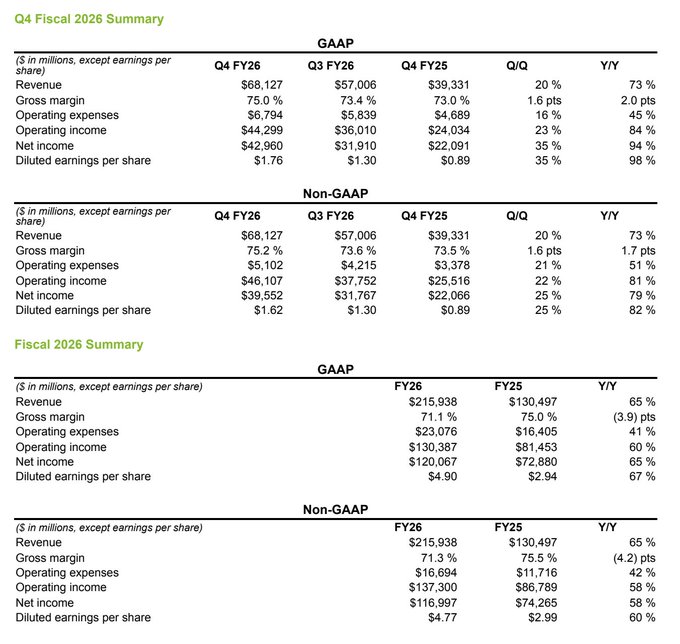

Yet again, Nvidia delivers another incredible earnings report, reinforcing that the AI investment boom continues. As we show below, they posted annual revenue growth of of 73%, handily beating Wall Street forecasts. Most importantly, strong earnings and robust forward guidance confirm that their customers continue to aggressively expand AI infrastructure. Nvidia delivers the critical computing backbone behind the global AI arms race. Think of them effectively as a toll collector on one of the largest capital spending cycles in modern history.

While Nvidia is collecting hefty tolls, i.e., profits, and expects to do so for the foreseeable future, the market is growing increasingly concerned about funding for the AI revolution. The company’s earnings strength comes from unprecedented capital expenditures by a relatively small group of customers financing massive data-center expansion. As economist Carlota Perez wrote about past technological revolutions, and as discussed HERE, innovation itself is rarely the bubble—the financing surrounding innovation often becomes the problem. Nvidia delivers confirmation that AI is transformative, but recent weakness in AI stocks, including a lackluster market response to Nvidia earnings, suggests markets are worried that capital to finance the massive data center expansion is becoming more dear.

“Financial capital is by nature footloose, impatient, and speculative, while production capital is tied to the long-term accumulation of capabilities.” — Carlota Perez, Technological Revolutions and Financial Capital

What To Watch Today

Earnings

- No notable earnings releases

Economy

Market Trading Update

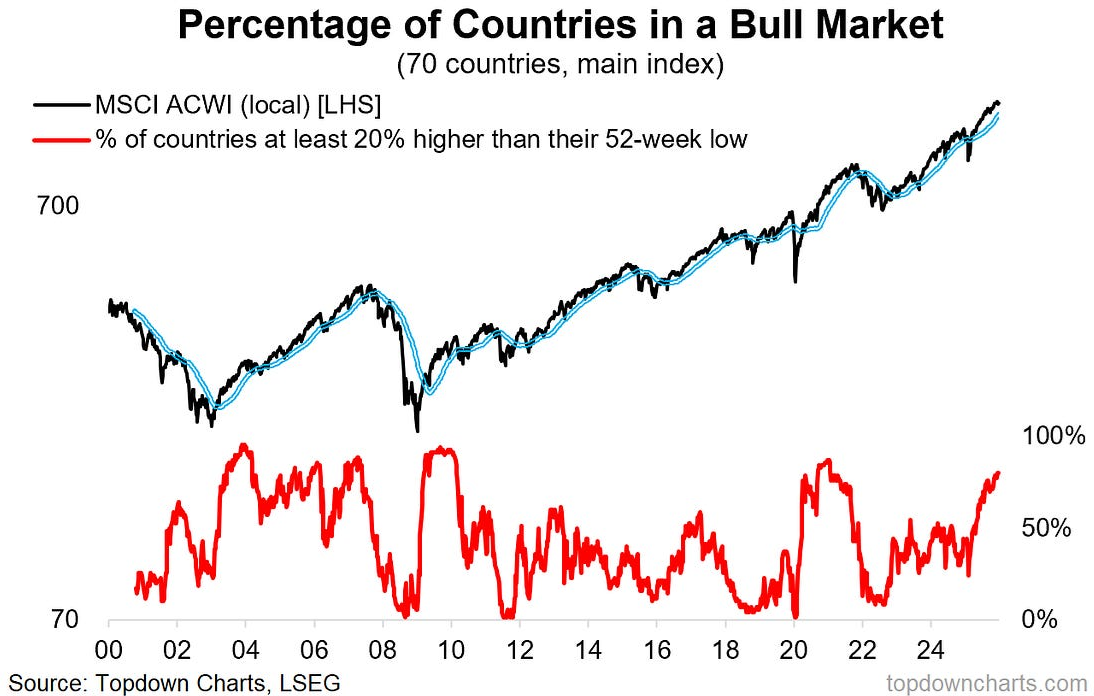

Yesterday, we discussed a recent report from Citadel Securities suggesting the AI impact may not be what much of the mainstream narrative expects. Over the past few days, we have discussed the potential of a market-topping process. While there are no guarantees that such is the case, it is worth paying some attention to. While the broad market has been stuck within an ongoing bull market, the rest of the world is also in a bull market. In other words, just about every asset class is going up at the same time as “too much money continues to chase too few assets.”

“80% of the world is in a Bull Market. Specifically, 80% of the 70 countries we track are up by at least 20% from their 52-week lows. This is a very positive sign, and the chart below shows this peculiar breadth indicator over time (the red line). What’s interesting is a few things. First, this indicator has rarely been above 50% over the past couple of decades (yet, it was steadily north of 50% during the 2000s global equity bull market). Second, when this indicator surges, it is typically a very good sign. Third, by contrast, the time to be concerned is when this indicator peaks and rolls over (no signs of that at the moment).” – TopDown Charts

While this is indeed bullish, you should also note, as he states, that when this indicator reverses, it aligns with short- to intermediate-term corrections. The peaks align with correction periods like 2007, 2010, 2020, and 2021.

Notably, while a healthy market environment “always has a bull market somewhere,” the bigger concern is when there is “bull market everywhere, all at once.” As Sam Stovall once quipped: “If everyone is bullish, who is left to buy?”

While none of this means a correction is imminent, it is at least worth considering the possibility and examining the risk in your portfolio. If you rebalance your risk, and nothing happens, then you continue to make gains. But if you don’t, and a correction does occur, how much damage will you take?

Just something to consider.

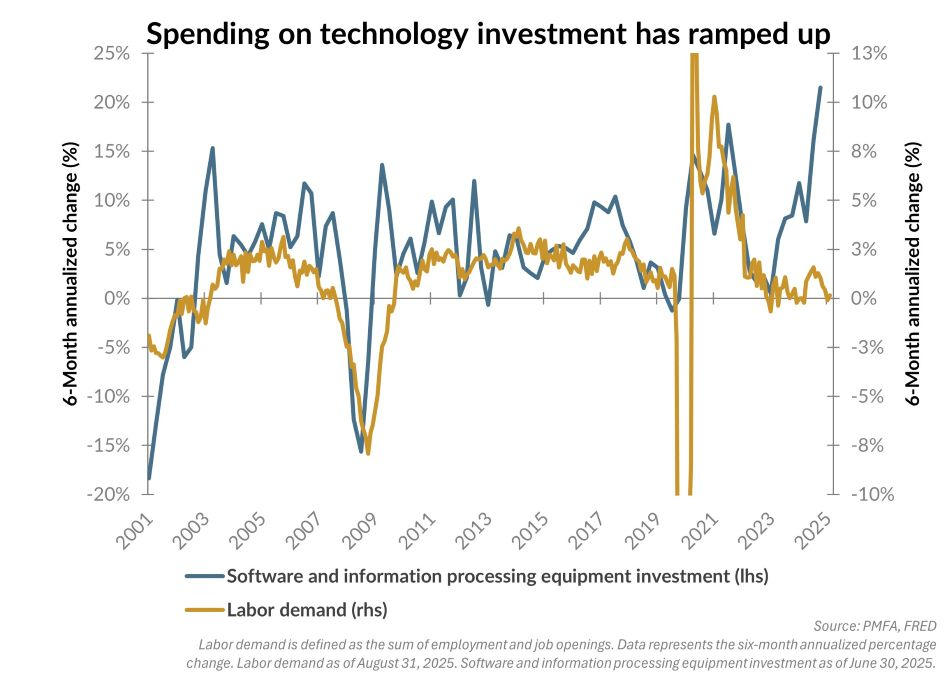

Will AI Flummox The Fed?

There are grave concerns that AI will displace jobs, resulting in a steadily rising unemployment rate. At the same time, the productivity benefits of AI threaten to reduce inflation, quite possibly below the Fed’s 2% target. Those pose a potential problem for the Fed, which is congressionally mandated to maintain “stable prices” and “maximum employment.”

Monetary policy works by adjusting aggregate demand—raising or lowering borrowing costs to slow or stimulate economic activity. However, AI-driven job losses and disinflation or deflation might be much harder to influence than traditional economic activity. Companies adopting AI-driven automation are doing so to improve productivity and reduce labor costs, regardless of interest rate levels. In such an environment, lower rates may stimulate spending or asset prices, but they cannot easily reverse technological substitution. The Fed can influence hiring at the margin, but it cannot prevent firms from replacing tasks that machines or algorithms can perform more efficiently.

In the future, AI may make the Fed’s policy decisions far less effective. For instance, if AI is resulting in a high unemployment rate, easing monetary policy may boost liquidity without meaningfully restoring employment growth. The result could be an unusual policy environment where financial conditions loosen while labor markets remain weak. Such may be a boon to the financial markets, but has little to no impact on the labor market. Similarly, lower rates to boost inflation may only stimulate asset inflation with little impact on real prices.

The graph below depicts the potential problem facing the Fed. There has been a distinct decoupling of business investment and labor demand.

Tweet of the Day

“Want to achieve better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Please subscribe to the daily commentary to receive these updates every morning before the opening bell.

If you found this blog useful, please send it to someone else, share it on social media, or contact us to set up a meeting.