The Bank of Japan’s (BOJ) policy meeting on Tuesday resulted in a shift away from yield curve control (YCC). Per the BOJ: “With extremely high uncertainties surrounding economies and financial markets at home and abroad, the Bank judges that it is appropriate to increase the flexibility in the conduct of yield curve control so that long‐term interest rates will be formed smoothly in financial markets in response to future developments.” Central banks use YCC to prevent yields from rising above a self-imposed limit. The graph below shows the cap on the ten-year note was at 0.50% until it recently lifted the cap to 1%. To cap rates, the BOJ buys Japanese bonds (QE), which weakens the yen. With the yen plummeting, the BOJ is relaxing YCC in hopes it stops the yen’s decline. For more details on Japan’s tricky situation, read the article we wrote on the topic.

So why should we care?

If the BOJ left a firm cap on yields, they would have likely been forced to support the yen as it would have weakened further. To do so, they would likely sell U.S. Treasury securities and use those dollars to buy yen. Given the recent rise in U.S. yields, we presume the U.S. Treasury pressured Japan to relax YCC instead. If the U.S. Treasury and BOJ are working together, the Fed can open currency swap lines so Japan can avoid selling Treasury securities if the yen continues to weaken. As we elaborate in a section below, U.S. Treasury yields typically correlate strongly with the yen. Accordingly, the BOJ actions and any they may take in the future have meaningful effects on the broader global asset markets. Therefore, if you own U.S. bonds, the BOJ’s action is a positive.

What To Watch Today

Earnings

Economics

Market Trading Update

The good news is that the market rallied again yesterday, giving the market sentiment a bit of a boost. We are not out of the woods yet, with the S&P still trading below its 200-DMA. The target for this initial rally is 4200. At that level, consider taking profits and rebalancing risks as needed. There is a chunk of resistance between the 200-DMA and the 50-DMA, which will limit upside over the next month. With the FOMC meeting announcement today, we could see a good bit of volatility depending on how “hawkish” or “dovish” the message is from Mr. Powell.

With the oversold condition improving and the MACD indicator flattening out, I suspect we have some decent risk/reward parameters over the next month. However, as is always the case, never take anything for granted until proven.

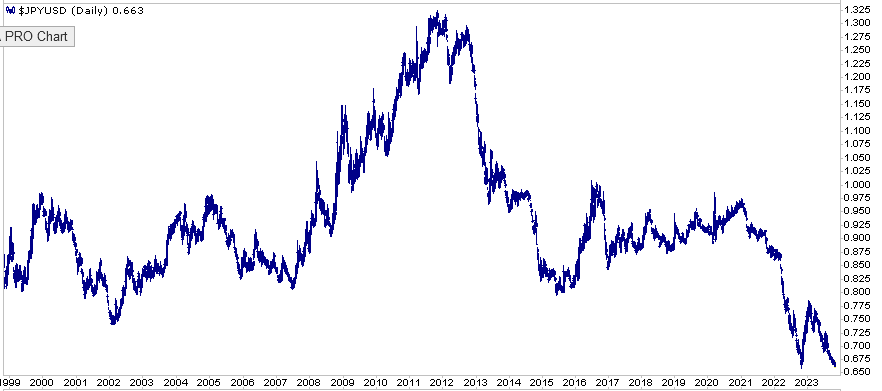

The Yen And Treasury Bonds

The graph in our lead shows the yield on 10-year Japanese notes approaching 1%. The first graph below shows the yen trading at 25-year lows. Consequently, the BOJ is reaching a point where they must decide on capping yields or supporting the currency. They seem to be favoring their currency.

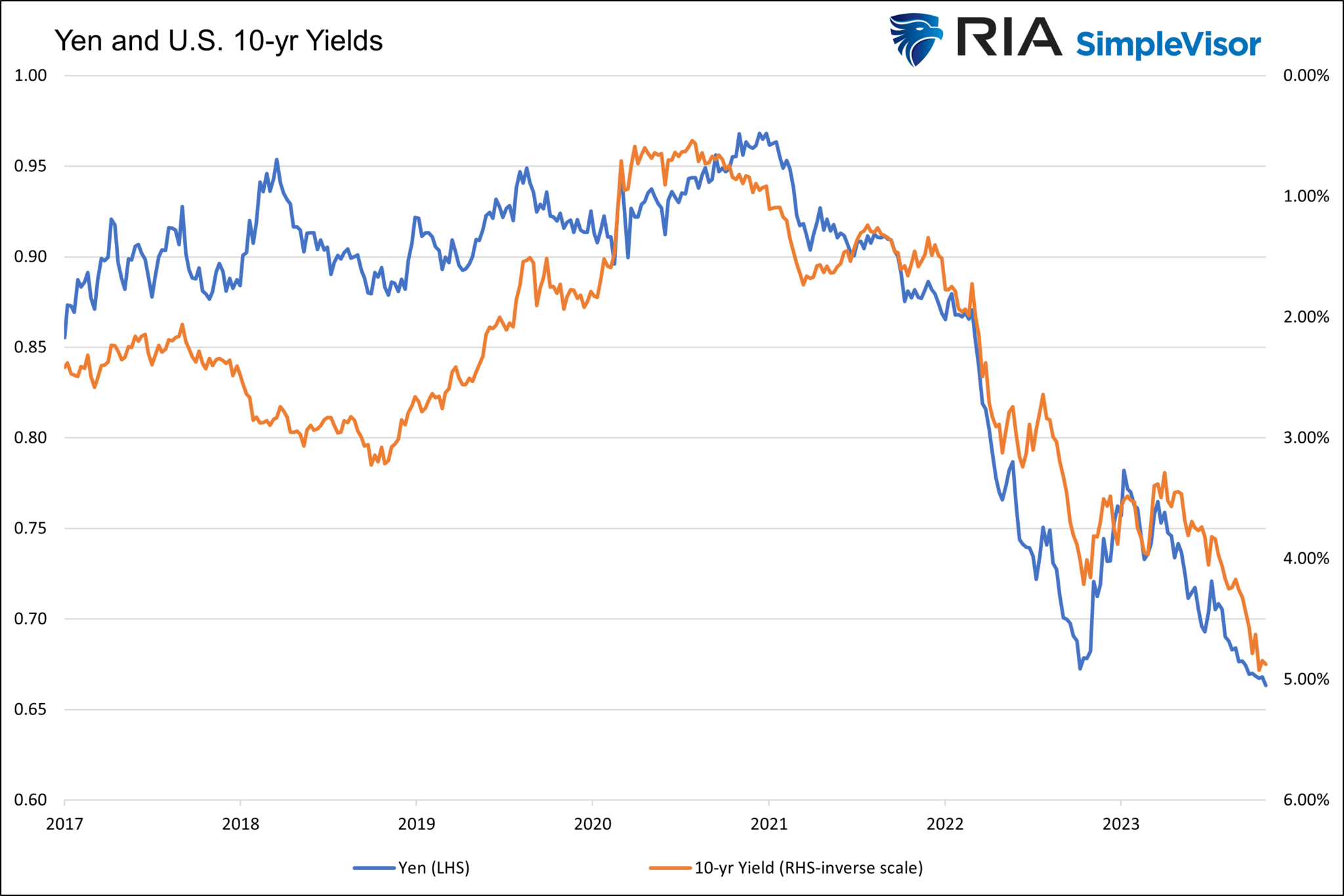

As discussed in the intro, the yen and U.S. Treasury yields have a strong inverse relationship. When the yen declines, U.S. yields tend to rise and vice versa. If, in fact, the BOJ is drawing a line in the sand for their currency, might U.S. yields start to decline?

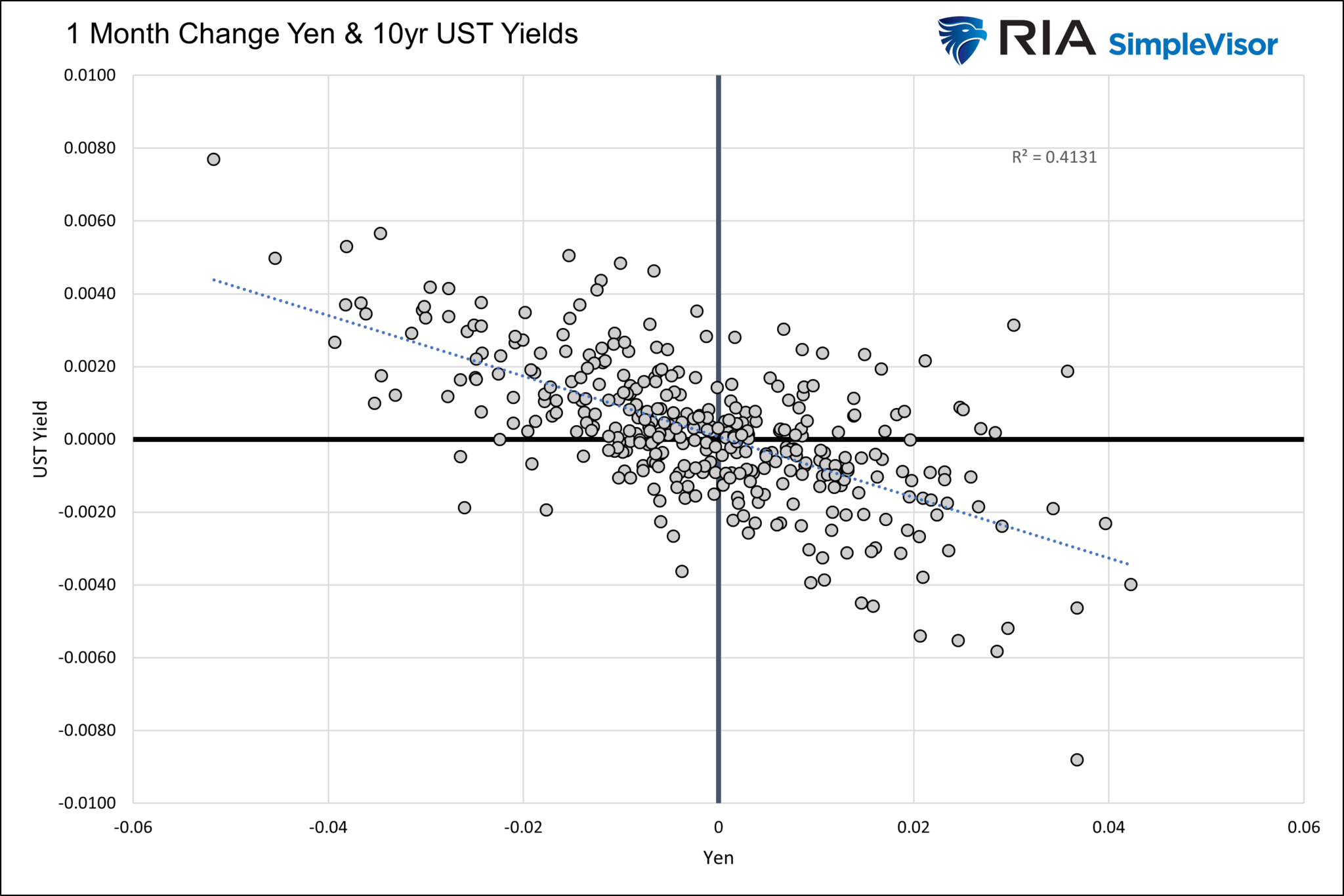

The second graph below charts the yen and the yield on the UST 10-year note. The scale for the ten-year note yield is inverse to show the relationship better. In addition, the third scatter plot compares one-month changes in yields and the yen. Again, the relationship is robust.

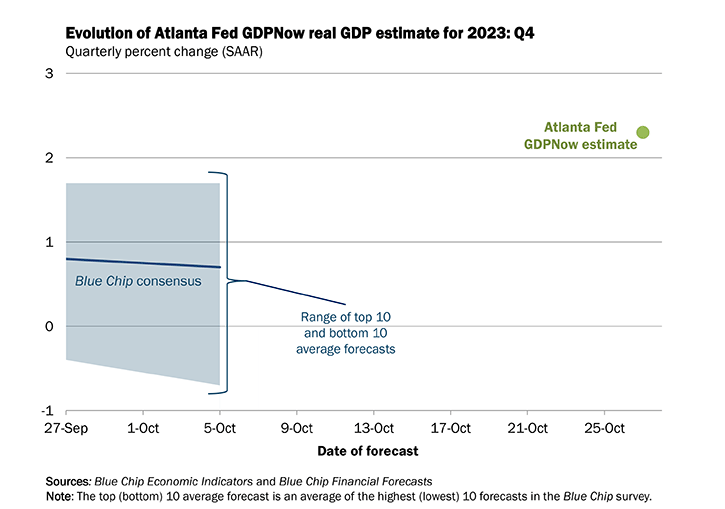

The Atlanta Fed Q4 GDPNow Is Out

The Atlanta Fed’s GDPNow forecast for the third quarter GDP was running well above economists’ models all quarter. While the Fed’s final forecast was a little high at 5.4% versus the actual reading of 4.9%, they were among the few that predicted such strong economic growth. With the fourth quarter now a month old, we turn to their model to see what Q4 may hold in store. As the graph below shows, the GDPNow’s first estimate for the fourth quarter is for the growth rate to slow to a more normal 2.3%.

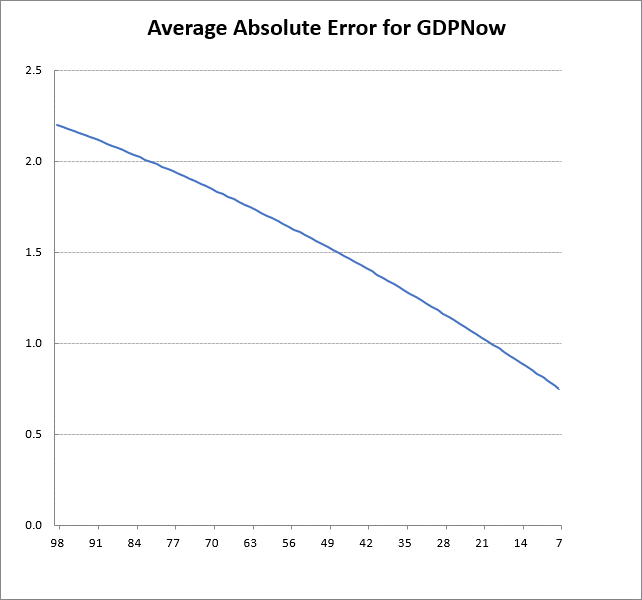

The GDPNow forecast improves as data is released throughout the quarter. The second graph from the Atlanta Fed shows the average error declines as the quarter progresses. The initial forecast is off by 2.2% on average, but it narrows considerably to .75% by their final forecast.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.