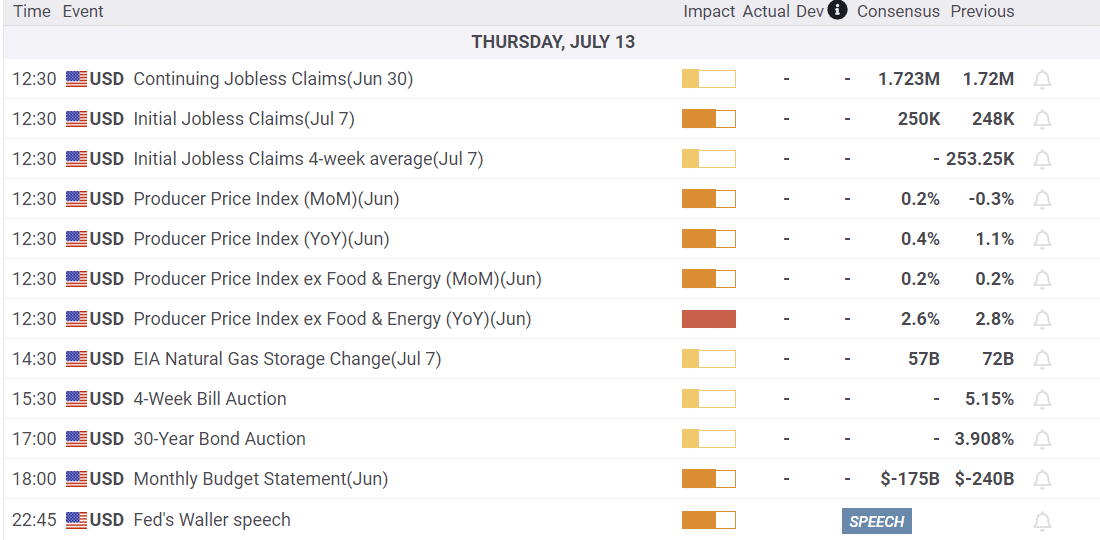

Economy

Earnings

Market Trading Update

As noted above, the Q2 earnings season is officially underway. Yesterday morning on our “Before The Bell” podcast, I noted the market had been in a tight consolidation range over the last couple of weeks. A weak inflation print would likely lead to an upside break of that trading range and support higher near-term prices. That inflation report was “market-friendly,” with the core inflation components showing signs of trending disinflation.

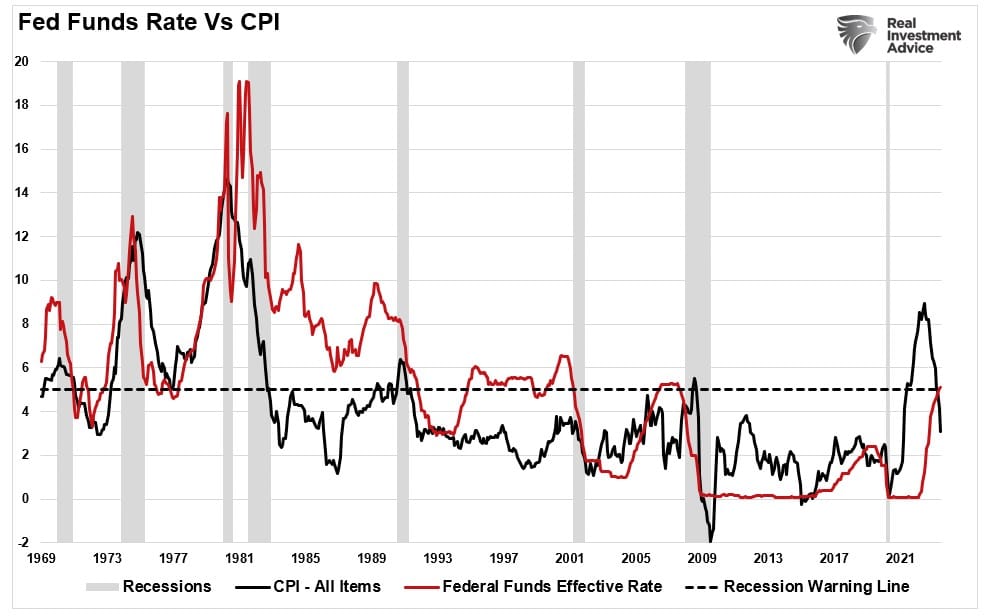

With inflation now at 3%, history suggests the Fed should cut rates. As shown, each time inflation has fallen fairly sharply, the Fed was also cutting rates to offset the recessionary impact. This is what the “bulls” are betting on in the market advance this year. However, this time is different, with the Fed focused on ensuring no re-inflation is coming. Such could mean higher rates for longer than the market is currently expecting, which may come with an eventual cost.

We will see what happens, but the bulls are clearly in control now. With the breakout above resistance yesterday, there is currently no reason to be overly cautious. We will eventually get a correction to work off some of the more extended deviations from longer-term means, but that could take longer than what seems logical. For now, low volatility, lots of bullish optimism, with a heaping spoonful of “hope” trumps a low liquidity environment.

More on the Inflation Data

Breaking News: Inflation cools sharply in June, good news for consumers and the Fed.– New York Times

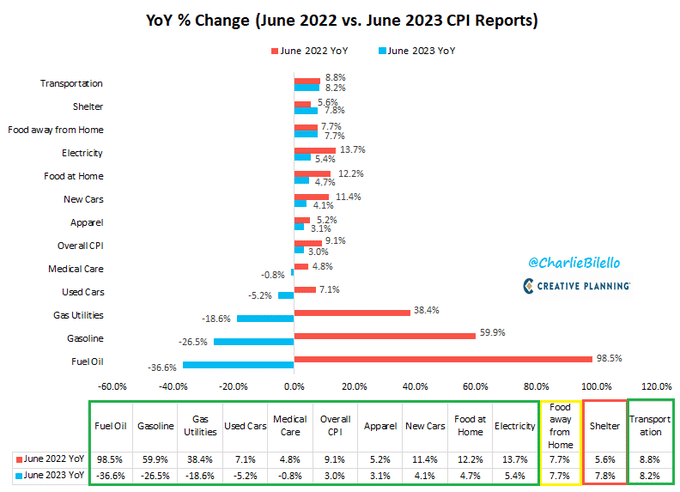

The media is celebrating the sharp drop in year-over-year inflation from 4% to 3%. The actual un-rounded number is now below 3% at 2.97%! While the Fed no doubt likes that number, they are probably more enthusiastic because the annual and monthly core CPI figures were below expectations. Importantly, core CPI fell below 5%. That marks the first time it was below 5% since November 2021. Further, the monthly core was 0.2%, its lowest point since August 2021.

Jerome Powell closely follows Core CPI services, excluding housing/rent (shelter). That figure was +0.1% monthly. On a three-month annualized basis, it is running at 1.4% compared to its peak of 5.2% in March. The third graph below shows it’s still running at 4% annually, despite the recent string of low monthly prints. Assuming this price index continues at current rates, Powell will likely remove future hikes from his forecast.

The second chart below, courtesy of Charlie Billelo, shows that shelter is the only significant contributor to CPI that is still higher versus last year. At over 30% of the CPI calculation, shelter prices are probably the most crucial factor in forecasting CPI. Per commentary from Charlie:

Shelter is the only major component that has a higher inflation rate than a year ago and it is a wildly lagging indicator (actual housing inflation is much lower w/ home prices/rents down YoY).

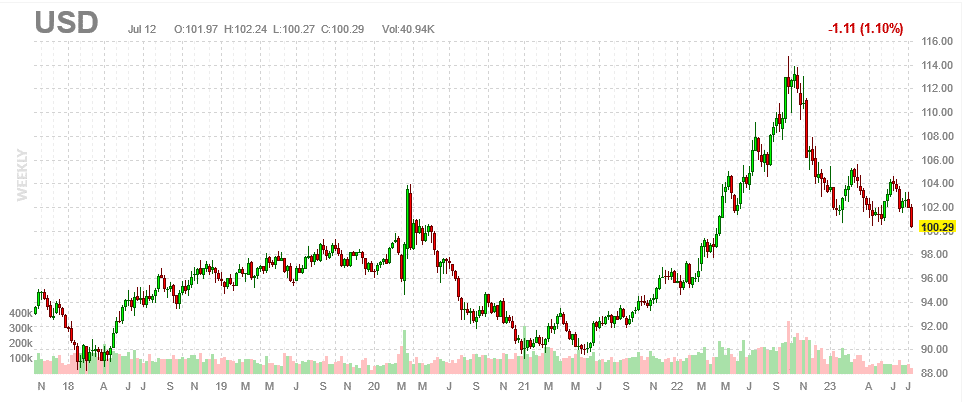

The Dollar Doesn’t Like CPI Data

The dollar index fell sharply yesterday on the weaker-than-expected CPI data. As we highlight below, the dollar index is clinging to the critical support of the recent lows. A real break from current levels leaves another 5-10% downside for the dollar. Such a decline, on the margin, should be supportive of U.S. stocks and bonds. The dollar is weakening because the CPI data implies the Fed may be getting closer to halting hikes and ultimately cutting rates. More dovish policy relative to other central banks concerns dollar holders.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.