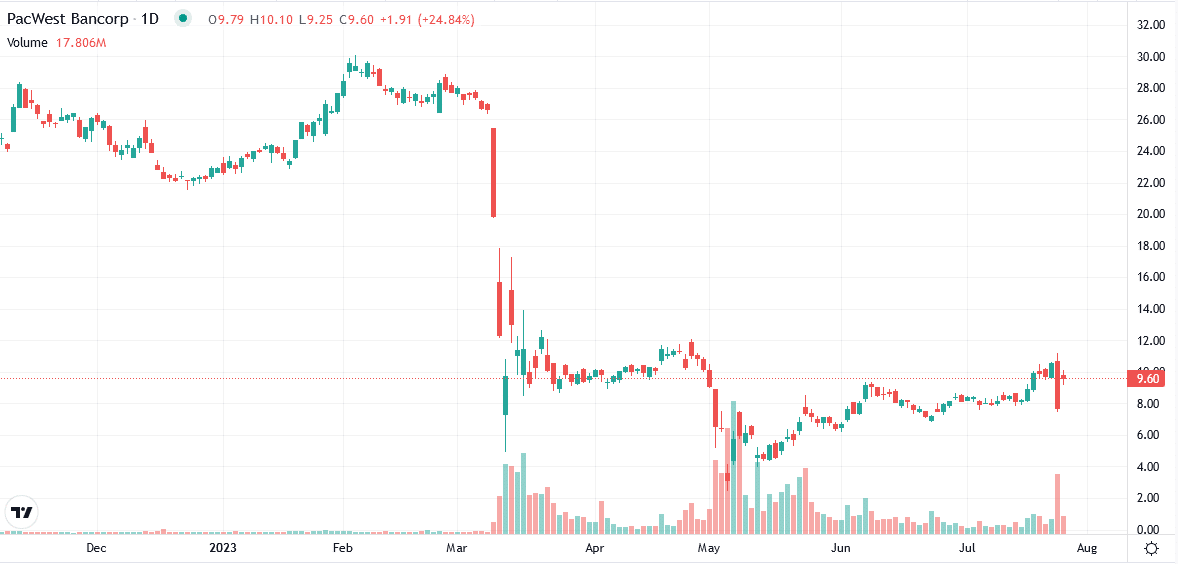

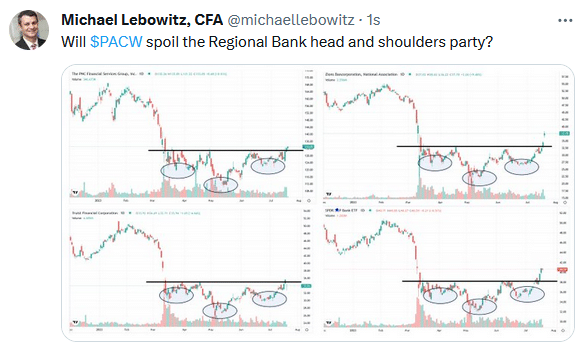

Remember PacWest? Following the demise of Silicon Valley, Silvergate, and Signature banks in March, PacWest Bank was on the ropes. Many investors feared it would be the next domino to fall and other larger regional banks may follow, thus worsening the banking crisis. PacWest shares hit a low price of $2.48 on May 4th, well off the $30 it traded in early February. Since that point, PacWest shares and other regional banks have traded much better. The Federal Reserve’s actions appeared to have worked, and PacWest shares were starting to make up lost ground. For more on recent price action in regional banks, check out our Commentary from July 21, 2023, and the Tweet of the Day below.

After peaking at $10.67 Tuesday morning, PacWest shareholders got stung. The stock closed Tuesday at $7.69, down over 25%. The reason for the sharp and sudden selloff was an announcement that PacWest’s management is in discussions to be bought by Banc of California. Fortunately, as more merger details were released, the stock recouped much of the decline. Typically, a buyout is good news as it demands a premium to current prices. However, the lack of a buyout premium speaks to continued problems with PacWest. There does not appear to be too much concern in the broader banking sectors, as regional banks are generally flat since the news was released.

What To Watch Today

Market Trading Update

The Fed Raises Rates as Expected

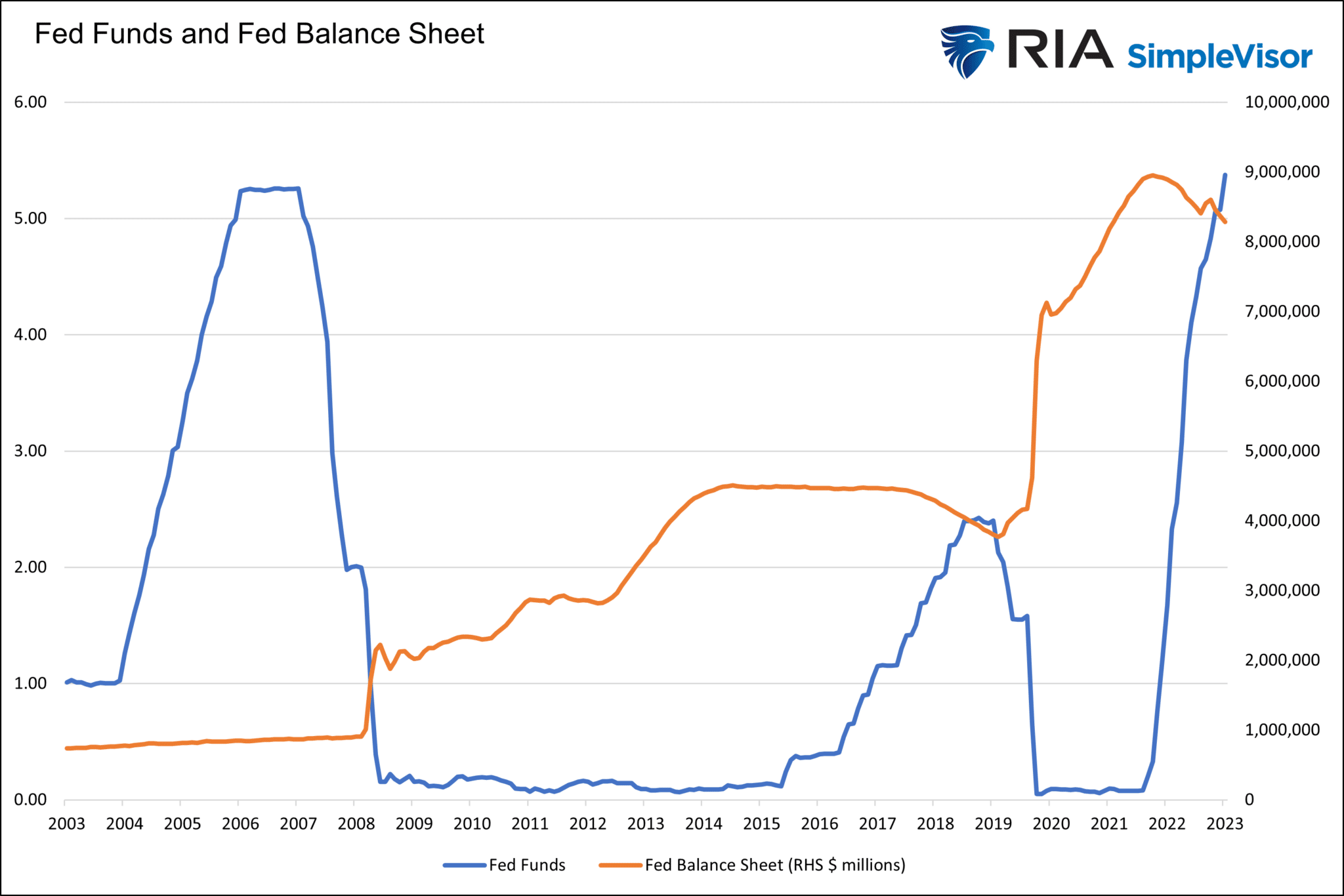

To no one’s surprise, the Fed raised rates by 25bps to 5.25-5.50%. The Fed Funds rate is now the highest since 2001. The statement following the FOMC meeting was largely unchanged from the prior statement. While the Fed did as everyone expected, the unknown remains what comes next. Following the meeting, Fed Funds Futures imply a 35% the Fed will hike again at the November 1 meeting. At the same time, it’s pricing in a 21% chance the first rate cut will occur at the January 31, 2024, meeting. The press conference did little to shine any new light on future policy.

Press Conference Highlights

Listed below are a few talking points and quotes from Jerome Powell’s press conference:

- “The process of getting inflation to 2% has a long way to go.”

- No decision was made on whether to hike rates again. They will go on a “meeting to meeting” basis regarding future actions. In other words, inflation and employment data will weigh heavily on the Fed’s decision-making. Powell reiterated the Fed will have two employment reports and two CPI reports before the next meeting.

- A reporter asked Powell if growth continues at its robust pace, is it a problem because it’s inflationary? His reply-“At the margins, stronger growth could lead to higher inflation.” Consequently, continued strength may lead to more rate hikes unless inflation falls further.

- Powell is happy about the June CPI data but wants to see it continue before pausing rate hikes. If the trend continues in July and August, we have likely seen our last rate hike for the cycle.

- Powell acknowledges the increasing risk they have done too much already. It appears the Fed would like to stop hiking. But, at the same time, they want to make sure the market understands it will do whatever it takes to get “inflation under control.”

- Due to the uncertainty of the situation, they will provide less forward guidance.

- “Lags can be long and variable.”

- “We can be patient and resolute as we watch it unfold.”

- “We do have a shot at a soft landing.” But “it’s a long way from assured.”

- “We don’t see ourselves getting back to 2% inflation or anywhere close until 2025.” – He also alluded the Fed could cut rates but continue QT. Stocks gave up ground on these final statements.

The Money Supply Continues to Tumble

Economist Steven Anastasiou wrote a thoughtful piece about the money supply. As his graph below highlights, money supply, as measured by M1 and M2, is down on a year-over-year basis. In both cases, their annual change is the most negative since at least 1960. More stunning, M2 growth has never been negative until now. M2 includes small bank deposits leaving the banking system to money market funds for higher yields. M1 doesn’t include these deposits.

Steven lays out three reasons we should expect these trends to continue. He writes:

- The Fed’s QT acts to mechanically reduce bank deposits, lowering both M1 and M2.

- The Fed’s aggressive tightening is reducing the growth in bank credit (which is now on the verge of turning YoY negative). This is being driven by banks selling their securities holdings (which allows them to raise cash to cover deposit outflows) and by a reduction in loan & lease growth.

- The Fed’s aggressive interest rate increases have resulted in money moving to areas where it can earn higher interest. This impacts M1 more than M2, which is why the M1 money supply is declining at a much faster rate than M2.

He summarizes the importance of recent money supply trends as follows:

Ultimately, just as the enormous surge in the money supply drove an artificial increase in demand and eventually created high inflation, the current large declines in M1 and M2 will pull the economy in the opposite direction. This means that falling nominal demand, and deflation, are the bigger medium-term risks for the US economy.

Tweet of the Day

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.