Outflows from bond ETFs, such as TLT, have been tremendous over the last two months. ETFs, unlike mutual funds, allow dealers to redeem shares for the underlying securities and vice versa. The exchanges most often occur when the demand to buy or sell the ETF is high, thus creating a small arbitrage for the dealer. Investors frequently associate strong inflows with higher ETF prices and outflows with weaker performance. While at times that is certainly true, other times, it’s a false indicator. For instance, as the graph of TLT below shows, fund inflows were at record-high levels in 2022 as TLT sold off precipitously.

Bonds are out of favor, and as shown below, TLT, the 20-year U.S. Treasury bond ETF, has seen record outflows. There are numerous ways to interpret the graph. Our take is that much of the recent decline is tax-related. With stocks gaining 40+% over the last two years, TLT is one of the few investor holdings that experienced a loss over the period. Therefore, investors looking to offset tax gains with losses were likely to sell TLT. Some TLT investors were probably selling TLT but buying Treasury bonds to maintain their bond exposure. Thus, selling the ETF and buying bonds created an arbitrage for dealers. That partially explains the large outflows from the ETF. However, some were undoubtedly due to selling pressure in bonds and bond ETFs like TLT.

For those interpreting the outflows as bearish, we offer up advice from legendary investor Sir John Templeton:

“The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

What To Watch Today

Earnings

Economy

Market Trading Update

As discussed yesterday, January’s market performance has historically set the tone for the year.

“Since 1950, when all three January indicators (The Santa Claus Rally (SCR), First Five Days (FFD) and the full-month January Barometer (JB)) are up, the S&P 500 was up 90.6% of the time (29 out of 32 years) with an average gain of 17.7%. When one or more of the Trifecta is down, in this case, the SCR, the year is up 59.5% of the time (25 of 42) with a paltry average gain of 2.9%.” – Stocktraders Almanac.

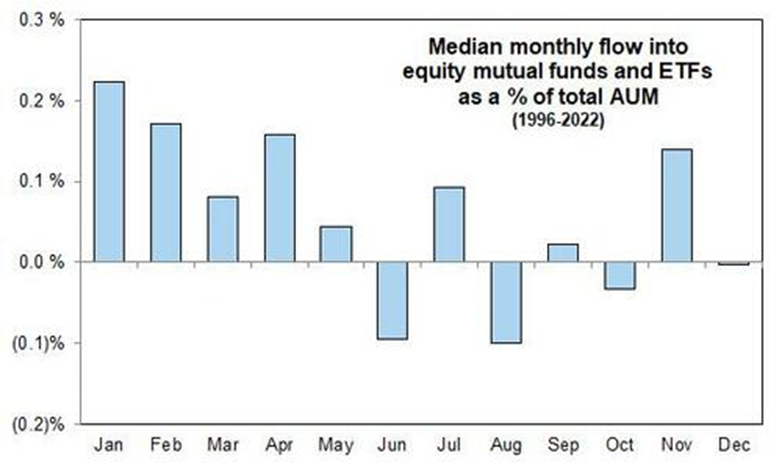

Additional market support will also be available over the next few weeks. First, the “January Effect” started Monday as portfolio managers returned from the holidays. January is the single most significant month of the year for inflows.

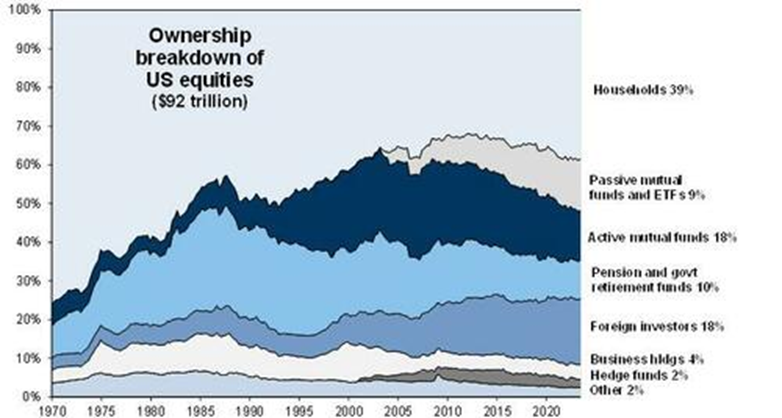

Secondly, given that households own 39% of the equities in the $92 trillion U.S. equity market, 18% of all mutual funds, and 9% of ETFs, the weakness in December was potentially related to tax loss selling to offset gains. However, the 31-day window to avoid violating the tax-loss rule will expire throughout January, allowing investors to return positions to portfolios.

As a reminder, when investors add $1 to an ETF, more than 0.34 cents goes into just seven (7) stocks, increasing those asset prices. Such creates a feedback loop of rising prices, attracting more dollars into those same ETFs fueling higher prices.

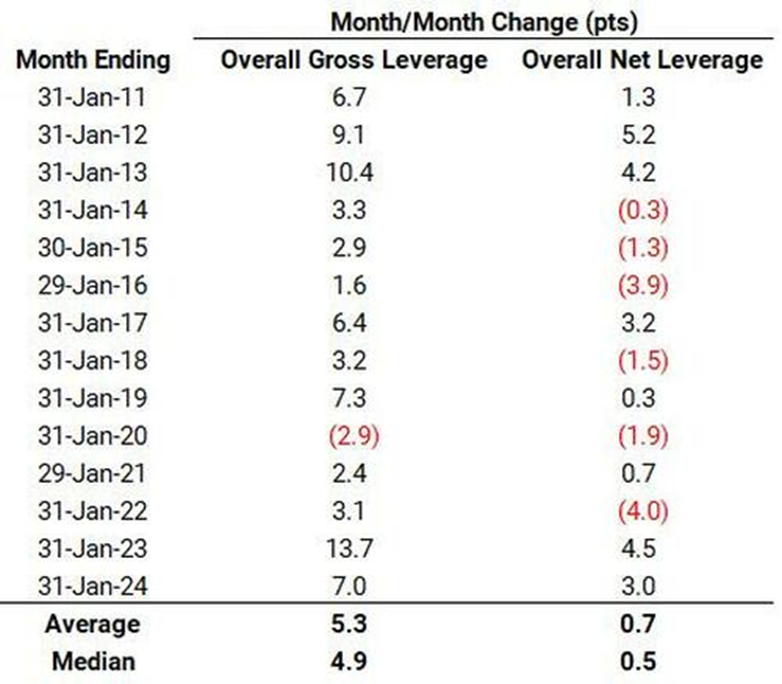

Lastly, all hedge funds typically re-lever their gross exposure in January. In 13 of the last 14 January months, overall gross leverage increased, supporting rising asset prices.

After the selloff in December, the market is in a good position to rally into the inauguration. However, once January is over, it will likely pay to become more cautious starting in February. Performance in election years tends to be weak following the inauguration as the new President begins to implement policies. Given the demand for President Trump to follow through on immigration reform, tariffs, and deficit reduction, how the market interprets the introduction of those policies could increase market volatility.

We expect to remain biased toward large-capitalization stocks during the month. However, as February approaches, rebalancing risk will likely be prudent.

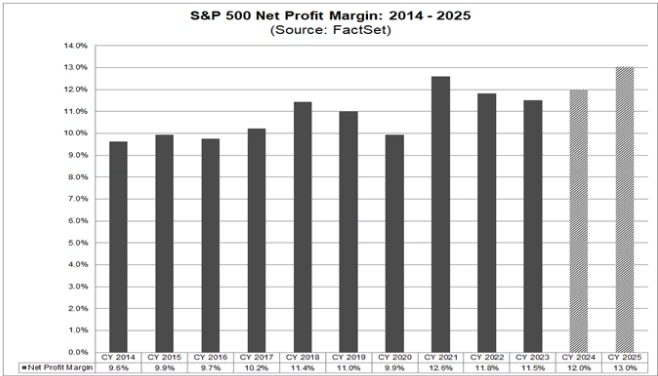

Record Profit Margins Drive Earnings Expectations

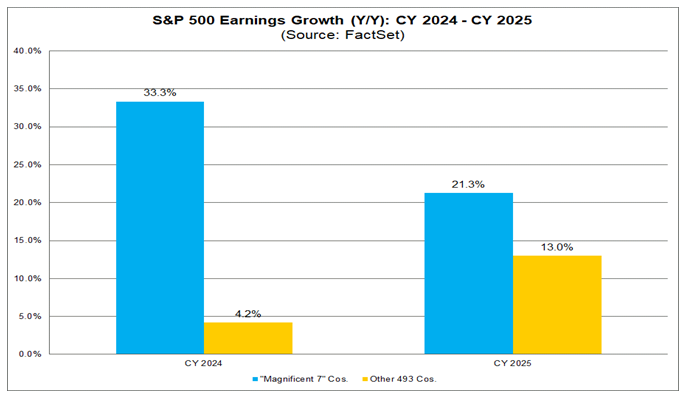

FactSet estimates that S&P 500 earnings will grow by 15% in 2025. The lofty expectations are partly because they think corporate margins will increase further into record territory. The driver of margin growth has been the exceptional growth of the Magnificent Seven stocks. As the first graph shows, the seven stocks had collective earnings growth of 33%, compared to a paltry 4% for the remaining companies. However, this year, FactSet forecasts earnings growth will slow for the seven stocks but will increase appreciably for the remainder.

We have doubts about earnings growth and record margins for most companies. Consider that revenue growth outside of stimulus-fed 2021 has averaged less than 5%. It’s hard to produce 15% earnings with 5% sales growth unless margins increase. Furthermore, with inflation slowing and the Fed maintaining restrictive policy, the economy may likely slow, making increasing profits on those revenues difficult. Conversely, if the economy remains strong, inflation will remain sticky. Thus, higher interest expenses will weigh on margins and consumers’ spending ability, reducing corporate margins.

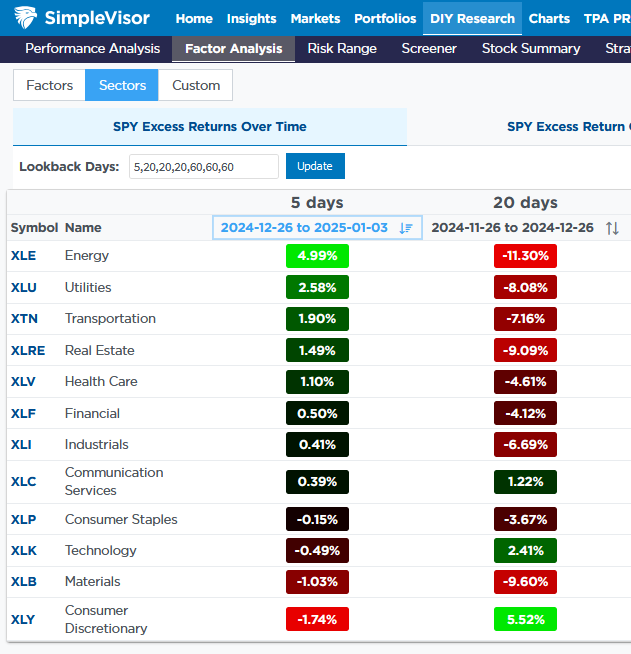

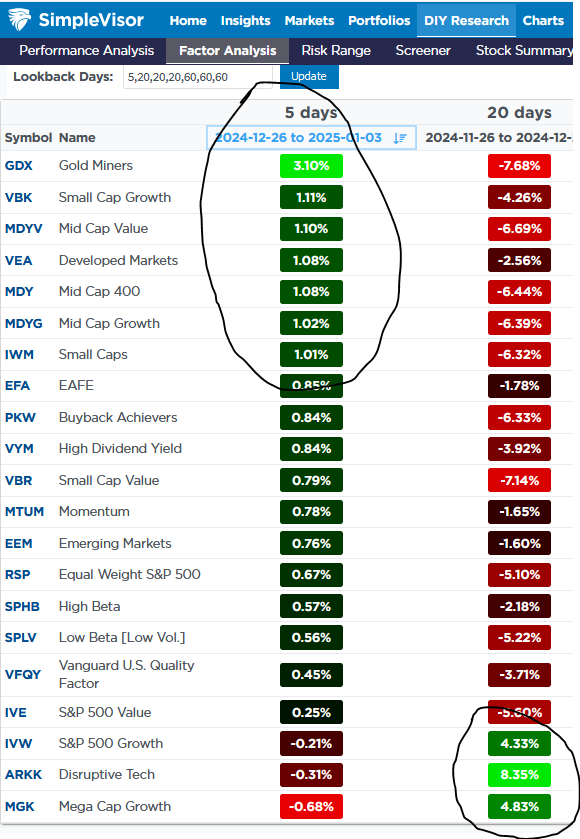

Breadth Recovers

The first couple of days of 2025 and the last few days of 2024 saw the horrendous market breadth of the previous two months reverse somewhat. The first SimpleVisor table below shows that energy stocks beat the S&P 500 by 5% over the last days after trailing the index by over 11% in the 20 days before. Conversely, discretionary stocks, led primarily by Tesla, were the worst-performing sector over the last five days after a strong outperformance in December.

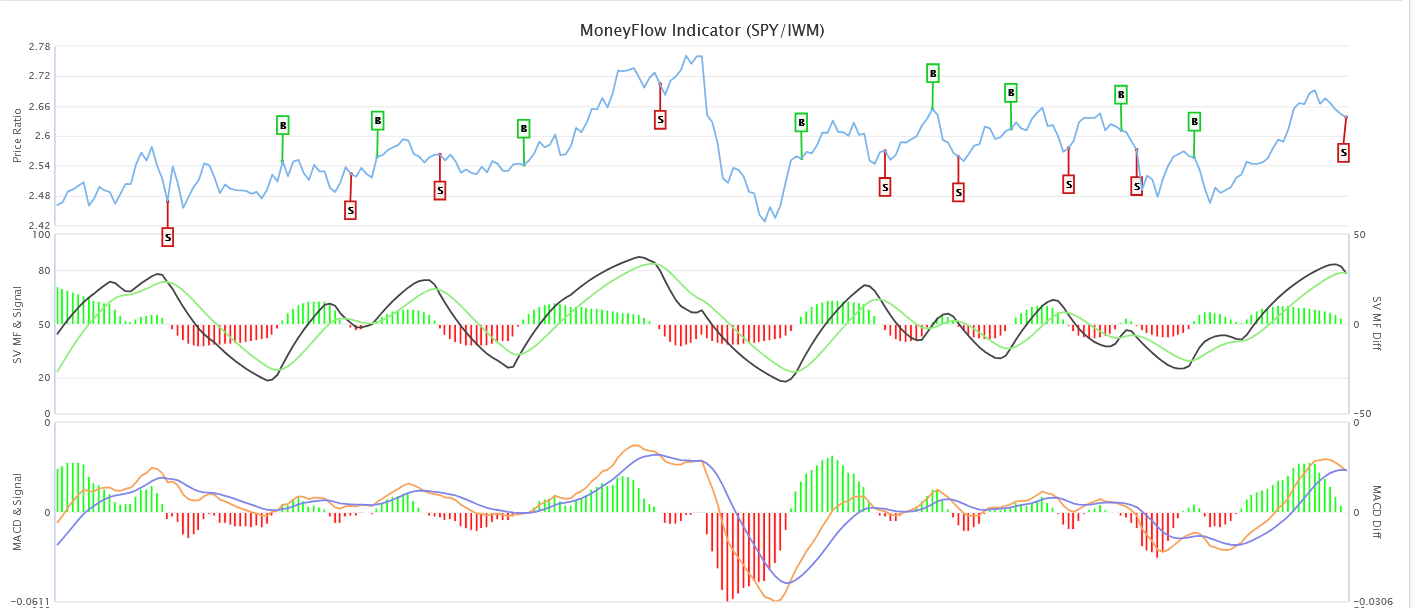

We share the third graph below to help us assess whether the breadth reversal can continue. It charts the ratio of XLY to XLE and a few key technical indicators of the ratio. It shows the ratio has been sliding due to the recent outperformance of energy versus discretionary. The bearish crossing of the MACD did a good job of projecting the change in performance. Those indicators are nearing zero, a turning point over the last year. Thus, if the trends of 2024 continue, we might expect the breadth reversal to only last another week or so.

However, if the market is entering a new regime, the outperformance of the cyclical sectors and small/mid-cap factors could continue. Furthermore, as shown in the fourth graph, the ratio of large cap to small stocks and its indicators are now flashing a bearish turn signal, suggesting the breadth reversal could last longer than a week or two.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.